Today's Top 10 is a guest post from Dean Anderson, product manager at sharemarket operator NZX's Smartshares.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

1. Warren Buffett.

Are you overwhelmed by the constant Trump references dominating daily headlines? Take a moment to digest this piece of wisdom from the legendary Warren Buffett in his 1988 Berkshire Hathaway Chairman’s letter:

We do not have, never have had, and never will have an opinion about where the stock market, interest rates, or business activity will be a year from now.

Buffet’s sentiments echo the importance of not letting the latest daily news headlines distract you from your long-term investment goals.

2. The Tao of investing.

Buffet’s advice fits well with the Chinese philosophy of Taosim, which teaches you to let go of the things in life we have no control over – and with investing that couldn’t be more important. To avoid getting caught in the news hype and making reactionary decisions based on market noise or media coverage, it is important to focus your investment attention on building a diversified portfolio suited to your risk appetite (while minimising costs). Jim Parker from the global investment management firm Dimensional sums it up nicely in this post – The Tao of Wealth Management

The path to success in many areas of life is paved with continual hard work, intense activity and a day-to-day focus on results. In long-term investment, however, that philosophy is turned upside down.

3. Walking the talk.

Putting this advice into practice is easier said than done. Investors (punters) typically chase the latest trends. As humans we seem wired to products that have done well – but will they continue to do well? Remember to always read the disclaimer which states past performance is not an indicator of future performance.

4. Challenges for active investors.

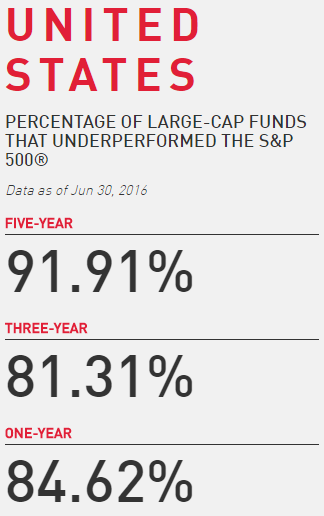

It isn’t just retail investors who get distracted by the hype. Standard & Poor’s produces an annual publication called SPIVA, which quantifies the performance of actively managed funds vs index returns – Standard & Poor’s Indices vs Active. This report covers markets and fund categories (and the challenges of finding great active managers). As the data below illustrates, over the long term 91.91% of active large cap US equity fund managers underperform compared to the S&P 500 Index.

5. It’s about the long game.

After all, it is about the long game – your retirement. Loads of investors check their investment balances on a weekly or even daily basis, despite some of these investments typically running for 10, 20, 30 years. You wouldn’t ask a real estate agent to value your house on a daily basis (unless you live in Auckland), so what’s so different about your investment strategy? Be sure to think about your investment timeframe when setting up your portfolio.

6. Educate.

Conversations about investing can create some awkwardness. To kick start the talk, take the Sorted Money Personality Quiz and see where you sit. It’s important we work to demystify the world of investing. To grasp the basics, Sorted also has a great range of resources to help you make more informed financial decisions.

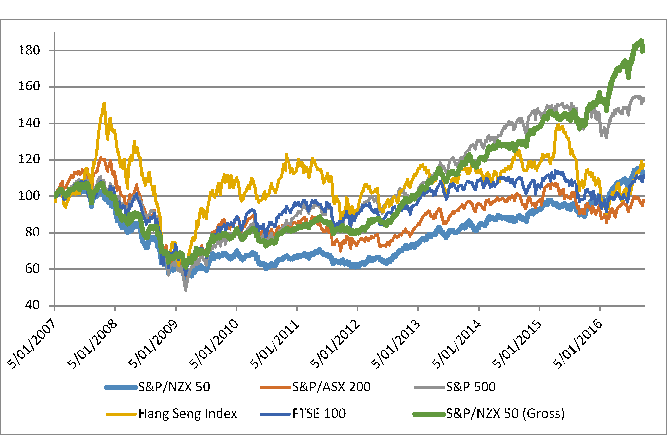

7. What is an index anyway?

Index jargon is everywhere. To help, S&P Dow Jones Indices has created the Index Literacy, which explains the basics – what an index is, how it works, and why is it relevant? As a starter for 10, the chart below sets out the relevant performance of key global market indices. Generally speaking, there are two key types of indices – capital or gross. A capital index assumes dividends are paid out, while a gross index assumes dividends are reinvested. Over time, the performance of the two types of indices will look quite different. For example, the bold blue line shows the S&P/NZX 50 on a capital basis and the bold green line shows the S&P/NZX 50 on a gross basis.

