Gareth Vaughan

The growing use of interest-only loans by New Zealand borrowers could prove "particularly problematic" if house prices fall, S&P Global Ratings says.

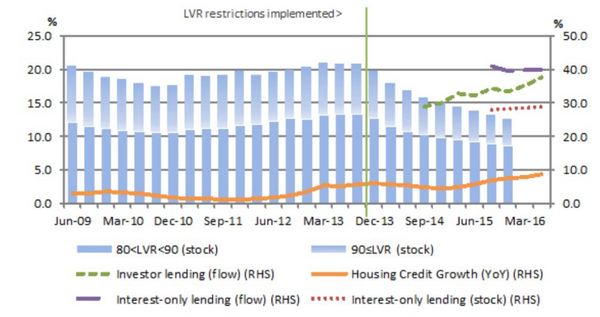

In a report on the risks of rising house prices for New Zealand banks, the credit rating agency notes imbalances are continuing to build. These imbalances include the increasing use of interest-only loans, which account for 40% of housing loan flows through 30% of owner-occupier loans, and 55% of investor loans over the past year against overall loan stock of 28%.

S&P points out interest-only loans are unlikely to be limited by the Reserve Bank's incoming, beefed up high loan-to-value ratio restrictions on banks' residential mortgage lending.

"The increasing use of interest-only loans could prove particularly problematic if house prices fall, most notably given the level of household wealth tied up in residential housing - the reverse event of rising house prices and related 'wealth effect'," S&P says.

The Reserve Bank recently lifted the lid on the extent of interest-only borrowing, with new official figures revealing around 40% of new mortgages by value are being taken out on interest-only terms.

Regulators in Australia became concerned when interest-only loans hit more than 40% of new lending across the ditch. In December 2014 the Australian Prudential Regulation Authority warned lenders it was "dialling up the intensity" of its supervision to reinforce sound residential mortgage lending practices. And the Australian Securities and Investments Commission announced it would "conduct a surveillance" into the provision of interest-only loans.

Here's a detailed look at interest-only lending as offered by New Zealand banks.

High LVRs fall as other imbalances build

The Reserve Bank's challenge

Meanwhile, S&P says that while some indicators of financial stability have improved since the Reserve Bank embarked on its macro-prudential intervention in 2013 with the introduction of the LVR restrictions, their effect has been narrow. This is because housing-related imbalances continue to build, highlighting the challenge facing the regulator as cyclical and structural impediments, mostly out of the Reserve Bank's control, remain unaddressed, S&P says.

"Against a backdrop of falling interest rates (which appear to have further to fall), strong net migration and thus far insufficient supply response, particularly in Auckland a city that accounts for around 50% of permanent (net) migration flow, the new restrictions can only be realistically expected to deliver a narrow improvement to financial stability, while the aforementioned issues - including the favourable tax regime for investing in housing debt - remain largely unaddressed," S&P says.

"It's probably also too early to determine what impact Auckland Council's Unitary Plan will have on housing supply in the longer run (400,000 new homes over the next 30 years appears a little hopeful given the average over the last 25 years is around 7,500 per year), although it does provide some optimism that supply constraints are being addressed."

"We also believe it is increasingly likely some form of debt-to-income measures will be introduced, in a similar capacity to the minimum serviceability requirements introduced in Australia more recently. These could prove effective in shoring up financial stability across the board as wage growth remains subdued and interest rates remain very low," says S&P.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

68 Comments

Well you certainly cannot say that S & P are not warning us of the dangers in the way our property bubble is headed and the risks it is placing on our banks. You would think that the Reserve Bank and the Government would take it more seriously and do something meaningful that will achieve effective timely results.

Don't worry, the government has a plan, immigration and maybe some more immigration and maybe sell our power stations, telecommunications, steelmill and pineforests, oh what? sold already?

"The increasing use of interest-only loans could prove particularly problematic if house prices fall, most notably given the level of household wealth tied up in residential housing - the reverse event of rising house prices and related 'wealth effect'," S&P says.

I guess this example of Aussie excess equally afflicts New Zealand.

