International credit rating agency S&P Global Ratings has warned of the increasing risks facing New Zealand banks as a result of the continuing rise in house prices.

In a new report, S&P has downgraded its Banking Industry Country Risk Assessment (BICRA) for NZ's banks by a notch, dropping it from 3 to 4, on a scale where 1 is the lowest risk and 10 is the highest risk.

However it has not changed the individual credit ratings of any New Zealand banks.

"In our opinion, economic risks facing financial institutions operating in New Zealand have heightened as a result of continued strong growth in residential property prices nationally," S&P said in its commentary accompanying the report.

"Reflecting the increased risks, we now apply higher risk weights in our capital analysis of the financial institutions we rate in New Zealand, and consequently, we expect forecast risk-adjusted capital ratios for all of them to be lower than would have been the case otherwise.

"Nevertheless, our ratings on all the financial institutions operating in New Zealand remain unchanged.

"This reflects our expectation that despite some weakening in the capital levels of all these financial institutions, their stand alone credit profiles (SACPs) would remain unchanged.

However S&P did downgrade the SACPs of ASB and Rabobank by one notch each, although it did not downgrade the two banks' credit ratings, "... reflecting our assessment of timely financial support from their respective parents, if needed," S&P said.

S&P said the increased risks to this country's banking sector had been driven by "...continued strong growth in residential property prices nationally, coupled with an increase in private sector credit growth."

"We believe the risk of a sharp correction in property prices has further increased and, if it were to occur - with about 56% of registered banks' lending assets secured by residential home loans - the impact on financial institutions would be amplified by the New Zealand economy's external weaknesses, in particular its persistent current account deficit and high level of external debt."

S&P said it had factored into its assessments recent changes introduced by the Reserve Bank to try and moderate the housing market, such as introducing new loan-to-value ratio lending restrictions on residential investment properties.

"We consider that these tools have been only partly successful in limiting the pace of buildup of risks facing financial institutions in New Zealand," the report said.

"In our view, structural constraints such as supply and demand imbalances and continued high migration levels will pose significant challenges to the effectiveness of macro-prudential tools."

S&P said it had lowered ASB's SACP to bbb+ from a-, and Rabobank's SACP to bbb- from bbb, "...reflecting its view that their forecast capital levels will moderate.

"The revisions of the SACPs of ASB and Rabobank NZ stem from our view of increased risks across the banking system in New Zealand.

"We consider that no new significant bank-specific risk, such as any asset quality concerns, have emerged that drive these revisions."

S&P added that the New Zealand banking sector's funding profile remains a weakness despite a modest strengthening of banks' customer deposits and a slight reduction in banks' dependence on external borrowings.

"Net external debt still funds about 32% of domestic customer loans and support from core customer deposits remains limited, at about 52% of domestic customer loans. Partly offsetting these weaknesses is our expectation of funding support for the banking system from the New Zealand government and central bank if needed in a stress scenario. We also consider the country's conservative banking regulation, stable industry structure, and banks' restrained risk appetite remain supportive of the banking industry," S&P said.

"It is worth pointing out countries such as Spain and Ireland as reminders of the impact that rising economic imbalances [such as particular persistent current account deficits and a high level of external debt] can have on a country's banking system."

74 Comments

Is this notice for pre-positioned OBR unsecured bank creditors to initiate a bank run or not?

APRA has already told the Aussie bank owners to get their capital out and raise local unsecured debt to replace it. Read more and more

Bill English must be joking.

"But as a general principle we support inflation targeting and what you see happening around the world is Reserve Banks certainly not giving away inflation targeting - in fact going to extremes to try and achieve inflation targets.

He said it was a misunderstanding that because inflation targeting was difficult and there was extraordinary monetary policy all over the developed world "that somehow inflation targeting is no longer relevant - it's certainly relevant".

Asked if he would be comfortable with official interest rates at zero, he said it was the central bank's job to make that decision. Read more

Yeah Right!!!!!

New Zealand central bank Governor Graeme Wheeler needs to get inflation back to target and some observers think he has “plenty of room” to cut interest rates, Finance Minister Bill English said. Read more

It's been time to get money out for at least a year. If S&P drop the ratings rapidly in one year then the answer will be yes.

