The domestic market remained steady with stable pricing and strong demand. Pruned logs became more plentiful in the domestic market as exporters tried to reduce pruned logs being supplied into China. Quality pruned logs, however, are still keenly sought after.

Export Log Market

September saw a modest appreciation of the kiwi dollar and firming ocean freight rates which offset modest increases in US$ CFR price for export logs.

China demand continues to be solid following the end of the hot season with softwood log demand up to a high level of 61,000 m3 a day in early September. This is higher than seen during 2015 and the first half of 2016.

Inventory has remained steady at 2.5 m m3, representing 42 days’ supply. This makes the market well balanced.

Russian wood supply is emerging as a real threat. The country has a vast resource of forest – standing timber inventory is estimated at 82.1 billion m3, 77% of which is coniferous. Furthermore, despite an official annual total allowable cut of 717 m m3, Russia is only harvesting 205 m m3 (29% of the allowable cut).

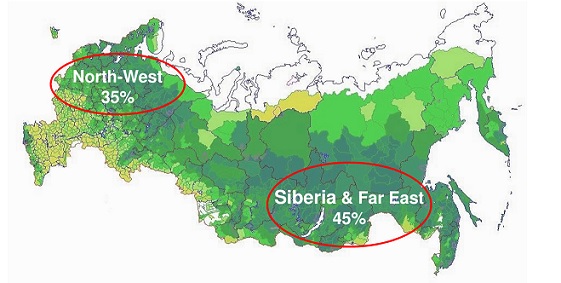

Softwood roundwood volume harvest % for 2014.

The North-West region is substantially increasing lumber exports to China. Source: Ilam Timber.

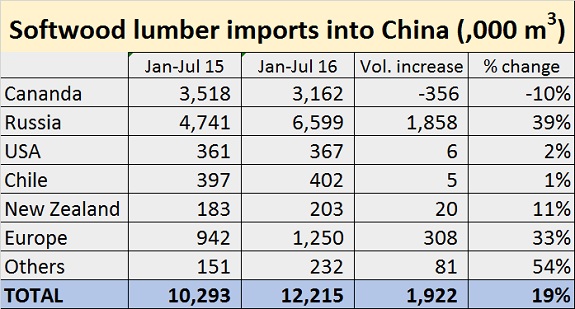

Harvesting is constrained by high costs and limited infrastructure, but a 50% devaluation in the ruble during 2014-15 significantly lifted sales revenues. Also, greater mechanisation is boosting harvesting productivity as is modernisation of the sawmilling industry. In addition very cheap container rates are allowing lumber from timber-rich North-West provinces to economically find its way into China (this region is the source of most of the increase in lumber exports to China this year – see table below).

Russian lumber supply has been at record levels of over 1 m m3 a month since April. The five year trend is for Russian lumber to peak in May and then to reduce through to the end of the year, and ideally we will now see Russian lumber supply tail off.

Source: DANA Limited

The longevity and full extent of the surge in Russian lumber exports to China will be largely influenced by the value of the ruble. Certainly, the massive devaluation has been highly stimulatory. However, modernisation of the sawn timber industry and advances in harvesting productivity will continue to allow Russia to harvest increasing amounts of its vast forest resource and sell lumber into China. Whether this has a significant adverse impact on the market for Radiata pine will depend on China’s ability to continue to increase its demand for softwood logs and lumber.

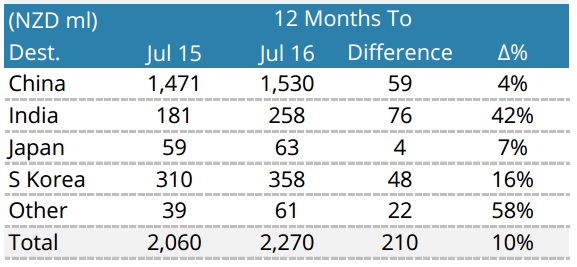

The Indian market is continuing its strong run and Korea and Japan are steady. The Indian market is providing a welcome higher-price option for lower grades at selected ports. The growth in log supply to India this year is clear in the table below. We are expecting India to become an increasingly important market for NZ Radiata pine.

Source: Champion Freight

Domestic Log Market

The rampant New Zealand housing market, spear-headed by Auckland, needs no more air-play in Wood Matters. Short-term it’s beneficial for NZ wood processors and forest owners selling logs (and those fortunate enough to own one or more of those “million dollar” homes in the City of "Sales"). Longer term, however, the bursting of a bulging housing market bubble is about the most potent mechanism to cause significant and sustained pain to an economy and its participants. For those that don’t own a home, any bubble-bursting holds some promise of delivering more affordable homes – if they don’t lose their jobs along the way.

