Tinkering with banks' regulatory capital requirements is small beer in terms of trying to move the dial on bank competition in New Zealand, Reserve Bank (RBNZ) Deputy Governor and General Manager of Financial Stability Christian Hawkesby says.

Speaking to interest.co.nz after the RBNZ released its submission on the Commerce Commission's draft report on competition for personal banking services, Hawkesby said the key point is the RBNZ disagrees with the Commission's analysis in terms of how big a role prudential regulation plays in competition.

The big four banks' economies of scale, and them having operating costs much lower than the small banks, is where the real advantage lies, he says.

"So making marginal changes with the prudential requirements...we just don't think it's going to make a material difference compared to this inherent economies of scale that the bigger banks have," says Hawkesby.

RBNZ doesn't want to relitigate its capital review

The RBNZ undertook its broadest ever review of banks' regulatory capital requirements during the three years between 2017 and 2019 when it faced aggressive push back from the big banks. Capital changes stemming from that review, announced in December 2019, are now being phased in until 2028.

Some aspects of the new capital requirements found support among NZ owned banks, including the softening of the advantage for ANZ NZ, ASB, BNZ and Westpac NZ in using the internal ratings-based (IRB) capital framework. The review also saw the development of a capital instrument for mutual banks, SBS Bank and The Co-operative Bank, that qualifies as Common Equity Tier 1 capital.

The Covid-19 pandemic led to the start date from when the new capital requirements would be phased in delayed twice, ultimately until July 2022. NZ-owned banks expressed some frustration about this, with the then-TSB CEO Donna Cooper telling interest.co.nz in November 2020 the delay meant NZ owned banks would remain disadvantaged against the Australian-owned big four for even longer.

Whilst the Commission suggests the most important of its 16 recommendations is the RBNZ reviewing its prudential capital settings to ensure they're competitively neutral and small banks are better able to compete, the RBNZ clearly doesn't want to relitigate its capital review.

RBNZ doesn't want to discard internationally accepted capital approach 'for little benefit'

Hawkesby says allowing the big four banks to use the IRB capital framework is important. Under the IRB approach, banks set their own models for measuring credit risk exposure which they must get approved by the RBNZ. In contrast the standardised approach used by other banks is set by the RBNZ.

"We operate in an international world where we have the internal ratings based approach, the IRB approach, for large sophisticated financial institutions who do have the resources and the ability to model risks more accurately. And it's a fundamental part of the international approach [to bank regulatory capital requirements] for that to be recognised, and for those institutions that can have a more granular analysis of risk for there to be some incentive for them to apply that. And so it's important that still remains an element to the framework. And so if we remove that capital treatment, we're effectively discarding that internationally accepted approach for little benefit," says Hawkesby.

The Commission's market study into retail banking competition is focusing on deposit accounts and home loans. This means it's digging into the nitty gritty of home loans, with Commission Chairman John Small telling interest.co.nz; "When it comes to well defined categories of home loans, we find it difficult to understand how the risk to a bank changes dramatically [for] a first mortgage on a house with an 80% LVR [loan-to-value ratio]...[It] doesn't seem to us that it's any more risky for Taranaki Savings Bank [TSB] to hold that mortgage than for Westpac, for example."