Aussies are buying Bentleys, BMWs and Mercedes in record numbers even as living standards fall in a sign that rising inequality seen in the developed world is spreading Down Under.

Top-end car sales surged to a record 104,277 in the 12 months through July, a 15.7 percent increase on the same period a year earlier, according to an index collated by CommSec, Commonwealth Bank of Australia's brokerage unit. Overall new vehicle sales last month climbed just 1.6 percent on an annual basis.

"A lot has been made of softer economic conditions over the first half of 2016, however the same cannot be said for the luxury car market,'' said Savanth Sebastian, an economist at CommSec. "Higher home prices are boosting wealth levels and consumer spending. Aussie consumers are keeping it quiet, but they are buying luxury cars in record numbers.''

Australia's central bank cut rates to a record-low 1.5 percent this month as it tries to tame the currency and spur consumer spending. But easy monetary policy can disproportionally hurt lower income earners as the wealthy can benefit from stronger financial and housing markets fueled by cheap money. In the first three months of this year, Australia recorded its ninth straight quarter of falling net disposable income per capita. Read more

Again, an indication of the RBNZ's very light handed approach at reining in the escalating housing crisis. They could, and should, put limits on the amount and percentage of interest only loans. These loans make banks (and hence depositors) more vulnerable.

It would be interesting to know if interest-only loans are allowed in the covered bonds pool of residential mortgages. If they aren't allowed, then NZ domestic depositors will be the ones who suffer financially under OBR. If they are allowed and start to non-perform, then they will be switched out of the covered bonds pool, again to be held against NZ domestic depositors. i.e. a lose-lose situation for NZ depositors under OBR.

It would be interesting to know what percentage of the interest only loans are for more than 80%/90% of the purchase price. Then we would have a better idea of how many of those mortgages would default in a crash.

The 30% of owner occupier mortgages being interest only means that they are speculating or cannot afford to pay a 30 year mortgage. While not all of them will be a high risk of default I'm sure a large number of them would be.

Running some quick numbers on a $1m house with $800k mortage at 4.25%. Monthly interest only $2833, monthly payment 30 year mortgage $3935.50. The difference in payment is not much more (in crazy Auckland terms). So if someone can't afford the 30 mortgage they've bought 39% more house than what they can actually afford.

I am not sure what is all the fuss about IOLs, in theory it make the borrowers position and ability to pay his loan better for longer ... why that has anything to do with the house price he has borrowed against? and isn't that a very personal situation, i.e. if someone has stretched himself too far and took too much risk then he will be under water not his lender ... especially that lenders are taking a lot of precautions and have a huge 40% cushion @ 7% or more interest rates to fall back against ( according to stress tests announced early this year by RBNZ and Gov) ... I feel that this falls again in the too many Doom assumptions that every one is trying to promote... Please let those who choose to be reckless with money sink and die ... they have been warned not to get too close to the water.... are these calls to protect the banks or the borrowers from mortgagee sales? With such a hungry market any mortgagee auction for 20 or 30% under market price will be very welcome to FHB and many others !!

My take is that with all the 15% stamp duty, 40% LVR or more, Loan to income and other limits ..etc these are an attempt by the RBNZ ( and rightfully so) to slow / dampen the rising of the price curve and prevent a severe overshoot which might hurt the banks if allowed uncontrolled ( it is once bitten twice shy ). The market , will reach a peak point when the equilibrium and balance between supply and demand is almost achieved and houses have reached their max values, ... many people believe that house prices will then remain steady and will oscillate around the results of S and D in a more saturated market ... the market then would most probably dictat gradual decline in nominal house prices overtime balanced against surging Land, building costs and inflation if any ...there is good evidence of the above dampening effect since the beginning of this year and the rate of rise is certainly slowing ... most economists still believe that the rise will continue into 2017 and possibly a bit further, albeit at much slower rates and in single digits.

The S&P report didn't call for immediate actions , which is a good sign.

Despite many similarities. some also believe that each country has its complex parameters affecting its own risk equations and assessment to a certain degree , many of these are related to social fabric and historical behaviour and culture ... a market crash in AUS or CA does not necessarily mean having one here even with similar towns or market conditions.

