By Gareth Vaughan

Is a major structural change underway with some New Zealand savers and investors falling out of love with bank deposits? Or is it just that they're looking elsewhere for higher returns due to the low interest rate environment?

This is a question pondered in KPMG's annual Financial Institutions Performance Survey (FIPS), out today.

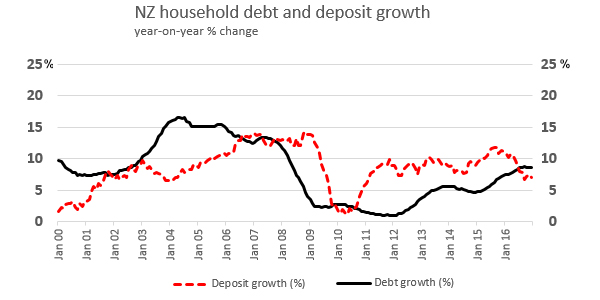

Covering the year to September 30, 2016, the survey notes banks experienced their fastest lending growth in eight years, with their loan books growing by 8.1%, or $29.7 billion, to $395.71 billion. This outstripped growth of deposits, used by banks to on-lend to borrowers and meet their Reserve Bank enforced Core Funding Ratio requirements. Lower levels of deposit funding mean banks need to borrow more money through volatile overseas wholesale funding markets.

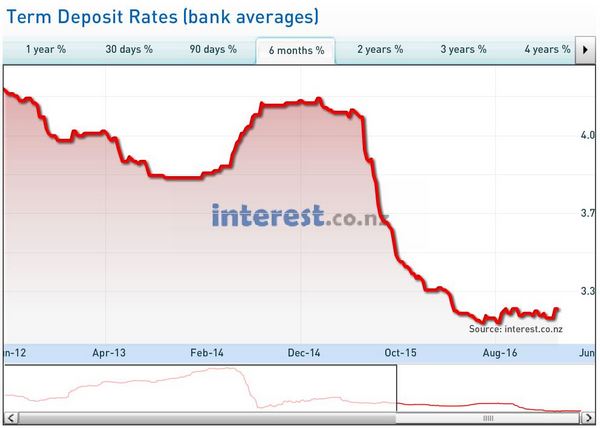

In a low interest rate world with the Official Cash Rate cut to a record low of 1.75%, banks' deposit interest rates have dropped to very low levels by historic standards with stiff competition among lenders to raise deposit funding.

"One of the questions raised with executives was whether the decrease in deposits experienced by some banks was the beginning of a structural change or more of a blip. Some executives speculated that it was the beginning of a move away from deposits, caused in part by a greater flow of money into KiwiSaver and other investments, which was caused partly by the low deposit rates and partly by consumer preference in the younger demographic," the FIPS says.

The million dollar question

John Kensington, KPMG's head of banking and finance, told interest.co.nz whether this was a structural change or a blip was the million dollar question. He points out many New Zealanders haven't had as wide a range of investments as people in some other countries, but the introduction of KiwiSaver in 2007 has given us an opportunity to understand a broader range of investments.

"There's only ever so much money going around and people only have a certain amount to invest. In the past it probably went into property, or maybe it went into deposits until you had the deposit for a property and then it went into paying off your property. And once it was paid off you went into deposits. So the New Zealand psyche was fairly simple and structured and straight forward," said Kensington.

"Maybe we've had too much [money] in property and deposits and not enough in other things. One catalyst will be that deposit rates are low, [and] another might hopefully be that people have become a little more educated on where to put their money, and how to spread their money around to diversify their risk."

"But is it a structural change or is it just a blip? That's the million dollar question I can't answer. Are we seeing younger people that are perhaps a bit more savvy, a bit more impatient and not just prepared to put their money in a deposit? If that is the case it could be driven by the fact that rates are so low. Or alternatively it could be driven by the fact, and it'd be nice if it was, that people understand more about investing now," Kensington adds.

"It's probably just too soon to tell. If you look at other countries there has to be some shift in where we are because we are heavily, heavily biassed toward property and heavily biassed, after that, to bank deposits for convenience. It could be the beginnings of structural change but I honestly don't know."

