By Bernard Hickey

There's a tipping point for any pragmatic policy-maker where the facts change to such an extent as to render any existing strategy redundant.

Depression-era economist John Maynard Keynes explained his change of mind on monetary policy after the Depression thus: "When the facts change, I change my mind. What do you do, sir?"

This week New Zealand reached that tipping point when it became clear the facts have changed and it's time for the government to change its mind.

The facts on the economy are so demonstrably different to expectations that the government, the Reserve Bank and voters should reassess the direction embarked on four years ago when the National-led government took power and committed itself to a 'hands-off' approach to monetary policy, the big Tax switch, and a plan to return the budget to surplus by 2014/15.

Thursday's Household Labour Force Survey showed unemployment blasted through expectations to 7.3%, its highest level since 1999. Employment actually fell 8,000 when it was forecast to rise by the same amount. Prime Minister John Key was clearly surprised to the point where he even suggested policy makers should rely on his anecdotal evidence rather than Statistics NZ's figures. Finance Minister Bill English was sensibly more subdued.

Friday's figures from the Real Estate Institute of New Zealand (REINZ) showing median houses hitting record highs in October both nationally and in Auckland simply reinforced that the economy is heading off in exactly the wrong direction.

And it's not a new direction. Cheap and easy credit along with supply shortages are inflating house prices beyond the reach of young families wanting to own their home, particularly in Auckland.

The median house price in Auckland rose 14% in October from a year ago. Sales volumes rose 44% in October from a year ago in Auckland. The median price rose 5.8% in October from a year ago and volumes rose 32.6% from a year ago. The market is so hot the REINZ even bragged that the market had 'roared into life' in October.

Party like it's 2007 with a jobless rate like it's 1999

We seem to be back where we started in late 2007.

A hot housing market is forcing the Reserve Bank to keep the Official Cash Rate higher than it would otherwise like. This in turn keeps upwards pressure on the New Zealand dollar, which makes our manufacturing exporters less competitive. That in turn costs jobs, many of which are high wage jobs.

Key may be seeing anecdoctal evidence of job creation in Auckland, but just this week Christchurch electronics manufacturer Dynamic Controls proposed shedding 60 jobs and high tech exporter Rakon announced it would cut 60 jobs and move production to China. Solid Energy and Tiwai Point announced hundreds of high paid job losses last month, which have yet to be registered in the jobs figures. Jobs are being created, but they are in lower value services sectors such as healthcare, big box retailing and restaurants that are not subject to international competitiorn, or are higher value jobs in real estate and financial services. That means fewer mine workers and factory workers and more Warehouse checkout operators and real estate agents.

The high exchange rate is sending a clear signal to consumers and businesses alike: buy imports, convert businesses from exporting to importing and employ people involved in real estate investment and financial services. The record low interest rate and a loosening of lending controls for mortgages is convincing a whole generation of borrowers that they can afford their dream home if only they can outbid their rivals by borrowing as much as they can with a 5% deposit and interest rates at 5%. The Reserve Bank is forecasting their rates will only rise around half a percent in the next two to three years and the Government's response to the Productivity Commission's Affordability Inquiry insures few new houses will be built any time soon.

Banks are offering free tablet computers, NZ$1,000 cash back bonuses, discounts on legal fees and low-doc loans, just as they were in 2007. The Financial Stability Report this week (figure 4.6) showed another easing of lending rules for households in the last six months and banks are at it hammer and tongs to win over disgruntled ANZ and National customers dislodged in their merger.

The messages are as clear as a bell. Gear up, buy property and you can't lose. Don't bother investing to export. You're much better off borrowing to import because foreign investors will keep lending to New Zealand forever and we can always sell off more businesses, state assets and land as well to make sure we fund our current account deficit. Leverage up and just wait for the tax free capital gains to fall into your lap. It's much easier than building or producing something to export it.

It wasn't supposed to be like this

The National-led government began with such promise and ambition. It wanted to turn around the economy's obsession with property investing and reverse the decline in the productive and exporting sectors.

The big tax switch of 2010 was designed to discourage consumption by increasing GST and encouraging production and investing by lowering corporate and high income tax rates. This was supposed to switch the incentives. The introduction of tougher tax rules for residential property investors was also supposed to knock the rental propety obsession on the head.

The aim was to reduce the indebtedness of the household sector and the vulnerability of the economy by earning plenty of foreign exchange revenues to pay high wages and invest in export businesses. It was supposed to create a virtuous circle.

