By David Hargreaves

Everybody's doing it to some extent, so it seems.

The 'everybody' are the banks and the 'it' in this case is interest-only lending for residential mortgage customers.

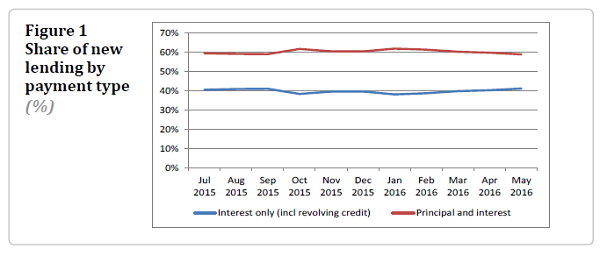

The Reserve Bank recently lifted the lid on the extent of interest-only borrowing in this country, with new official figures revealing that around 40% of new mortgages by value are being taken out on interest-only terms.

The RBNZ has been collecting the information for over a year but has not previously published it.

The figures for May show that $2.996 billion worth of interest-only loans were taken out, which represented about 41.1% of the $7.287 billion worth of mortgages advanced.

Regulators in Australia became concerned when interest-only loans hit more than 40% of new lending across the ditch.

In December 2014 The Australian Prudential Regulation Authority (APRA) warned lenders it was "dialling up the intensity" of its supervision to reinforce sound residential mortgage lending practices. And the Australian Securities and Investments Commission (ASIC) said then it would "conduct a surveillance" into the provision of interest-only loans.

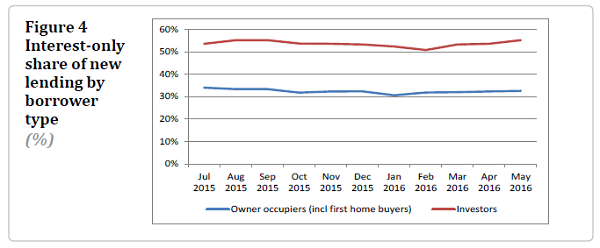

The RBNZ said that in terms of the whole country, in May 2016, over half of new lending for investor purposes was on interest-only terms. The RBNZ said these proportions have been fairly steady over time. "Only 1% of interest-only lending for investor purposes is above 80% LVR and this has been declining over time," the RBNZ said.

The RBNZ says interest-only loans are defined as having no scheduled repayments. This includes loans where borrowers independently choose to repay principal such as revolving credit loans which have a fixed limit.

The RBNZ said in May 2016, almost 60% of all new mortgage lending was on principal-and-interest payment terms, while 40% was on interest-only payment terms.

Westpac NZ last week announced it was reducing its interest only lending term from 15 years to a maximum of five years "as investors continue to dominate the housing market".

Simon Power, GM Consumer Bank and Wealth, said the reduced term for interest only home loans was to provide customers with a check point at the end of the interest only period to assess if they were still comfortable with and able to meet their obligations.

“With the way market conditions are we see this as a prudent and timely move. The last thing we want is for customers to overstretch and get into difficulty while interest rates are at historic lows,” Mr Power said. “This gives the customer the opportunity to reassess their needs and financial situation.”

Intrigued as to what the wider market situation was, interest.co.nz approached eight big banks to see what their approach was to interest-only lending.

We asked them all the same questions, specifically:

How widely is interest-only borrowing available to your customers?

What is the maximum term you offer interest-only for?

What is the requirement regarding repayment/renegotiation of the loan at the end of the term?

Are different terms/deals available depending on whether you are an owner-occupier or an investor?

Could you outline those differences/terms please?

The response is that they all do interest-only to at least some extent and mostly on similar terms and conditions. Westpac's previous 15 year limit very much made it the 'market leader' in terms of length of interest-only. Now that title goes to the biggest bank, ANZ, with 10 years. The BNZ says its general maximum is five years, though "under special circumstances, by exception" it might too allow up to 10 years, while ASB says "in general terms" it's maximum is five years. This suggests too that maybe if you ask nicely you might be able to get it for longer.

| Bank | Availability | Max Term |

| ANZ | Yes | 10 years |

| ASB | Yes | 'in general terms' 5 years |

| BNZ | Yes | 'in special circumstances' up to 10 years |

| Co-op Bank | Yes | 5 years |

| Kiwibank | Yes | 5 years |

| SBS Bank | Yes | 5 years |

| TSB Bank | Yes | 3 years |

| Westpac | Yes | 5 years (recent change from 15 years) |

Banks can be fairly coy about how much of respective types of lending they do,although with the RBNZ collecting increasing amounts of data from the banks these days, more and more industry-wide information is available.

