By David Scobie*

With nine years of historic returns now available for New Zealand’s flourishing retirement savings vehicle, David Scobie, senior consultant at Mercer, reflects on the risk and return outcomes experienced by KiwiSaver members since inception. The journey has been an eventful one, and yet KiwiSaver has successfully transitioned from timid toddler to composed adolescence. A lesson for members is not to lose sight of the end-game. A tolerance for volatility, where possible, offers scope for a greater pool of retirement assets in the long-run.

What was on your investment mind back in 2007? The bursting of the US housing bubble? The Bank of England bailing out the Northern Rock mortgage company? The wisest amongst us were perhaps contemplating the dawn of a far-reaching financial calamity, warily checking share prices on a newly-released gadget known as an iPhone.

Meanwhile there was another notable invention cautiously rearing its head that year – KiwiSaver. Born amid an inauspicious economic environment, but gently encouraged by some state-sponsored sweeteners, the scheme quickly grew into a force to be reckoned with. Today, at some $37 billion all-up, KiwiSaver stands shoulder-to-shoulder with the largest of New Zealand’s investment funds. So what path of performance has this savings saviour travelled?

The Road of Returns

A wide variety of fund options comprise KiwiSaver, so it’s helpful to break them down into categories. For the purposes of the Mercer KiwiSaver Survey, funds are separated into universes based on (1) “Default” status (most conservative) and (2) the benchmark level of exposure to growth assets. Notably, returns are compiled on both an after-tax and after-fees basis, thereby replicating as far as possible the actual experience of members (excluding cashflows).*

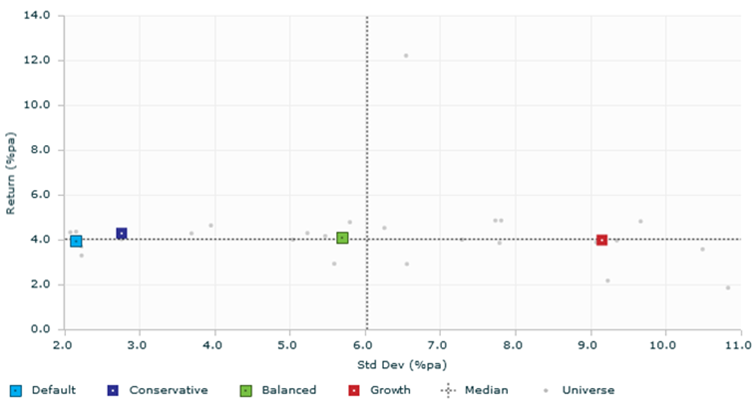

The following chart plots the annualised return against the annualised standard deviation (return volatility) of surveyed funds which have been in existence since the launch of KiwiSaver. Category medians are shown by the squares, while median outcomes for the full universe are represented by the horizontal and vertical dotted lines.

Return and Risk (Standard Deviation)

A first observation is that the typical average fund return did not alter regardless of whether it was positioned at the relatively risky or more conservative end of the investment spectrum. How can this be! In essence, while equity markets generated impressive returns over the last seven years of KiwiSaver’s life, the first two years included a particularly severe event - the Global Financial Crisis (GFC). Meanwhile, fixed interest assets produced almost consistently positive results over the full period, assisted by sustained falls in interest rates. Both of these events were notable in their uniqueness.

The second thing one notices is that there’s a good chance a typical KiwiSaver fund’s average annual return was a fairly modest 4% per annum over the full period. However, it’s helpful to note that, in practice, most members will have secured an average return above that figure. This is due to the larger account balances built up in later years - arising from compounded returns and accumulated contributions - receiving the benefit of stronger asset price performance in those later years.

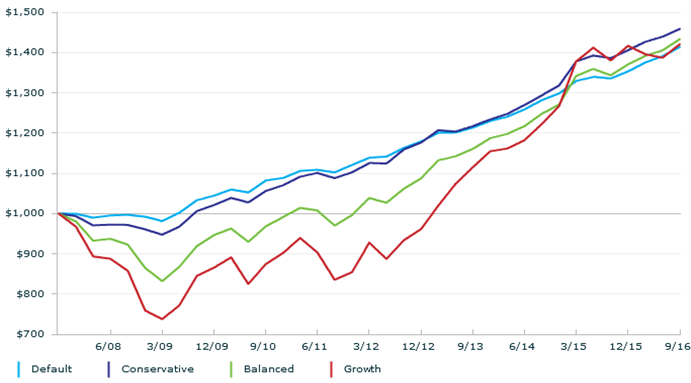

The pattern of fund returns over time is illustrated in the graph below which shows the worth of $1000 invested in the median category manager at the advent of KiwiSaver (assuming no additional contributions).

Growth over Time of $1000 Invested

As the discussion so far has implied, the end outcome is remarkably similar for all fund categories, albeit a less comfortable ride for those that invested in (and stuck with) more growth-oriented options. One could be forgiven for asking – why bother with extra investment risk? Should I just opt for a more conservative fund and expect a similar or better return?

