Housing should now be affordable for first home buyers in most parts of the country, even if they are earning average incomes.

Auckland and Tauranga are the only major urban centres where housing is still considered unaffordable for typical first home buyers and even in those centres there is some good news, with affordability levels in both cities steadily improving.

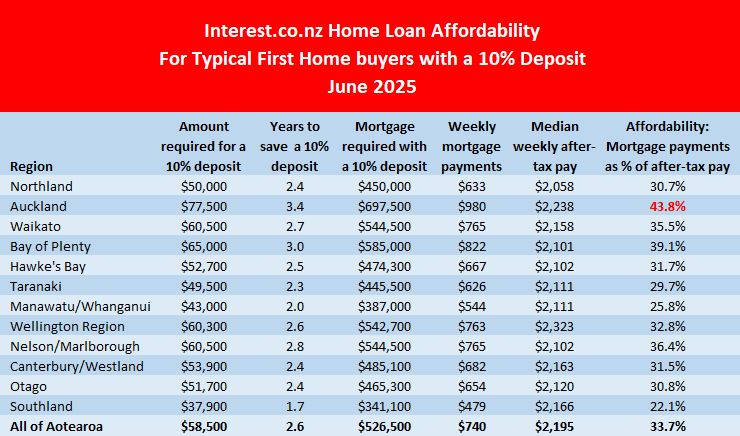

Interest.co.nz measures affordability levels by tracking changes in mortgage interest rates and the REINZ's lower quartile selling prices, to estimate the mortgage payments on entry level housing in all of the main urban districts around the country, and compares that to after-tax incomes based on median wage rates for people aged 25-29, representing couples just starting down the path towards home ownership.

Home ownership is considered unaffordable when the mortgage payments consume more than 40% of a couple's after-tax pay.

At the national level, affordability has been steadily improving since November 2023, when the mortgage payments on a lower quartile-priced home would have consumed 45.8% of a typical first home buying couple's after-tax pay, severely stretching their household budget, especially when other home ownership expenses such as rates, insurance and maintenance are factored in.

But by June this year the situation had improved considerably, with the mortgage payments on a lower quartile-priced home chewing up just a third (33.7%) of a typical first home buying couple's after tax pay, well within affordable limits.

The improvement in affordability was driven by three factors:

- Lower mortgage rates: The average two year fixed rate declined from 7.04% in November 2023 to 4.96% in June this year. This was the main driver of improved affordability.

- Lower house prices: The REINZ's national lower quartile selling price declined slightly from $600,000 in November 2023 to $585,000 in June this year. Although that decline was modest, every little bit helps.

- Slowly rising incomes: Interest.co.nz estimates the combined, median after-tax pay for working couples aged 25-29 (assuming they both work full time) increased from $2043 a week in November 2023 to $2195 in June this year, through a combination of modest increases in pay rates and last year's tax cuts.

All of which adds up to good news for aspiring first home buyers, even if, like everyone else, they are facing general cost of living pressures.

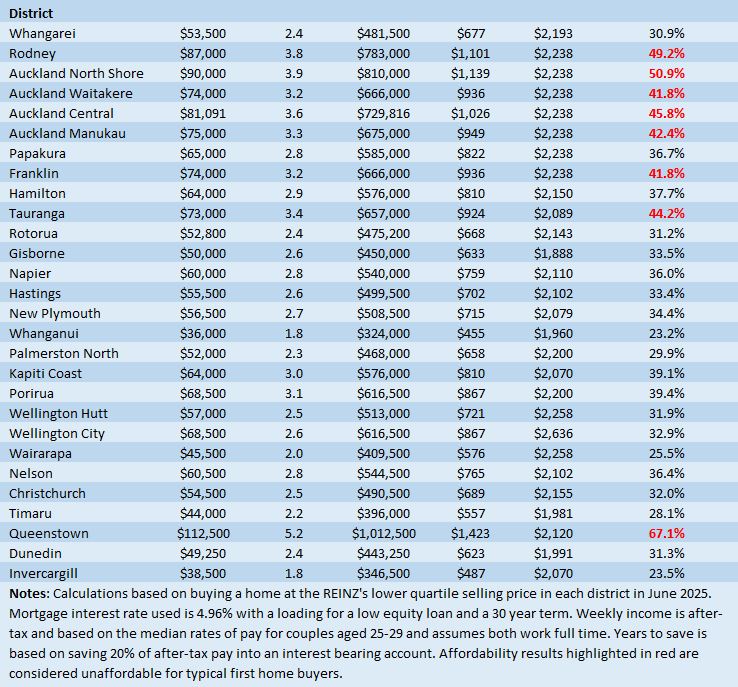

In Auckland, which is still squarely in unaffordable territory, there is also good news for first home buyers.

The REINZ's lower quartile price for the Auckland region has declined from $810,000 in November 2023 to $775,000 in June 2025, while interest.co.nz estimates that after-tax pay for a typical first home buying couple in the region has increased from $2090 a week to $2238 over the same period.

