By Gareth Vaughan

Question; Name an industry in New Zealand that's dominated by overseas owned businesses that, thanks to local regulations, are handed a major advantage over their domestically owned competitors?

Answer; Banking.

ANZ NZ, ASB, BNZ and Westpac NZ, our four Australian owned banks, currently enjoy favourable capital positions over their Kiwi owned rivals such as Kiwibank, TSB, SBS Bank, The Co-operative Bank and Heartland Bank.

This is because the Aussie owned banks, which control 88% of NZ banking system assets, are allowed to use what's known as the Internal Ratings Based (IRB) approach to credit risk measurement whilst other NZ banks must use what's known as the standardised approach. The IRB approach is an international banking standard that was imported into NZ by the Reserve Bank in 2008.

It means the big four banks are allowed to set their own models for measuring risk exposure which they must then get approved by the Reserve Bank. In contrast banks using the standardised approach have their credit risk prescribed by the Reserve Bank.

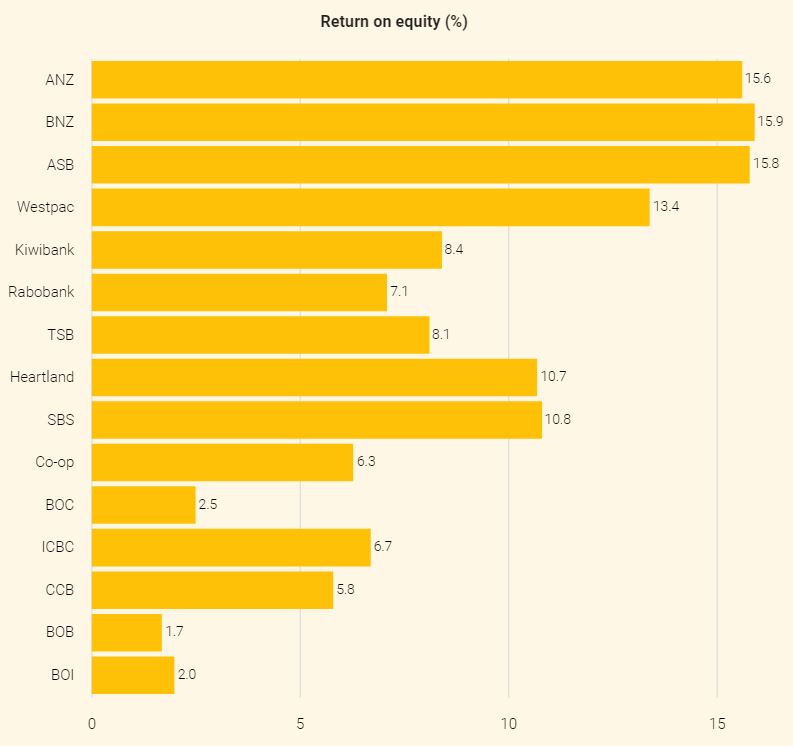

Effectively what this means is the big four banks are able to hold less capital than if they used the standardised approach giving them a profitability advantage over their Kiwi competitors. Or put another way, the Aussie owned banks can use a smaller portion of equity funding for mortgages than standardised banks, which translates into a funding cost advantage. This is a factor in the significantly higher return on equity the Aussie-owned banks generate than their local rivals, as demonstrated in the Reserve Bank September quarter dashboard chart below.

Stark contrast

The differences between the internal and standardised approaches can be stark.