Bill English has shown glimpses of understanding if you think back to when he called a debt a debt. He badly wants some real inflation rather than the fake CPI inflation. All those billions of debt that are building up each month are going to have to be repaid in non-inflated dollars at the rate this is going.

That said household debt is getting easier to service, and the effect of the OCR cuts has not fully kicked in yet. It could take another 12-18 months to kick in fully. I've also been talking to a lot of people that are still on floating rates for various reasons. Some of them should really be switching to 6-12 month fixed but are often too lazy or too busy to take action.

I'm not seeing the risks of a near future bank run.

All those billions of debt that are building up each month are going to have to be repaid in non-inflated dollars at the rate this is going.

That reality is already upon us.10 year NZ government bond yields have halved since 2014 to ~2.275% today, leaving the taxpayer to underwrite 4.5% coupon interest payments out to 2027. The NPV cost of the Transmission Gully PPP payment stream has nearly doubled from an earlier estimate of $850 million.

It all adds up to long term deflationary pressure, and it's not just here. All future generations have been sold out by the current Government's financial mismanagement.

It's all relative. Public financial health in NZ is amongst the best in the world. Private debt levels are a worry but there is tons of room for govt to step up and take on more debt, why do you think the nzd is so stubbornly high? Because we are winning the ugly contest.

If the 10 yr has halved since 2014, do we halve the discount rate used to calculate NPV on our rental properties too? (As up have done in your transmission gully calc)

If so then my Palmy properties returning a net 6.5% yield have doubled in value using NPV to value an asset based on all future earnings at a halved discount rate.

Shame so few understand this concept so can't figure out why prices can and will double in places like Palmy.

Bond dealers are totally aware of capitalising future coupon payments today as yields fall, but they also incorporate the cost of position financing in live IRR return calculations to constantly be aware of all cash flows impacts given different borrowing options. Any term fixed mortgage interest rate cash outflows are detrimental to the outcome in a falling rate environment.

Public financial health in NZ is amongst the best in the world. Private debt levels are a worry but there is tons of room for govt to step up and take on more debt, why do you think the nzd is so stubbornly high? Because we are winning the ugly contest.

Public and private debt cannot be high together due to taxpaying citizen funding constraints. Incomes are such it cannot be possible without a so far elusive economic miracle.

Will a government actually allow people with savings in a bank to take a haircut with the OBR. Or will they bail out the ban, as they have previously done. Sure the OBR is there, but will it actually be followed? The OBR has also always been marketed as only being needed 'in the very unlikely event', but the way I see it, it is a 'likely event', and NZ banks have failed in recent history and needed bailing out. If people lost a percentage of their savings due to the OBR, the government will be out, and their will also likely be civil unrest as a result.

That is the big question. Any Government that does allow it is likely to become un-electable? yes, well maybe the cart before the horse scenario. By this I mean the "civil unrest" is already likely to be occuring as there would be significant un-employment and home losses already to cause an OBR, so what's a bit more?

'likely event' indeed IMHO Peak oil guarantees it.

The Government would most likely bail out a major bank but they have claimed in the past that they wanted flexibility, especially after the SCF failure. One approach might be to apply a haircut to bank balances over a certain amount. It's to difficult to say until an OBR event happens and the Government has to make some tough decisions. It any bailout is mismanaged with a major bank our entire financial system could completely seize up.

The general rule is that if people are starving then overthrowing the Government becomes likely so they will likely avoid that. I doubt John Key would want to end his time as PM like one Dutch PM who was eaten by a number of people dissatisfied with his performance.

So why isn't the Reserve Bank forcing the banks to raise the capital adequacy ratios instead of standing by while their Australian owners strip out their capital at time when our rising property market significantly increases their loan books.

It is almost as if the NZ authorities are trying to manoeuvre the banks into a OBR situation?

because politically the banks dont want to and Govn will not allow it?

https://nz.finance.yahoo.com/news/nobody-believes-anything-anymore-why-…

This could be NZ's future if we don't act.

"widespread hatred not directed to anyone in particular, it's like all against all."

