By Gareth Vaughan

The Reserve Bank has raised the spectre of it using more than one of four so-called macro-prudential tools to dampen a credit boom or bubble, but has given a strong indication it's not keen on using what has been the most talked about of the four tools it's considering, restrictions on high loan-to-value ratio residential mortgage loans.

The Reserve Bank has released a consultation paper on the four tools entitled Macro-prudential policy instruments and framework for New Zealand, plus a background paper and added a question and answer section on the tools to its website.

Although most of the public and media discussion on the macro-prudential tools has been around possible ways of cooling an overheating Auckland property market, the Reserve Bank notes the tools' role is broader than that. It's to enhance financial stability by increasing the resilience of the banking system during periods of rapid credit growth and by helping to dampen excessive growth in credit.

The Reserve Bank says the tools may provide support for monetary policy but aren't alternative tools to the Official Cash Rate. Nor are they likely to be used continuously.

The four macro-prudential tools, which would only apply to registered banks and wouldn't affect existing loan agreements, are:

- the countercyclical capital buffer (CCB), effectively banks holding more capital during credit booms;

- adjustments to the minimum core funding ratio (CFR), altering the amount of retail funds and longer-term wholesale funding banks have to hold;

- sectoral capital requirements (SCR), or increasing bank capital in response to sector-specific risks;

- restrictions on high loan-to-value ratio (LVR) residential mortgage lending.

See full detail and description of the four here.

Deputy Reserve Bank Governor Grant Spencer said these tools wouldn't replace the existing prudential regulation of banks already carried out by the Reserve Bank, but would be supplementary tools, used from time to time to help manage risks arising from the credit cycle. The four tools are the ones identified by the Reserve Bank that it says "may" have a role in promoting financial system stability.

A four step plan

The consultation document runs through four steps the Reserve Bank would take in deciding to apply one or more of the tools, starting with a systemic risk assessment and focus on whether debt levels and asset price imbalances are, or are likely to become, excessive and whether lending standards may be too loose. This will be followed by mulling whether macro-prudential intervention is warranted, selecting the appropriate instrument(s), and determining how the individual tool(s) should be applied.

"In some cases, the optimum response might involve using more than one instrument," the Reserve Bank says. "For example, during a credit boom it might be appropriate to not only constrain the build-up of leverage in the banking system with the countercyclical capital buffer but also to target high risk borrowing more directly (eg through the use of LVR restrictions)."

Judgement 'important part of decision making'

In terms of the four tools, banks would get varying "notice periods" of their impending implementation. For countercyclical credit buffers there'd be up to 12 months notice. For sectoral capital requirements banks would get up to three months notice. For adjustments to the core funding ratio there'd be up to six months notice. And for restrictions on high LVR housing lending there'd be at least two weeks notice.

"Macro-prudential instruments will not be applied in a formulaic manner. They will be applied in a forward looking manner and they will not affect existing loan agreements," the Reserve Bank says.

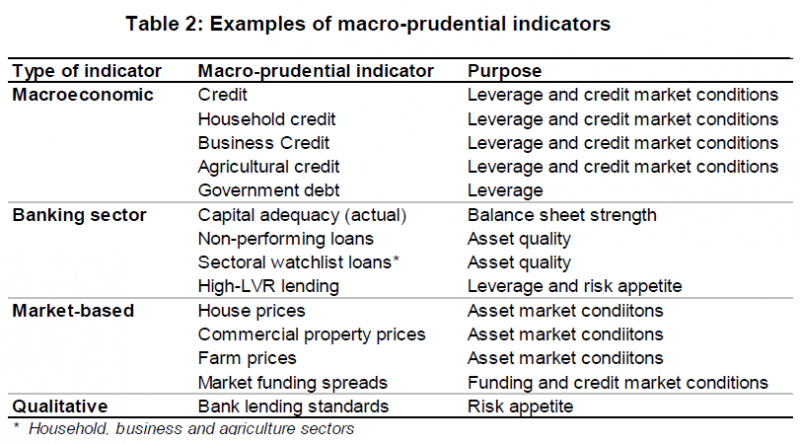

The central bank says it'll monitor a broad range of indicators on whether the use of macro-prudential tools is required, which will vary over time. These will be supplemented by both market and supervisory intelligence and stress tests of banking sector resilience, with judgement an important part of the decision making process.

