By Jenée Tibshraeny and Gareth Vaughan

Flipping - buying a house and reselling it quickly for a profit - has become a favourite pastime for some Auckland property buyers.

Barely a week goes by without stories appearing in the media of astronomical profits being made by people on-selling houses, sometimes within only 24 hours.

Yet there’s more to this than buyers making a quick buck.

With the real estate sector currently excluded from New Zealand's Anti-Money Laundering and Countering Financing of Terrorism Act, there's no doubt some money’s being parked in Auckland property for nefarious purposes. (See Caroline Courtney's call for action on this from last year).

Flipping is also seeing property buyers game the Reserve Bank’s loan-to-value ratio (LVR) restrictions on bank mortgages.

Interest.co.nz has been told of ethnic Chinese buyers tricking the system by essentially getting mortgages to fund the total 100% value of the properties they are buying.

That's not to say this type of behaviour isn't being practiced by other ethnicities. It's just that we've particularly heard about it taking place in the Chinese community.

These "back-to-back" sales are said to be hiking Auckland house prices, and potentially leaving banks more exposed than they think.

What’s clear is this behaviour is occurring. What’s unclear is how widespread it is. Here’s a look at how it works:

The scheme

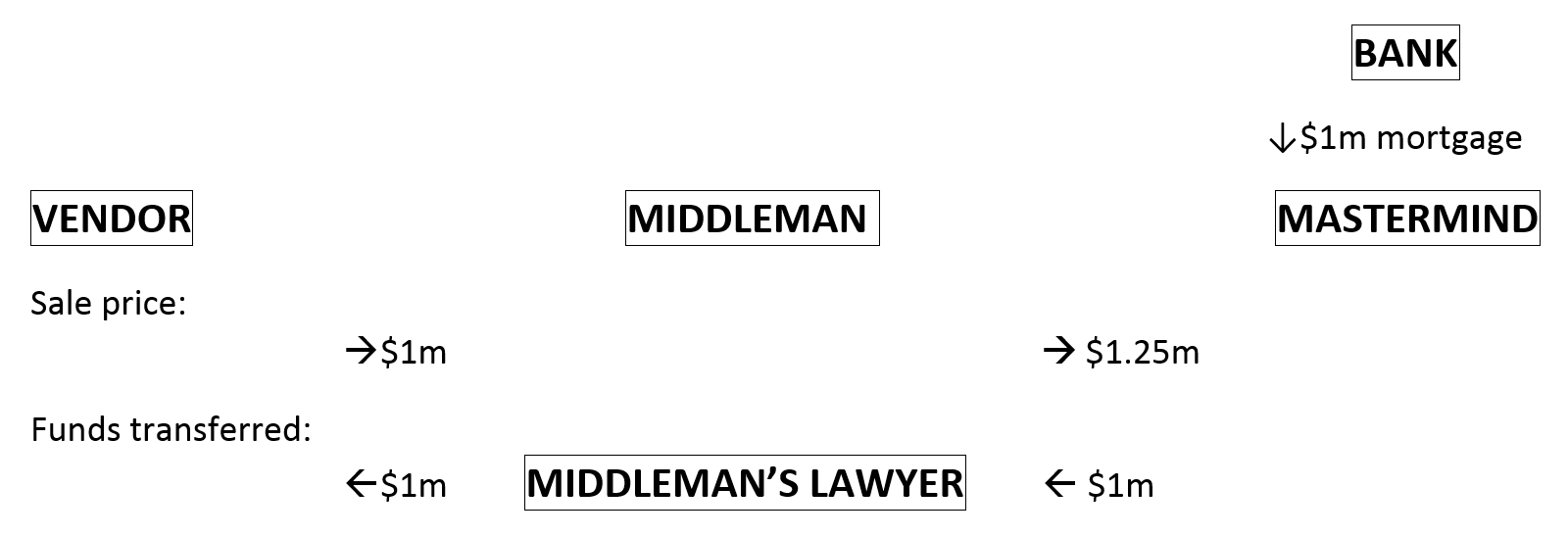

A person we will refer to as the ‘Mastermind’, wants to buy a property on the market for $1 million.