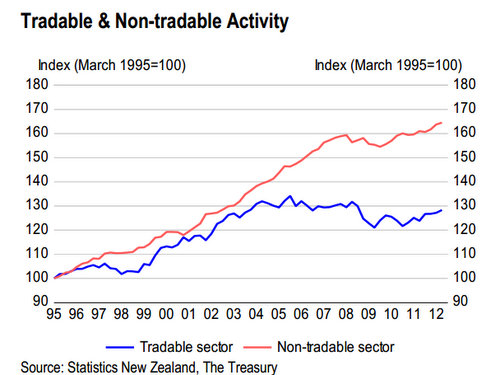

Instead, the gap between the tradeable sector (including exporters and those competing with imports) and the non-tradeable sector (financial services, government, real estate and retailing) is even wider now than it was in 2008.

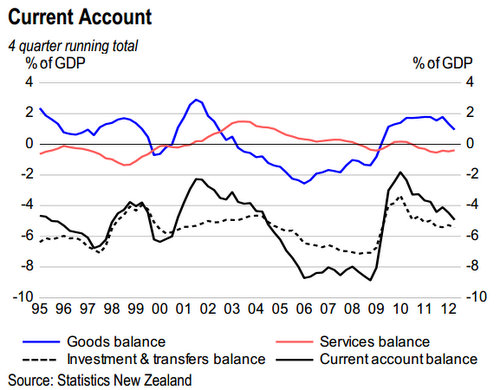

New Zealand's net foreign debt is only marginally lower, largely because of reinsurance payments for the Christchurch earthquakes. The 'foreign drain' of interest payments on foreign debt and dividends on foreign owned assets remains embedded in the economy.

Even Treasury is forecasting the current account deficit to rise to 6.7% of GDP by 2016 from 3.8% in 2011. New Zealand has actually been running a goods and services trade deficit this year. That's before the interest payments and dividends to foreign owners. Simply from the four banks alone, their profits rose 12% to NZ$3.2 billion or about 1.6% of GDP this year. See more here in Gareth Vaughan's article.

Yet the New Zealand dollar is still 15% over-valued according to the IMF and above where it was in 2007. The usual economic theory says the exchange rate will act to help balance a current account deficit. It should be falling to close the gap.

The usual theory

The trouble is the theory of free floating exchange rates responding to commodity prices and economic fundamentals such as current account deficits has been blown out of the water by the Global Financial Crisis and the various responses of intervening and printing by central banks and governments.

Central banks and governments in six of the top 10 currencies by volume are intervening directly or indirectly in their currencies. The United States, Japan, the European Union, the Bank of England, Switzerland and Hong Kong have all either engaged or threatened Quantitative Easing (Money Printing) to try to boost their economies and weaken their currencies over the last year. The other four in the top 10 who aren't intervening in their currencies are Canada, Sweden, Australia and New Zealand.

Capital flows, much of it printed by central banks at 0% interest rates, are now cascading around the world to those currencies with higher interest rates (than 0%) where money is not being printed. Much of this money is flowing into property sectors and stock markets. At least some of the demand for central Auckland property is from Asian investors able to source funding in their home countries at much less than the 2.5% of our Official Cash Rate.

Many countries have acted to stop these unnatural capital flows from damaging their productive sectors. Some have imposed capital controls. Others have printed money to buy foreign currencies to stop their currencies from rising. FT.com reports here that Switzerland's latest interventions have been successful in capping the rise of the franc.

They all have a similar problem. If they cut interest rates to give some relief to their productive sectors and weaken their currrencies, this would just encourage more leveraged investment in property, risking the financial system blowing up another asset bubble that destabilises the financial system. The last thing they want to do is create another bubble of Too Big To Fail banks and unsustainable house prices.

There is another way

So central banks and regulators have acted to cauterise their property markets from the blunt instruments of monetary policy. They've used so-called 'macro-prudential tools' to slow down lending into these property markets to either avoid having to hike official cash rates or allowing them to cut rates. Here's an IMF paper on 'macro-prudential tools' to show how it's being done elsewhere.

Canada's Minister of Finance announced in June this year that mortgages with government-backed insurance would be limited to 80% of their home value (down from 85%) and be cut to 25 years (from 30 years). Any borrowers' maximum debt service ratio would be also be limited to 44% of income and borrowers would not get government-backed mortgage insurance on houses worth more than C$1 million. In March Canada's Office of the Superintendent of Financial Institutions announced it would limit home equity lines of credit (HELOC) to 65% of the value of a home and would not provide mortgage insurance for HELOC loans. See more here at The Global Mail.

Last week the Bank of Israel imposed a loan to value limit for first home buyers of 75%, a limit of 70% for existing home buyers and a limit of 50% for rental property investors. See the Bank's directive here. At the same time it announced a surprise cut of 25 basis points in its Official Cash Rate to 2% to help support its economy and offset the impact of a rise in its currency. Israel's house prices have risen 2.9% in the last six months.