Banks battling for deposits has a flow-on effect to the non-bank sector comprising finance companies, building societies and credit unions. Executives in this sector say they are finding it increasingly difficult to compete with banks for deposits, especially when the banks carry out special six-to-nine-month deposit offers at the same rates as offered by credit unions and building societies.

"Finance companies that are backed and funded by a bank are also being cautioned that they can no longer borrow the same level of funds at the same historically low interest rates that they have enjoyed. This is a clear signal from the banking sector to expect tougher times ahead as they shore up their capital balances and source additional deposits, while also trying to rein in lending growth," KPMG says.

Return on equity & return on assets both drop

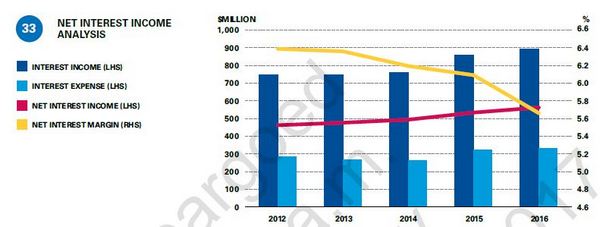

The FIPS report notes bank sector profit fell for the first time n seven years, dropping 6.5% from the 2015 record high of $5.17 billion to $4.84 billion. The drop came as the sector interest margin fell 13 basis points to 2.15%. KPMG attributed this to "less relief on the funding side of the balance sheet and intense competition on the lending side."

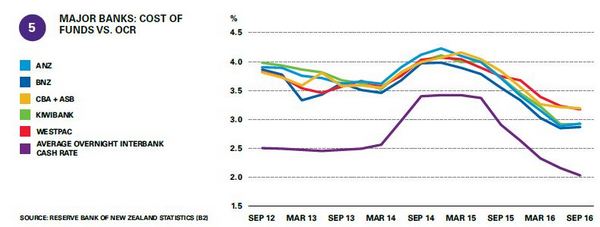

Funding costs across the sector fell 62 basis points to 3.25% as interest expense, or what banks themselves pay to borrow money, fell 10.6%, or $1.5 billion.

KPMG also points out that the banking sector's return on equity (ROE) and return on asset (ROA) levels fell on an annual basis. ROE fell 200 basis points to 13.96%, and ROA dropped 16 basis points to 1.00%.

"The decreases in ROE and ROA played a large role in why banks have scaled back lending growth in recent months, as they look for deals that are appropriately priced as opposed to primarily looking for loan book growth. These decreases are also a reflection of an increasingly challenging environment where banks are finding it more difficult to maintain current levels of earnings. The cost pressure of growing regulatory compliance, increased competition, volatility in markets and the costs associated with staying digitally competitive are examples of the current challenges the industry is facing," the FIPS says.

"Funding's going to be as challenging, if not a little bit more challenging, to get. Banks, especially the large Australian ones, [are] recognising they may have some tightness on the funding side coming up, and it might be a good time to be a bit careful because the property market is quite heated up. Over the last two years they have hit some return on equity and return on asset triggers that have meant that there's deals that they need to look closely [at] to see if they want to do it," Kensington says.

Meanwhile, the FIPS report also says bank executives perceive that the Reserve Bank is "becoming increasingly cautious" about the banking system's liquidity and credit quality.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

33 Comments

And the highest mortgage rates in the OECD.

UK, Germany, USA 1.5% -3%

NZ is certainly the experimental lab for financial testing.

Current 30 year mortgage rate in the US is @ 3.7 to 4.6% - depending on credit score, state and city

https://finance.yahoo.com/rates/

If you want lower interest rates move to the US or Europe.

or is it the OBR at work,

why should I risk my money with a bank for their return when I can get a better return elsewhere for the same or lower risk.

is this not what the RB intended, or did they think most people would be uneducated and head for the apparent safety of a bank after the finance companies collapse

I don't think it's the OBR per se, rather the fact that everything looks a bit unstable at the moment.

Banks used to be considered "safe", but I think that view is changing.

This perception is not helped by the perceived money grabbing, i.e. lifting Mortgage rates without touching deposit rates.