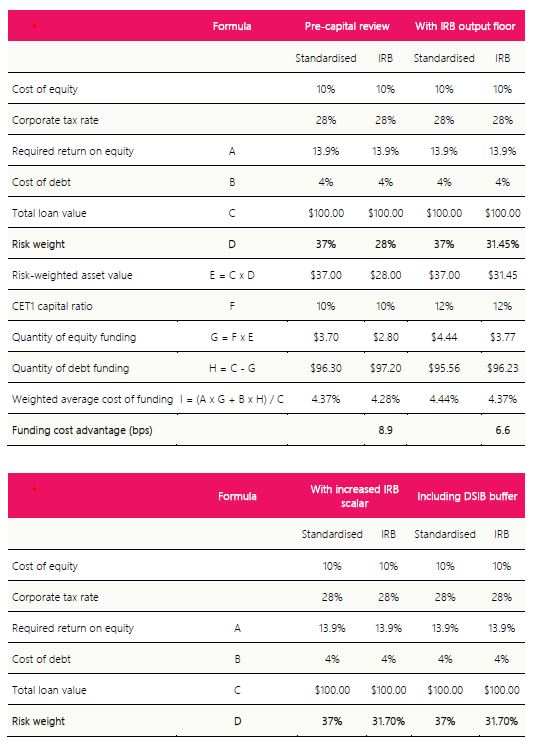

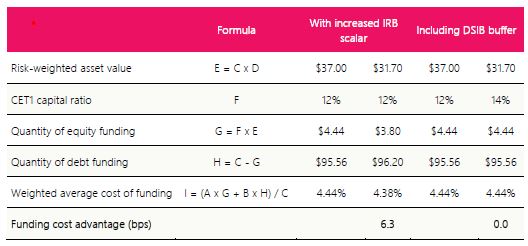

Hawkesby acknowledges that even after the new bank capital requirements are phased in, banks using the standardised capital framework will still have higher risk weight requirements than those using the IRB approach for mortgages. (See table at the foot of this article). Risk weightings are used to link the minimum amount of capital banks must hold, with the risk profile of the bank's lending activities.

"The key point that we would make is just that one around more accurate, more granular, more specific risk modelling needs to be recognised and acknowledged. And so this idea that the same risk is being treated differently is not right in the sense of, these risks are being measured, managed, modelled much more accurately [by IRB banks] so that they should be treated differently," Hawkesby says.

Commerce and Consumer Affairs Minister Andrew Bayly expects to receive the Commission's final report in its market study by August 20, after which the Government will consider its recommendations.

(Also see: RBNZ says difference in average cost of funds between big banks & the rest moving to 'approximately zero'. And see more on the differences between, and background to, the IRB and standardised capital requirements here.

*The tables below come from the RBNZ's submission on the draft report from the Commission's market study on personal banking services.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

9 Comments

Agree the only way to help smaller financial organizations is to have a government funded secondary mortgage market like the USA. Its the only way smaller players can access competitive funding.

'The only way to help smaller financial organizations.....'

Bzzzttt wrong

- Commerce commission has ideas to help (which this article is about)

- Check out Chris's idea below

Am sure there are many more, keep taxpayer money out of this - remember if our dollars get in the ring, they risk being part of a 3 yearly 'changing of the tides'- would you be comfortable with the Greens running such a scheme?

"The big four banks' economies of scale, and them having operating costs much lower than the small banks, is where the real advantage lies, he [Christian Hawkesby] says."

And once again I question why we have a sliding tax scale for personal incomes but still don't have them for corporate incomes?

Surely having lower rates of corporate tax for smaller, growing businesses would be a great way of ensuring competition is fostered?

(I'd also point out that this is done via various schemes overseas.)

Never heard this idea before, but am immediately interested, would be very keen to hear the counter-narrative if anyone has one...

Do you have any thoughts on the tax treatment of losses in this construct, or how this is handled overseas?

Sorry OB, I'm not an accountant. Were I to guess - I'd expect standard GAAP (Generally Accepted Accounting Principles) would apply to losses.

So the choice is between

1) Big banks having a 15% 'per dollar' advantage, and NZ being aligned with overseas practices.

2) NZ being non-aligned with overseas practices, removing a structural advantage for the oligopoly, and de-risking the system a bit.

I really hope #2 wins the day.

The piece about scale bringing operating cost efficiencies is true, but is also a despicable bit of 'whataboutism', how did that come into the conversation?

In the last 5 years were not one of the big four found to have capital regulatory issues? I think the bank was found out by RBNZ. So much for internal risk analysis. Anyone?

The RBNZ is dreaming if it thinks the internal risk models of the big banks are so sophisticated that they can model the risks accurately, the reality is they have no idea where house prices will be next year let alone interest rates, unemployment, default rates, recovery rates etc etc. The advantage that resi mortgages have that makes them practically bullet proof is they benefit from a free put from the RBNZ. Start by making them non-recourse, offer 30-yr fixes and we might get better pricing of the risk

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.