Yet they want to sidestep LVR restrictions, which generally require you to have a 20% deposit, and buy the property 100% funded through a bank loan.

So they get an associate, we will refer to as the ‘Middleman’, to sign a sale and purchase agreement to buy the property for $1 million.

The Mastermind signs a separate sale and purchase agreement to buy the house from the Middleman for $1.25 million, with both contracts due to be settled on the same day.

The Mastermind then gets a tame valuer to provide a property valuation of $1.25 million and uses this to apply for a $1 million mortgage from their bank. The valuer may be tipped off at this stage.

To the bank, it appears they are providing a loan of $1 million on a home which is valued at, and is being purchased for, $1.25 million.

The purchase of the property by the Middleman and its resale to the Mastermind are then usually settled contemporaneously, meaning the Mastermind essentially pays the original vendor $1 million via the Middleman’s lawyer, rather than the Middleman seeking their own funding to pay for the property. The Middleman never actually takes possession of the property.

So the Mastermind gets a $1 million property with 100% bank funding (assuming they meet the bank’s lending criteria by proving they can service the mortgage), while the bank has the transaction recorded as meeting LVR rules because there's supposedly a 20% deposit.

The bank sees the property’s title. This shows the property’s being on-sold quickly, but doesn’t show the extent to which the price has been escalated.

Altogether, the set-up looks like this:

Provided the Mastermind fulfils their mortgage repayment obligations, the bank benefits from the property’s value being inflated, as the mortgage it writes is bigger ($1m as opposed to $800k for example), so it earns more in interest.

Banks also tend to regard Chinese property buyers as low risk, as they typically have access to money and so meet their mortgage repayment obligations.

The role of the valuer

For this flipping scheme to work, it’s essential the valuer agrees to inflate the property’s valuation.

ANZ, BNZ and ASB confirm they only accept valuations from valuers they’ve approved. However Westpac’s valuation requirements will vary depending primarily on the requested LVR.

Westpac says: “A registered valuation is required if the LVR is over 80% or sometimes to confirm the LVR is below 80%. In that situation, we offer to order a valuation for the customer or the customer can arrange one of their own.”

Interest.co.nz has been told the lawyers involved in this sort of transaction won’t typically dig very deep into the matter if it looks like a normal conveyancing file.

The Middleman may understand how they are being used in the scheme and possibly be paid a fee for their part in the transaction, but it won't be anywhere near the $250,000 profit they have supposedly made on paper from the deal.

Alternatively, they may be a family member who signed a few documents and was oblivious to the extent of their role in the set-up. They could also be based offshore.

The Mastermind could be a company, but it’s most likely they’re an individual living in New Zealand.

Contact us

As we foreshadowed in June, the major banks have now closed the door on mortgage-seeking foreigners with offshore income, or left it ajar in ANZ's case.

They have played down suggestions that this was, at least in part, due to concerns about mortgage fraud, even though their Australian parents halted lending to non-residents and temporary visa holders earlier this year, with reports both ANZ and Westpac had discovered they had approved "hundreds" of home loans backed by fraudulent Chinese income documents, allegedly put together with the assistance of mortgage brokers.

As noted above, we know some of these "back-to-back" sales, where mortgage fraud is being perpetrated, are taking place. But we don't know how common this behaviour is.

As we did in June, we again ask for anyone with information about such fraudulent deals, and mortgage fraud more broadly, to contact us. To maintain the integrity of the financial system, fraudulent transactions need to be unwound. You can contact me, via email, at jenee.tibshraeny@interest.co.nz.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

61 Comments

I've seen valuers as a weakness in the system for some time and have often wondered if there are any who are providing dodgy valuations. Where valuers fail to do their job it's no different to credit rating agencies giving AAA to something that is far less than that.

This is also a set up for people to stop paying mortgages. If there is little or none of their money in the property it's no big loss to stop paying. How many mortgages would immediately go into default if the mortgages end up underwater?