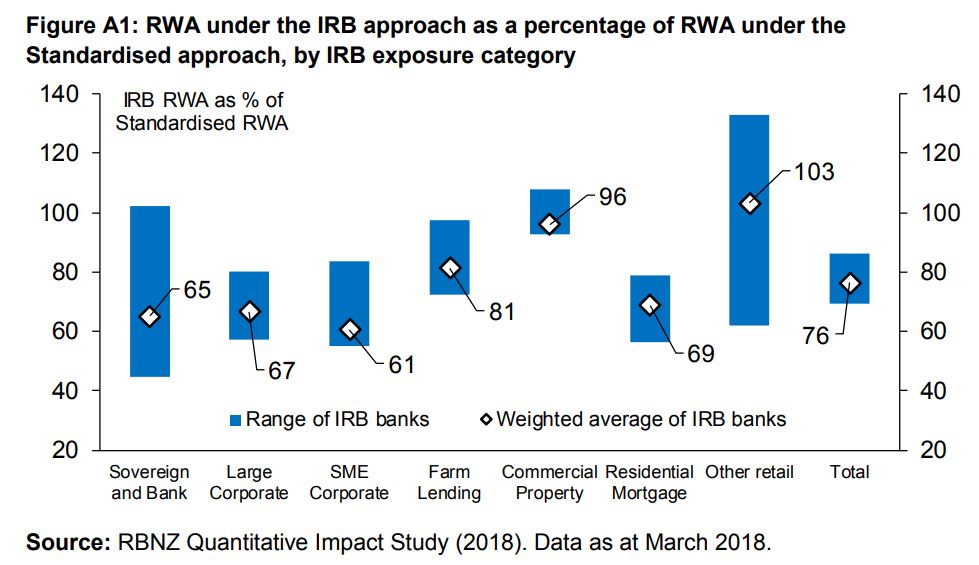

A Reserve Bank probe of the big four banks' use of the IRB approach to credit risk shows them with risk weighted assets (RWA) equivalent to 69% of the standardised approach used by all other banks for residential mortgages. Across all types of lending combined, ANZ, ASB, BNZ and Westpac have credit risk RWAs of between 67% and 86% of the comparable standardised calculations, with an average of 76%.

Risk-weighted assets are used to determine the minimum amount of capital that must be held by banks to reduce the risk of insolvency. The capital requirement is based on a risk assessment for each type of bank asset. There is considerable variation both across different types of loans and across IRB banks.

For example, ANZ NZ's latest General Disclosure Statement shows an exposure weighted risk weight of 19% applied to total residential mortgages of $76.168 billion at September 30. That means the bank's risk weighted exposure was $15.761 billion, and total capital held against its home loans $1.261 billion.

At Kiwibank, the biggest of ANZ's standardised competitors, risk weightings on home loans start at 35%. With $16.956 billion of home loans at June 30, the state owned bank had risk weighted exposure of $6.488 billion, and a minimum capital requirement of $520 million.

That means Kiwibank's minimum capital requirement against almost $17 billion of home loans was equivalent to 3% of that sum. At September 30, ANZ's minimum capital requirement was equivalent to just 1.65% of its more than $76 billion of home loans.

The Reserve Bank's says its proposed changes would increase the total RWA value required by the four Aussie owned banks from $251 billion, where they were at March 31, to $290 billion. Note, as of September 30 the big four had combined total assets of $447.038 billion and Tier 1 capital, which consists of the likes of paid-up ordinary shares, retained earnings and preferred shares, of $34.247 billion.

The chart below comes from the Reserve Bank consultation paper.

Levelling out the playing field

The proposals outlined in the Reserve Bank consultation paper issued on Friday go some way towards evening the playing field for the NZ owned banks against their Aussie owned rivals. That's because the Reserve Bank is proposing to make the Aussie owned banks increase the assets they use to determine the minimum amount of regulatory capital they hold to the equivalent of 90% of what's held by other NZ banks, up from about 76% now.

In a combined submission to the Reserve Bank last year, The Co-operative Bank, SBS Bank and TSB Bank argued the regulator should standardise the measurement of risk weighted exposures across all banks.

"This would result in all banks holding the same level of capital for the same underlying risks, ensuring a level playing field across the banking sector. This will encourage further competition in the banking system, consistent with the Reserve Bank of New Zealand objectives," the three banks argued.

A submission from the New Zealand Superannuation Fund and Accident Compensation Corporation, who in 2016 bought a combined 47% of Kiwibank, also touched on levelling the capital playing field with the big four banks. Remember the Super Fund's CEO at the time was none other than Adrian Orr, who took over as Reserve Bank Governor in March. And Rabobank also called for a more detailed look at the differences between IRB and standardised approaches in its submission.

The Reserve Bank consultation paper also calls for the four Aussie owned banks to hold more capital than their Kiwi rivals because they are systemically important, or too big to fail. It calls for a Tier 1 capital ratio of 16% of RWA for banks deemed systemically important because of their size, and 15% for all other banks. Currently all banks require a minimum Tier 1 capital ratio of 10.5%.

Even though they too will need to increase the amount of capital they hold, this is a victory for the NZ owned banks over their much bigger rivals as, if the Reserve Bank proposals are adopted, they will be operating on a leveller playing field. Not completely level, but better than where it is now.

All banks combined will need $20 bln more capital than they had in March

The Reserve Bank's consultation paper suggests the proposed increase to banks' regulatory capital requirements means NZ banks collectively would need $13.7 billion more Tier 1 capital than they held at March 31. They'll also need to replace $6.3 billion of what's known as Additional Tier 1 capital, which the Reserve Bank says will be non-compliant. Note, Tier 1 is the likes of paid-up ordinary shares and retained earnings. Additional Tier 1 capital is capital instruments such as preferred shares that are continuous given there's no fixed maturity date.