We know for example, based on those new figures from the RBNZ, that while lending on interest-only terms is running at about 40% of new lending, as far as banks' total outstanding mortgage lending is concerned, it as of May made up about $60.8 billion of the $213.7 billion outstanding - that's about 28.5%.

Volunteering information

In responding to us, just two banks volunteered information about the extent of their interest-only lending.

BNZ said its proportion of interest-only lending was "significantly lower" than the RBNZ's stated 41% for the whole market in May, while Co-op Bank said currently interest-only lending made up just 10% of it's mortgage portfolio and this figure included revolving credit facilities.

SBS Bank said the "majority" of its borrowers were on principal and interest payments.

"In the current low interest rate environment, residential borrowers are generally taking advantage of low interest rates by increasing their principal repayments to reduce the term of their borrowing. Interest only borrowing is more widely used by borrowers that are able to claim interest costs as a deductible expense for taxation purposes, such as property investors," SBS said.

Different offers and terms?

We wondered whether banks were more inclined to offer interest-only terms to property investors, rather than owner-occupiers - but they say not and that it's equally available and on the same terms.

Co-op Bank said: "No the terms are not different however owner-occupied tends to be for the period of a construction loan before reverting to full principal and interest or bridging finance period."

ASB said it considers requests for interest-only repayments on a case by case basis taking into account a range of factors, the most important being that customers can afford their loan repayments comfortably on a principal and interest basis.

"Where this is the case, interest-only repayments are an option available to any of our home loan customers based on their individual circumstances and reasons for wanting interest-only repayments."

TSB Bank said most of its interest-only activity relates to investment situations.

"In these cases the interest only term will be for the maximum period of 3 years. If the facility remains within current credit criteria and there have been no repayment issues we will consider extending the period of the interest only facility.

"The majority of owner- occupied interest only periods would be for specific purposes and limited periods of time on a case by case basis.

"In all situations, as required by the responsible lending code, we would have to consider whether the loan was in the best interest of the customer, and whether there was a workable exit arrangement for clearing the debt."

What about at the end?

Which does bring us neatly to the question of what happens at the end of the interest-only period. Problems have been caused in places like the UK where customers have been required to repay loans at the end of their interest-only period and not been able to, and then not been able to refinance.

According to the answers we got, the majority of the banks' interest-only loans here simply switch to principal and interest repayment terms for whatever the original term was of the loan.

ASB said it's considered on a case-by-case basis, taking into account the customer’s particular circumstances at the time and subject to normal lending criteria. "This includes ensuring that customers can continue to comfortably afford their loan repayments on a principal and interest basis." Westpac also said its decision on what happens at the end of the interest-only period is "case-by-case", or "customer-specific".

BNZ said: "At the end of a term, say five years, a customer’s loan will automatically roll back to a principal and interest repayment structure. If the loan was originally for a 25 year term, the payments are recalculated and spread out over the remaining 20 years.

'Careful consideration'

"Any extension to an interest-only loan is carefully considered in a conversation with customers on their specific needs and circumstances. We calculate all interest-only home loans on the basis a customer can service both the principal and interest through the life of the loan."

Another set of monthly interest-only figures are due out from the Reserve Bank before the end of this month. Doubtless the central bank will be watching closely for any marked upward blip in the figures.

Reining in interest-only lending would be presumably one measure the RBNZ could consider to rein-in the fast rising house market. There's no suggestion at this point though that such a move is among the macro-prudential measures currently under urgent consideration.

*This article first appeared in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

38 Comments

a very dangerous lending practice that relies solely on GC I hope they are charging extra bias points to reflect the risk

it has shades of the finance companies about it and we know that ended well

In June more than 50% house were bought by investor as most FHB Kiwi buyers have given up in Auckland as out of the balance 50%, non resident will be about 35% to 40%, people down sizing or upgrading will be 10% to 15% and any left will be actual Kiwi FHB.