Most banks had an agreement with E-Valuate for all Registered Valuations to be ordered via the bank on behalf of the customer through their portal then the valuations request would go to one of a group of approved valuers. Most banks signed up for this however it seems that most are now not sticking with it. Valuers are being used who do not meet the requirements for E-valuate and yet the cost is the same. So no benefit to real customers wanting a real value and high risk to a bank.

Is the IRD smart enough and quick enough to collar the Middleman over the non-existent profit?

If not what are we paying them for and why do we bother to pay our own taxes?

Hell No, the IRD are too busy at the end of town doing working for familiy credits and school donation refunds, they not care about the real money - too hard, computer systems not big enough.

IRD would catch this arrangement with a simple data query to Land Information New Zealand and tax the $250k profit. With the new brightline test there would be no defence.

This article has conspiracy nut all over it. It assumes the registered valuers are fraudulent crooks. That has not being my experience with them and I would want to see evidence of wide scale fraud before accepting this story.

I agree,,, this story is very fishy and I cannot believe a word of this Fiction / scenario.... registered valuers are honest and they risk their whole company and career if they do such a blunder .... Banks do not lend on any property without checking against QV, E value and the Valuer first .. they are not Stupid !!... If the story is true, The mastermind can only get 20% LVR once and should have to have quite a strong position to service a loan of $1M .. so someone like that why bother risking a lot to do such a trick? doesn't make sense even it was a speculator ,,, no property will appreciate by 25% in one year..then there is the 15% CGT if sold under two years ... there is no logic and no profit in this ....this is far too much exaggerated ....

The gain on disposal of the property is taxed at the owner's marginal rate (33% for individuals who earn over $70k).

unfortunately it is happening, there are syndicates operating in this fashion: FYI banks aren't the only source of funds.

The solution to this is easy. Make the tax payable at time of settlement. Very easy to see that the property has been purchased less than 2 years ago. Having to pay $66k in tax on this should put a stop to this practice.

That assumes the person can be taxed in NZ.........loads of Taxation Agreements between NZ and other countries.

dp

duplication gremlins

BB - have you considered that Options to buy may the Middlemans tool ?

Fascinating thanks. However, doesn't the newish bright line test mean that Middleman owes taxes on that supposed $250,000 profit? Any idea if these are being dodged or counted as part of the cost of business?

That's just fraud isn't it?

Yes

The problem with tax is the time delay...no issue with IRD at the time. The issue arise at a later date, often much later if a return is actually filed. If no return is filed, the a tax payer has yet to take a position in respect of that transaction...... So it's just a late return. And not doubt middleman man has left country, been struck off (if a company) or was fictitious anyway. Tax won't be a hindrance for this scam to work.

Buyers and sellers need to provide valid IRD numbers which require NZ bank accounts. They also need to provide identification papers and tax number if tax resident in a foreign country.

If the middleman is a non-resident their solitcitor would need to withhold tax under the new Residential Land Withholding Tax or risk being liable themselves (see http://www.ird.govt.nz/rlwt/ir1101-rlwt-declaration.html).

This article needs more research and evidence, at the moment it is all innuendo and "Chinese" fear mongering.

very correct. As you have mentioned it looks like this article is either outdated or written by a conspiracy theorist.

Its a good thing now that the IRD will collecting the ird numbers through the deal - where as this wasnt happening until a year ago - thanks to our governments "open door mat" policy.

Been waiting for this to rear its head

Overt evidence was published about 5-6 weeks weeks ago. Friendly valuers not required

The case of a run-down dump in Otara changing hands 5 times in less than a month is symptomatic of a collusive action on the part of a few associated players to "tick the price up" by frequent transactions. Ticking the market up or down is a common practice in financial markets

It's not the value of the property being traded. It's the new value of all the properties in the immediate vicinity of the dump that increased in price by $200,000 in one month. All those nearby properties can now be revalued and refinanced

Which means the original money can now be taken out having been nicely laundered thanks to that one dump being ramped up

With each "ramp up" being subject to tax... So very inefficient.