The Reserve Bank is proposing a five-year transition period to the new bank capital regime. The regulator suggests the required capital increase will differ from bank to bank, ranging from between 20% and 60%. This, it says, represents about 70% of the banking sector’s expected profits over the five-year transition period. The biggest of the NZ banks, ANZ NZ, estimates it'll need to find up to $8 billion.

Against this backdrop there's expected to be what the Reserve Bank describes as a "minor" increase in borrowers' interest rates, and potentially a small reduction to Gross Domestic Product. The Reserve Bank argues this will be worth it to make the financial system stronger and safer, including for bank depositors.

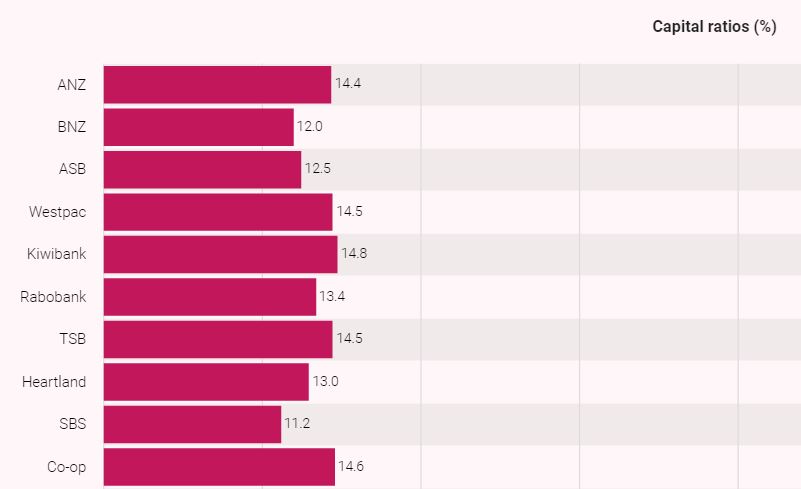

The Reserve Bank dashboard chart below shows banks' Tier 1 capital ratios at September 30. The Reserve Bank proposals would mean a minimum of 16%, as a percentage of RWA, for the big four banks and 15% for the other banks.

Choking on their schooners

NZ's Australian owned banks this year made combined net profit after tax of $5.128 billion, an increase of $433 million, or 9% year-on-year. They paid annual dividends of $3.39 billion. These dividends are set for a dramatic drop if the Reserve Bank proposal becomes reality.

Hence that strange sound you heard on Friday afternoon could have been senior bankers in Sydney and Melbourne choking on their schooners of beer.

The Reserve Bank is seeking submissions by March 29 next year and wants to make final decisions on its bank capital adequacy review, which has been running since March 2017, by June 2019.

So between now and then buckle in and get ready for some serious big bank lobbying, painting doomsday scenarios if the Reserve Bank has its way. Because if the Reserve Bank does get its way life will get a bit tougher at the Kiwi debt farm for the Aussie owned banks.

Crikey, there has already been a report from Macquarie banking analyst Victor German suggesting the Reserve Bank's capital proposals could result in the Aussie banks cutting back the supply of credit to the NZ economy, and potentially even selling their NZ subsidiaries. So fasten your seatbelt. It's going to be a wild ride.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

34 Comments

Dear Aussie Banks Go Home

You suck too many $Billions out of the NZ e con omy every year

That’s not a very nice thing to say. Please apologise at once.

Be careful what you wish for.... you are about to see how that works when they choose to allocate less capital to NZ. Then you will whinge about the high mortgage rates.

Yep, I'm very surprised about the naivety of NL's comment, maybe he was just making a casual comment. I'm not pro OZ at all but the NZ economy cannot exists if all OZ banks were to close shop in NZ tomorrow

I'm not pro OZ at all but the NZ economy cannot exists if all OZ banks were to close shop in NZ tomorrow

You don't see any issue with this fact?

Whether there is an issue with it or not is a separate point.

The fact remains the NZ economy cannot function if all OZ banks exit NZ tomorrow

Just like all landlords sending eviction notices to their clients because of legislation changes, it will never happen, so don't bother worrying about it.

Great, lower house prices via higher interest rates. The stupidly leveraged get punished and the more prudent get rewarded, and reduce borrower debt based enslavement.

Banking looks more and more like a global ponzi of leverage. Trust them to sort it themselves...tui.

