By Gareth Vaughan

ANZ New Zealand is far and away the country's biggest bank. As of September 30 last year it had total assets of $159 billion. As NZ's biggest home lender, these assets included about $76 billion of home loans.

So, under Reserve Bank enforced regulatory capital rules, how much capital is ANZ required to hold against these home loans?

Remember that, as explained in Part 1 of this series, ANZ uses the internal models approach meaning it's allowed to set its own models for measuring credit risk exposure and then get them approved by the Reserve Bank. Also introduced in Part 1 was the concept of risk-weighted assets (RWA), used to work out the minimum amount of regulatory capital a bank must hold. The capital requirement is based on a risk assessment for each type of bank asset.

ANZ's latest disclosure shows, at September 30, it had $76.168 billion of residential mortgages, $15.761 billion of risk weighted exposure and a minimum total capital requirement against these home loans of $1.261 billion. ANZ's risk weight on its housing lending was 19%.

The bank does hold more than its minimum capital requirement. At September 30 ANZ required minimum total capital of $4.487 billion to cover its total credit risk exposure, not just that to housing. However, the bank actually held total capital of $11.857 billion. In Part 3 of this series we'll look at regulatory capital ratios and the composition of bank capital.

In the meantime many bank customers may be surprised to learn that ANZ is technically able, under current bank regulatory capital rules, to hold just $1.261 billion of capital against $76 billion of home loans.

NZ's other big banks - ASB, BNZ and Westpac NZ - are also accredited by the Reserve Bank to use the internal models approach. The risk weightings used by the four differ from one another, with ANZ's risk weightings typically the lowest. The table below shows where the four stood as of their latest disclosure.

| Bank | Housing loans/loans secured by residential mortgages |

Risk weighted exposure |

Minimum capital requirement |

Risk weights |

| ANZ NZ | $76.168 billion | $15.761 billion | $1.261 billion | 19% |

| ASB | $62.387 billion | $18.119 billion | $1.450 billion | 27% |

| BNZ | $43.312 billion | $13.088 billion | $1.047 billion | 30% |

| Westpac NZ | $56.219 billion | $16.562 billion | $1.325 billion | 28% |

*ANZ, BNZ & Westpac figures above as of September 30, ASB as of June 30.

Again as noted in Part 1, other NZ banks must use what's known as the standardised approach where the banks have their credit risk exposure prescribed by the Reserve Bank. This includes NZ-owned banks active in the housing market being Kiwibank, TSB, SBS Bank and The Co-operative Bank.

Through the 2008 introduction of Basel II the minimum risk weight on housing loans under the standardised framework was reduced from 50%, which had applied to all banks up to that point, to 35%. And this is what the NZ-owned lenders work with today.

Thus, as of June 30, Kiwibank had $10.560 billion of home loans at a risk weighting of 35%. This gave risk weighed exposure of $3.696 billion, and a minimum capital requirement of $296 million. The bulk of the balance of Kiwibank's home lending - $5.337 billion, was on a risk weighting of 40%, giving risk weighted exposures of $2.135 billion, and a minimum capital requirement of $171 billion. Kiwibank had a further $1.059 of home lending at risk weights ranging from 50% to 100%, giving risk weighted credit exposures of $657 million, and a minimum capital requirement of $53 million.

Kiwibank's 3% plays ANZ's 1.65%

So all up that leaves Kiwibank with a shade under $17 billion of home loans, $6.488 billion of risk weighted exposure, and a minimum capital requirement of $520 million. That's capital equivalent to about 3.08% of the value of Kiwibank's home loans. ANZ's minimum capital requirement is equivalent to just 1.65% of its home loans.

Meanwhile, a more detailed break-down from The Co-operative Bank shows its home loans to owner-occupiers with loan-to-value ratios (LVRs) under 80% have a risk weight of 35%. At almost $1.6 billion, this includes the vast bulk of the bank's home loans.

Co-operative Bank's loans to owner-occupiers with LVRs between 80% and 90% have a risk weight of 50%, those at LVRs of 90% to 100% have a 75% risk weight, and the small volume with LVRs at 100% have a 100% risk weighting. Co-operative Bank's loans to property investors have a risk weighting of 40% for loans with LVRs below 80%, 70% for LVRs between 80% and 90%, 90% for LVRs between 90% and 100%, and 100% for LVRs of 100%.