Yes I can already sense something like this bubbling.

Horizontal Violence is behavior associated with oppressed groups and can occur in any arena where there are unequal power relations, and one group's self expression and autonomy is controlled by forces with greater prestige, power and status than themselves (Harcombe 1999).

We need to realise who we should be directing our anger at instead of turning on each other

It isnt "if" its when, cant be avoided by moving the deck chairs about as it seems most advocate.

''Partly offsetting these weaknesses is our expectation of funding support for the banking system from the New Zealand government and central bank if needed in a stress scenario"

TBTF..here we come.

The RBNZ is unlikely to be able to support the economy, with the tools at it's disposal, at a rate of growth that is capable of supporting a residential property bubble - global central banks are currently impaired when it comes to such duties - hence the recent public hand wringing calling upon fiscal stimulus to jump start the failed monetary stimulus endeavours.

Can an indebted nation such as ours jump to the task? I doubt it.

New key household financial statistics from the Reserve Bank for the three months to the end of March show that household debt is now at a record high of 163% of disposable income, up from 162% as of December. Read more

Stephen.... How are global Central Banks impaired.... ??

BOE...ECB....BOJ are basically monetizing US $500 billion of Govt spending/debt every month.... skys the limit..!

https://www.richardduncaneconomics.com/qe-is-now-cancelling-half-a-tril…

{kind=link}

Ok.... not really a constraint for trigger happy Central Banks to keep Monetizing Govt debt.???

The only constraint I might see on the long term horizon ...would be inflation.??

NZ will simply ...."follow in the foot steps" ,,,, which gives us a kinda roadmap, here in NZ .... maybe

The only constraint I might see on the long term horizon ...would be inflation.??

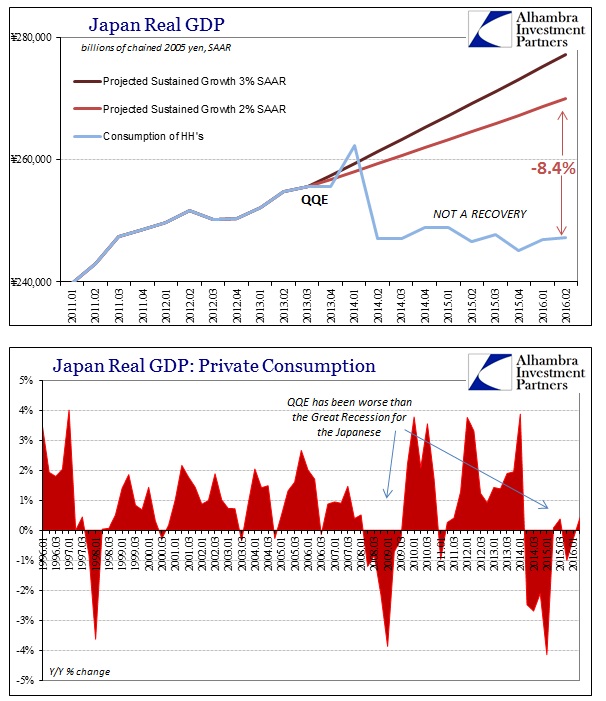

I doubt it - the central bank credits for assets purchased have to offset each other on the respective sovereign balance sheets. Hence the asset seller's proceeds remain moribund on a digital liability ledger. In reality Japanese private credit growth is particularly tame. View graphic

{kind=link}

The immense and swelled holding of bank reserves, as in the US, Europe, and everywhere else QE and its variants intrude, was itself a rejection of monetary policy at its core. In early April, as all these monetary developments achieved critical confluence, Takuji Okubo, chief economist at Japan Macro Advisors told CNBC that, “People are starting to feel the BOJ realized that lowering interest rates further doesn’t really help the economy and there’s significant international opposition to such a move.”