For the time being, however, domestic logs sales are buoyed by strong demand for unpruned and pruned logs and most domestic wood processors are enjoying strong demand for their products both in New Zealand and their key export markets.

Red Stag sawmill, Waipa, Rotorua, has invested in new sawmilling capacity to grow its share of the NZ structural lumber and remanufacturing market. This expansion increases lumber production to 750,000 m3 per annum, making it the biggest sawmiller in Australasia.

It’s great to see more attention to innovative wood-focussed building design emerging in New Zealand. The design approach and leadership for Nelson airports $23m redevelopment must be applauded. The use of wood as the primary building material, and in highly innovative applications, looks set to create not only a compelling aesthetic, but also a showcase for locally grown and manufactured timber. Apparently around 440 m3 of locally grown timber will go into the project which is expected to be completed late 2018. Click here to read more.

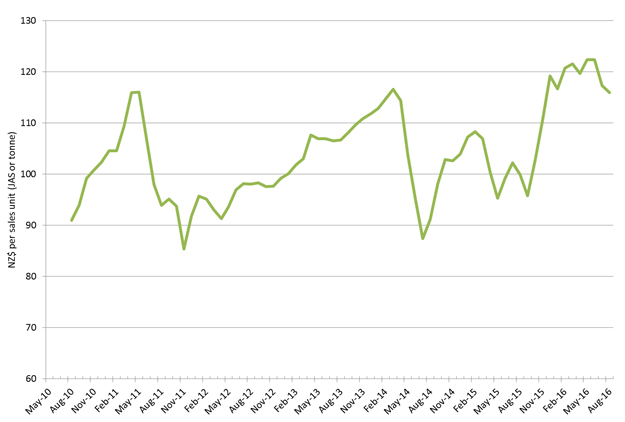

PF Olsen Log Price Index to September 2016

The PF Olsen log price index remained steady in September at $116. The index is $29 higher than its 6-year low of $87 in July 2014 and $11 above the two-year average and $13 above the five-year average.

Basis of Index: This Index is based on prices in the table below weighted in proportions that represent a broad average of log grades produced from a typical pruned forest with an approximate mix of 40% domestic and 60% export supply.

Indicative Average Current Log Prices - September

| Log Grade | $/tonne at mill | $/JAS m3 at wharf | ||||||||

| Sep-16 | Aug-16 | Jul-16 | Jun-16 | May-16 | Sep-16 | Aug-16 | Jul-16 | Jun-16 | May-16 | |

| Pruned (P40) | 192 | 192 | 192 | 196 | 196 | 163 | 165 | 172 | 195 | 195 |

| Structural (S30) | 111 | 110 | 111 | 113 | 112 | |||||

| Structural (S20) | 101 | 100 | 99 | 98 | 98 | |||||

| Export A | 120 | 120 | 120 | 131 | 131 | |||||

| Export K | 115 | 115 | 116 | 124 | 124 | |||||

| Export KI | 102 | 102 | 102 | 112 | 114 | |||||

| Pulp | 50 | 50 | 51 | 51 | 50 | |||||

Note: Actual prices will vary according to regional supply/demand balances, varying cost structures and grade variation. These prices should be used as a guide only.

Market Outlook

Higher log supply volumes are expected from New Zealand through the remainder of this year as we move into more favourable seasonal harvesting conditions and the large early 1990’s plantings are starting to emerge into a reasonably well-priced log market.

The domestic market is expected to continue with strong demand and stable pricing for high quality unpruned domestic logs. Small downward pricing pressure is expected for domestic pruned logs in the fourth quarter (Oct-Dec 2016) on the back of large falls in the export log market. This could manifest itself in a bigger pricing differential for quality which would be a good development for the market.

At current settings for the export market, the outlook is for moderate increases in unpruned log prices and a larger rise in pruned log prices (noting that export pruned logs have fallen over $50 in the past three months).

If the appreciating kiwi dollar trend continues through September, however, it will have a negative impact on NZ$ at-wharf-gate log prices, unless offset by rising US$ CFR prices. Already this month the NZ$:US$ cross rate has increased from a start point of 0.724 to trade at 0.735 at the time of writing. During that period it has traded as high as 0.748. Each 0.01 appreciation in kiwi dollar shaves about NZ$ 3.30/JAS m3 off the NZ$ at-wharf-gate price.