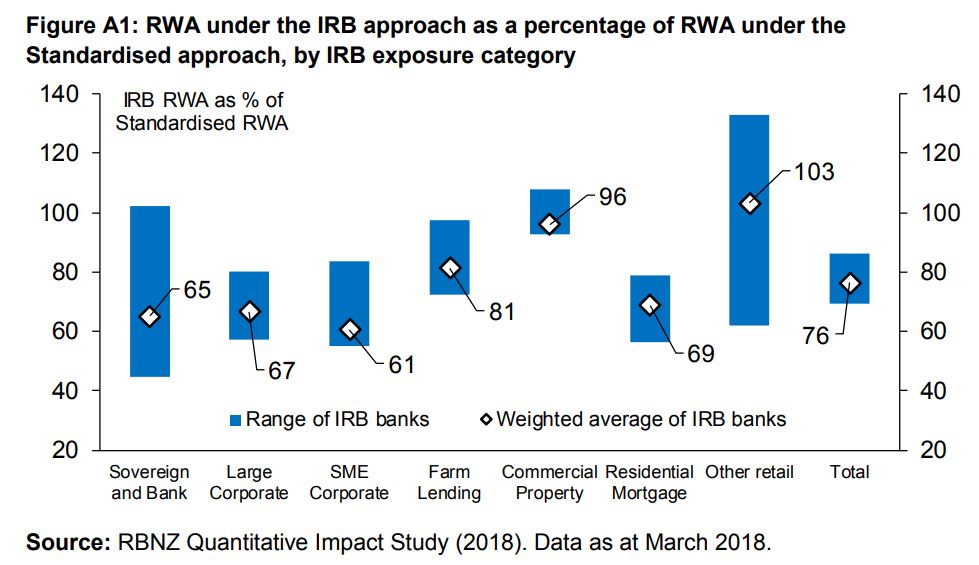

Big four at 69% of standardised banks' residential mortgage RWA

As I reported in December, the Reserve Bank's consultation paper on its proposals to increase bank capital includes a probe of the big four banks' use of the internal models approach. This shows them with RWA equivalent to 69% of the standardised approach used by all other banks for residential mortgages. Across all types of lending combined, ANZ, ASB, BNZ and Westpac have credit risk RWAs of between 67% and 86% of the comparable standardised calculations, with an average of 76%, as shown in the Reserve Bank chart below.

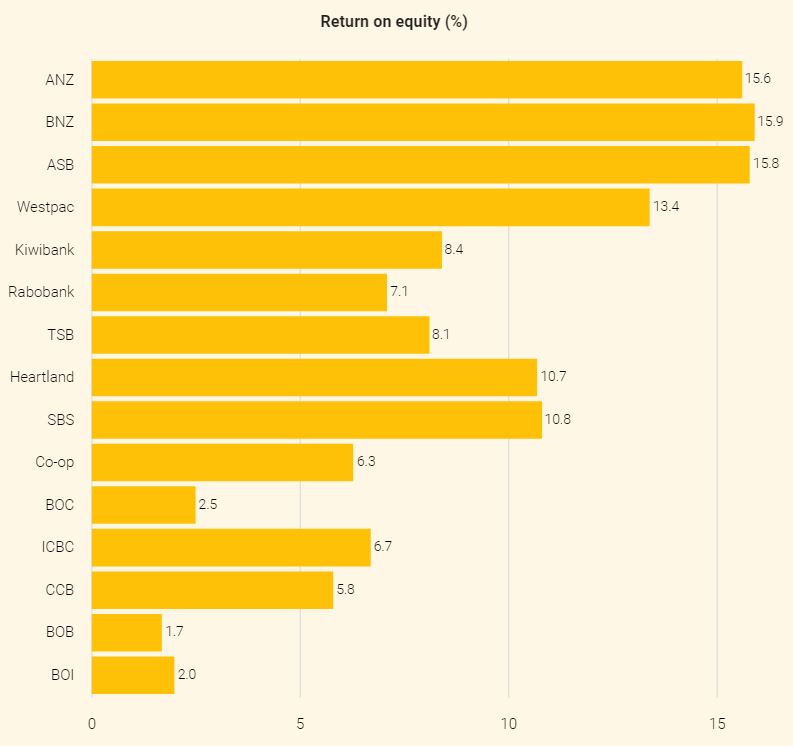

Effectively what this means is the big four banks are able to hold less capital than if they used the standardised approach giving them a profitability advantage over their Kiwi competitors. Or put another way, the Aussie owned banks can use a smaller portion of equity funding for mortgages than standardised banks, which translates into a funding cost advantage. This is a factor in the significantly higher return on equity the Aussie-owned banks generate than their local rivals, as demonstrated in the Reserve Bank September quarter dashboard chart below.