Yep, great, no businesses, no jobs anymore in NZ, just wonderful…

Please think about how an economy works before posting

He probably is.. and wants more allocation of capital to productive rather than extractive enterprises.

Yet it seems we were happy to sell....

steven - My father - like a lot of average joe investors hated being forced out of his BNZ shares. There was no happiness.

Sorry but this article is extremely naïve... and I find somewhat short of the normal articles posted on Interest.co.nz. It fails to identify the reason why the internal models regime exists and why it is in fact being pushed even harder overseas.

The simple point is a bank should understand its risks and invest on understanding them to a greater degree. The FRTB regime being implemented in the coming years in all G20 countries will in fact go the opposite way to the RBNZ and require banks to invest heavily in their internal risk systems and having to rely on the standard model when their risk systems don't meet strict performance criteria (and yes, there will be a floor between the internal models and standard as well... but not at 90%).

The RBNZ don't have the skillset to challenge the banks on their current internal models and how they are implemented. That is the issue.

You call it levelling the playing field..... its more like saying all race cars have to run using the same motor mower engine. It wont be efficient, it wont promote investment in risk systems and will in fact make the whole NZ banking system completely prone to the shortcomings of the standard approach.

And yes for the sake of openness, I work for one of these nasty banks who happens to be investing heavily on improving risk systems.... but why would we bother if there is to be no benefit and the capital methodology will be to cater for all.

There is no need to understand your risk, to allocate and price capital efficiently if all loans are put through the same cookie-cutter approach.

There is no further proof needed of the RBNZ's ineptitude than by them focussing on common equity... yup.. we saw how confused they got with Kiwibank's capital issuance.... they have simply put loss absorbing issuance in the too hard basket. Sophisticated investors understand where they are in the capital structure.. pity there is no element of sophistication at the RBNZ.

Agree with you entirely, although I think what you wrote has gone completely over the heads of the typical reader. They’d rather debate the merits of auctions.

..good article with a good counter andyb. That's why we come here.

Andy, I'll be writing more on this. I'm not a fan of the IRB approach or excessive financial engineering in general. I've been consistent on this for some time. For example;

https://www.interest.co.nz/opinion/90935/gareth-vaughan-argues-westpacs-capital-stuff-demonstrates-why-combination-hands-bank

and;

https://www.interest.co.nz/opinion/74349/gareth-vaughan-argues-rbnz-should-tighten-requirements-how-big-4-banks-credit-risk-mea

You say the RBNZ doesn't have the skillset to challenge the big banks on their IRB models. There's plenty of evidence the big banks have struggled with their own models too. For example the Westpac, BNZ and ASB scenarios that feature in the stories below;

Cheers.

Last time I sat through a presentation on moving to an Internal model, the pitch was all about how much money could be saved by reducing capital requirements.. Your are being disingenuous if you are trying to convince anyone these models are about "better risk systems". They are about saving money, and increasing profits.

slams stable door shut

But is the horse inside or has it bolted and left us a steaming pile of fertiliser?

here is a little streaming for your next car trip

a view on the macquarie-fication, infatilisation and predatory banking system.

https://www.youtube.com/watch?v=PZmd2Vz0PvU

Source: http://GunsandButter.org

http://Michael-Hudson.com

We discuss Michael Hudson's book, J is for Junk Economics: A Guide to Reality in an Age of Deception, with an emphasis on the degradation of economic vocabulary that hides the real state of the economy; language affects peoples' perception of reality; history of economic thought no longer taught; classical political economy focused on society's unearned income or rent; the rentier landlord financial class; fictitious capital; the real reforms of the progressive era; classical political economists expected capitalism to evolve into socialism; classical economic concepts of value, price and rent; productive versus extractive economic sectors; public financing of infrastructure a windfall for the private sector; effects of the tax deductibility of interest; monetary policy and the Federal Reserve; economics is political - politics has always been about who is going to get what; National Income Accounting; fiscal policy and Modern Monetary Theory; the three stages of debt leveraging.

A former Wall Street analyst, government adviser, and fierce critic of neoliberal economic order, Hudson is Distinguished Research Professor of Economics at the University of Missouri, Kansas City, and Professor of Economics at Peking University in China. He gives speeches, lectures and presentations all over the world for diverse academic, economic and political audiences. He is the author of many books on the global economy, with a focus on financial history, debt, land tenure and related economic institutions from antiquity to the present.

andyb - the problem with the internal models regime has been that the big banks have been under assessing their risks so were able to leverage their equity and generate greater profits. This was revealed in the RBNZ's review of farm lending a few years ago. The banks had lent too much to a sector with a resultant increase in vulnerability to any downturn in commodity prices.