Source: NZX data

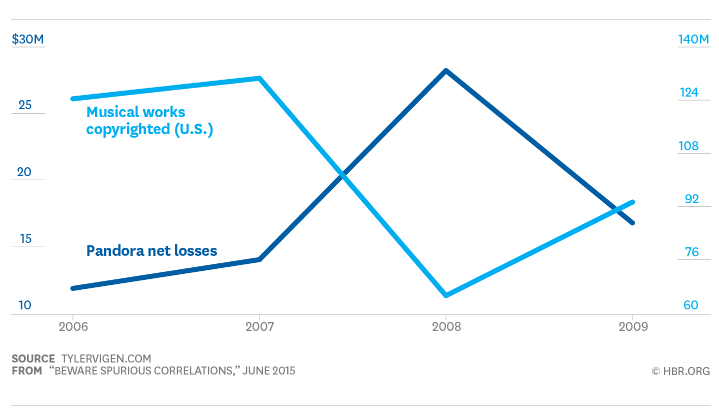

8. Remember correlation isn’t causation.

Like all things in life, investing requires a bit of common sense. Just because two things look correlated, doesn’t mean they are – correlation doesn’t imply causation! The Harvard Business Review has highlighted three things to watch for in its Beware Spurious Correlations article.

9. Just get started.

With all that financial jargon, it’s easy to feel overwhelmed when it comes to setting your financial goals. You could spend hours trolling Google for help – or just reach out to an Authorised Financial Adviser (AFA). Mary Holm has a handy 101 web page to help investors understand how AFAs work, and the fees they charge.

Bloggers Ryan and Ruth have also documented their investment journey, providing early stage investors with unique view points on their personal experiences of investing. Check out their blogs Ryan Johnson and the Happy Saver for tips.

10. And start early.

Growing up, I watched my grandparents diligently complete banking forms and record each dollar spent. While tedious, it established an early dialogue with money and saving. To kick start this conversation with future investors, a group of kiwis has launched Banqer, which brings the world of banking to the classroom, and getting kids set up with the concept of saving and money early on. Surely in the digital age this is a total no-brainer?

33 Comments

Index investing, balancing and maintaining diversity doesn't draw any comments. Sensible investing advice in a sea of arguments about housing risks being lost in the noise.

So much for starting early; student loans and saving for a house really kills retirement saving. Especially paying back student loans that were charging around 9% that makes investing pretty much pointless. Now the students I know have much larger loans, although 0% those loans are still taking 12% of every dollar earned above $19k.

I recommend saving 15% of gross income unless the individual has calculated what they need for retirement. Unfortunately there's not much left for a low earning age group to manage anything like this. It's good advice for the top earning 50% of the population.

I made investmenst that i thought were for the long haul,however my private super scheme investing in commercial buildings wound up last year and now my forestry investments are being wound up.

Reasons given for both,compliance costs.

I would have been better buying a rental property.

Very droll.

Don't give up Ngakonui Gold...one could always send parliament an account for payment of the loss of your rights....after all they take your rights away when introducing regulation because those rights are worth something to them and their system........look at how well the Maori have done due to their rights being abrogated........could be a nice wee annual earner in your golden years!!

I'm figuring 30 plus years of being a free tax collector must be worth millions! And that is only the start!

Smartshares are interesting. NZ's first and only local index funds,but most NZers see to have no idea that they exist. I read the annual report two years back and was surprised that there are few individual owners on Smartshares and most seem to be owned by institutions. As a savings vehicle, they seem to make sense. The only issue seems to be how easy they are to sell. Whenever I have looked on the ASB sharetrading platform, the market depth of the NZX50 undex fund looks shallow.

The number of standing orders is pretty deep. At the moment there's over $380k of buy orders so it's pretty easy to exit unless you had millions.