Restraining, but keeping, the internal models approach

Last July the Reserve Bank unveiled a decision for the big four banks to be required to start reporting their RWA and associated credit ratios using both the internal models approach and the standardised approach. The regulator said credit risk models "need to be constrained more" given its experience with the internal models framework. Nonetheless it still appears to buy the argument, at least to some degree, that the internal models approach increases the sensitivity of capital requirements to key individual bank risks.

"On balance, the Reserve Bank prefers an approach that retains IRB [or internal] models in the New Zealand framework, while putting in place restraints on IRB modelling to mitigate the disadvantages of internal modelling [being] competitive neutrality and the opaqueness of internal models," the Reserve Bank said.

"The recent example of the Global Financial Crisis (GFC) also provided strong evidence that in times of stress, market participants and other stakeholders quickly demand simplicity and clarity about the measurement of capital, which is a clear advantage the standardised framework has over the IRB [or internal models] approach."

'Difficult for an external observer to know... whether they are reasonable'

As its capital review has unfolded since March 2017, it has been clear the Reserve Bank has concerns with the internal models approach. In December 2017 it said; "Although banks disclose some information about model outcomes it is difficult for an external observer to know how these were arrived at or whether they are reasonable."

The regulator noted the four banks have different internal definitions of things as simple as the loan origination date for a home loan, making it "difficult to provide consistent data for benchmarking exercises [between banks] as well as to analyse existing portfolios."

"In most cases the variables used in banks’ internal models are readily available but in a significant number of cases important data is implausible, missing, truncated, or inferred from relationships with other variables rather than provided in raw form," the Reserve Bank said.

The banks themselves have also had problems with their internal models, as demonstrated by these interest.co.nz headlines;

RBNZ gives Westpac 18 months to get its capital requirements sorted

BNZ using incorrect unutilised credit limits on some loans for 15 years

ASB's 9-year non-compliance with banking registration rules

And in its latest disclosure statement ANZ notes non-compliance with conditions of its banking registration due to "commitments jointly held" with its Aussie parent "in the risk weighted exposures for the Banking Group for capital adequacy purposes." Rectifying this saw ANZ's Tier 1 capital ratio decrease by 13 basis points to 14.4%, with a $58 million increase in its minimum capital requirement also needed.

A leveller playing field

On a different tack the Reserve Bank believes the staff, systems and compliance costs for the big four banks of running their internal models eats into the risk weighting gap between them and the standardised banks. Thus it argues its proposals detailed in December will largely level the playing field for the NZ owned banks against their Aussie owned rivals. The proposals would see ANZ, ASB, BNZ and Westpac increase the assets they use to determine the minimum amount of regulatory capital they hold to the equivalent of 90% of what's held by other NZ banks, up from about 76% now.

The proposed changes would increase the total RWA value required by the four Aussie owned banks from $251 billion, where they were at March 31 last year, to $290 billion. Note, as of September 30 the big four banks had combined total assets of $447.038 billion and Tier 1 capital, which consists of the likes of paid-up ordinary shares, retained earnings and preferred shares, of $34.247 billion.

As I also reported last year, The Co-operative Bank, SBS Bank and TSB all lobbied for the Reserve Bank to standardise the measurement of risk weighted exposures across all banks, saying this would ensure a level playing field across the banking sector. Kiwibank shareholders the New Zealand Superannuation Fund and Accident Compensation Corporation, have also raised the concept of levelling the capital playing field with the big four banks. And rural lender Rabobank called for a more detailed look at the differences between internal models and standardised approaches in a submission to the Reserve Bank.