But back in Orthodox land...

Meanwhile, New Zealand house prices, as measured by the REINZ's stratified index that takes out some of the 'noise' from more sales of expensive houses, rose 3.5% in the last 3 months and 6.9% in the last year.

If only the Reserve Bank could slow down the housing market with macro-prudential tools instead of the Official Cash Rate.

The Reserve Bank is investigating using such tools, including Loan to Value Ratio limits and things such as 'counter cyclical capital' buffers, which would require banks to hold more capital at times of strong economic growth.

But this work is still only investigatory and the Reserve Bank has yet to agree a Memorandum of Understanding with the Government on how and when it would use such tools. New Governor Graeme Wheeler even said he wouldn't use the tools even if he had them....yet. See more here in this piece with a video of Wheeler's views. Previous Governor Alan Bollard looked at using them in 2006 and decided against it. He reiterated last month he was opposed to using them.

It beggars belief. So when would the Reserve Bank and the new Governor use them? Is a 14.4% rise in house prices in the country's biggest real estate market in one year (past tense) not enough? House prices rose 3.5% nationally and 7.7% in Auckland in the last 3 months. That's twice as fast as the growth being seen in Israel. Also, inflation is running below the Reserve Bank's own target band of 1-3% and below the 2% average that he has agreed to focus on in his new Policy Targets Agreement. I

Why won't he act? Surely he's not asleep at the wheel(er)?

....And back on Planet Key

In the meantime John Key has pledged to stay the course with the government's 'hands off' strategy for the currency and the Reserve Bank Act, and will stick to the plan to get the budget back into surplus by 2014/2015. This implies a fiscal policy tightening of around 4% of GDP over the next three years.

If the government is going to tighten by 4%, which part of the economy is going to expand by the same amount or more to avoid going into recession? It was supposed to be the private sector and, in particular, the export sector. That now looks very unlikely with a currency stubbornly over 81 USc and rising towards 80 Australian cents. It also looks unlikely with Europe in or near recession, China slowing from a 10% plus growth rates to closer to 7% and Australia slowing to under 3% growth.

So what to do?

If the government and Reserve Bank do acknowledge the facts have changed, then what should they do?

Here's a few ideas in no particular order:

Introduce loan to value ratio limits similar to the Israeli ones - They are conventional monetary policy tools now and would avoid a whole new generation of borrowers getting up to their eyeballs in debt just before interest rates start rising again. They will also reduce the financial vulnerability of any banks were house prices to fall sharply because more equity means less chance of mortgagee sales.

Introduce counter-cyclical capital buffers - This would slow down bank lending growth in a much simpler way than an increase in the Official Cash Rate and doesn't punish existing borrowers for the actions of those borrowing at the fringes. It would mean banks have to top up their equity, probably by not sending dividends back to their Australian parents. That would help reduce the current account deficit in a similar way to what happened in 2009 when banks agreed to pay higher tax rates. It would allow the Reserve Bank to cut the OCR and give relief to business borrowers, or at least offset any increase in interest rates imposed by bank shareholders to protect their profits given the higher capital requirements.

Increase the risk weightings and capital requirements for mortgage lending - This would force banks to slow mortgage lending and put aside more of their own capital to back these loans. It could be argued this would reduce the 'over-weighting' of New Zealand bank assets to one type of asset. Any investment manager will tell you that diversification reduces risks. Gareth Morgan has suggested such a move in his 5 point plan.

Introduce a land tax or capital tax or capital gains tax - This imposes a holding cost on land-banking property developers and transfers some of the easy wealth gains of the recent gains to non-property owners. It also evens up the playing field so that capital gains are taxed as much as income. Gareth Morgan's Big Kahuna idea for a tax on capital is the simplest and most redistributive idea around.

The Central government and local government must urgently work together to build 50,000 new homes in Auckland and Christchurch - The combination of the market and local council regulation has clearly failed to deliver the affordable housing desperately needed to put some pressure downwards on house prices and make New Zealand an attractive place to live.

Rewrite the Reserve Bank Act to allow it to target other variables than inflation - These other targets should include a combination of the exchange rate, employment levels, the current account deficit, inflation and wages. Inflation targeting is now widely discredited overseas, yet the orthodox dominates at the Reserve Bank and Treasury.

Rewrite the Reserve Bank Act to allow it to buy government bonds directly from the government - This would allow the Reserve Bank to finance the government deficit once interest rates are cut to the lower bound of % and avoid deflation. It also removes the financing restriction for rebuilding Christchurch's infrastructure and Auckland's infrastructure, including housing. It may not be necessary just yet, but we're not far off given the current trends with employment, inflation, the global economy and the budget deficit.