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11677…

One should not bend stick to such a level that it breaks. This is what has happened to FHB species which will soon be extinct in Auckland.

Thanks to JK and his legacy.

Good or Bad future will decide.

Interest-only loans only add fuel to the fire... Could this be the intended consequence?

If there was a desire for reigning in the exuberant property market, amortization of loans would be a harmless solution in the short run and a mayor benefit, for home owners and the economy, in the long run. However, rampant investment and the consequential capital gains due to price appreciation are good for the tax base. We should brace for higher rates in the near future and a capital gain tax in the medium term.

Meanwhile, let the party rage and rumble, and expect a doubling in prices before the end of the decade.

I agree with much of your comment. Your prediction of a doubling in prices is not based on past history, however. Cheap loans show the housing bubble is ready to burst; and a capital gain tax, if done right, could be the pin to induce the necessary correction in values. If the family home is exempted, or if there is no lead-in period for the CGT, that would encourage prices to appreciate as you predict.

So renting from a bank is popular as long as the perceived cg continues. What a warped desperately non productive economy we are driving.

OMG. This is exactly like the sub prime mortgage issue in the USA!!!!!!!!!!!!!!!!!

Its not "exactly" like it at all. There are some big differences. One being the LVR requirements for a start.

The ugly truth is we are collectively insolvent, so the banks are by default insolvent.

Most investors with Interest Only will have positive cash flow and massive Capital Gains are just a side affect of a badly skewed market.

How many houses are bought and financed with Interest Only, negatively geared, clearly for Capital Gains only?

IRD should be requesting the info from the banks and interest only loans to me have an intention GC for a private investor so should therefore be taxable on the gain

How come people only talk negatively about property related interest only loans and their ability for tax deductions? You can get interest only loans for other type of investments as well. You can buy shares from that loan and get tax deductions for interest payments. That is a common knowledge. Investors expect capital growth in shares they purchase using interest only loans as well.

You're desperately trying to justify an ethically wrong position and comparison. Apples with oranges man.

Can you live in a share portfolio? Homes are "needed" by us all to "live" in, lead productive lives, bring up families.....etc

They are not an object or exist to just speculate on for pure selfish greed using other people's money.

if you cannot buy a home you can rent and satisfy your basic need (a roof over your head). You do not need to buy a property to live. BTW, the point that I am making is you cannot say interest only loans are bad for one type of investment and good for another type of investment.

PS: See my comments regarding interest rates. I think property investors should be subject to commercial rates. Its pointless criticizing the fact that they get interest only loans.

Yeah, again you are not really getting it. The ONLY reason someone would take out an IOL is if they wish to pursue it from a pure speculative cg advantage only.

It applies to all types of investors who take IOLs. Not just property investors

Again, you really are playing ignorant on this one. You are not an "investor" if playing in IOL's, you are parasitic "speculator" and most mainstream banks won't go near you UNLESS it's to fuel property speculation cause banks don't really give a toss as long as they get that interest slice of a pie.

Go to your bank and try asking for a IOL to purchase a dairy farm or any product based business? Good luck getting the same rate as a Property... speculator.

You are very incorrect when you say you cannot get Interest Only loans for any business other than property investments. Again you are ignorant enough to ignore my stance on commercial rates for property investors. You can get Interest Only Loans for businesses. Banks openly advertise those products. Many people get IOLs to maximise the cash-flow in initial years. We also have such a facility from A-Z but at a commercial interest rate. We also get tax deductions every year for interest payments. The bottom line is IOLs are not bad at all. It helps to improve the cashflow and its cheaper to use that cash to develop your business if your business is growing well. But again all the businesses (property investors, shares investors) should get commercial interest rates as I stated several times.

Really Justice. Do you really think an 'interest only loan' can conceivably have only one reasoning behind it.

Yes, no other reason not to want to try and pay principal if wanting to own. Perhaps you could give me and others some actual examples of why anyone would be 'dumb' enough to take out a IOL if.....IF...not expecting to solely capitalise on the speculative cg and tax advantage?