I know it makes me wonder what their plan is, looks like a typical smash and grab before trouble hits.

The OBR is based on the premise that a bank won't be bailed out by the government. If one of the big four and probably Kiwibank needed a bail-out then the government would of course do it. Governments tend to like winning elections and if the BNZ failed again then the Gov would bail out no question in my mind. Also I think the big four banks here are as safe an investment you can possibly get. The profits are extremely high and all other markers point to them been the best performing banks in the world.

That's the catch though isn't it.

Profits are exceptionally high, yet they are complaining about lack of deposits.

Could they not raise the deposit rates and only take in semi-record profits for a change?

High profit, high leverage=high risk

It seems pretty straight forward to me but I look at micro economic behaviour a lot. If you compare repayments for borrowing $100k @ 8% and $200k @ 4% what you'll notice is the payments are higher even though the interest is the same by simple calculation. So higher house prices even with lower interest rates remove more cashflow from household budgets.

Then combine the terrible interest payments that people receive people look elsewhere. I have had a number of people saying that their kiwisaver has done better than any investing decisions they've ever made so they have no issues contributing the full amount.

Flat pay and increased cost of living is tapping the last of the money that people have. So for a typical (?) family they have high mortgage payments, kiwisaver, car payments and kids cost a lot of money. It's not uncommon for my friends to say they have no money left after paying for everything. Given that this is a common experience for those who are supposedly middle class I don't see where savings are going to come from.

So my opinion is that the finance industry is tapping people for every dollar they can. One bank employee I was talking to last month discussed the conflict of given customers good advice (like paying off their mortgage early) and the internal conflict that the bank ends up making less profit. What I put forward was that with my business I help my clients make more money instead of focusing on milking them for money. This is an alien concept to the banking industry but over the long term if you help you clients do well financially they return with more business and more money. Maybe if banks weren't trying to shaft their customers there would be a long term benefit of deposits.

Dictator, I suspect your comment that 'their kiwisaver has done better than any investing decisions they've ever made' is an important factor in the move from from fixed deposits. Increasing numbers of people are telling me how good Kiwi saver is. And some of these have for years been trotting out the tired old 'the 1987 crash wiped out so many people I wouldn't touch shares again' nonsense. I reckon there is a significant fundamental attitude swing under way, not just driven by low FD rates, a general increase in risk appetite happening as people feel more secure that the economy is trending positively.

In my bank this week arranging to move a largish matured fixed deposit to my cash account and was interested in how focussed the consultant was on whether I will be rolling over some of it for another term.

First point: sure, shares are doing well at the moment. Partly due to the wall of money being thrown at them by all the incoming Kiwisaver money. If/ when the share prices fall i.e. the more aggressive kiwisaver fund units start falling, people will readjust their fund portfolios into cash funds en mass and that's when shares will really start tanking. Remember how useless the aggressive funds were in the period just after Kiwisaver started! They were dorked by the conservative and cash funds. It could happen again.

Second point: If you want a govt guarantee of sorts, put money into Kiwibank right now. Its NZ post guarantee for new term deposits ends in just over a weeks time. It increased its longer dated rates a few days ago: they are now very competitive.

You could be right about some people moving back to less aggressive kiwi saver funds during share price correction phases, but not convinced this will happen ' en mass'. I have a feeling the message is finally getting through about taking a long term view on investment strategies. If so people might tend to stay the course.

Impossible to know for sure but with people like Maxwell banging on endlessly, combined with a younger more progressive cohort starting to seriously think about saving for retirement, I reckon our investing is becoming a bit more sophisticated.

Thanks for your perspective on Kiwi bank. Personally - shares have treated me very well over decades. Cash and fixed deposits are strictly short term holdings to provide balance in my portfolio. Although the strong growth in shares over the last 5 years means I'm now (theoretically) well underweight in cash.

Shares are doing well at the moment but incoming KiwiSaver money wouldn't have anything to do with it. We're just the tail of the dog. The dog is the US and Europe. We go as they go.

Dictator - you are on the money with this

"Flat pay and increased cost of living is tapping the last of the money that people have..."