I think one of the problems is not so much that people don't know the index funds are there but that they have no idea about passive investing. It seems to be an alien concept, with few kiwis even knowing how to invest. Look at all the people that think houses are the only financial asset that exists.

Passive investing - that'll be the day!

Since the start of QE2 in 2010, the 500 companies of the S&P 500 have repurchased an astounding $1.5 trillion in stock (through only Q1), sending the index soaring while at the very same time confounding economists as to why the productive base in the US and globally may be so eroding. That this has been done via cheap debt also indicts the monetarist impulse of “historically low interest rates” as a means for economic growth that is efficient, and thus actually sustainable.

But it isn’t just the opportunity cost that is corrosive here, as monetarism directly impacts corporate actions beyond the short-term financialism. The debt borne by each of these companies, induced by that monetary effect of low interest rates, is an anchor upon future considerations, particularly as businesses are well-aware of cash flow implications arising from interest payments changing and the very real prospects of less-than-ideal rollovers. Liquidity considerations become far more paramount, in terms of this financial investment, about balance sheet structure on the liability side rather than the asset side where productive investment in actual capacity resides.

In other words, businesses should be using the liability side flowing from needs on the asset side (and I’m not talking about goodwill), rather than using the liability side exclusively to promote tomorrow’s share price alone. Never in our history has so much been devoted to that which is so fleeting. Read more

It's interesting that the passive investing gurus have said that the S&P500 is going to perform poorly for a long period of time. It's as if it's a crappy index these days. Although if you avoid all of the indexes where there's relentless money printing you'd have to avoid everything in the EU, US and Japan. People have to make some tough decisions about the mix of their portfolio.

On the ASB sharetrading platform, only $180K of units were traded today. That's not what I call "deep."

Re passive investing, I was in from day one purely as I thought that passive investing would take root in NZ, thereby increasing demand. Doesn't appear to be the case, at least locally.

I was just looking at FBU and you'd think that they wouldn't be traded so heavily given the fall in price but no $20m turnover.

Passive investing has lost out to kiwis loving to bet on individual shares, chasing dividends and kiwisaver funds. I'm slowly trying to spread the word but most people don't even seem to give a damn that their kiwisaver in their 20s is sitting in a low risk default fund growing at a snails pace.

The market maker will essentially buy/sell all you need to move unless you've got a huge holding, the amount that's actually traded doesn't matter too much from that point of view. Obviously the spread adds another transaction cost but it's intended as a long term investment. If you do have a huge holding, I think that you can redeem directly with SmartShares

J.C. take a look at the concept of market makers, when applied to ETFs; they provide the liquidity. I think that Craigs Investment Partners is the SmartShares market maker at the moment.

Not to detract from Dean's advice as I think it's great, but it would be pretty risky in my opinion to buy an index fund for the NZX50 right now.

We've just had a massive bull run and our stock market is so exposed to a correction if the housing market turns sour. In my opinion buying the index puts your at risk of a big hit - downside risk looks greater than upside reward...

That's part of passive investing. You have multiple indexes and not all in one country. For all you know housing might crash and the NZX50 might increase by 30%. Instead just use dollar cost averaging approach and rebalancing.

Good point Dictator

I have a few friends that took that approach in the US markets right through 2007 to now and did a quite well when you'd think that would have been the worst time possible to start.

Any idea what the total P/E is for the NZX50 right now?

I haven't run the actual numbers but picking data from the top 10 companies (in TNZ) that's around 22-23 P/E using a simplified calculation.

I agree Dictator. Smartshares appears to be one of the only low-cost, dollar cost average option available to most Kiwis.

Dollar cost averaging will help, setting up an automatic payment to invest through SmartShares directly is one way to do it. But I agree with you, the whole world looks relatively expensive in terms of price/earnings ratios. NZ and Australian stocks do give pretty good dividends, though, compared to other parts of the world. As usual, I'd say: diversify, and keep a good chunk of the whole investment in international shares, bonds, property, etc.

Forgot to add: SmartShares' international share ETFs are unhedged, so if the NZ economy does tank, then the NZD will most probably drop on the USD, especially if there's a flight to safety in USD, which will help the value of your international shares to go up during a downturn.

The whole asset allocation thing right now is in an interesting space.