Those changes, combined with lower interest rates, have seen mortgage payments on a lower quartile-priced home in the region purchased with a 10% deposit, decline from 60.4% of take home pay in November 2023 to 43.8% in June 2025, a substantial improvement.

And although most districts within the Auckland region remain within unaffordable territory for first home buyers, Papakura in the south of Auckland remains affordable, with mortgage payment on lower quartile priced home there taking up just 36.7% of typical first home buyers' take home pay, well within affordability limits.

So even though home ownership remains challenging for many, the latest figures show a steadily improving affordability picture around the country.

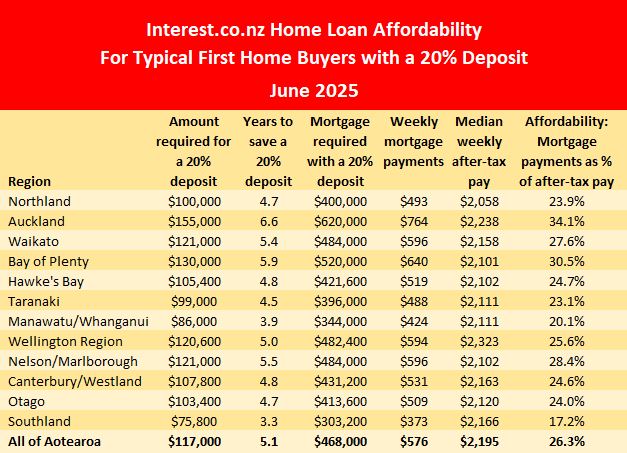

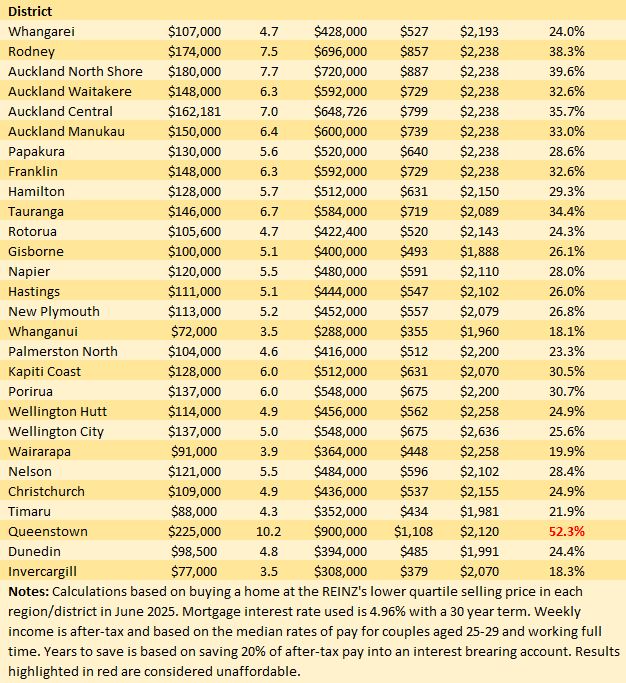

The table below show the main affordability measures for homes purchased at the REINZ's lower quartile price, with either a 10% or 20% deposit, for all significant urban centres around the country, as at June 2025.

The comment stream on this article is now closed.

27 Comments

Affordable is 3 to 5x your earnings. Those paying more, are being duped.

Other factors such as mortgage & income tax rates are key in assessing house affordability.

Imagine what affordable house prices look like at 18% pa interest & 66% marginal tax (50% on earnings >$100/wk). Which I've previously paid.

Paying 55K for the house would be helpfull, at 18% rates......

https://youtu.be/I21OHrjBduQ?si=t6q0WC-WVoIIcSVQ

The animals are informing on the humans, this from a pigeon

Good work Gecko

... be careful what you wish for. The last time average house prices were ~$55k was the mid 1980s, average wage ~$10k pa.

Yes that would have been stressful from a cashflow perspective

From an equity perspective the gain in the 70s and 80s was massive and set that generation up handsomely

Not a sure thing:

https://www.greaterauckland.org.nz/2016/07/11/remember-the-last-time-ho…

We've all had this conversation a few times b4

"by Phoenix (FKA JC) | 15th Jul 25, 9:04pm

There was rapid and massive house price inflation in the 70s and 80s, missing out meant being left behind.

Between 1971 and 1974, real house prices increased by 60%. This rise was driven by a surge in demand, a run-up in immigration, and shortages in builders and materials. After 1974, the sharp rise reversed, with house prices falling in real terms for the rest of the decade. By 1980, real prices had returned to roughly their 1970 level, meaning the decade ended with little net real gain. This was largely due to high inflation, which eroded the apparent dollar value gains."

https://www.interest.co.nz/economy/134218/new-zealand-should-%E2%80%98d…

Forget about real growth rate, as on a nominal basis house prices increased through the roof and so did incomes. A few years of this and it deflated away the size of the mortgage which after a couple of years became small compared to the house value and incomes

Forget about real growth rate, as on a nominal basis house prices increased through the roof and so did incomes

The gold price increased 15x in Kiwi pesos during the 1970s.