Not sure how the money has been laudered as the source would be easy to locate (i.e. each purchaser would be asked "where'd you get the purchase money from?). Laundering money normally requires an untraceable source of funds (e.g. a bakery with lots of little cash customers).

If the person perpetrating this scheme owns 10 houses in the neighbourhood that are each now worth $250K more than last month, and the capital gains are realised, that is $2.5M income from nothing and with nothing. So what if you lose a third to tax.

I said on the site a few years back, following an argument with Don Brash where I said the same, that taxing capital gains is like taxing a thief. I think this article is a touche.

If someone is paying a "middle person" to pay an extra 20% for a property so they can pay tax on that illusory gain, and this results in that person being able to sell 10 other properties at a 20% mark up which is also taxed; I cannot see the problem.

This article was about manipulation of the LVR for financing purposes.

If you are talking about price manipulation all I can say is if the buyers are bona fide third parties happy to pay the purchase price then there is no issue. Furthermore, if taxpayers get a third of those gains then I say "more please"...

Heavy....making yourself sound more like a lightweight.

chuckle .. also sounding like a stooge

Don't have to sell the other 10 properties ... just refinance them to the hilt ... pull the original deposit out plus any additional equity .. and walk away .. disappear .. it then becomes the banks problem as per the theme of the original article

No sale, no transfer of title, no LINZ, no conveyancing, no IRD - clean

NB: all valuers pay particular attention and take account of recent sales and values in the immediate neighbourhood

Take the tin foil off your head and stop talking smack.

This housing 'situation' certainly brings out the very worst in people. Let's hope the system catches them out. When the boom ends some people might have to start doing some honest work.

And then there's the other scam.

I own a house with a mortgage.

My mate owns a house with a mortgage.

I buy my mates house for an inflated price (larger mortgage) and rent it back to him for a nominal amount.

My mate buys my house for an inflated price (larger mortgage) and rents it back to me for the same nominal amount.

On the ground nothing has changed, but on paper both me and my mate have suddenly become "investors" with all the associated tax benefits, plus a bunch of cash in out pockets to do the whole thing over again.

Except that you are supposed to rent it out at market value. The other issue is when you find out your mate is addicted to P and starts cooking it in your house. He defaults on the mortgage so it goes to mortgagee sale and you can't sell your house because it is now a P house. The house you live in gets sold for 75% of what he paid for it and your house gets sold for much less because it is now contaminated with P. So you are now homeless and poorer. The other more likely issue you will encounter is the new 40% LVR for investors would cap how much you could borrow to make it worth while. This isn't that much different to people that used to buy their house with a trust and then rent it out to themselves and claim the tax benefits. The government cracked down on that some time ago.

..really? If you own 5 rentals via a company and rent one of these yourself, I'd suggest there's b-all IRD could do. If you owned 4, same thing. Two and you might have fun, but even with one you can still do it. The reason being they have to prove tax avoidance. Where's the tax avoidance if you pay market rent?

Market rent won't save the arrangment from tax avoidance and the IRD, see http://www.stuff.co.nz/business/money/3097565/Test-case-rules-out-self-…

Did you actually read the article you cited?

"Wellington tax adviser Brent Gilchrist said "Mrs B" was not a great test case because the arrangement was not cleverly executed, with no tenancy agreement or rent payment"

and

"But if the property was one of a few investment properties owned by the LAQC and the family was treated like an arms-length tenant, then there was still room to allow losses from such an arrangement to survive an IRD "attack", he said."

Read between the lines. Own more than one home, do the paperwork correctly and the IRD are not touching them, its all bluff (even this case no penalty was imposed - strike you as odd?) - they do not want the publicity of a loss.

So get your kids to pool their resources, form a company and rent from the company. Lets all be landlords....it what this govt wantst aint it?

There was rent paid of $300 per week (read the case http://www.ird.govt.nz/technical-tax/case-notes/2009/cn-2009-own-home-l…).