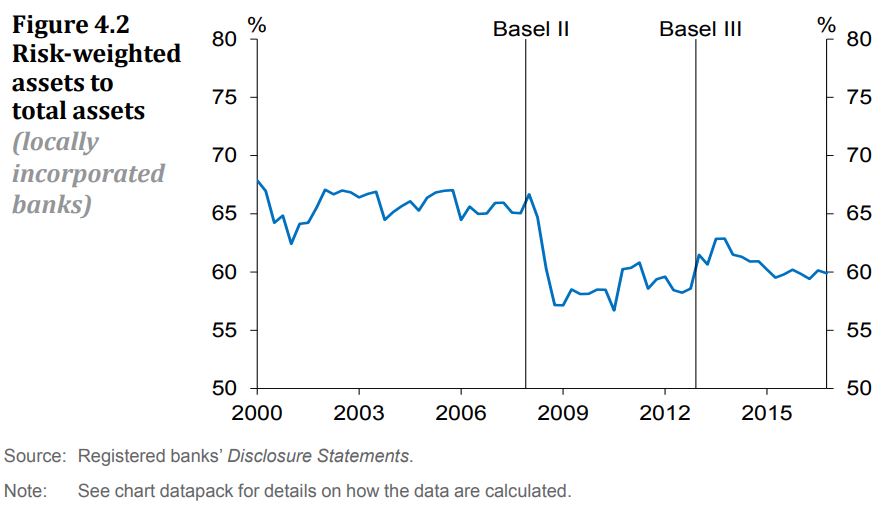

The Basel II impact

The introduction of Basel II in 2008 enabled banks to reduce capital. This is demonstrated by the 2017 Reserve Bank chart below, which highlights a drastic drop in RWA to total assets after Basel II was applied. The post-GFC Basel III subsequently led to a minor increase.

Interestingly, a 2001 submission from then-Reserve Bank Governor Don Brash to the Basel Committee described a 50% risk weighting on residential mortgages as "very conservative" given the "low risk" nature of this form of lending, and that it's secured by residential properties.

With neither the Reserve Bank nor Basel Committee rejecting the internal models approach outright, they are accepting that banks looking at their own data and analysing their risks and own capital needs is a good thing. Nonetheless by reining the internal models approach in, regulators are trying to put the genie back in the bottle to some degree.

The Reserve Bank's proposals to increase bank capital requirements released just before Christmas do not propose to change risk weights used by standardised banks. Thus the 35% minimum for housing loans will stay, remembering this was set at 50% before 2008.

The regulator wants a leveller playing field both among the internal models banks, and between internal models and standardised banks. Thus if standardised banks' home loan risk weights average out at 38%, the Reserve Bank wants banks using internal models to be between about 33% and 36%. This means a significant increase in risk weights used by ANZ in particular.

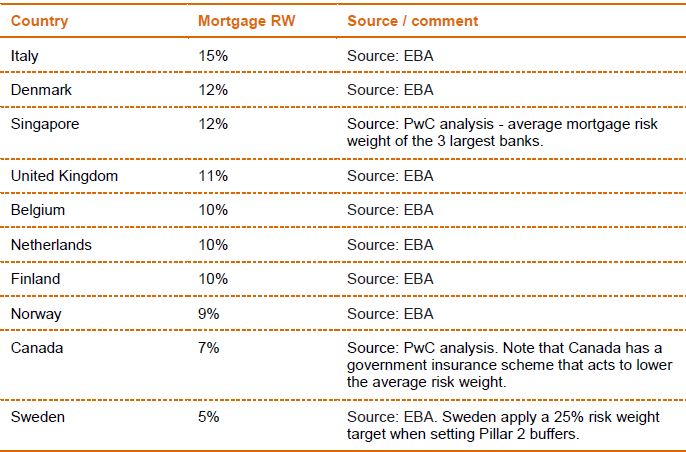

An international comparison

A March 2017 speech from then-Deputy Governor and Head of Financial Stability Grant Spencer kicking off the Reserve Bank's capital review, featured the table below comparing housing loan risk weights in a range of countries with NZ's the highest. Note, the Australian Prudential Regulation Authority has had Australian banks using the internal models approach lift the risk weights on their housing loans to an average of at least 25%.

