By Gareth Vaughan

Cast your mind back to events in global financial markets during 2008. The news was dominated by tales of woe involving US sub-prime mortgages, falling share markets, collateralised debt obligations, worthless AAA credit ratings, a global credit crunch, failing financial institutions and taxpayer funded bailouts in events that became known as the Global Financial Crisis (GFC).

Thus 2008 appears to have been a particularly bad year for bank capital rules to have been liberalised. But that is exactly what happened in New Zealand. Although to be fair to the Reserve Bank, which approved this liberalisation, the timing was the result of a long running international process.

From 2008 the Reserve Bank accredited NZ's big four banks - ANZ, ASB, BNZ and Westpac to use what's known as the internal models approach under the Basel II bank capital adequacy regime. These international bank capital rules were imported via the Basel Committee on Banking Supervision, a Swiss-based group established by the central bank governors of the Group of Ten countries in 1974.

What this 2008 move means is NZ's four Australian owned banks, which today control 88% of NZ banking system assets, are allowed to set their own models for measuring credit risk exposure which they must then get approved by the Reserve Bank. In contrast all other local retail banks, including Kiwibank and TSB, use what's known as the standardised approach where the banks have their credit risk exposure prescribed by the Reserve Bank.

A key result of this is the Aussie owned banks are able to hold less capital, notably against the key lending area of housing loans than their NZ owned counterparts, thus boosting their profitability. But more on that later.

Although the Basel Committee doesn't have formal supervisory authority, it has encouraged convergence towards common supervisory approaches and standards for bank regulation. In 1998 it developed the Basel Capital Accord, or Basel I, to align the capital adequacy requirements applicable to internationally active banks. Prior to this there had been no uniform international regulatory standard for setting bank capital requirements. Subsequently Basel I was updated with the Basel II framework released in 2004, and Basel III in late 2010 in response to the GFC, which left the internal models approach intact.

Why capital matters

Coming with Basel II, the internal models approach was a move away from a one-size-fits-all approach to global bank capital rules. But before delving into the internal models approach, let's remind ourselves why bank capital matters.

As then-Deputy Governor and Head of Financial Stability Grant Spencer put it when kicking off the Reserve Bank's biggest ever review of bank capital requirements in March 2017, which is ongoing, bank capital is an important cushion for the financial system.

"It is the form of funding that stands first in line to absorb any losses that banks may incur. Having sufficient capital promotes financial stability by reducing the likelihood of bank insolvency and moderating the effect of credit cycles," Spencer said.

Bank capital includes ordinary shares, retained earnings, capital instruments issued by a bank that are continuous given there's no fixed maturity date such as preferred shares, and long-dated subordinated debt, such as bonds, issued by a bank.

Previewing the then-imminent release of the Reserve Bank's December consultation paper on bank capital, in late November 2018 Reserve Bank Governor Adrian Orr made some strong comments on bank capital at the central bank's bi-annual Financial Stability Report press conference.

"Bank capital ratios have declined continuously in the last 30 plus years even though bank crises have been as frequent as they ever have," Orr said.

"Bank capital is the number one safety valve for citizens of a country because that allows us to absorb losses before it becomes taxpayers' losses and/or future generations' losses. People forget losses are not just borne by the current taxpayer, but by the lost output now and for many years to come. And this is the framework we're bringing together to talk about bank capital," Orr added. "We will be expecting [banks to hold] more capital and ... good quality capital."

Orr didn't specifically mention bank depositors. At last count households had $175.311 billion deposited with banks and this is also protected by bank capital.

Banking crises

It's important to remember that banking crises have happened right here in NZ. Most recently BNZ needed to be recapitalised twice, in 1989 and again in 1990. After a $648 million annual loss, the 87% government owned BNZ was bailed out by a recapitalisation worth $610 million that diluted the government's shareholding to 52%.

This first recapitalisation involved a government underwritten rights issue of new shares worth $405 million, where the government gave up its rights to the new shares to Fay Richwhite's Capital Markets Equity Ltd. The recapitalisation also involved the issue of preference shares worth $205 million to Japanese investors. The government also provided bridging finance of $200 million.

Then, in 1990 after BNZ's $124 million profit turned out to be overstated due to creative accounting, BNZ was recapitalised with $200 million of taxpayers' money and $50 million from Capital Markets Equity. Current owner National Australia Bank bought BNZ in 1992.