Scion’s latest log price outlook reports a consensus that both pruned and unpruned export logs will rise over the next 6 months and can be read here.

This article is reproduced from PF Olsen's Wood Matters, with permission.

13 Comments

Great! We're exporting raw materials instead of adding value like we could be doing! Something to celebrate I guess

Don't Russian logs grow at a lot slower rate than ours?

If so then wouldn;t it be benificial for Nz to plant more forests now as Russia even with large resources simply won't be able to replace them.

But slower-growing means better quality. Denser than the spongy stuff we grow. That's how it works in Finland, anyway. So NZ logs vs Russian logs isn't necessarily a straight comparison. Do people want to buy something that'll last, or something that'll rot in a few years? And if Russian logs are cheaper plus better ... yeah. That might be a problem.

Those Russian softwoods are mostly Baltic pine or very similar. Quite attractive with distinct annular rings and generally small grown in knots. No stronger or more durable that radiata pine though.

The headline is pretty misleading. New Zealand with 200k m3 against Russia's 6.5 million m3 exports into China and they're suddenly a threat to us? What am I missing?

Perhaps New Zealand is threatened by anyone with more standing wood than us.

Paging Dr Freud.

Well, as you do.

Russia is, at least in part, milling forests grown over permafrost. There is a serious issue when the ground is exposed to the sun and turns to mush in which the trees do not grow again. Canada faces similar issues in the North.

What do they use the land for once logging is completed?

From what I understand of the matter the issue is the top layer of permafrost melts and turn the area into a bog. The soils are also poor anyway. Two effect to global warming are that methane is release as the permafrost melts, and the lost of the trees in one of the worlds largest carbon sinks.

I visited a forestry site in Sweden where they left old trees 30 meters or so apart to self seed after harvesting the rest. It was impressive but these are family owned forestry blocks and have been managed for generations, I wish I could post some photo's for you. I suspect Russia could learn a lot about sustainable forestry.

Our problem is a poor species as our main tree crop, I talk to friends working for large forestry corporations who are now very active in looking at alternatives.

I remember visiting a eucalyptus plantation in Chile that was being milled for a local paper mill near Valdivia, went back a few years later and they had coppiced and we were unable to see the tops from our horses. The growth was astounding.

The photo here is similar to what i saw in Sweden.

http://viavasterbotten.se/wp-content/uploads/2010/02/The-Swedish-Forest…

Could be wrong but aren't Arbogen a part owned NZ co involved in finding new species of trees to grow or something along those lines.

Radiata is the "jack of trades and master of none" species. However it is one of the fastest growing softwoods on the planet resulting in a smaller plantation forest footprint. Swedish forestry is expansive areas and slow growing forests. 60 to 110 year rotations depending on how far north you are so you have to be fairly patient. It is chalk and cheese compared with NZ plantation forestry. Also quite a bit Pinus contorta gone in there in recent decades.

Our radiata is getting worse. Thats just from my own experience. I ran out out of my own pine trees on the farm so was forced to purchase some H3 radiata. The cattle yards I built with 6x2 was at best average, I ended up using some of my own Poplar as it was much much stronger. The sheep yards were a total fail, they have increased the size of timber from the old 5x1 1/4, but it was all covered in knots, soft and unsuitable. They fell apart as we used them and now are a menage of any timber I had lying around, including some Gum, which got a little hard after 5 years in the shed. On one fence it was so knotty that as it dried it twisted so much that 5" nails couldn't hold it so I was forced to wire every rail. now it looks ridiculous as it has all twisted between the posts.

All the timber at the yard appeared to be unpruned framing type, knotted and twisted and very young. I take it we export the good pruned log and sell the poorest quality locally. That top log they take is very young and very soft and I think it should not be used for framing but pulped.

I saw Kiwi pine in the States it was all straight and clean, perhaps from Nelson or Northland where I hear the best pine comes from.

I believe one of the reasons for looking at a more balanced forestry is red rust, amongst other diseases staring to appear. I have seen pine beetle damage from Arizona to Canada and that or Pitch Pine canker would have to be be a disaster in NZ.

http://ipm.ucanr.edu/PMG/PESTNOTES/pn74107.html

I am never going to build a house in NZ out of what passes for building grade timber today, I can no longer use my old pine trees off the farm so I guess I will just have to go steel, earth block or just buy an existing house.

Although they are telling us that Pine today is older, I am able to count and the trees around me are being felled in their very early 20's still.

http://www.nrcan.gc.ca/forests/fire-insects-disturbances/top-insects/13…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.