While I'm all for natural selection with respect to mortgages I'm ok with the typical default rates. What I'm not ok with is if we end up with excessive default rates that threaten financial stability.

While a house is security for the lender and it works well enough. If things turn bad banks can end up with a porfolio of properties that they need to dump. While some may not think it's plausible it did happen in the US because they had to address capital requirement problems which halted lending and nearly destroyed their banking system. There are solutions to that problem but let's hope it never happens here.

I can understand why you aren't as worried about IOLs but what percentage should we be concerned with 50%, 80% or higher?

Thank you, that is True, when there is a very high percentage of reckless borrowers ( don't know how much really off the total 50% or 80% would be reckless if that number was reached) AND we have a great exit or worldwide economic disaster in a scale of the GFC, then that might affect the whole market and the banks - but for over 40 years we never had a severe and painful decline .... the banks lend to a Max of 37% ( usually 35%) of income, almost all the IOL borrowers are property investors or business owners where there rental incomes are already devalued by 25% for the purpose of income calculation ... etc .... PLUS banks are already very cautious with these guys and they get a health check call ,every 6 months or so, from their account manager to check their situation and their accounts are usually under the microscope !! So there are plenty of early warnings with these type of people. -- My point is that during 1987 and 2007 market dips, only the reckless borrowers or too stretched gamblers lost their shirts -- almost all prudent investors and home owners did not ( well apart from a temporary paper loss)... unlike what happened in Detroit 7 years ago the whole town was wiped off but for very different reasons ,, which some hopeful people are trying to compare Auckland with -- calling for doom and gloom and property falling off cliffs...

I mentioned that countries are different, one of the reasons which saved our bacon in 2008 was that our banks were not too much or directly involved in toxic investment instruments and derivatives etc and i guess everyone is very wary about indulging in such types of cheap money albeit with different forms and shapes nowadays.

And BTW, the economists that I listen to are the ANZ, ASB, BNZ and Westpac chief economists among other realistic people who contribute to banking policies... not some doom and gloom ones with certain obvious political bias and agenda!

The bank economists have no agenda when it comes to mortgage lending

Ecobird , go to the RBNZ website, and take a little look at recent credit growth. When you look at any metric Auckland house prices are overvalued by 55 percent and they will fall by that amount or more. But keep listening to your economists and your understanding of IO loans , keep believing that there will be some plateau, I'm sorry its a cliff , and the 2006 S and P annual report painted a very similar picture in Ireland 2006.

Sorry, I disagree .... My house in Auckland is now valued at 1.2 - 1.3M if to be sold today, A registered valuer valued this house at 600,000 in 2007 ... so let's use a bit of common sense, Is the RBNZ saying that my house should be at 540,000 now ?? or even 900,000 according to QV 2014 valuation? .. why doesn't everyone pay rates on the 55% devalued price then??

There is no cliff, this fantacy only exists in the imagination of the hopeful who have missed a train and don't like to wait for another!!,

No one will allow the market prices to decline dramatically { including RBNZ and S&P } ...sensible governance ( of any colour) will only allow systematic and smooth corrections over a period of time to save everyone's bacon including the ones who are crying blue murder now ! ...

And, what's fancy about IOL is that it allows the borrower to utilise the principle money in an investment instead of paying it to the bank at the residential borrowing rate - Not spending it in any other unprofitable way like holidays or cars ...

So it is useful to people who have investment mentality and destructive to people who dont.

Actually there are massive bubbles in multiple markets. It's not always possible to have a control unwinding and that's why we need a strict focus on financial stability. We also have hidden risks inside our economy and in other markets. We will likely only find out how bad (or good) things are when an event happens.

Stop trying to push your own opinion of where people are financially who have concerns about our financial stability. People who haven't missed the boat are also concerned.