Among the “people” that have figured out the illusion of QE are these financial institutions. Because QE just doesn’t work where it is supposed to, there is no reward to providing the money dealing functions that the wholesale system requires. What banks and previous money market funds were left with was nothing but risk both in terms of economic conditions that never improve (and have gotten worse despite emphatic denials in the face of increasingly unambiguous evidence) but also monetary “easing” in the form of these increasing penalties. Why be in the business of money when there is no upside at all and a more harmful stance to monetary policy? Read more

I doubt it - the central bank credits for assets purchased have to offset each other on the respective sovereign balance sheets. Hence the asset seller's proceeds remain moribund on a digital liability ledger. In reality Japanese private credit growth is particularly tame

Not quite sure what u are saying here.... R u talking about sellers proceeds remaining moribund as reserves held at the BOJ..??

If so... the I'd use the term "potential energy" rather than "moribund"... It can be spent at any time, and is like petrol on a fire, in regards to the potential to create credit ....( if the private sector should ever go an a credit growth binge... )

My view is that QE was about influencing long term interest rates.... and in that regard , it has been a raging success and, in fact, is resulting in ALL yields in ALL asset classes being lowered...

QE a fantastic success ????

Bubbles In Bond Land—-A Central Bank Made Mania,

http://davidstockmanscontracorner.com/bubbles-in-bond-land-a-central-ba…

No doubt about domestic Japanese banks capitalising the value of future government bond cashflows today. I did the same for 16 years in the UK and retired early. Nonetheless, they (Japanese banks) seek increasingly expensive USD financing, to fund business beyond the borders of Japan. The domestic liability chart I posted above is testament to such endeavours. The yen reserves are of little interest.

Transferring wealth from the taxpaying public to wealthy bank bond dealing franchises does not grow an economy for the many.

Duncan has for some time talked about the possibility of direct government spending as a way out of the doldrums. I see the same thing, but perhaps for different reasons. I like the way Duncan tracks liquidity, but I think her weakness is perhaps not understanding the link to resources. Government spending is simply the government taking over the consumption of resources from the private economoy. That results in a step away from capitalism toward a centrally planned economy.

In answer to your comment about credit growth and interest rates made on the 13th, they are opposite sides of the same coin. Supply more money, and its cost goes down. But you are right about credit growth, as I posted on Monday the ratio of GDP to M3 has grown from 1.08 to 1.43 in the last 10 years. In the 1970's M3 was less than GDP (probably because of velocity, which shows that even in the 70's there was a lot of money being used for trading assets, or financial investments, rather than goods).

Chickens are coming home to roost

ANZ said prices bubble

S&P say bubble

RBNZ say bubble

John key this crisis is on your watch

You can't blame anyone

Prices up 85% in 4 years. Shame on national

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11699…

A third of Aucklanders have considered moving out of the city as it becomes increasingly unaffordable, a new survey reveals.

Experts say the trend could leave the city short of workers such as teachers, nurses and police who can earn similar salaries in more affordable cities.

That's why shortly, we'll see John introduce the next tax payer subsidy to keep the ponzi going - higher pay rates for the above professions you've mentioned.

Let's not forget, this is the best salesman we've ever had.

I considered it before deciding that it was a terrible idea for me.

Yeah mate many of the recent open homes in Palmy I've been to has had at least one auckland nurse or teacher who has flown down to Palmy for the weekend. Big hospital and education hub both growing strongly are attracting teachers and nurses from auckland. Hamiltons gone from 300k to 550k for a 3 bed for this reason. Palmy is very similar, better in some instances with more govt. departments being close to welly. You'll also be paying 30% more to buy in Palmy in 12 months time..

move out to where exactly? no jobs, no move.

It is interesting how the government is distancing themselves from the water crisis in the north island, and putting the responsibility on the council. I suspect they will also distance themselves from any banking crash, and put the blame on other parties. The problem is that if there is a banking crash, there isn't really going to be any one organisation to blame, as there isn't really one thing that caused it. It was a whole series of things which caused a perfect storm. The government policies on immigration, and allowing foreigners to buy NZ houses though IMO hasn't helped. They are saying that many are NZers returning to NZ but that is just spin, as most aren't.

its very easy for the reserve bank to halt this debt explosion. they could get the banks to recapitalise, and secondly put a max limit on external (offshore borrowing). This would stop the Aussie parent banks stripping out profits, whilst preserving our capital base. So what if this slows down the fate of expansion.

it is a shame we have a trader and not an accountant running NZ

Don't gamble on NZ's future john Key .... Short term election wins against long term pain for ordinary kiwis

hold on we have an accountant in charge of immigration who can not see any problems and whose Ponzi scheme is helping fuel this mess

http://www.newshub.co.nz/politics/immigration-scam-corruption-organised…

Immigration Minister Michael Woodhouse admitted that "hundreds" of students could be here illegally.