Run a deficit for longer - The government needs to abandon its budget surplus target for 2014/15. Moody's has already said it would not downgrade New Zealand's credit rating if this happened and last year's credit rating downgrades by Fitch and Standard and Poor's did not lead to interest rate increases.

49 Comments

Great article. It seems almost impossible for the RBNZ to gain control of the housing bubble without destroying the rest of the economy in the process, so they just let the bubble keep inflating. Did they learn nothing from the USA or Ireland experience. This could come back to bit them on the bum very hard.

Australia is grappling with ths same problem, house prices starting to take off again the the RBA unwilling to lift rates for fear of damaging retail and other sectors. See below...

What can Australia learn from recent house price movements in New Zealand?

What Australia and NZ both need is better macroprudential policy, but with the inept governments we have in power, thats unlikely. So they keep pulling broken levers and failing to fix the problem!

Inflation should not / cannot be let loose.

"NO" to additional taxes.

Who says inflation is going to be let loose?

The problem of the next decade is going to be deflation. Just ask Japan.

And, anyway, what's wrong with a bit of inflation to make debt go away?

Not much fun for savers, but better than a catastrophic writedown of assets in some sort of financial meltdown.

Inflation is a problem for wealthy hoarders and the old. Might convince them to invest it in something productive. Although you'd have to make sure it wasn't simply geared up investment in property. ;)

cheers

Bernard

Sore loser

Thanks for limiting the capital letters to a few...I think

I shouldn't rise to the bile, but I can't help myself. You accused me of being a lazy, self interested shill for the banks.

The arguments I advance above would make me personally poorer. They would likely reduce the value of the house I'm selling and/or the one I'm likely to buy in Wellington.

The most personally financially sensible thing for me to do would be gear up the equity we have in our house with lots of big 95% loans to buy rental property and just wait for house prices to rise.

I'm not doing that. I'm deleveraging because leverage is dangerous when thinks go pearshaped.

You raise an interesting point about my productive-ness. Fortunately (or unfortunately depending on who you are) Interest.co.nz is now part of the tradeable sector of the economy. That means we compete against imports in the form of advertising on google, facebook, yahoo, etc, not to mention the news and advertising on overseas sites such as Reuters/FT etc.

You say that I've been advancing the interests of the banks. Have a chat to the banks about me. My face is on plenty of dartboards in bank call centres ;)

Read all the articles we do on banking on this site. We are far from shills. We regularly report on the level of profits, leverage and looser lending standards of the banks, not to mention the risks around covered bonds and open bank resolution.

cheers...I think ;)

Bernard

Well spoken Bernard, i agree with you.

I think it would be a good idea if all those people who are registered to comment on this site could make some small contribution.

Maybe as a start point you have a fee of $10 per annum to register. Hell that's less than 20 cents per week, but it is a start and it is something. It is well worth making some effort to keep a good site running. I am sure many would be disapointed if it had to close because of cost.

Is it possible to put a team together and draw up a plan to produce a TV series, and later released on DVD, a documentary called "THE HISTORY OF THE NZ ECONOMY" or something like that. Starting, say at pre European times when Maori did not use money.

Once you put it together you could then apply for funding from NZ On Air. You could then employ a bunch of students to go right through all the newspapers, including houses for sale, jobs, etc. Also old TV and radio news clips and so on.

You could then have a very comprehensive, searchable database which you could charge people to search as well as doing a TV series and a DVD.

Just a thought Bernard

My face is on plenty of dartboards in bank call centres

Hardly the hub of corporate decision making - a reflection of the company you keep Bernard?

well we have all been saying this for a year now and the only suggestion is to give the people who could not see it more power

yeah right!!

Can't really improve on the article, Bernard.

Memo to John Key and Bill English;

Follow the current path and the legacy looks as follows:

Unemployment continues to be higher than since National were last in power (and your first go as Finance Minister, Bill)

Current Account as high as ever; with national wealth very low, and national debt massive.

Productive economy outside farming largely gutted.

Massive exodus of young productive New Zealanders.

And you would think, zero chance of getting reelected in 2014.

Or, as Bernard notes, you can at least pretend the facts have changed, and not have us be the last orthodox out of touch economy in the world. The opposition parties have more than opened the door for a change in approach. Some minor loss of face maybe; but the legacy would be massively different. Have an honest chat with two or three marginal export or import substitution businesses, and discover their real pain. It can be fixed. But you need an open mind. Urgently.

And as a small aside, given the internet, people like Bernard (and me and a very quickly growing number of like minded people) are otherwise going to make your lives pretty miserable for the next couple of years. And yet we all have many other things we'd prefer to be doing. And Bernard even would like to be positive.