Playing for Time

If an investor today was in their later stages of life, or expecting to shortly buy a first home, or had great confidence that sharemarkets were poised to enter a prolonged bear phase, then that may be a justified stance. But for the multitude who recognise that saving for retirement is a long-term exercise, and that shorter-term market movements are hard to accurately predict, history suggests that taking greater risk will likely pay off with the benefit of time.

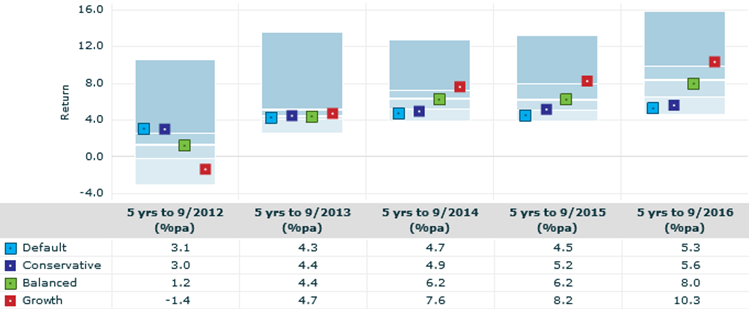

The chart below, showing rolling 5-year fund returns going back several years, highlights this perspective. As asset prices recovered in the wake of the GFC, periods displayed a more “normal” pattern of higher-risk funds (red/green boxes) outperforming lower-risk peers (blue boxes). Also of note is the pleasing level of returns in recent years – mostly in the realm of 5-10% per annum.

Return over Rolling 5-Year Periods

When looking back over KiwiSaver’s lifespan, we can surmise that the majority of members will have had a broadly positive experience in terms of growing their savings balance. This conclusion is strengthened once the significant benefit of government and employer contributions is factored in. Those members with a less positive experience are likely to be those who joined up early and “lost their nerve” along the way.

Future Focus

Looking forward, investment markets pose some interesting challenges for KiwiSaver members. Historically-low interest rates have buoyed fixed interest returns for many years, but any prolonged upward movement in yields (which we have seen hints of recently) will dampen the performance of conservatively-oriented funds. And global share markets, having predominantly rallied for the last several years, cannot be assumed to maintain this impressive pace indefinitely. That said, investment markets are more than capable of surprising on the upside and, over time, the power of diversification remains on the side of the average KiwiSaver member.

It’s worth recalling that uncertainty in investment markets is nothing new; in fact, it is part and parcel of seeking returns over the long-term which have a good chance of bettering the common alternative of ‘money in the bank’.

In summary, KiwiSaver has endured a fair share of turbulence in its life to date, and we can anticipate more bumps to come. However, members who invest with regard to their true investment timeframe, while factoring in their tolerance to withstand volatility along the way, can expect to be amongst KiwiSaver’s future winners.

Notes:

- The Mercer KiwiSaver Survey contains fund returns after fees and after tax at a Prescribed Investor Rate of 28%, being the highest tax level KiwiSaver members face.

- Returns are after all fees that are asset-based being management fees, performance fees, trustee fees and other in-fund costs.

- The Survey categorises funds into universes on the following basis:

- “Default” status funds

- “Conservative” funds, being those with a weighting of 20-39% to growth assets

- “Balanced” funds, being those with a weighting of 40-60% to growth assets

- “Growth” funds, being those with a weighting of 61-100% to growth assets

- Growth assets are regarded as investments held in equities, real assets and alternatives, whilst investments in fixed income and cash are regarded as Income assets.

- Funds with returns available since KiwiSaver’s inception represent a sub-set of the selection available today.

- Mercer is a KiwiSaver provider with fund returns included in the Survey.

*David Scobie is a Principal in Mercer’s Investments business, based in Auckland. He advises institutional clients on their investment policies, structures and fund manager selection, linking in with Mercer's global research capability.

This article does not contain investment advice relating to your particular circumstances. No investment decision should be made based on this information without first obtaining appropriate professional advice and considering your circumstances.

4 Comments

Those are the averages, some funds did much better/worse than that; could these be named?

You will get a fair idea from our KiwiSaver reviews who are above/below the line. Mercer might show the information to their larger fee paying clients but don't expect it to be disclosed publicly.

What is interesting to me is that many would use the graph above to prove that it doesn't matter which fund you're in...it looks like you end up with the same returns eventually, right?.

No. That is only true of a lump sum - paid once. KiwiSaver members paying in little and often every payday will have much, much more in a Growth Fund due to the bouncy volatility along the way. This is why interest.co.nz's "real" returns for KiwiSaver members contributing regularly is more useful than investment returns expressed in traditional ways.

I'd like to see more emphasis around explaining volatility and exposure of risk-adjusted returns for each of the funds. Maybe a chart of expected return ranges and how the fund has performed in relation to the expectations might be better.

What the line chart shows in the article is that conservative funds have performed the best on a compound basis but this is not the fact when you take into account regular savings. Many will see that conservative funds are ahead of the game and stay in their default funds and this is not what the regulators want.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.