There's a detailed wrap of NZ banking crises from the Reserve Bank here.

More recently, at the onset of the GFC, NZ banks received taxpayer sponsored bolstering via the Crown retail deposit guarantee scheme, and the Crown wholesale funding guarantee scheme covering overseas bank borrowing, in which taxpayer liability peaked at $10.7 billion in November 2009. The wholesale scheme was used by ANZ, BNZ, Westpac and Kiwibank. Across the Tasman Aussie banks benefited from the same GFC backstops.

'Basing their minimum capital requirements on their own economic-capital models and systems'

Now back to the internal models approach.

As a Reserve Bank Bulletin article from 2005 put it; "Over the past decade banks have invested heavily in economic capital models and systems that can better help them identify, measure and manage the key risks that they face. The capability of modelling techniques has improved to the point that banks use them increasingly to determine internal capital targets, feed in to pricing strategies, assess risks, determine economic value added, and contribute to executive remuneration...Banks that apply the Internal Ratings Based [internal models] approaches will base their minimum capital requirements on their own economic-capital models and systems."

Regulators like the Reserve Bank view the internal models approach as being about balancing the incentives on banks to try and minimise capital against the outcomes of allowing banks to model their own capital, which has been seen as increasing the sensitivity of capital requirements to key bank risks.

In a 2009 article the Reserve Bank noted the NZ banks accredited to use internal models are all Australian owned, with parents accredited to use internal models by the Australian Prudential Regulation Authority. The NZ banks generally base their internal models on those used by their parents, the Reserve Bank added.

How capital requirements work

Let's now look at how capital requirements work in practice. Here we need to introduce the concept of risk-weighted assets. These are used to work out the minimum amount of regulatory capital a bank must hold. The capital requirement is based on a risk assessment for each type of bank asset.

Here's an example. A housing loan valued at $1,000 with a risk weight of 30% means risk weighted assets are worth $300. The capital requirement is then determined by multiplying risk-weighted assets by 8%. For our example this gives a minimum capital requirement of $24 for that $1,000 mortgage.

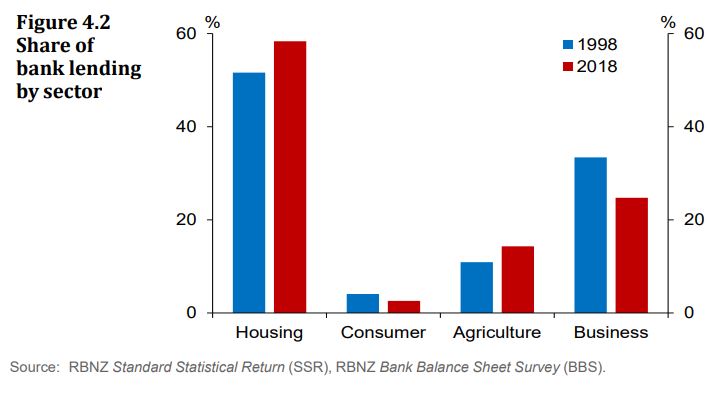

Based on the most recent Reserve Bank figures, housing lending comprises $257.484 billion, or 57%, of NZ financial institutions' lending. Thus it's the key area of bank lending exposure. And as the Reserve Bank chart below shows, housing's share of overall lending has grown over the past 20 years.

Parts II and III

In part two of this series we'll look at what allowing the big four banks to use the internal models approach means in practice, specifically in terms of the capital held against their hundreds of billions of dollars worth of housing loan exposure, and how and why this gives ANZ, ASB, BNZ and Westpac an advantage over their NZ owned rivals. We'll also look at how the Reserve Bank is proposing to change this.

Then in part three we'll look at how the owners of NZ's big four banks have fared over the past decade, and how the Reserve Bank's proposal to increase bank capital requirements could impact this, and what it may mean for bank customers. We'll also look at a couple of other key aspects of the Reserve Bank's proposed changes to bank capital requirements.

You can read Part 2 in this series here.

You can read Part 3 in this series here.

(You can see all our articles on bank capital here).

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

17 Comments

So for mortgages the risk weight % is basically a function of the borrowers loan to equity ratio. In a falling market the borrowers equity deteriorates and the risk weight goes up then the bank should theoretically have to hold more capital against the riskier loan. I doubt that would ever happen. The underlying assets would just never be mark to market revalued.