So have a deep think about the alternatives over the weekend; and pleasantly surprise us at some stage.

Stephen L

I don't want to throw too many rocks. I actually think Key and English are more pragmatic than it might seem when pushed.

You're right. They need an excuse to back down.

I've also made a point of including positive suggestions for change in this article.

Here's hoping it sparks some debate.

cheers

Bernard

Hugh,

Cities are built up, property developer subdivision by property developer subdivision. Later Councils find they need a road so they have to kick people out of their homes to build the roads.

Don't you think we should get a first class WHOLE CITY plan first? One that takes us way into the future and includes all the infrastructure.

I don't think panic solutions are the answer

Indeed, Bernard. Am not looking for you to be too one sided or critical from a political point of view; and appreciate you have come out with a good number of sensible options to consider. Some of us might use more strident language if no change is made; and the data remains very negative. Rather I do think the internet medium makes it more difficult for any governing party to carry on delivering poor results, appear to do nothing about it, and not even to present coherent arguments why they are not considering alternatives presented to address the key problems.

I do think the medium will make it harder for them to hide behind "Because Treasury or the Reserve Bank says so" type of statements that they might have got away with in the past. And credit to you guys at interest.co.nz. I suspect your site is now an opinion leader for the other media, and some of the politicians, on some key economic matters.

"I don't want to throw too many rocks. I actually think Key and English are more pragmatic than it might seem when pushed".

You are not planning to move closer to the trough, are you?

No more tiresome than long harangues on the one - and only the one - topic by someone who refuses to investigate anything which might upset his pet applecart.

:)

Spot on PDK. I have actually come to the conclusion that HP is actually a shill for the house inflation industry. By constantly decrying anything that WOULD have effect on halting house price inflation (ie credit controls etc) and focusing on a single issue that will actually have little effect (see what happens if you build more houses in a cheap credit environment - all those housing speculators will just buy up all the extra supply with the cheap credit pushed their way) he cunningly diverts attention away from the key issues.

Self promotion ad nauseam (pun intended).

And they told Iain Parker off?

And the points you disagree with ?

The yet another self-promotional link!!!!!

Hi Hugh,

NZ quantity surveyors manage the QS profession, ethics, training, international realtions etc. For $m2 refer to the Rawilinsons Contruction Handbook 2012, its NZds construction cost bible.

http://www.rawlinsons.co.nz/handbooks/

Keep the good work up for those less forntunate, in need of help and ignore those who one suspects benefit from property value increase as they try to shoot you down rather than provide constructive criticism.

Cheers

Bernard, debt doesn't "go away" with inflation. Enormous asset price inflation; all is fine. Bubbles burst, debt must be paid or defaulted on; oh no, deflation, can't have that, let other people pay.

Dissapointing.

Great piece Bernard, agree entirely EXCEPT that I am not as optimistic as you on Key and English's 'pragmatism'. They are free market idealogues masquerading as moderates.

they will continue to be hands off, and the NZ economy will well and truly go down the gurgler.

The frustrating thing is that there ARE solutions out there

The higher house price is the only way to fix the employment issue. THe higher house price will make people feel richer and start spending. After that the employment condition will be improved.

Just like the 2002 to 2007 fantasy land?

Did you take in the chart showing what happened to our current account deficit the last time people felt richer? That, so called, wealth was just more debt, debt that has saddled this country with among the very worst net international investment positions in the world.

http://en.wikipedia.org/wiki/Net_international_investment_position

That's us at the bottom of the page with Greece, Ireland and Portugal; countries that also "felt" rich not so long ago.

Great article Bernard you are an national treasure. NZ is lucky to have such high quality debate, now it is up to the powers that be to do something with it.

I have a different take about the Reserve Bank. I think under Bollard there might have been the thought that if things got really bad re the housing market, exchange rate and economy in general unrelated to inflation he might take action.

What Wheeler has done is send a message to the government not to expect him to do the heavy lifting when in reality they (English and Key) have the power and responsibility to rectify the situation directly.

Wheeler is simply saying that he will not act outside the Reserve Bank legislated framework. He has thrown the ball back to the government. If the government got the housing market under control, then the Reserve Bank could lower the OCR because other than rising house prices, inflation is quite tame. This should lower the exchange rate and help the economy in general.

The government has said it can control the housing market by supply side measures, such as somehow getting councils to reduce the cost and increase the number of housing consents. Of course we are still waiting on the details.

What Wheeler has done is force the government to put some actions with their words. If they want to try supply side measures, do it. If they are not confident that these will work, well their are plenty of other options as this article outlines, including changing Wheelers job description.