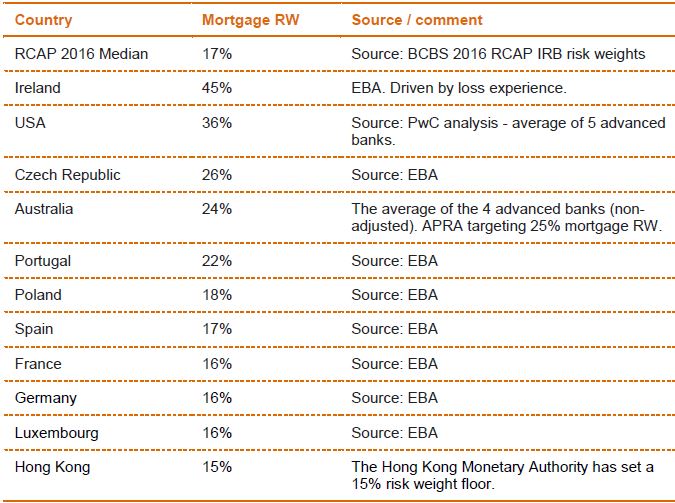

The table below, also comparing a range of international mortgage risk weights, comes from a 2017 PwC report commissioned by bank lobby group the New Zealand Bankers' Association. (Note RCAP stands for the Regulatory Consistency Assessment Programme of the Basel Committee for Banking Supervision, or BCBS).

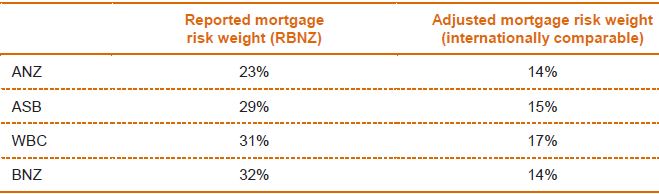

PwC also adjusted the big four NZ banks' risk weights to make them more internationally comparable. This shows them at or below the RCAP median of 17%, below. PwC notes the only countries with materially higher risk weights are either those with a history of significant losses or, in the case of Australia, as a result of specific regulatory supervisor overlays.

Part 3

In Part 3 of this series we'll look at how the owners of NZ's big four banks have fared over the past decade, and how the Reserve Bank's proposal to increase bank capital requirements could impact this, and what it may mean for bank customers. We'll also look at a couple of other key aspects of the Reserve Bank's proposed changes to bank capital requirements.

You can read Part 1 in this series here.

You can read Part 3 in this series here.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

38 Comments

According to the banks the foreign buyer ban is actually having a big impact on sales and prices.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

But the NZ public were previously told that foreign house buyers had no/very little effect.

3 percent.

Little breeders

3 percent on the way in - 20 percent on the way out

Mind you the 3% story was choreographed by National for so long it became cemented in

Then again Coalition haven't done anything to correct the message

Marvellous - doin' a good job

In the June 2018 quarter

"The tax residency status for 41 percent of transfers was unknown."

https://www.stats.govt.nz/news/just-over-3-percent-of-home-transfers-go…

Cant find the September quarter report

Alternatively, a New Zealand tax resident could be an overseas citizen who lives in New Zealand, or a company with overseas owners.

3% yoy over 10 years, 3% + 3% + 3% + 3% + 3% + 3% + 3% + 3% + 3% + 3% = lots

Almost 35% compounded in 10 years yes. I suppose a lot of those buyers would tend to hold too, or sell for a capital gain likely funded by the next buyer taking out a bigger mortgage. Simplified, we're borrowing money to send overseas so that we can have our property back.

I’m not sure your maths is that great. What about the 97% + 97% +97% ...

On the housing front, National told us foreign buyers were buying no more than 3 per cent of the housing market. Now Judith Collins comes out and says the foreign buying ban has having a major effect on the housing market.

And after the complete stuff up by Nick Smith on housing, National have all the answers.

These politicians (from both sides) take the public for complete fools.

'Expensive houses were a sign of success' weren't they? Or are the National party actually just hypocrites? Live by the sword, die by the sword I say...

Hi Itsme. and who votes them in.

You only get what you ask for.

Isn’t the internal risk model just the biggest conflict of interest. Maximizing bank ROE and offloading risk to the public. At the end of the day the bank's equity is all that stands between your bank deposits and an OBR bail in (or more realistically between the governments balance sheet and bank bail out.)

So Gareth has told me that the banks have essentially been able to make up their own rules, and the the playing field for competition is not level. To me this reinforces my argument that the banks must be robustly regulated. the current situation is currently closer to the wild west of no regulation. Capital requirements don't cut it for me. they are not regulation and do little to protect my savings and deposits. Forgive me for I consider myself to be representative of at least a part of the ordinary people in NZ. Although i am debt free, and own my own home, i do not have a lot of savings and cannot afford to lose any. Equally I am only a few years off 65. I expect that as i have little choice about where i place my savings, and all the banks from my perspective look pretty much the same, I have to use them. But i feel that i am highly vulnerable to bank excess's and risky business practices. A part of the capital they talk about are my savings, but they are not protected. I am just an unsecured creditor. I expect more from my Government to protect my interests. i do not expect a free ride. i do expect that the Government will regulate a private industry to protect my interests, and provide a power balance. So far this is not happening.