You do realise that most people actually make bad choices in relation to where they put their money. The percentage that invest the money (and get leverage gain) is a minority. Most will buy a flash car instead of being responsible. IOL is a useful tool to those who use it correctly. I doubt that all of the owner-occupiers are as responsible as you are claiming.

well, thanks ... but

"Stop trying to push your own opinion of where people are financially ..." ....

so, putting out a view on this site, as a comment on an article or a response to other comments that does not go very well with most commentators here, is Pushing My Own opinion - well you are right , it is My Own Opinion !! and I am entitled to it ... just like you are to yours ... and entitled to put it up here , just like you are to yours ....

I am one of those people who is NOT concerned as much as others .... some like to paint a gloomy picture and clinging to any piece of stat or number anywhere to prove a point..

"I doubt that all of the owner-occupiers are as responsible as you are claiming"

I am not claiming that all owners are responsible or not ..I was saying let the irresponsible ones learn to bare the consequences of their wrong doing ....instead of punishing the rest who are responsible.

So, if there are few reckless people out there who will hurt themselves because IOL is available ... we should call out or support to ban it ? or make it sound like its a bad thing ? WHY ?? and because of the few irresponsible people all, other sensible ones should suffer?

People make bad choices with car driving, knives, and many other things that can cause harm to themselves and their families .. are we going to call for banning these too?? or is that pushing an opinion too?

I am happy that you agree with at least some of my views - and that is democracy

maybe another read of my comments might make it sound better,

No train missed, selling an Auckland property currently, to ensure I land on platform , before train goes off cliff. Out of interest , how will S&P prevent price falls and indeed the RBNZ . What do you think will happen when NZ residential real estate prices starts falling , S&P will cut and cut hard. No one will allow market prices to decline dramatically, now that is funny

Well done ... and i hope you make a handsome profit and laugh all the way to the bank and back ... and keep laughing at the rest of us when ( IF ) the market falls of the cliff ...

some of us will hang on to what we have just like we did in 2007- 2008 to see them doubling again today - it's a personal choice!

I still think that houses will still be higher in two years time by about 15%

I think, house prices will start correcting ( call it falling coz that makes some feel better ..lol) they might slide down gradually by 5 -15% ( depending on the area, and I am talking Auckland) over a period of few years ... ALL Depending on the continuity of rates of immigration and the supply of new houses as per the unitary plan ( because everyone knows that it will start bearing fruit effectively within 18-24 months) ... then some think that it will oscillate around the new plateau whatever that might be depending on S & D and building costs etc and also inflation because many people's situation will improve too.

If history was to be taken as an example, the same happened in 2008 -2010 -- prices and sale numbers went down by 5 -15% ( didn't even change in some areas) and took off from there and caught up sharply from 2014 -- And that was a real world class CRASH !

some will tell you that is a hoax, sure.. but its just what i saw and it's my Opinion !!

You see, some of us chose to ignore the fact that houses will always change hands, be it at high or low prices .. it is just that the rate of the change might differ depending on the economical weather and peoples personal status. This time it was the immigration ( or I like to call it - the net population gain ) which caused the distortion at a time when supply was strangled ... its not the RBNZ that is sleeping at the wheel, it was the ACC snoring there for years...

never mind, we are now where we are .... and the 25 bp drop in interest rates and Wheeler's comments yesterday just proves that there will be smooth riding of this "Crises" to avoid Overshooting as well as avoid severe Undershooting .. Both are harmful ...the first can help the economy is few ways ( not all) but the second is disastrous and can abolish the economy ...that's why I think no one will allow it to happen ! Just common sense

One last point.. in the property market there is an automatic safety mechanism that always kicks in as soon as prices go down - people stop selling !! ( unless they really have to) and that holds prices around where they have started falling to ... We saw that dampening effect in 2008.

I think house prices will be 15 percent higher in two years time, I think house prices will start correcting sliding maybe 15 percent over a few years. Eco you have confused me, your obviously confused.

Simple mate, you don't seem to like reading long comments

Prices will continue upwards by about 15% in the next 2 years ( average 7.5% a years) ok?

Then once at the peak ( in 2 years) they will slide down by 5 -15% depending on ....

Is that now clearer mate ?

At your service my friend.

