One of the great recent innovations from the data wonks at the Reserve Bank has been their mortgage market reconciliation, C35.

There is a lot of data around that reveals key aspects of this market, but C35 ties it all together.

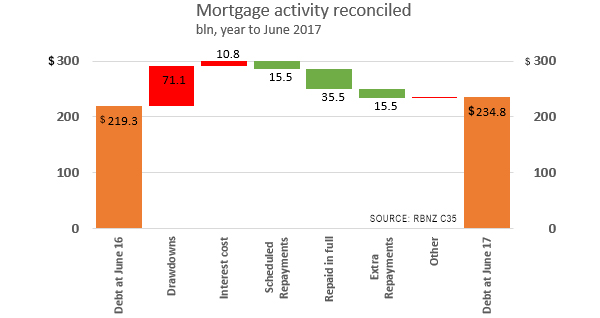

In the year to June 2017, banks charged (earned) $10.8 billion on a mortgage book that averaged $227.4 bln over the period. That is an average interest rate of 4.75%, which you have to say is surprisingly low. That is down from 4.91% in the year to March 2017. It would be easy to assume it would have been a little higher than that given that many borrowers would not have been able to score the best rates on offer for a whole series of reasons.

Our average in the same year across two year fixed carded rates was 4.64%, those for one year was 4.51% and for floating was 5.65%. To get a system-wide average of 4.75% must have involved substantial discounting from carded rates for most prime borrowers.

Borrowers benefit

So the conclusion can only be, banks competed hard on price and almost all borrowers benefited from that competition.

To give the scale of the consumer benefit, in the previous year to June 2016, they charged $11.5 bln in interest at an average rate of 5.46%. In the year to June 2015, the interest charged was also $11.5 bln at an average rate of 5.88%.

Home loan borrowers saved $0.7 bln in interest costs in a year.

That made payments easier to make - so house buyers bid up prices. And took on more debt, on the basis the payments were 'affordable'.

"Loan drawdowns have been rising" ... er, that may have been the assumption, but it turns out it wasn't true. In the year to June 2017, these drawdowns amounted to $71.1 bln which is down from $75.4 bln in the previous year which was the highwater mark. The rate of loan drawdown started to decline in the June 2016 quarter and have been steadily slipping since then.

And then there is the rate at which we are paying these mortgage loans back. Believe it or not, we have been upping our regular (scheduled) repayments. The just under $4.0 bln repaid in the June 2017 quarter is the highest in this RBNZ data. (And that is true even if you adjust the data for the tiny level of repayment 'deficiencies' recorded in the system.) That is $15.5 bln in scheduled repayments in the full year.

Who would have thought?

But borrowers make more than just scheduled repayments - and those additional repayment levels may well surprise you. Regular, scheduled repayments are $15.5 bln per year, but other excess repayments are almost as much, and amounted to just under $15.5 bln in the year to June 2017. Apparently, on average, borrowers are making actual repayments at twice the rate they are required to in their loan documents. Who would have thought?

And before you ask the question, those additional repayments do not include paying off the full loan when you shift from one borrower to another (or when you make that final payment to become mortgage free). Those types of repayments are captured separately in this RBNZ data reconciliation. Those 'repay in full' amounts total $35.5 bln in the year to June 2017. Interestingly, that is the lowest annual rate since September 2015, which suggests that we are not switching institutions at the rate we once did. Lenders are doing a much better job of retaining clients even when faced with competitive pressure. This behaviour also supports the tightening of the interest rates charged.

Knowing this data for mortgages allows us to derive what banks are doing with lending for loans other than for mortgages.

| year to March 2017 | Interest charged |

Mortgages (average) |

Other loans (average) |

Rate (average) |

| $ bln | $ bln | $ bln | % | |

| - ANZ (GDS and G1) | 6.234 | 65.189 | 50.855 | 5.37 |

| - ASB (GDS and G1) | 3.988 | 49.527 | 25.682 | 5.30 |

| - BNZ (GDS and G1) | 3.767 | 35.166 | 40.651 | 4.97 |

| - Kiwibank (GDS and G1) | 0.826 | 15.968 | 1.313 | 4.78 |

| - Westpac (GDS and G1) | 3.974 | 44.838 | 30.888 | 5.25 |

| - All others (difference) | 2.325 | 9.391 | 14.862 | 9.21 |

| Total interest charged by all banks (S21) | 21,114 | 220.079 | 164.251 | 5.49 |

| Total mortgages (C35 and G1) | 10.805 | 220.079 | 4.91 | |

| All other lending (difference) | 10.310 | 164.251 | 6.28 |

Banks may be incentivised by the capital adequacy rules to prioritise lending for mortgage lending, but there is no getting away from the fact that home loan borrowers have benefited from this by being offered lower interest rates - and those benefits are substantial.