The average house price was approx $15K in early 70s and reached approx $25,500 in 1980.

Forgetting about real growth is not wise.

Then by 1985 the average house price increased dramatically to be $80k, then by 1990 $125k - Ka-Ching!

OK. I don't make it a habit to battle with Ponzi cheerleading. Even though the Ponzi didn't really kick off until the late 80s, I will concede.

Regardless, even if you take 1970-1990 as your barometer for the infallibility of the Ponzi, the gold price appreciation in the 70s gives some perspective.

And even though I would be mocked at the BBQs, I think that we need gold as an alternative 'money' yardstick compared to fiat.

its still the same asset with the same market value relative to alternative properties. Price simply reflects money as the medium of exchange, re/devalued by monetary and fiscal policies outside the control of the asset owners.

The early Boomers were born at a fortunate time in history

Home ownership is considered unaffordable when the mortgage payments consume more than 40% of a couple's after-tax pay.

Maybe that should be made more realistic by including rates, insurance and R&M? They are all increasing at a faster rate than mortgage declines.

houses are so cheap, they must be flying out the door !

Cue the gold card holders screaming their rates and insurance are too much, demanding greater rates rebates with the councils while sitting on 2x,3x,4x increase in equity across the span of ownership of their properties. The heart bleeds.

House prices are all very interesting to many but I prefer to get overall housing news from interest. From MSM is that 1/3 of all Auckland houses in the last year failed their final inspection. I rate this as important. Please diversify your housing news.

Timely. My Aussie colleague who thinks about things like affordability says:

When you have coercive control over someone, like the banks do over mortgage holders in Australia, it gets sold to all of us as something else. It’s marketed as an investment, as security.

But think about it: we’re bidding house prices up by paying banks more money, and we’re told that’s a good idea in fact the very best idea (apparently). Apparently, it’s better to overpay for shelter, especially to banks that created the money out of thin air, we need the stress.

Someone who sits in a cubicle in the city demands you pay them for the privilege of sleeping indoors at night. They didn't build the property - they have nothing to do with it.

It’s better, they say, to pay bureaucrats. And that’s what the financial sector really is - financial bureaucrats. We’re expected to thank them for designing systems that indebt us to them, indenture our work to them. That’s the highest form of servitude: to thank your masters for the cage you built.

It’s not even our democracy. The RBA doesn’t answer to the people; it answers to the financial system. And what does the financial system demand? Full employment, not for prosperity, but so everyone can keep servicing debt. And price stability - not to keep food affordable, but to protect loan values. Asset price inflation gives them more of your wages.

They’ll ignore housing inflation entirely, because higher asset prices and low CPI mean you’ll pay more to the bank for longer. That’s the point: low inflation preserves the value of debt, for them - not you.

We are conditioned into the cult from birth. It's all we know, all we can imagine.

Agreed. Big picture its a form of financial enslavement just the control the shelter you enjoy. A global mouse wheel where the productive worker runs ever faster just the enrich the banking system and owners.

According to Chat GPT, the NZ Banks owned by Aussie Banks. Aussie Banks owned by US Banks. Major share holders of US banks are Vanguard, Blackrock, and Statestreet. Those three are the major owners of each other. After that trying to attach actual names of those share holdings get lost inside some opaque legal structure.

It's a rough (and generous) guess but I would think <20% of the population has a basic handle of understanding about all this. I have colleagues who I consider to be astute, intelligent, and informed who don't fully grasp it yet. No fault of their own. They're simply not interested.

I've mentioned here before how much better we could all be if houses only cost 20% of what they do now. That is get rid of loans completely.

Have been laughed at and derided. The cult sees no other way.

The price of houses should be set by what we have/can afford. Not by what banks are prepared to lend as is the case now. Just means we all (even those without loans) get the dubious honours of helping the banks fleece the economy of $7b

Exactly - housing market is/has been financialised. No longer about being a home/shelter/place to raise families/economic and community inclusion, but it has become a product of the banking sector that is marketed and sold and used for financial gain instead of social outcomes.

redcows, you better work out how to get cheaper land and reduce building material cost.

Completely missed the point there Pat

I love the sentiment red... keep it up

100% - RBA and RBNZ are supposed to regulate the banks for the betterment of the country but over the past few decades things have only got worse. The central banks have allowed the retail banks to completely financialise the housing markets. Houses are no longer viewed as assets used by families to create lives and raise children (good social outcomes) - but instead are looked at as financial assets make the banks rich (so the executives can get paid >$1,000,000 for creating a product out of thin air and turning their customers into their weekly slaves for a 30 year period - using a product called a mortgage!)

The bankers' smug answer would be to buy their stocks, especially CBA. And the franking credits are the icing on the cake!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.