If English and Key do nothing, then they have to face the consquences of that choice. We can vote to get rid of them, we do not get to vote on Wheeler.

Hugh, Inflation is a degrading of money that is why prices go up. You need more and more money to buy the same thing because money is loosing it's value.

Hugh,

You may well be right on housing and local government issues; although I am very sceptical that whatever moves the government are making will help in Auckland much before 2014, if at all. I also note that someone posted yesterday that all the house price appreciation in Auckland is in the inner suburbs; the outer generally cheaper suburbs are relatively stagnant , slightly challenging the premise that there is demand for housing yet further out. Nevertheless am willing to concede you are all over the subject, and what they are proposing can do little harm.

Admitting that you don't know anything about monetary policy, and then suggesting the government leave it well alone, is not persuasive. Since they have come to power, the NZD has appreciated by 33% against the USD, the main benchmark trading currency. So all of our locally managed costs, would be all else being equal, 33% higher in USD terms than they were. Am sure some market adjustments have been made since, so the overvaluation is probably closer to 20%.

These costs include rent, rates, electricity, utilities, government fees, as well as wages (which need to remain high in NZD terms to pay all the other NZ costs), and collectively make it near impossible for any new business, without a very significant competitive advantage in some aspect of their business, to even consider setting up here. And many who are here, are either falling over, selling up, or moving out.

In the meantime, hands off monetarism has let the banks flood the market with foreign money, all looking for property to secure itself against. As Westpac noted, that is the overwhelming reason for the current bubble resurfacing. And this foreign money is causing all the other problems we have.

So it's good if housing supply is being fixed; if indeed it is; but the monetary area is far more urgent for the productive economy.

Hugh just because the government is focusing on what you think is the solution to housing doesn't mean the government is necessarily taking the right action. I would look more at financial bubbles and greater inequality as bigger issues, based on the economic commentary I read e.g. the paper by Adair Turner that was referred ton on one of last weeks Bernard's top 10; or Minsky's John Maynard Keynes.

Bernard, thanx for a fantastic article - brilliant

Bernard, when you do an article on the economy can you take a more in-depth look at why banks would rather lend on houses than to businesses. I see it this way.

Pre Rogernomics businesses, over many decades, had built up such good businesses that they had plenty of assets. Such as they owned their own buildings that their factories were in and so on. When these businesses needed cash to expand or other business purposes the banks were keen to lend to them because they could use their assets, such as buildings, as security. Also the banks charged them a higher interest rate than home loans. So from the banks point of veiw they had good security and got a higher interest rate.

Then Roger came along, well you know what happenned. This was good news for the likes of Brierly because he could take control of the business and asset strip them, making a fortune in the process. Now bussinesses can not do this because they make a good take over target for asset stripping - So naturally the banks wont lend. Now businesses have to rely on their share value which is not as good as the buildings they once used to own. So lending is much harder.

That's how it see it, please correct if i am wrong.

Great work Bernard, cant you be more forcefull in making them anwser these points though in interviews etc. I wish I had the chances you have to really give it to them. They are failing our countryand should be shown no mercy.

And here we read about the financial fiscal fiat money farce that now fronts for the UK economy...

"The latest little (actually quite big at a tidy £35bn) money printing wheeze comes about as close to outright monetising of government spending as it is possible for the Bank of England to go without simply creating the money and handing it by the lorry load to the Treasury, a la Weimar."

The fact that these crooks are entering into a scheme that has but one ending...failure of the currency....is no reason for the RBNZ to follow along the same mad road.

Somewhere out there lurks inflation....it is gathering strength as any storm does...the longer the fathead behaviour prevails...the more dreadful will be the damage.

This explains why more countries are buying up gold...

No Mention of the crazy price of building materials. Building costs 30% lower in NZ, Tradesman wages 50% higher. Go figure.

No mention of of the lunacy of allowing wholesale immigration with house prices and unemployment going through the roof.

Key and English et al have embarked on a course of policies that will see them both remembered by future generations as failures. This bank licking sickness they display with policies that encourage cheap credit to flood into another round of property bubble idiot behaviour, has to be deliberate....and that leads to the question...who is gaining what from their policies.

Sadly, this govt's policies will lead to a return of the socialist marxist life meddling idiots gaining control of the system and they in turn will set about adding to their past destructive stupidity. Expect Shearer and 'watermelon greenies' to rush into 'printing' .....Be prepared to remove your capital from the harm those fools will cause.

Some good news for a change Wolly. The UK government has introduced a new 'tax avoidance tax rate' all the tax you can avoid, up to and including pay no corporate tax. The pilot scheme only allows large multi-national companies in however maybe they will probably widen the scheme if its a success. Given Starbucks massive hoards of cash and now zero disincentive to invest, soon there will surely be a Starbucks on every single street corner and the UK economy will be humming. Since its your recovery theory how long before this all kicks in in your humble opinion?