IF the right thing were done, and foreigners were dealt to in the housing market, it would correct almost immediately Notice "correct" because allowing them carte blanche for as long as we have has skewed the market, in fact NZs especially Auckland's, housing market, is a false one, as it does not reflect the buying power of what it is intended for, to house NEW ZEALANDERS. The sooner this anomaly is fixed, the better.

Fast fwd to a few months out until election time. The polls will be punishing National and the ever increasing disposessed and rentier class will be backing the parties that suggest anything to smash property prices. By this stage we would already have had many months of President Trump. If you think good old NZ property will still be bubbling along then good for you!

Eco , I'm female , not your mate nor do I need servicing. I'll make it clear for you , At this point in time Auckland house prices have peaked, no city has the extraordinary debt/ income ratios as Auckland. The fall in prices will far exceed your tepid analysis or wishes. .

Eco Bird,

I am just an old fogey,but IOLs make me uneasy. When I bought my first house in 1969 in Scotland, there were no such loans and I don't think they became available until sometime in the 80s,when markets were being deregulated. I would prefer that they did'nt exist and I would also like to see loan to income restrictions.

In my simple world,houses are for living in,not financial instruments,but I am well aware of very old fashioned that is.

I cannot see it as positive that the rate of home ownership is falling. There is growing wealth inequality and that is not good for the long-term health of society,in my view.

Excellent comment there is no benefit to a drop in home ownership and increasing inequality.

There is no inequality in NZ...free schooling, free housing, free medical, in fact I cant think of one thing you need to pay for in NZ?

Although I believe another global Economic event is on the horizon, I believe the prices will only drop or correct by around 20% at their worst in central Auckland areas, higher on the fringes and in the regions of NZ. But as Auckland is transforming into an international city and the rest of the world continues to turn to crap, Auckland will hold its value reasonably well as it continues to be a popular destination to live. Have you been to Ireland? You can't even compare the two! Dublin is grey and old compared to Auckland which is vibrant and green with the beautiful Hauraki gulf. And Dublin didn't have such high Chinese interest either. It did have high migration but it was under different circumstances to Auckland and NZ at the time. Ireland also had a huge oversupply as well. It all goes in cycles so people just need to be ready to ride out the storm that is coming soon. If prices do drop then rents will also drop and it will solve many problems while also creating others. We can't win either way in this situation unfortunately unless smarter measures are taking place.

Maybe you should look out the window today at vibrant, green Auckland.

Have been to Dublin , many times. Vibrant place in 2006 , not bad now, lots of history or is that old . When prices drop , central Auckland will be hit significantly harder than fringe/regions, It will not matter how pretty the Hauraki Gulf is. As you say Auckland is different, I heard that in Ireland in 2006.Credit markets have turned in New Zealand,

Dublin - Vibrant? Guess you only went on holidays/business trips.

Dublin as a place to live was the opposite. Very dark and dreary. Rent was restrictive, groceries were expensive, and work was relatively low paid.

The IRA has a lasting impact on a range of services

- Postal (they would destroy any undelivered packages after 24 hours)

- Banking (limited to how much you could keep in a single account)

Then you had the political scene which was about as corrupt as you could find anywhere.

But in saying that, it was a great night out, and the beer was good.

Auckland is overpriced and it doesn't have the fundamentals of a heavyweight city. We aren't the king of the Asia Pacific region. We're Sydney's runty brother. Won't be the HQ in APAC for global heavyweight companies and 1,000 Nautical miles additional flight distance.

Legislation is what is going to make the Auckland property market fall flat on it's face. If you can't see this coming you're blind.

Nothing exotic about interest only loans, oh dear ..Once again the RBNZ asleep at the wheeler. Will there be accountability when the merry go round stops Another increase in property listings in Auckland.

"Asleep at the wheeler". Nice.

Freudian slip

Asleep at the wheeler .... haha

RBNZ is also acting very slowly - just following their bosses - PM.

Do S & P actually have any credibility?

People or entities use IOL for a many reasons.......paying down principle attracts tax........so reducing one's loan size is often not in the best interests of the business.

When the % of interest-only loans increases sharply in a period of low interest rates then alarm bells should start ringing

Rubbish I can think of multiple reasons why people would choose IOL and maybe it has more to do with people getting more savvy about the financial products and taxation rules available to them.