The other part to my concern is that it is the RBNZ's role to monitor risks of the whole financial system. If each bank runs their own internal modelling of risks but there is no diversity of risk across an industry or sector the system as a whole becomes more vulnerable to one aspect of our economy failing.

Greater profit and bonus lead vs fiscal responsibility and stability...I suggest its been clear whats printed on the motivational posters within banking circles.

Why be responsible if you'll be bailed out if it goes wrong?

Lots of criticism of the internal models approach and how its run by the banks.... I cant disagree.... but I would argue its surely a reason to encourage to the banks to spend more on their models and risk systems... not less.

"Lots of criticism of the internal models approach and how its run by the banks.... I cant disagree.... "

and thats a reason to double down?

The incentives haven't changed, it's still in the banks (short-term) interests to bend the modelling to allow them to lend more with lower capital requirements to make more money. Higher bonuses for managers, higher returns for shareholders.. until it goes tits up and either OBR or a bailout of another sort is called upon.

We should charge the RBNZ which rigorously testing the internal models... and ongoing tests... its what is being proposed elsewhere in the world. P&L backtesting.. and when your models are found to be ineffective in predicting even ordinary profit and losses you force them to use standardised.

Telling the banks to use standard models will mean they understand their own risks less and will simply arbitrage the standard model.

Incentivise the banks to understand their risks better.... and make sure they do so .... a cookie cutter approach where all banks use the RBNZ's default risk weighting of a farm loan, or corporate loan, or financial derivative is extremely dangerous..... what if the RBNZ get the risk weighting wrong?

Andy’s,

Perhaps the incentive for senior management should be the real threat of imprisonment for wrongdoing.the list of malfeasance by banks globally,is long and depressing.

Let’s take the banks back to basics:no wealth management,no insurance,nothing but old-fashioned lending with leverage limited to say 10. These Narrow banks would be secure. All other activities would then be undertaken by investment type banks which would be allowed to pay themselves whatever the market would bear.

No disagreement from me there. No doubt directors understanding of what goes on the in the bank is woefully inadequate and some of the past capital errors should have seen directors held accountable.

I would be happy with that. Regular banks regulated, adequately capitilised, and with an (implicit or explicit) state guarantee. Investment banks reasonably free to do whatever they want, but with the explicit knowledge that if they fall over, their investors get handed a hanky, not a bailout.

Or instead of spending 4 times as much time testing 4 different banks own internal models, plus developing and testing a model for the local/small banks.. they just spend twice as much time developing and testing the one model, and make all banks play in the same sandpit?

Banks of course being free to suggest improvements to the model, the RBNZ can assess and test, and if found acceptable then they can adopt those changes.

Edit: and with the bonus that the RBNZ would be developing and testing its model to maximize stability, not maximize the banks profits. Banks could also of course test the RBNZ model and if they find weakness point it out to the RBNZ. After all, we all want less risk right?

andyb - I am not a bank basher. - you keep mentioning 'incentivise the banks to understand their risks better" but how? To date the incentive was to operate at a lower capital requirement than the non self modeling banks - the trading banks used this opportunity to lower the risk profile of their lending thereby meeting the RBNZ requirements, increasing their profitability - but adding to the vulnerability of our banking system. What a surprise !!

Meanwhile; 'Reserve Bank aims for best regulatory relationships' - https://www.rbnz.govt.nz/news/2018/12/reserve-bank-aims-for-best-regulatory-relationships

I wouldn’t call it a victory, rather a leveling of a playing field that has favoured the Aussie banks over the smaller kiwi ones for nearly 40 years. About time.

That said,it’s not a free lunch for the kiwi owned ones either, the cap on their two will be a challenge for the building mutuals going forward.

And a good time to impose, when credit demand is muted, so risk of pure transfer to interest rates is minimised.

All in all a good result for New Zealand and the tax payer.

Next, make them bring back their services and systems into New Zealand, or get rid of Aussie depositor preference.

16% of the actual loan book? Or 16% of the "adjusted" smoke and mirrors figure?

There are two issues here. First, what level of reserves is sensible. Second, how do we transition to the new rules. There is no reason to compromise on the first issue in order to solve the problems of the second. Just extend the period of adjustment as necessary to achieve the objective.

Alan Greenspan suggested that equity of 20% to 30% of the loan book with no adjustments was probably the only system that would be stable long term.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.