Make it up as you go along Nic....you decide on my "recovery theory"...whatever you dream up!

Thieving multinationals are in the same boat as thieving banks and both share a common relationship with dreadful politicians and shabby govts.

Get with the scene Nic...less govt and more individual responsibility...tell us what's so wrong with those goals.

Or are you in the camp that believes there are special politicians who are so much better at managing your life that you are willing to ask them how much of your income you are allowed to keep to spend and invest as you wish!

The UK economy is a corpse. Our economy is little better. Recovery is something for the liars to promise come election time Nic....not something that is real.

Hold on to your wealth now as the NZ farce blows the property bubble larger....a collapse will only be bigger.

This is hilarious. Video clip of the JK press conference where he discusses the slang language that has been getting him in trouble .. and his last word is "bugger"!

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=10846333

In reference to David Beckham being wealthier than him :-).

Kate,

Thanks for the link. Am not a great fan of John Key, although personally would prefer both the media and opposition concentrated their efforts on challenging his policies and economics, where there is plenty of fertile ground, rather than pursuing matters of relatively little consequence.

He's right, I know from family experience, that teenage kids commonly did use the term gay to describe nearly anything; and his record is clearly supportive of gays and lesbians.

His Beckham comment was dumb, and embarrassing for not only him but us; nevertheless was apparently made in an area where he might have expected some privacy.

Being pedantic, I actually think his last word was "okay" and not "bugger", as it happens. Hard to be sure, as his articulation is clearly not great, and I think he's just not got his tongue around the word. To be fair, it's him pointing out that Beckham has made more money than he has.

A hot housing market is forcing the Reserve Bank to keep the Official Cash Rate higher than it would otherwise like. This in turn keeps upwards pressure on the New Zealand dollar, which makes our manufacturing exporters less competitive. That in turn costs jobs, many of which are high wage jobs.

Both the UK and US have explicitly cut interest rates close to zero, executed QE and yet the London Housing market is booming and general economic indicators, particularly in the UK, are appalling.

Please explain beyond repetitive howlings about getting into line with failing economic policies similar to those operating in the UK and US.

Quote

Your "Irish economics" is making an old man of me !

It reminds me very much of the Irish immigrant getting off the ship in this country - and the first thing he asked was "Is there a Government in this country"...to which the response was "yes" and the Irishman responded "well...I'm agin it !!!". H. O'Pavletich

lol

Has there been any research done on places where there is ample develoment land available and folk still can not afford to buy houses? Provincial towns? Land may be cheaper but buiding costs are still out of reach? Seems BH is on to something.

Excellant comperhensive artical Bernard with "solutons". We see the "same old same o" from the beehive boys (The bureaucratic civil servants cruising along in high paying jobs - what are they doing where are they - nothing?), it seems not until the wheels(er) fall of the apple cart then crises management kicks in. Interest.com is NZds best economic think tank and comment forum with views from all levels and angles some good, some well.. . Take these cocepts you have absorbed and developed to the powers that be. As you note NZ economic landscape needs new direction. If National won't listen and act maybe Labour well ther looking for a game changer?

Bernard, a good quote from Keynes. He changes his mind when the facts change! I always thought that was evidence of an unprincipled person: he just hops around from one policy to another in a world of ever-changing circumstances. Unfortunately this is typical of current politicians and economists, constantly rearranging the deck chairs to change the list of the ship as it submerges.

I cannot make sense of the policies you are advocating. On one hand you want the govt to turn on the money-printing so we can keep in step with other money-printing countries. This will, of course, disadvantage savers who will see the value of their money evaporate. What will savers then do? Instead of saving they will buy stuff that they think will hold its value, like houses. But on the other hand you are promoting a number of policies designed to stop them buying houses! Maybe they will then decide to buy gold and silver. But you will not want them to do that either, because that is an unproductive use of money. You will need to make some laws to stop that too! And so it goes, a never-ending series of interventions to fix the unintended consequences of the previous interventions, which is why we are in the fix we are in today. I am all in favour of sacking Wheeler, but why stop at him? Close down the Reserve Bank completely, we do not need it.

Yes & No

Take property we compete amongst ourselves to borrow maximum and also pay interest to foriegn banks sending billions overseas whilst risking passing ownership on defuault. Yet where one of the most unpopulated countries with ooooodles of land. Its almost like shooting oneself in the foot.