"It could be - I don't want to put a figure on it."

Your company has made a profit. I don't want to put a figure on it but I balanced the accounts on the scales and the receivables weighed more.

Agreed however all the government ministers and departments dare not cross Key..... so Michael is purely a puppet in his role

Gdp growth requires

Strong immigration (tick)

Booming property sales (tick)

Gdp per capita (nothing to see here )

Banks have put well over 50% of their eggs into the ponzi housing bubble basket.

When combined with the nonsense that is OBR this is an accident waiting to happen. The banks know it, S&P knows it, RBNZ knows it and, despite their protestations otherwise, I suspect Key and English know it.

However, the "do nothing and hope" approach (a recurring theme of this Government) appears to have won the day. New Zealanders have been badly let down by the self-serving manner in which they have handled this crisis.

The big issue for NZer's here is the OBR, another douzy under national's watch. If the banks get in trouble some creditors can be paid out before depositors. Depositors funds are now at more risk. In comparison most other developed countries have insurance over deposits, we have the opposite, favourability to creditors

Depositors' funds are certainly at more risk with the draconian OBR. What's more there is no deposit guarantee scheme in place in NZ for depositors whereas in Australia the "Big Four" banks that are here guarantee their depositors funds up to $250,000. Win win for Aussie depositors at our savers' expense. We're like lambs to the slaughter and this Government is doing nothing to stop it.

Yes it's a shocker for NZ bank depositors....see point 4 in OBR, link below, depositors still have a legal claim to their frozen funds as "unsecured creditors". Meaning secured creditors and employees claims rank in front. And point 8, no deposit insurance. Thanks national!!

http://www.rbnz.govt.nz/-/media/ReserveBank/Files/regulation-and-superv…

So who guarantees the deposits? surely it is even more draconian to expect the tax payer to cough up the losses? At least the depositor has the choice to stay in a deposit or leave.

if you dont like the deal, well take your money somewhere else.

We don't expect the tax payer to cough up. I am sure savers would be prepared to pay for the deposit guarantee by way of a small annual premium. This would be much better than losing part of their hard earned savings. NZ is now the only country in the OECD with OBR and that is draconian. The OECD in 2013 urged the NZ Government to offer a bank deposit insurance, but this has fallen on deaf ears. NZ depositors should not be asked to prop up banks which are making $millions in profits. Where would you suggest depositor's take their money then??

brilliant comment. Thank heaven someone who understands what's happening and can communicate it. Big ups to you missy5248.

Australia, up to 100k

NZ is 0. Even worse a lot of creditors and employees can line up in front and take depositors money. Crazy. Wake me up.

Follow this link to see details of the Australian Deposit Guarantee scheme. http://www.apra.gov.au/CrossIndustry/FCS/Pages/fcs-adi-html.aspx

This scheme not only covers banks, but also Building Societies, Credit Unions and Foreign Subsidiary Banks up to $250,000 per account holder.

There are 100 or more Australian financial institutions covered by their deposit guarantee scheme and the $250,000 guarantee is per account holder per bank allowing spreading of risk. And if you have a partner, he or she can have accounts in their name which are also guaranteed.

This scheme will prevent any run against any specific bank - unlike the NZ situation with no guarantee of any sort and a small number of banks. OBR will encourage and enable a major disruption in the whole NZ financial system should one bank be even rumoured to have difficulties. Unintended consequences are easy to spot with the NZ OBR system all of which will reduce financial stability of the country.

The NZ OBR situation is unique in the world and greatly flawed.