Yields on bonds are terrible and chances are interest rates are going to rise, reducing value. Basically get punished financially for no reward.

Property values in Australasia are outrageous so buying shares in a commercial property group, you're really exposed to a downturn in residential housing.

Shares are ending one of the longest bull runs in history and as you say P/E values are historically quite high. I think I like the concept of buying up shares in companies with relatively low P/E and reasonable earnings outlook. Yields beat bonds and cash, with at least the possibility of a capital gain...

Leave your cash in the bank and you get taxed on the pitiful amount of interest you earn - while in New Zealand at the risk of being victim to an OBR event and losing your savings....

Buy a house in most part of NZ you're in significant debt for the next 30 years with very few options - and at risk of the house of cards falling over.

So where to turn?

Travel back in time to when you could afford to pay off a house in 15 years or less.

Something Stephen Hulme pointed out to me long ago was that we can't escape this and it's all the options we have. Also stuff buying low yielding bonds with interest rate increases on the way.

I think this is where current asset allocation theory falls down. I've told to buy bonds to balance my portfolio but I've read a lot of books and it doesn't make sense in the current market (in the past yes). My understanding of the theory is that if markets tumble, the expectation is that the Fed/Reserve banks will drop interest rates to stimulate the economy, as a result value of bonds rises. So you lose value in shares, but bond values increase. So you balance your portfolio and sell some bonds (increased value), and buy new cheaper shares.

But what happens now when we're already at historically low interest rates? If share markets tank now what will the Fed and Reserve Banks do? Go negative? And if they don't, you lose value on both shares and bonds...douby whammy. So whats the benefit at all of bonds anymore?

Bonds are pretty much worthless "paper". Don't forget that bonds can go from AAA to junk in a matter of days. Some of the bonds in the markets I've looked at are already turning to junk.

There are some rules of thumb for bond allocation by age but with longer lifespans the ratios have been shifted out by 30 years so bonds probably only start making more sense once you are 60+. Although if things carry on the way they are now bonds may be completely pointless.

Yeah that's a bit concerning - and at that you've got to trust the rating agency, which after GFC I certainly second guess.

I'm holding my bond equivalent in cash for now (in a few currencies) to see what happens - deposit for house if market crashes and OBR event doesn't destroy my savings - or buy more shares if there's a market correction there.

dictator,

I have reduced the %age of bonds in my portfolio to around 4%,simply by not replacing them as they have matured. Most of my capital-some 59%-is in dividend paying NZ equities,with cash at 12% and approx. 20% in rental property.

I have raised the cash %age steadily over the past year or so,with most of it in short-term PIE funds. I think the market is somewhat overstretched and hope to see a significant correction-say 15%. In that event,I will reduce my cash to around 5%. I would not go below that.

To labour the obvious, It really does not matter how much you pay for any investment, or what anybodys' opinion is about the value of it at any given time. It matters only when you wish to sell that you are able to do so at or above your buy price. Only then is the wisdom of your investment realized. I intend to invest for my retirement, wher possible, by pre-purchasing as much as I am able rather than attempting to save/invest and purchase later. Risk of loss is possible both ways, each must judge which they prefer.

Point 10. Agreed. Get kids savings early. Our kids are thrilled with Clever Kash. We pay them for chores, the electronic elephant makes happy noises when it's fed money (electronically obvs) and the kids can check on their savings any time. It's a great system to incentivise saving and very easy to use.

Just hold your nose and buy overvalued assets. its going to make someone rich!!!

I totally agree with your bonds comment. Listed property has taken the place of bonds in my asset allocation. It'll get hit by an interest rate increase, but long term inflation will lift rents and recover the loss.

But I'm heavy in term deeps too for the first time for years - on the basis that NZ has a recession every year ending in an 8 for 50 years.

Dave2. I'm a life time investor and figuring out the right asset allocation strategy in this market is as tricky as its ever been. A recession could hit us and your faith in the recurring recession pattern system may prove justified but the old maxim of time out of the market being as risky as time in, also still holds true. Inflation seems to have stirred from its slumber which could test your TD strategy if asset values continue to rise.

dictator: I think you said to save 15% - if you are in the half who can afford it. My view is that if you low income you have to save 15% - you can't afford not to.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.