14 Comments

We should all feel very queasy to note that mortgage lending grew by 15.5B, or 7.1%, a growth rate significantly greater than the growth of incomes.

You are right, but the difference may be a bit less than you think. According to StatsNZ, (QES table 5), gross weekly eranings went up from $1,696.30 to $1,777.80 in the year to March 2017. That is a rise of +4.8%. What is happening is that wage rates are going up only +1.6% pa (Table 8) but average hours worked are going up because many more people are working full time now and less are woking part-time. See Table 4 which shows hours up +3.1%. Overall, people are now working 38 hrs per week when full time. That isn't changing much, it is just more people are in full time work. Hence pay is rising faster than pay rates.

Is the increase in scheduled repayments partly a factor of larger mortgages? Maybe, but I hope that the message is getting out there to pay more than the minimum. The rate of inflation is still low so every dollar of debt is debt (for debt repayment CPI matters more than house price inflation).

It's correct that the banks have been very competitive with interest rates. They have offered very generous rates to those with existing mortgages.

Those that I've seen struggling with mortgage debts are in a far more comfortable position these days. Which seems consistent with the data from the previous articles. Overall it looks like RBNZ has room to move for an interest rate increase at some point after the election.

The rate of inflation is still low so every dollar of debt is debt (for debt repayment CPI matters more than house price inflation).

Not sure what you're trying to say except that it's easier to repay debt when debt servicing is low.

That it's most effective paying down debt while inflation is low. Leaves you with more spending power in the future.

David we are not 'upping our scheduled repayments.' Scheduled payments are a simple dynamic of the total debt and interest rate (and the percentage of interest only loans within the sum total.) There is also an important element missing in how these figures should be reconciled and that is the flow of revolving credit and how it is being used .In relation to drawdown , this is mainly a reflection on housing activity and our ability to either fund house building or purchase homes from one another and the prices we pay for them ,Average interest rates bottomed in the September quarter at 4.6 percent , now 4.9 percent, repayment deficiencies albeit small have risen quite sharply

Modern monetary theory on RNZ with Bill Mitchell.

http://www.radionz.co.nz/national/programmes/sunday/audio/201852897/bil…

Government surpluses may be a bad thing -irresponsible

And countries with a fiat currency will not run out of money.

National Govt listening?

Greens are neoliberals on bikes. Labour are neoliberal lite.

National are neoliberal.

So where are the alternatives?

1. Steve keen has clearly articulated those ideas. He's published loads of material on social media, youtube, published books, created a sophisticated economy modelling software package called Minsky which anyone can download on sourceforge, and teach themselves to use on youtube.

2. You could regard neoliberalism as selling assets, having a light handed approach to governing the economy, not caring who's buying houses businesses or whatever or where the money's coming from. Clearly the greens, Labour and especially NZF are not at all neoliberal. In fact they are the only parties that provide an alternative to neoliberalism.

3. If private borrowers are deleveraging and there's less chinese money buying all the houses and banks are lending less, then of course the government will have to run a defect to prevent the economy from imploding. But if Labour or the greens or NZF were to suggest that, or even propose any policies based on modern monetary theory then the National backing fake news Herald would tear their heads off. Labour, the Greens and NZF know the dice is loaded against them, and they're playing accordingly.

Labour will allow all of Point 2 to continue, even if to a lesser extent

"2. You could regard neoliberalism as selling assets, having a light handed approach to governing the economy, not caring who's buying houses businesses or whatever or where the money's coming from. "

You could add to your definition: " allow global corporations to dominate the economy and government decision-making". Which Labour will also be forced to follow - lite.

It was a while ago but the last anti TPPA rally I attended, NZF and Labour candidates were there and gave good speeches. Jane Kelsey always gives an excellent well though out talk. I cant for the life of me recall any national MP's in attendance :)

Well, hopefully they can offer an authentic alternative.

Was Helen Clarks govt much different from John Keys really?

My how things have turned ...........Has anyone noticed that the Banks have all but ceased advertising or offering really low "special" mortgage rates in the past 6 - 8 weeks?

Now first off the block , Kiwibank, want to squeeze anyone with a Mortgage by increasing floating rates .

Things have changed. The tightening by banks seems to be more than is required give this statistics above. I'm being to think they are all looking carefully at their cash flows. Now they have locked a lot of people into low interest fixed terms there's only one place they can extract additional money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.