The many problems seen with LVR restrictions

On the potential use of restrictions to high LVR residential mortgage lending the Reserve Bank points to several potential problems. These include; adversely affecting efficiency, favouring wealthy home buyers/investors over first home buyers, arbitrage through non-mortgage (unsecured) top-up loans, and a risk of "leakage" to the unregulated sector and foreign banks should there be an increase in new lending by the non-banking sector.

It also notes restrictions on high LVR lending would need to be "vigorously" enforced and monitored in order to reduce avoidance.

"LVR restrictions may particularly affect new home buyers with little equity," the Reserve Bank says. It doesn't raise the possibility of a first home buyer's exemption.

It also hints at extending the use of macro-prudential tools beyond banks to other financial institutions such as finance companies and building societies, if necessary.

"LVR restrictions would only apply to registered banks and could induce disintermediation towards the non-bank lending sector. Should there be a substantial risk of financial sector disintermediation, the bank might need to investigate the possibility of extending the perimeter of macro-prudential regulation."

In the background paper the Reserve Bank notes that LVR restrictions could take the form of an outright prohibition on mortgages that exceed a specified proportion of the property value (the loan-to-value ratio), or quantitative restrictions on the share of high LVR lending, either as a proportion of the lender’s housing loan book or of new housing lending.

"For example, when writing new loans, banks might be restricted to writing no more than 10% of residential mortgages with a LVR above 90%."

Analysis by interest.co.nz shows the country's big five banks, combined, grew residential mortgages where the borrower has less than 20% equity by NZ$3.3 billion, or 10%, during 2012. Home loans with LVRs above 80% are now up NZ$4 billion, or 12.5%, to NZ$36 billion since the Reserve Bank first mandated the banks break down their home loan books by LVRs in 2008.

As of December 31, borrowers had less than 20% equity on 24% of ANZ's residential mortgage book, or NZ$12.9 billion worth of loans. ASB was at 21%, or NZ$8.2 billion, Westpac at NZ$8.5 billion, or 24%, BNZ at NZ$4.1 billion, or 14%, and Kiwibank at NZ$2.3 billion, or 19%.

Concerns about the development of 'part-purchase, part-rent models of home ownership'

Of tighter LVR caps the Reserve Bank says they restrict the quantity of credit by limiting the funding available for marginal borrowers, reducing effective housing demand and increasing savings.

"In principle, house prices will tend to ease, reducing households’ ability to obtain credit and withdraw equity more generally. The effective demand for credit is therefore likely to fall more broadly. The strength of these transmission channels may be moderated by the fact that LVR limits do not directly affect the cost of borrowing – they simply restrict the ability of a specific group to borrow. While this may constrain some households, it is also possible that the demand from others with sufficient wealth might continue to drive house price growth," the Reserve Bank says.

"LVR limits provide a highly visible signal of the central bank’s discomfort with developments in the housing market, which is likely to increase its impact on expectations . However, there is a risk of expectations playing a destabilising role under some circumstances. If caps are expected to be tightened, households might respond by bringing forward borrowing. House price growth might then accelerate, at least temporarily. These effects may be avoided by implementing limits over relatively short periods of time. Accordingly, the notice period could be as short as two weeks for LVR restrictions."

Further, the Reserve Bank says if households are constrained by LVR limits over an extended timeframe, the structure of the housing market could evolve in ways countering the intended effect such as through the emergence of part-purchase, part-rent models of home ownership.

"In such a scenario, underlying demand for housing would remain unaffected and, hence, house prices would be unlikely to react to changes in LVR limits. This suggests that the use of LVR limits would have to be accompanied by tight market surveillance; these risks are expected to be mitigated by the temporary nature of such restrictions, which are not intended to be in place for protracted periods," the Reserve Bank says.

"An unintended consequence of LVR limits is that they will tend to directly impede some viable borrowers’ access to home ownership, or to use their equity for other purposes."

What about debt serving ability?

Meanwhile, the central bank notes debt servicing ability has an important bearing on the default risk of mortgage lending, and that some countries have applied restrictions on debt servicing ratios as part of their macro-prudential frameworks.