This gives some reasoning why = the underlying return on energy

https://surplusenergyeconomics.wordpress.com/2017/02/16/87-a-world-econ…

"taking Britain as an example, the cost of household essentials rose by 48% between 2006 and 2016, far outstripping much smaller increases in wages (+21%) and general CPI inflation (+25%). At the level of national economies, much the same occurs, with the cost of essentials outpacing both income and broad inflation as ECoE increases.

This is one reason why seemingly-positive data on the economy as a whole increasingly clashes with individual experience – the data says the economy is growing, but the individual feels poorer, not wealthier. An increasing ECoE – and its transmission through the cost of essentials – helps explain this apparent contradiction."

The banks are saying that “lending growth outstripped growth of deposits” and “lower levels of deposit funding mean banks need to borrow more money through wholesale funding markets”.

However, the balance sheet of the entire banking system means that “the need to borrow” through wholesale funding markets to meet lending demand necessarily reduces deposit creation one-for-one.

It seems the banks themselves are the cause of their problem. Weak banks borrow via wholesale funding markets and thus reduce deposits available to the stronger banks.

Exactly.

Furthermore, indefensible nonsense issued from the mouths of so called experts has to stop.

There's only ever so much money going around and people only have a certain amount to invest

Is he kidding? There is as much credit and hence money as banks wish to fabricate, both onshore and offshore.

“In a barter economy, there can rarely be investment without prior saving. However, in a world where a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.” Read more

On the topic of indefensible nonsense from so-called experts, I love this one too:

"Maybe we've had too much [money] in property and deposits and not enough in other things. "

Universities teach the exact opposite of the truth, of how banks create loans. New loans are simply ADDED to the bank’s deposit account.

http://investmentwatchblog.com/universities-teach-the-exact-opposite-of…

This article explains how,

rather than banks lending out deposits that are placed with

them, the act of lending creates deposits — the reverse of the

sequence typically described in textbooks.

The article mentioned is a pdf by Bank of England:

Money creation in the modern economy

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin…

The RBNZ is just as culpable.

However, banks in New Zealand appear to be relatively efficient in the core intermediation role of receiving money in the form of deposits and recycling that money via loans to creditworthy borrowers. Read more

Peri, can we find out who the weak banks, that are borrowing on the wholesale market are? Under OBR that knowledge should be available to depositors.

The RBNZ reports this only in the aggregate

(See RB table C4 including Lending to NZ Residents in both NZD and FX versus funding from non-residents. Columns AJ + AP and X)

To get the position of individual banks is more difficult, requiring interpretation of the disclosures from each individual bank. It is information that is easy for accountants to obscure and confuse which seems to be the aim.

And might be why the resistance to the RBNZ's proposed dashboard was so strong?

Much of this has to do with globalisation, believe it or not. Large corporations can produce cheaper goods and services overseas without distributing the factor rewards in the form of rent, wages and other expenses to the national economy. So in a way, these companies can expand their bottom line, which translates into economic growth, without increasing wages (in fact reducing wages by moving their manufacturing base overseas).

As soon as bankers start woffling about structural changes in the market you know they are clueless as to whats happening or driving anything. This is excellent 2 part article

http://www.feasta.org/2014/03/17/how-to-be-trapped/

"Even if we were to ‘solve’ our financial and monetary problems, we’d walk straight into oil and food crises which are systemically de-stabilizing.

Our predicament and the tragedy of attempting change is: given time and resource constraints and the reality that we depend upon a de-localized networked system without central control, how do we change the system while ensuring we do not collapse its essential functions. Decreasing global resilience and the increasing complexity, interdependence, tight coupling and the speed of the processes we depend upon make this a fundamentally uncertain, dauntingly complex and very dangerous set of challenges. So we dig in because we can’t dig out. We grasp for growth, we buy time and kick the can, and with each step become more vulnerable.."

http://www.feasta.org/2012/06/17/trade-off-financial-system-supply-chai…

>"So we dig in because we can’t dig out. We grasp for growth, we buy time and kick the can, and with each step become more vulnerable.."

That's also a great summary of the last three terms of National government. Housing, pension, immigration, foreign property buyers, funding critical infrastructure etc.