With the 40% equity rule coming in I'm less worried about investors. It's the owner occupiers with IOL where I see risks. Even that there will only be a percentage of them that are at risk. As the number rises there will be more risk.

What's discussed above is some will be using IOL for business financing. Some people with their mortgage broken into pieces may be lumped in there as well, even though they have have structured their mortgage in a responsible way.

The biggest risk is gamblers.

I don't think there is too much to worry about as many owner occupiers use their houses for IOL for their business as the interest rate is simply cheaper. Banks don't generally allow the IOL practice unless there is some business activity or asset behind the scenes.

Most of the comments against this practice on this site come from people who are not in business and have a poor knowledge of both the banking products/requirement and tax rules......

In regards to the new equity rules coming into effect I think there is another agenda at play so people should be watching the tax take numbers in the next 18 months or so........the flow through will take a bit of time depending on tax filing dates etc but If people have to throw some earnings on the table here in order to get their equity into order some of this will flow through to the tax take.......

This is what our media here should have highlighted instead of blindly talking up the govt/central bank measures and at the same time indulging in house porn daily...Where is the responsible media here ?

Mass media only cares about profit. There's little in the way of investigative journalism or social responsibility.

House porn and people patting themselves on the back is a national pastime.

I just wish I had put more on interest only and would have leveraged even higher, but I have been prudent and done ok, but the credit train has stopped now from the bank so I can't do anything to further improve my properties, I think many landlords will be in my situation...

Now world is talking about child poverty in NZ. The government have mastered the art of denying, lies and manipulate so does it matter to them

http://www.stuff.co.nz/national/83543705/international-media-batter-new…

Number of people in extreme poverty, by continent, from World Bank:

551 Million in Asia

436 Million in Africa

15 Million in South America

5.9 Million in North America

0.3 Million in Europe

50 Thousand in Oceania

vs. Guardian "data" from Stuff speel - "Unicef's poverty definition in New Zealand is children living in households earning less than 60 per cent of the average income, about $28,000 a year or $550 a week. This definition puts around 300,000 Kiwi kids below the poverty line."

Povery is on the run - no wonder Unicef is talking their book.. "Even in 1981 more than 50% of the world population lived in absolute poverty – this is now down to about 14%. This is still a large number of people, but the change is happening incredibly fast. For our present world, the data tells us that poverty is now falling more quickly than ever before in world history. The first of the Millenium Development Goals set by the UN was to halve the population living in absolute poverty between 1990 and 2015. Rapid economic growth meant that this goal – arguably the most important – was achieved (5 years ahead of time) in 2010." The only other metric falling fast than that is Guardian readership - their circualtion is south of 200k.

Has worldwide poverty actually dropped since 1981 or has their DEFINITION of poverty changed ? The rich are getting richer, thats just the way it works when you have the power and control the puppet strings. I see new definitions emerging in NZ like the "Working Class Poor" and more and more people living in garages and sleeping in cars. All of these indicators point to things getting worse and not better for the average person. Wage growth in NZ ? not in my industry and in some industries its actually gone backwards. Sometimes I don't believe figures, its like the weather forecast, a better indicator is look out your window and see whats actually happening.

Perhaps read the link rather than looking out the window? Or perhaps visit a country that actually has poverty rather than a % threshold that ensures the poverty industry has fodder. Inequality is in rapid decline also (read the link).

"The World Bank, which gathers data on income from people around the world, defined absolute poverty as living on less than $1.90 per day. This is measured in international dollars (in prices of 2011) that are adjusted for the fact that people in different countries face different price levels (PPP adjustment). It is also expressed in real terms to adjust for price changes over time. (How these adjustments are made is explained in theentry on GDP data.)"

It is the legacy John Key's government will leave behind. People living in cars

"ALL Depending on the continuity of rates of immigration and the supply of new houses as per the unitary plan ( because everyone knows that it will start bearing fruit effectively within 18-24 months) "

You forgot to mention foreign buyers (Students and Temp Workers) . See below from the Herald.