I wouldn't believe a thing Brent Gilchrist wrote or you could end up a criminal like him;)

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=111…

The avoidance comes when the arrangement is solely for tax purposes. Like being the sole beneficiary of the trust that owns one house. If the company had multiple shareholders and multiple properties then you could argue it was a clean way of dealing with the property and my guess is you would get away with it.

Mostly I would take this article as a conspiracy theory, although there has to be one or two of these for sure. It would be good to hear more detail of the properties flicked multiple times (see 'two other guys" above) and just who are the parties and how connected they are.

As for the IRD it would be good to hear from them as to how much tax they are collecting with the bright line test, and does it work with the same day flicks. A story from the coal face IRD would be informative.

Finally, if there is anything in this at all, there is the Fraud aspect on lending, lack of security for the bank (mentioned in the very first comment above) right up to a threat to bank stability. While the rest of us painfuly pay our tax, when the s#*t hits the fan, the sleezy guys won't be found in New Zealand

On the face of it, this appears to be a story and nothing more.

Can't really see Chinese wanting to borrow 100 per cent finance from a NZ Bank when they generally have cash and/or they can borrow money far cheaper in China.

Don't also believe any valuer would be prepared to value a property 20 per cent higher than what someone has paid for it, as they would have enquired from the real estate agent what the original sales price was!

There is no way that the valuer would want to be caught doing fraud and lose their license plus the bad publicity once caught!

You're not getting it. If I said to you that, without any input of your own, you could buy and hold a property for a period and sell it at the end, pay the fees and walk away with $$$$$ I suspect you would entertain the notion. It will end when capital gain is not guaranteed and the lenders will find their clients mysteriously evaporate leaving a property which is not worth what they have lent on it. I say, bring it on.....

Sorry, don't think you are getting, with respect.

What is in it for a registered valuer?

He isn't going to falsify a valuation knowing what the original purchase price is and risk going to jail for the price of being laid a valuation fee!!!!

It is hardly an exact Science though. Very subjective. Statistics are manipulated at will to give the "correct" outcome. You cant tell me that relationships between valuer and purchaser don't come into play on occasion.

Have you never meet a valuer who massages the value to magically equal what the purchaser requires via mortgage? I have and only interest seems to be having their bill paid after 5 mins cut and paste report.

I mean really how hard is it to pull numbers out of the air???

That is my experience too, 3 properties bought to date and (un)surprisingly the valuations are precisely the figure that was agreed as the sale price, not 1 cent either way. I imagine it would be very inconvenient if the valuation was found to be anything else, who would blow against the wind?

I have been dealing with registered valuers for years and I can tell you with confidence that no valuer

will value "high" just to get a fee.

Arguing with a valuer may get a tweak or two as it's not an exact science, but the sort of numbers quoted in the article where a property is hyped up 25% are impossible.

On the contrary in the 100's of valuations I have done over the years, I have met only 2 valuers that where the "speculators friend" and both where struck off within a very short time.

Further any lawyer who suspects, but collaborates with what is essentially a fraud on the bank will be disbarred. I have been an actual witness to this practice on one occasion and got much satisfaction when the lawyer got 3 years jail for his actions.

This whole article is, in my view, totally made up by people who need to create a headline. Bring on actual examples and I will apologise immediately.

everything in this article sound like fiction .( or stirring the proverbial ) .. nothing adds up, there is no possible gain to anyone ... YET , here is the rub, the article illudes if this fraud is widely spread and questions whether if it is/has affected house prices ? ... that is what exposes the credibility of this story !!

There is plenty to gain.

1) 100% finance

2) A sale in the area at a high price. might help push prices up and make anyone buying it for say $1.15m feel like they are getting a bargin..

3) no tax on capital gain if sold within 2 years provided it sells for less than $1.25m. saves $66k if sold for $1.25m

The middleman bought a property for 1m and sold it for 1.25m on the same day to Mr. Master Mind. The middleman has to pay tax on 0.25m gain.

Middle man is long gone and won't pay. If they hang around the whole thing blows up.