Agree- its actually a great summary of the last 10 years everywhere - no Politician wants the reckoning on their watch, but physical laws will prevail over imagined economic ones.

Fed president says US banks have “half the equity they need”

http://www.ronpaullibertyreport.com/archives/fed-president-says-us-bank…

Which begs the question, why doesn't the RBNZ call out our own four large Australian banks, which self calculate/regulate residential property mortgage capital requirements ~27% of 8% tier one capital, amounting to demands of ~$2.16 for every $100 (2.16%) of mortgage debt issued?

Starkly below Fed President Kashkari's demands of 23.5% bank capital set against banks assets in the US.

Our plan would increase capital requirements on the biggest banks—those with assets over $250 billion—to at least 23.5%. It would reduce the risk of a taxpayer bailout to less than 10% over the next century.

Alarmingly, there has been recent public discussion of moving in the opposite direction. Several large-bank CEOs have suggested that their capital requirements are already too high and are holding back lending. As this newspaper reported, Bank of America CEO Brian Moynihan recently asked, "Do we have [to hold] an extra $20 billion in capital? Which doesn't sound like a lot, but that's $200 billion in loans we could make." Read more

But does the RBNZ care? Not a jot. It has lined up bank depositors to bailout indiscriminate, barely regulated bank lending under OBR.

One doesn't need to be financially savvy to realise that there are currently better returns than term deposits largely as a result of "money printing" by the USA and other banks in response to the GFC.

For generation Y saving for their first home, share market returns through their KiiwSaver active growth accounts have far outstripped returns on term deposits. A no-brainer.

For baby boomers about to retire or have just retired, with memories being bitten by the share market crash in 1987 and investment company crashes in 2007, and seeing their homes increasing at double digit figures compared to term deposits, are by default investing in property as it is obviously far more attractive. Again, a no brainer.

Generation X and middle age mortgage holders - without surplus cash - are just enjoying the fruits of low interest rates and capital gains (and possibly leveraging to buy that rental property if they can).

So where is the cohort of anybody below 70 plus years of age who is going to be putting money into term deposits??

Is this a entrenched situation; off course not. It is just a reaction to the current situation. As conditions change, and in particular term deposits become competitive again, then Generation X and baby boomers are likely to look again at term deposits.

People aren't stupid and have a little financial savvy to react to changes.

One doesn't need to be financially savvy to realise that there are better returns than term deposits.

For generation Y saving for their first home, share market returns through their KiiwSaver active growth accounts have far outstripped returns on term deposits. A no-brainer.

Deposits change hands when bank savers buy stocks from a seller.

Buying houses is the same for cash rich buyers purchasing from a seller. Residual seller mortgages (bank assets) net out against the deposit (bank liability ledger). If the buyer needs a mortgage the bank debits the new mortgage ledger to credit the buyer's deposit account..

Furthermore,

Banks do not have pre-existing funds in the form of legal tender (NZ currency in circulation ~$6.3 bn) to lend, except in miniscule amounts (NZ currency in circulation ~$6.3 bn) relative to the size of their loan portfolios (NZ bank claims 432 bn). In other words, banks create demand deposits out of nothing, and it therefore remains a nothing. Read more

Cash lurk: banks skim millions from customers, again

http://www.michaelwest.com.au/cash-lurk-banks-skim-millions-from-custom…

The 1st sentence of the article asks:

"Is a major structural change underway with some New Zealand savers and investors falling out of love with bank deposits? Or is it just that they're looking elsewhere for higher returns due to the low interest rate environment?"

It's the latter, no need for fancy graphs and long spiel, just looking for a better return

IMO, bank term deposits are too low a return with too high a risk. If the housing market has a hard landing, some banks may not fare so well, in which case they are legally entitled to confiscate customer savings down to the last $10K. Just to keep the banks going and take more risks at savers' expense. What a flawed system, but savers can pull their funding in protest.

No they arent; I don't think you understand OBR.

http://rbnz.govt.nz/~/media/ReserveBank/Files/regulation-and-supervisio…

Shareholders, then capital, then the OBR freeze which is designed to speedily release as much funds as possible.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.