At least in Australia you know the "rules of the game" and are able to arrange your affairs to protect your savings. New Zealand depositors however do not have any such protection for their funds. Depositors can lose a portion of their funds (known as a "haircut") - the percentage and deposit level to be determined according to funding required. As an example, Cyprus had an OBR system in place when there was a bank failure in 2013 and the "Troika" of creditors agreed the final deposit levy on Cypriot accounts was 47.5 percent for shareholders, bondholders, and depositors with more than 100,000 euro (Approx NZ$150,000) in the two largest banks. In NZ there is no protection for savers in a bank, credit union or building society.

Well said missy 5248,

I am of the generation which the banks did not “lend” money to. The only way I could finance a mortgage was the big lawyer's finance fiddle which every so often you had to refinance.

The Muldoon generation came along and told me I would have to save for my retirement as there would be nothing to give me a pension. I did and now on low-interest rates that give me an income that “just” covers my outgoings, we are expected to finance any bank failure after they have made excessive profits. I don’t expect the taxpayer to bail me out, but I also don’t expect to bail out banks.

Why is it those who have benefitted with readily available mortgages are not also liable to pay for any bank failure.

As a pensioner without the years on my side to earn further income, if there is a bank failure, like missy, I would also like to know where Steven thinks I should put my money to avoid the OBR.

And just where are most ordinary depositors supposed to take their money? As another contributor has said,a deposit insurance scheme would spread the cost widely and would,I believe,be eagerly welcomed by most depositors.

I regard myself as reasonably financially sophisticated and have deposits in several banks as insurance,but what else can or should I do?

NZ corporations are pulling the strings....

when you get headlines in the media that the banks not passing on the cuts is good news you know you are in trouble (cheers Bernard)

Banks can take excessive risks as they know the government will bail them out or provide guarantees for them when the sh*t hits the fan....

Banks cannot take excessive risk and you are deliberately spreading nonsense in stating this. For a kick off the banks are all registered companies in NZ they must abide by the rules and regulations set out by the Companies legislation and part of those rules means that you are not allowed to trade when insolvent. Then the banks have to meet the RBNZ requirements as well. The fact is banks aren't allowed to use all their capital in business activity, imagine if e.g. A dairy farmer was only able to milk 3/4 of their cow herd!! The banks like any other company have the right to take the profits off the table and disperse to shareholders. Many people ranting on this site would prefer that NZ becomes a communist state with Government owning all business activity..........maybe consider that it would still be your taxes bailing out the banks if they failed under that type of system.

Excessive risk that leads to insolvency would mean a few bank directors would face prosecution for their actions. However like the leaky building fiasco if a failed bank was following all regulatory requirements imposed then the of course it is the bureaucracy who led them to failure so of course it will be tax payers bailing the failure out. You cannot have freedom and restrictions operating at the same time.

Gee imagine if that farmer could fractionally reserve his cows, then he could own one and milk nine. Then if he could leverage it in real estate at a 20% LVR he could milk 45 cows. If course 44 of those cows would be imaginary.

uh isnt that what a mortgage is?

S&P - always good for a laugh. Stand up comedians that missed the GFC.

They didn't miss it, so much as ignored it due to conflicts of interest around receiving payment for ratings assessment

They were kind of accomplices in GFC, along with other rating agencies.

Ratings agencies are very quick to rerate when there is good news but very slow on the downside.

As they have now downgraded NZ banks how bad is it?

In the words of the immortal Fred Dagg - "We don't know how lucky we are..."

"So if things are looking really bad

you're thinking of givin' it away

Remember New Zealand's a cracker

and I reckon come what may

If things get appallingly bad

and we all get atrociously poor

If we stand in the queue with our hats on

we can borrow a few million more."...

S&P should be rebranded S&D ...... SLEEPY and DOPEY after the two dwarfs in the fairy-tale

They have a penchant for being asleep and stating the obvious after the fact

IMO at some stage the bubble on this unsustainable market is going to burst. Really the question is who is going to be the most affected by it. I have been watching over the last few years banks credit ratings getting downgraded. That is a major concern IMO. Our banks aren't as safe as they once were according to the credit ratings.

This is exactly what I have been going on about:

Foreigners are buying 29 per cent of New Zealand residential properties, not the low 3 per cent reported

Mary Anne Shanahan, a New Lynn-based conveyancing lawyer, expressed annoyance at interpretation of Land Information New Zealand (LINZ) data which shows extremely low transaction numbers for foreigners.