We all need to have the option of banking with the RBNZ if we wish. Just a Deposit Account. Retail banking will still be done by the commercial banks we see about us today.

Open an Aussie bank account for more insurance.

Don't you have to front up in person, provide your ATO number and a copy of a utility bill with your local Aussie address on it to do that?

Just asking, as that's what some other countries now do.

Just your passport otc for a bank account.

Address details and a billing doc for a CC

Done that. tranferring money between them, even though they are the same bank essentially (CBA, ASB), still incurs fees at a rip off rate.

currencyfair

Ofx.com

Dealing with boomers approaching retirement, many like to gloat about how expensive their houses are but appear ignorant to the fact we have no deposit guarantee in this country. They say ' what do you mean my deposits could disappear'. And I say 'well you like your expensive house don't you'. And its only because of the risk they have to losing cash deposits, that they have an expensive house (banks leveraged position). So would you like to have your cake and eat it too?

Well said, there’s very little protection, and these banks have a lot of exposure to an inflated property market.

"ANZ hold(s) just $1.261 billion of capital against $76 billion of home loans."

That's a ratio of 60:1.

Northern Rock in the UK only got to 55;1 and when the property market shuddered, it went down and the taxpayer had to stump up to save its customers ( think, borrowers in the main, there)

No wonder Adrian is set on changing The System. It needs changing, and fast.....

Is he really, or will it just be hot air that gets lost in a series of committees and consultation?

It's an absolute disgrace that foreign owned banks have an inbuilt regulatory advantage to entrench their market position. Imagine the outcry if this was happening in any other industry? Putting the Big 4 banks on the standardised approach should have been done yesterday.

That's all ignoring the fact that those numbers are downright scary too.

Gareth - Thanks for a bloody good article. You explain things in a way that makes your points easy to understand without dumbing down the message. Having read many RBNZ originated papers they sure could use your ability to deliver a clearer message to the public. The public arena is where the banks will wage their war against changing the rules.

Thanks Wilco.

The root problem with Basel and risk weights:

The root problem is that one cannot extrapolate from moderate one-in-a-hundred type of risk events to the extreme one-in-tens-of-thousands type of risk events that are relevant for solvency. As Riccardo Re-bonato nicely put it, no study of the height of hamsters, however good, will ever give us much sense of the height of giraffes.

Property values in Sydney suburbs have been diminishing by roughly the price of a smashed avocado breakfast every hour.

Newly published figures showed median house prices in parts of these areas dropped by more than A$200,000 (NZ$212,000) over the past year, a fall of A$500-plus a day.

This equated to a drop of at least A$20 every hour, roughly the price of an Aussie cafe favourite, smashed avocado on toast and coffee, a meal once at the centre of the housing affordability debate.

So any investors who are complaining about the drop in property values should heed the advice flippantly dished out to First Home Buyers on the way up?

Dammit IT. So the Sydney house goes to a mortgage sale, and no more daily breakfast out with avocado.

Mind you, young people might be able to afford to buy the house, start a family and have an ordinary like us old folks did.

Now all the foreign buyer bids are gone its a long way down to where the FTB domestic investor bid "was". Naturally those bids are now lower as well due to revised expectations about short term price movements.

The first 10% downturn is always orderly

Very well written. In Table 1 you compare NZ/AU RWA's with other countries but then include an adjustment by PWC that standardises them to international convention. Table 1 suggests our RWA's are higher but this is contradicted later, which is it? thanks

Te Kooti, the figures in table 1 are based on RBNZ rules and come from the RBNZ. The PwC table at the bottom makes adjustments designed to make the NZ risk weights more comparable on an international basis in an attempt to make an apples with apples comparison. Unfortunately calculating risk weights can be a complex business given there are lots of ways to skin the cat, so to speak. Cheers.

Thanks, which is why it's such a good idea for internal model banks to report standard model as well!

the only piece of regulation needed is a noose hanging outside the head office.

Irreversiblechaos, Love your sense of humour

Gareth Vaughan

Thank you. you are producing some excellent articles at present. Very much appreciated.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.