A close associate needed a low valuation about 10 years back, because he was a relative of the RE agent. When told that that the valuation was a bit high, he asked "what do you want it to be", and subsequently dropped it 20%. You must know it isn't an exact science Big Daddy, so there is a bit of leeway in justifying a price either way. Ever been to the family court and seen the disparity between the two parties valuations? Come one my man, a bit off your game today.

It's definitely going on. But not limited to the aforementioned nationality.

The Ponzi is real people.

Dropping a valuation is an easier thing to achieve as it's a matter of conservatism. Even so that has strict limits.

The article was trying to make the point that valuations can be hydrauliked to defraud the bank. The most tweak that should be between two identical valuations is around 5% either way and to be able to "flip" with this sort of slim margin is a hard ask.

You can achieve a big difference if the same property can viewed from two different perspectives e.g as a home to live in or as a development site. Likewise a block of flats as a total investment or each flat as an OYO with its own title.

Moral of the story is that Asians with understanding and support from John Key has Scr$#@ the system and NZ.

Blame everyone or national JK who have have become blind and deaf to truth and when speak only speak lie or how else can they defend their masters who are controlling them by remote.

Shame.

.

The only solution is tax foreign buyers - all who are not citizen or resident and if as per PM hardly any than why not impliment tax as canada. If the number is not too big why not impliment the tax to foreigner and change public perecption about govt working for foreigners - why be afraid.

http://globalnews.ca/news/2887766/data-is-the-metro-vancouver-real-esta…

This the reality, government may try to delay it but cannot avoid it. If government could stop no bubble would ever burst as whenever any bubble burst is harmd the ecenomy abd society.

This article is like the Heather Du Plessis fraud for obtaining guns...yes if I am a criminal I could game anybody for anything...I could tell the bank manager that I am Bill Gates and earn 1 billion dollars a year, am failing to see the relevance?

I would have thought the simple solution to this problem would be for the banks to use the government's valuation on the house - ie the CV. This would help add a bit of stability to the runaway house prices too.

CV's are so far off the mark it is almost criminal to base a tax on it. Nothing sells for anything less than CV + 20 - 25% in my area. Sometimes is it CV + 50% or more.

There is a big story about money laundering but no criminal prosecution because of deal done to return the money. Will that be the rule henceforth for all scammers too ?

Firstly Valuers in NZ have consistently stated that their values have been below market prices ......and market prices end up being the new valuation. Prices paid have very little to do with valuations especially in Auckland but not isolated to Auckland.........Price paid is aligned with ability to service the debts rather than any valuation of land + bricks and mortar etc.

This article makes claims that there is fraud but I would suggest a closer examination of the facts would be in order...........Are there any Options involved on the properties that are being sold? I'm assuming that Options to Buy are in place due to the same day settlement of contracts. If there are Options to Buy then I would assume the Middleman had the Option to Buy expiring on the same day the Mastermind purchases the property.........Under this practice the Middleman has never owned the property so if one hasn't owned the property this cannot be a fraud and there is certainly no taxation obligation issues to be met as no income derived.....perhaps tax deductions for costs involved.....;-) ....

NZ moved away from LVR's years ago because they are known to cause price distortions as people find legal (and maybe not so legal) ways to achieve their goals.

All the issues NZ has with house price distortions are because of an incompetent network of rules and regulations........there is no protection of the constitutional rights of the people (shame the authors don't think that is a worthy cause to bring to the public's attention) as all the protection is granted to the system which keeps dishing up more distortions and that is where the real fraud is!! When are you journalists going to deal with the real causes of stupid house prices?? It is the rules that make the system that artificially interfere with the free market that is causing the problems. You cannot have freedom and restriction operating together.

Why onlly get 100% loan by fraud, can maake hard cash. It is a scam but who cares and what to expect from our denial PM.

sounds like a variation on pump and dump.

buy some houses in a area, then start turning one over pushing the price up each time, locals help out here also when selling matching the new price in the area.

when ready offload all your houses and walk away with the profits

works well in a bear market, and guess what if you pay your taxes on the profits no one will come after you

https://en.wikipedia.org/wiki/Pump_and_dump

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.