My understanding is mark to market really helped hammer the US during the GFC. Helped force a lot of mortgagee sales.

In reading this article there appears to be a lack or understanding or alternatively a general refusal to acknowldge that the greatest risk to banks are their own business practices. The Aussie royal commision and the GFC both demonstrated that it wasn't market conditions that created the problems, but the banks themselves driving what happened. The list of their misbehaviours is too long to recount here and I am sure there are many who could do a better job than I, but they cannot be ignored. I hope Gareth's intent behind these articles is to demonstrate that banks must be robustly regulated to limit the damage they can do to a country, and that thay must be held accountable for how they treat, and risk, depositors funds.

Having said that I applaud the articles and look forward to reading them, but I have some questions. Gareth provides an example of a mortgage of $1000, with a risk weight of 30%. He then states that that risk weight means the value of the asset is $300. My question on this does this mean that the value to the bank is $300? If so why then did they lend $1000 on the loan? Does this mean there is effectively $700 unsecured, or is the $700 secured, and $300 unsecured? I am assuming the risk weighting a a measure achieved throught the collection of data which allows the bank to assess the risk of the terms of the loan to not be met? If so does that mean that the risk that this will occur is 30% or 70% (taking the first question from a different perspective). And where does the 8% come from? what does this represent? If I read this right only $24 is required to loan out $1000, effectively a capital to loan ratio of 41? Seems a little high to me?

Agreed "a general refusal to acknowledge that the greatest risk to banks are their own business practices"

They need regulation to set minimum standards. They are unable to regulate themselves when conflicted with their own profits/bonuses.

Murray86, this series of articles won't be all things to all readers. But hopefully they'll give a broad oversight of where bank capital has come from, where it's at, where it's going and why.

I wonder what the original rational for fractional reserve lending was? Aside from bankers greed. Total debt/bank lending is over twice the deposits held as per this article. Crazy to think that most of those deposits are made up by by this lending/debt anyway. Adrian Orr is doing a frustratingly good job of managing this Ponzi scheme and he is making it a more stable Ponzi but it is still a Ponzi non the less.

Once lowering interest rates has lost its effect we will see the rubber meet the road. Let’s hope there’s no socialisation of the loses as there has been minimal socialisation of the profits!

by lowering lending standards against houses banks have created bubbles in the housing market and farm land.

'There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

Amen. Let me just reinforce that in case anyone is in any doubt. There is no way of avoiding the collapse of credit fuels asset bubble. Talk all the bullshit you like about the supply of houses, but without a runaway credit supply the price would stay suppresses regardless.

jump to 2.19. This is why banks need to double capital held.

Good article, well explained, It should be compulsory reading. I think it's inevitable A/NZ banks increase capital reserves - starting with cutting the dividend payout ratio.

Do they risk weight all mortgages the same?

Using current market valuations of property collateral such as QV.co.nz or some other data supplier banks can now calculate up to date LVR's on mortgages. A mortgage with a LVR of 20% has a signifcantly lower risk profile to a mortgage with an LVR of 80% -90%. Risk weightings should adjust for this. If they don't, the banks are applying a potentially understated risk factor in their risk weighted assets calculation.

Not sure if this is accounted for when the banks do their risk management stress tests - when they assess probability of loss and loss given default.

There's some detail on this in Part 2 of this series.

Thank you Gareth. Look forward to reading it.

As I understand:

1) under Basel II, the risk weighting rate for residential mortgages is based on exposure at default, and no explicit mortgage LVR .

2) under Basel III, the risk weighting rate for residential mortgages is dependent upon the mortgage LVR. It is interesting that a 100% LVR mortgage only has a 70% risk weight in the risk weighted assets calculation - to allow for the fact a 30% drop in the value of the asset in the event of a default perhaps?.

Not sure if the banks in NZ are applying Basel II or Basel III at the moment.

As per wiki - Basel III was agreed upon by the members of the Basel Committee on Banking Supervision in November 2010, and was scheduled to be introduced from 2013 until 2015; however, implementation was extended repeatedly to 31 March 2019.

As a guide, FY18 ANZ NZ had $122bn loans with $61bn RWA. So across all lending they average around 50% RWA. That would require around $6.5bn to $7bn loss absorbing capital.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.