"While the Reserve Bank is not contemplating such measures at this time, our regular assessments of financial conditions take into account trends in the household sector’s debt servicing burden as well as bank standards applying in this area. The impact on the credit cycle is less well documented, as relatively few countries have instituted LVR caps in a macro - prudential fashion," the Reserve Bank says.

"The available evidence suggests that imposing LVR caps during booms slows down real credit growth and house price appreciation. One recent study finds, for instance, that tightening LVRs tends to reduce real credit growth by 1 – 2 percentage points and real house price appreciation by 2 – 5 percentage points. The latter effect on property prices is, however, not as clear cut in other studies."

But whilst the evidence is generally supportive of the effectiveness of LVR restrictions, the Reserve Bank notes LVR restrictions have often been deployed in countries with fixed exchange rate regimes (such as Hong Kong) with little discretionary monetary policy capacity, and as part of the micro-prudential framework rather than as macro-prudential interventions.

Should they be used, LVR restrictions would typically be removed when there was evidence housing credit demand had cooled.

On the minimum core funding ratio requirement, the Reserve Bank notes its introduction (in April 2010) has seen the system-wide core funding ratio rise from a little under 70% in October 2008, when the Reserve Bank first consulted on the policy, to 85% at the end 2012. It says this reflects both an increased volume of stable funding and relatively low rates of lending growth over the period. The core funding ratio minimum is currently set at 75%.

Countercyclical capital buffer could be higher than 2.5%

Meanwhile, the Reserve Bank reiterates that a countercyclical capital buffer framework will be implemented on January 1, 2014 alongside other aspects of the Basel III capital adequacy regime in New Zealand.

"The CCB framework aims, during the credit cycle upswing, to provide the banking system with an additional cushion against subsequent losses or sharp increases in risk-weighted assets that may be associated with periods of credit downturn. When risks to the New Zealand financial system are judged to be low, the CCB will be set to zero. However, where private sector credit growth is judged to be becoming excessive, banks may be required to hold a CCB, which will provide the banking system with an extra layer of high quality capital (common equity)."

"The CCB rate is typically expected to range up to the equivalent of 2.5% of risk - weighted assets; however, there is always the possibility that it may need to be higher," the Reserve Bank says.

As for sectoral capital requirements, these would single out specific sectors where excessive risk was being taken on, such as households, commercial property or the farming sector.

"The requirements would typically be applied through overlays to sectoral risk weights, say for housing lending or agricultural lending, but could also be applied through a capital add-on that is calibrated as a proportion of banks’ risk-weighted exposures to the sector. When sectoral risks are judged to be low , there will be no macro-prudential SCR in effect . Sectoral capital requirements applied via risk-weights would be part of the minimum regulatory capital requirement, whereas a capital add - on would be treated in the same way as the CCB."

Finance Minister Bill English last week said he expected to sign a memorandum of understanding with Reserve Bank Governor Graeme Wheeler by the middle of the year on the macro-prudential tools. The Reserve Bank says the memorandum will provide a framework for the use of the tools by setting out the agreed objectives, instruments and operating guidelines for macro-prudential policy. The memorandum will be published on the Reserve Bank’s website.

Submissions close on April 10.

This article was first published in our email for paid subscribers. See here for more details and to subscribe.

4 Comments

RBNZ is not going to do anything to cause a fall in house prices.....or improve affordability.

Their attention is more on the banks balance sheet if and when a fall in house prices affect the banks profitability and solvency....not another 2007 event !!!!

All talk will remain TALK

I agree Kin, if the RBNZ implements any of these tools it will be to protect the system from failure (protect a banking collapse) rather than be doing so to influence the housing market without raising rates. They will do both if/when the time comes.

Babyboomers sell their big houses in this current fat market to make a handsome lump sum for their retirement.

Govt has no incentive to dampen this motion. It is much better to let new house owners to pay for BB's retirement costs than to do it by the Govt. Also, have you heard any noises from BB about this crazy house prices? Of course not.

PE's in their teens and interest rates in nappies - needs to be t'other way about, as history will show.

Ergophobia

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.