But Shanahan said people had failed to add in foreigners here on work or student visas.

Those people had not been classified foreigners yet they clearly were, she said, because they are not New Zealand residents.

LINZ revealed that foreigners on work and student visas bought more than 8000 properties they intend to occupy and further 4707 properties they did not intend to occupy them.

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11699…

I wonder if things like the Chinese property website, Hougarden, touting for listings via radio advertisements helps in keeping this "market" propped up. Of course, they could just be a figment of my imagination, eh?

She blamed the media and the Government for failing to examine the data closely enough and interpret it correctly.

And also...

"The New Zealand Herald has in its editorial quoted the 3 per cent number with the indication that those of us who know the number to be higher are xenophobic. This issue needs to be raised. As the Herald has put an awful lot of information about the current property bull market on the front page, I believe the analysis of these figures belongs on the front page. The general public has a right to know," Shanahan said.

John Key - come out of denial

https://www.tvnz.co.nz/one-news/new-zealand/admission-id-happy-if-value…

I imagine he's having a lovely swim in it, seeing as few of our rivers are up to scratch in that department any more

As Roy1 says Mr PM - Come out of denial

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11699…

Shame John Key and his gang for manipulating data and facts.

Who wants our country being run by manipulative liars.

National PR spin backed by the media and large corporations....

ignoring 13,500 foreign buyers that were students or temp workers

The problem is 29% doesn't include any foreign buyers using Trusts or Companies so the figure is likely to be much larger.

No surprise if this is an issue in Canada and Australia why would NZ be immune to foreign student buyers and temp worker buyers after all we have

96,000 foreign students

207,000 temp workers

Joe public what else should we expect from manipulative liars. Do not like saying it for people whom we voted but they are not embaraseed being shamelessly egoistic arrogant but we are of electing them.

Truth hurts but has to be highlighted. Our leaders (if we can call them leaders) are not ashamed of not doing anything than why should people be ashamed of highlighting it.

anecdotally i have heard that the banks have pulled back big time with respect to any large scale property development. whereas 12 months ago they were jumping on any proposal, they are currently binning 90%. This shift came about after the rbnz introduced the 40% lvr rule, which has altered the risk matrix massively.

If this is the case and I have no reason to doubt it, supply will almost certainly dry up in the foreseeable future.

This will also result in a massive flow on with respect to the construction sector, lawyers, architects, and retail sector that supply housing related goods.

My prediction is that the housing market will become "locked" for a number of years, and prices will stagnate. That is unless some other economic "event" rears up its ugly head. Then all bets are off.

Even in Canada was same story - politicians deny, lie and manipulate but atleast better sense prevailed and the govt acted by imposing tax on foreign buyer and the result is for all to see.

http://m.huffpost.com/ca/entry/10872994?utm_hp_ref=canada-british-colum…

Nothing is silver bullet but why be afraid. For people manipulate and lie only when have something to hide.

Result of Tax on Foreign buyer - not silver bullet but Golden Bullet

http://www.zerohedge.com/news/2016-08-18/vancouver-housing-market-implo…

It is a totally naive conception from unlearned 'want to be' economists to think that lowering interest rates makes people spend more (bringing more inflation). For me I spend less because I know my money will be less in the future until interest rates go up again when I'll not be digging into my principal as much. All the lowered rates are doing is promoting the housing crisis combined with unfettered immigration. When will the RB employ some actual 'real world' educated economists before making decisions.

Not only that, how is the govt. going to control the financial collapse when interest rates go up and people can't pay back the loans which are already way past servicing. Take it out of my savings in my uninsured bank account to pay the borrowers I guess, after the bank gets ITSELF into trouble. Such third world policies have been the downfall of so many third world countries it really begs to suggest that certain drugs have already been made legal in govt. offices because they live in total unreality.

The reserve bank is grasping at straws in a game that has gone way past their ability to play.

It's been asked where you should put your money. With much of the world now in negative interest rates and the rest rapidly following the big money is going into physical precious metals and precious metal mining shares. Hardly rocket science.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.