You certainly are of limited imagination Justice. You want an example here is one. I recently bought a commercial building for my own use. 100% financed, secured over other things. But I hate debt and will repay this completely over two years or so. I can dump a big amount of cash into it each month and a couple of times a year along comes a lumpy windfall so I knock that off the loan as well. It's interest only.

I am doing this because on a cash basis it's much cheaper than leasing premises, I have control over the setup which is useful for that business, and frankly I just like to own stuff.

According to you I am 'expecting to solely capitalise on the speculative cg and tax advantage'. Your thinking is self limiting Justice

KH - I'm pretty new to this game, but what do you mean by 100% financed and yet you're taking a loan from the bank? Are you buying 120% of a property?

So you mean it's not 100% financed...? I'm confused about the terms you're using..

Independent observer. Heres an example. Lets be clear tho its not my own exact situation.

You own about ten million worth of property. No debt. One property is a farm worth five million. It works out there is a building you would find useful. You buy it one million. You find the cash by raising a loan one million with a mortgage on the farm.

Another. You own ten houses worth 500K each. You want eleven (greedy) You increase the current mortgage of 50K on each house to 100K. Buy number eleven with cash.

If you are have equity this is plain and simple business. If you are one of those crazy Auckland borrow and hope dreamers it's quite possible to build a disastrous house of cards.

really in essence you are agreeing with justice

Not at all Mr imhenry. Justice has the view that people would only do interest only loans for speculation and capital gain plays. He can see no other reason. I gave him a couple of straight examples of other reasons

People need HOMES not just a roof over their head, that is what we seem to have lost sight of.

Can you imagine walking into a bank asking for an interest free loan to fund your speculative share investment portfolio? Good luck convincing the bank, plus even if you got your loan it would be at the bank's higher business interest rates.

Whereas walking into a bank to fund your speculative investment property you'd be treated like a king! Cash advances, a competitive interest rate and the bank's rubber stamp ready to approve.

Agree with you in terms of interest rates. The property investors should be subject to commercial rates. That's what should be done. Its pointless beating interest only loans.

That is what RBNZ may think of imposing next, higher interest for property investors, along with debt to income ceilings...

you can already do margin lending on shares at ASB securities,

https://www.asbsecurities.co.nz/section35.asp?

There are all sorts of Flexible Finance / Margin Lending / Revolving Credit (all IO) products by all the main banks. The point is, they are generally priced for risk. Same can't always be said of IO / Revolving Credit for Residential Property Investors

Government too knows the consequence of all this but the intent is missing from government to actually control the housing market (not Crash but control or many will panic) for if done in a control manner, may be the result is not as bad as it would be for the government can only delay the inevitable by ignoring and not taking any action.

High time that government comes out of denial and take responsibility as that is what most Newzealanders want. No better opportunity than now to act along with RBNZ.

Policy is to blame here. Interest only loans shouldn't be there in the hope you profit off the CG.

There is a lot of headline thinking here, but 'interest only' covers a wide range of very different things. Certainly there are situations where it is interest only because the borrower is stretched to the max on cashflow, thus a very dangerous thing. But there are also loans where the borrower is technically on interest only, but also has capacity to repay capital at a high rate, and is.

If there is negative gearing mostly it will be claimed as a tax loss. So the IRD will already know about it, which owners and which properties. To me it's clear that anybody claiming a cashflow loss is in the business for only one reason and that is to make a capital gain profit.

So if the IRD already knows who they are, and that the purpose must be capital gain. It should not to too hard to connect the dots and apply capital gain tax. I think they already are.

Maybe the IRD are tooling up? They have a massive new IT project underway and I bet this little baby will be able to do a whole lot more. At present they are hamstrung by old tech, but for obvious reasons are not advertising it.

We really do have a fragmented , uncoordinated approach to this housing crisis don't we? The RBNZ is doing one thing , the Government has , until recently been in denial , and the banks continue to do anything they want to grow their lending book .

If anything , the banks should be cognizant of the risks of interest only loans on their books

The Banks know they are TBTF and will be bailed out when the crash comes..Especially in NZ with only few players you can count on the fingers of one palm.

I for one will be out in the street partaking in violent civil disobedience if the banks are bailed out....

there's no way they should be bailed out, they've gained hugely from the bubble, if it crashes then they crash too. That's business.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.