On the other hand people in this day and age basicly need affordable shelter at a quality you'd expect (within reason) , We want young working people to live, grow - basicly invest their lives and energy in NZ, But not at such a cost that it affects ones life style, a ration of 1 to 2.6 of the average annual income has been floated,

That money should not contimually being spent on the same unproductive asset, but export earning bussinesses providing employment, future and quality of life,

The Government role is to try and keep the country on an even keel and therefore should step in and balance the man made monetary system in areas of basic human needs and maintain the equilibrium in society whilst directing it towards foriegn trade - PRONTO!

spot on

"The big tax switch of 2010 was designed to discourage consumption by increasing GST and encouraging production and investing by lowering corporate and high income tax rates".

Can someone tell me how you are supposed to encourage production by discouraging consumption?

Easy peasy.

By raising the GST, you encourage people to switch to a cash market, where everything is done on mates-rates for a few back-hand bucks. With the 15% you save, you can afford to buy 15% more of other stuff, which normally you couldn't afford. This will need to be produced, thus increasing the GDP a few percent. Or that of China's.

So much for corporate tax rorts...look what socialist pollies get up to!

"The Labour MP has been one of the fiercest critics of tax avoidance by companies such as Starbucks, Google and Amazon. However, she is likely to face questions over the limited tax paid by Stemcor, the steel trading company in which she owns shares and which was founded by her father and is run by her brother"...........Oh brother

Bernard, when talking about quantative easing (money printing) we should also take into consideration all that interest that is being paid on money that is printed out of nothing.

Look here http://www.bbc.co.uk/news/business-20270002

at the shamozel over all the billions and billions of dollars paid in interest on printed money.

Just think how many billions the FED is making from it's printed money and that's a private bank so the money is going to the 1%.

Imagine the profits that are going to be made when interest rates eventually rise on all the printed loans still outstanding.

Globaly, over time, trillions of dollars are going to be paid in interest on printed money.

Mike,

Being slightly pedantic, I'm very confident the FED is government owned, so the interest they earn benefits the government. If they have loaned the money to themselves, then it is interest saved.

Whether you like QE or not, it has also saved the British taxpayer huge amounts of interest on its fiscal deficit; apart from the free capital it has also created for them, while causing modest still less than 5% inflation.

Crikey Bernard, you are being exciteable today.

The way monetary policy is supposed to work is that the wage inflation rate goes up, which causes the interest rate to go up, which causes the exchange rate to go up, which causes the unemployment rate to go up, which causes the wage inflation rate to go down, which causes the interest rate to go down, which causes the exchange rate to go down, which causes the unemployment rate to go down, which causes the wage inflation to go up..... and so on forever in an endless loop. That's my understanding of the theory anyway. Confusion is caused by all parties by using consumer price inflation as a politically correct stand in for wage inflation.

Is it a callous policy? Yes. Does it encourage asset price boom and busts? Yes. Does it favour those who have first use of borrowed money when it becomes available? Yes. It does seem to encourage a lot of waste of human potential.

What I'm not sure about is what New Zealand can do about it, other than to "soften the hard edges of the resssion" to quote Bill English. A housing crash would cause a lot of suffering, as does losing jobs. Tiwai and Solid Energy are just casualties of the global over capacity of their industries, lowering the NZD will not change that.

Some policies are a good idea in my mind, but they are ones that set up NZ for the future rather than try to delay changes that are inevitable. So changes that allow adaptability so we can get new mines up and running early in the boom rather than at the end. Lowering the corporate tax rate to get corporates to move jobs here from Aussie. Buying gold at a steady rate when the dollar is high in order to have gold reserves if we ever need to buy missiles that can take out aircraft carriers. These are sensible to me. Reducing the amount of debt in the economy is highly desirable but is hard.

Interesting point, "tradionally" most economists who talk "sense" talk about core inflation and not cpi. This of course is history, we have now gone past peak oil so we have seen that there is no wage inflation even though goods want to inflate. An interesting problem for vendors, they want to chargemore but mostly cannot.

If however you look at even CPI at 0.9% and then look at rates, my rates are up 6% year on year....power a few %....food, dunnot but it must be 1 or 2 %....this means that some sectors must be deflating to compensate...hence the un-employment figures, shock, no expected.

Mines, no thats a one time resource use besides which you jsut said over-capacity...so more mines? makes no sense IMHO.

Cut the tax rate, no, no advantage, most of our big companies are foreign owned thats more money leaving. Gold we dont need its of no use. We have food, anyone who has oil will "swap" for food.....and its renewable.

Private debt is the huge worry....because its expected the tax payer picks that up....it all funnels through the banks and we teh tax payer will have to prop them up....

regards

While I agree there are elements of our economy that are laissez faire, entrenched entities like councils, govt and banks are anything but. Unfortunately we kind of have the worst of all worlds at the moment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.