Foreigners are buying 29 per cent of New Zealand residential properties, not the low 3 per cent reported

Mary Anne Shanahan, a New Lynn-based conveyancing lawyer, expressed annoyance at interpretation of Land Information New Zealand (LINZ) data which shows extremely low transaction numbers for foreigners.

But Shanahan said people had failed to add in foreigners here on work or student visas.

Those people had not been classified foreigners yet they clearly were, she said, because they are not New Zealand residents.

LINZ revealed that foreigners on work and student visas bought more than 8000 properties they intend to occupy and further 4707 properties they did not intend to occupy them.

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11699…

FANTASTIC VIDEO ON VANCOUVER....

http://www.newshub.co.nz/tvshows/story/could-nz-copy-vancouvers-new-for…

,

Eco bird that is your best comment to date. Love it :)

...

I am happy you did, at least didn't mention the student saga this time in yours .. :)

but there is reason for that ... I did post a bitter comment on the QATAR owned Guardian and Al Jazeera about poverty in NZ ... but I decided to take it out .... so had to put the comment that you and your mates liked ....

Covering up Poverty in NZ doesn't make it go away

Yes foreign student buyers are similar in that covering up the fact it is happening doesn't make it go away..

People need to understand that compared to Canada(Van), Australia, Singapore & Hong Kong foreign buyers have ZERO purchase tax and NZ has an open door policy which is hurting kiwis...yes some kiwis are benefiting (investors) however the vast majority are not.

lol, Gosh Joe, I couldn't agree more ....

there is a difference between covering up an issue and manipulating numbers to make it sound like a plague and ruin NZ reputation around the world using lies and exaggerated numbers ... some people wouldn't have a clue how to investigate these numbers and would take the headlines for granted ... repeat these few times and they become FACTS in the mind of the audience / readers ... that is VERY dangerous. We live here we know how many poor we have and WHY ! hand picking a distressed woman and pray on her tears and hardship in that way and circulate it around the world is not journalism ... it is a propaganda ! and it can burn the country with all its Parties ....

However, that aside... you are still missing the point ( as you did in your comments earlier ) and you are fixated on only one issue which you think is the only cause of the problem , Fine ... it is one of the factors Not ALL .... and unfortunately you are not prepared to widen your horizon on this matter to even think about anything else ... so let's leave it there.

I will look forward to your comments on Foreign students tomorrow on any subject .. :)

and wont be commenting on that ....

Cheers National PR Bird

John key has completely ignored foreign demand and focused only on supply.

Then national talk about resident buyers versus non resident yet Canada , Australia Singapore etc focus on citizen vs non citizen

The later classify students and temp as foreign buyers. 32% of buyers in NZ according to LINZ

Supply is tight. My solution helps supply and demand

Foreign and investor Stamp duty on existing homes. Zero stamp duty on new homes. This should encourage more new builds.

What part of that don't you get ?

You're a shill and want to see your 1.3m dollar house to continue surging in value.

Frankly , it appears from my reading of the situation , most New Zealanders are appalled at the RBNZ lack of proactive steps to cool the housing market

Sorry the RBNZ has taken action, it's Chong Kee, who hasn't.

#make New Zealand great again

I had to toss out a family from one of my places...as they did not pay rent for months and the tribunal was unapologetic to the family...giving them notice...what I supplied was a warm, dry house for low rent and they didn't bother to pay the rent with no excuse and will probably go on to another low rent place and stick it to the next landlord....what can I say...this person now might be homeless with their kids, but didn't even bother to try and work it out with me...there are no homeless in NZ but only those that choose to be...

How much is low rent?

how much do you think Guido? what does it matter, take my word for it...

I thought you invested in central Auckland villas, that will retain their value in the next downturn, wouldn't think they would be cheap.

enough that WINZ could cover it...

Interest only mortgages issued by banks need to be stopped as they have elsewhere in the world. Pure and simple.

Investors really no longer need to pay off principal if they have to place 40% down...

There should not be ANY interest only loans, period. It is just a way of preying on the people that cannot afford the loan in the beginning.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.