Rising debt-to-income (DTI) ratios of new borrowers in New Zealand have caught the eye of the Reserve Bank of Australia (RBA).

The RBA is similar to the Reserve Bank of New Zealand (RBNZ) in that it produces two reports each year on the stability of the local financial system.

And since Australia's big four banks each have considerable businesses in New Zealand, the RBA also keeps on eye on what's going on here.

So when it says that rising debt-to-income ratios for new lending in New Zealand pose additional risks, not just here, but to Australia's financial system, we should take note.

New Zealand bank bosses reckon an ideal DTI ratio in the local context would be about five to seven times. Worryingly, most borrowers are at levels more like nine to twelve times. See more on that here.

The RBNZ last year asked the government to add a tool limiting debt-to-income ratios to its macro-prudential toolbox. As Governor Graeme Wheeler explained to Parliament's Finance and Expenditure Select Committee in February, a DTI tool would complement the Bank's ability to restrict high loan-to-value ratios on home loans.

But Finance Minister Steven Joyce kicked the policy into touch, effectively until after the 23 September election. Many have argued that this was due to the prospect of a load of bad press ahead of the general election. (Think front pages full of aspiring first home buyers unable to get on the property ladder because the mortgage required would have been too high compared to their incomes).

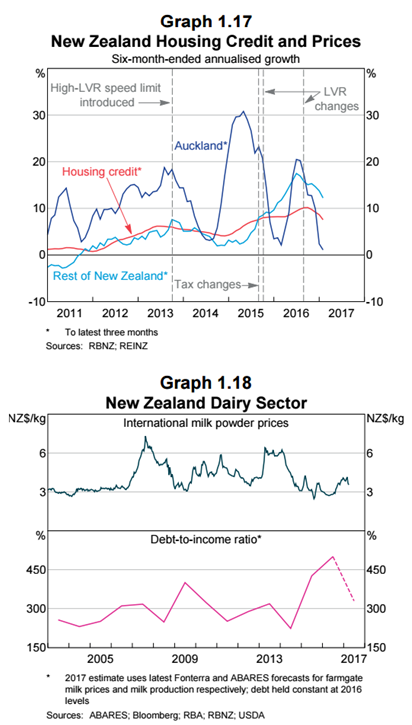

The RBA on 13 April released its latest semi-annual Financial Stability Review. Below are its comments and charts on New Zealand. It also focuses on risks faced by New Zealand's dairy farming sector:

The four major Australian banks all have large operations in New Zealand, with business models that are similar to those in Australia (see ‘The Australian Financial System’ chapter for more details). Economic and asset price cycles in the two countries are also strongly correlated, and hence any widespread losses in New Zealand would likely affect the Australian banks at a time when they were already under stress from their domestic operations.

Housing prices and aggregate household debt have risen strongly over recent years, although price growth has slowed somewhat over the past six months. New Zealand housing prices now average about 6½ times annual average household disposable income, which is very high by international standards (Australia’s internationally comparable ratio is currently around five, though making international comparisons can be difficult; Graph 1.8). While housing price increases are partly being driven by fundamental factors (including a high rate of migration to capital cities), there is a risk that these factors could slow or reverse. The share of new loans with high debt-to-disposable income (DTI) ratios (greater than six) has also increased, to be around one-third, and investors account for nearly half of such loans. More broadly, the investor share of all new loans has been high (peaking at just under 40 per cent in mid 2016). This presents additional risks, because high DTI borrowers are less resilient to income or interest rate shocks, and investors may be more likely to sell in a downturn, which could exacerbate price falls.

In response, the Reserve Bank of New Zealand (RBNZ) has introduced three rounds of macroprudential policies since 2013, mainly targeting high loan-to-valuation (LVR) loans and investor borrowing. These policies have helped to reduce the share of riskier housing loans on banks’ balance sheets and appear to have, at least temporarily, slowed the growth of housing prices (Graph 1.17). The RBNZ has requested that restrictions on high DTI lending be added to the set of agreed macroprudential tools outlined in the Memorandum of Understanding on macroprudential policy with New Zealand’s Minister of Finance, which could be used to contain a further build-up in housing risks.

In contrast, the immediate risks in the dairy sector in New Zealand have subsided due to a rise in global dairy prices, though some underlying vulnerabilities remain (Graph 1.18). Dairy sector debt has continued to increase, and the more highly leveraged, higher-cost farmers remain somewhat vulnerable to any future weakness in dairy prices or a rise in interest rates.

7 Comments

"The RBNZ last year asked the government to add a tool limiting debt-to-income ratios to its macro-prudential toolbox." .. "kicked the policy into touch, effectively until after the 23 September election".

When the brown stuff hits the fan I wonder who will blame the government and electorate who put them there before they blame the RBNZ?

I can hear the cries now, "RBNZ fails again", "RBNZ out of touch with worlds best practice".. etcetera.

The RBNZ is already failing on DTI limits by it own standard. The RBNZ told the Minister earlier this year that consultation on DTI would have begun in March. see here

Where is is the DTI proposal for consultation from the RBNZ?

Did you read the article your posted?

"The Bank has indicated that public consultation will commence in March and occur during the first half of 2017."

So one assumes the "full cost-benefit analysis on Debt-to-Income (DTI) limits and public consultation", which was requested by the minister, will come after than public consultation phase - which won't be finished until the end of June.

The RBA is trying to highlight the effects of macroprudential policies, something which it hasn't really been able to do because of ideology or political pressure. The Aussie central bank is under much pressure.

RBA or for that matter RBNZ knows nothing and do not have the experience to raise concern. If you do not believe ASK national government who knows everything and as per them their is nothing to worry as their is no housing crisis.

9 years in power can make anyone arrogant to feel the same way as national that is I, Me, Myself.

Election approaching in NZ. Think and Vote.

New Zealand housing prices now average about 6½ times annual average household disposable income, which is very high by international standards (Australia’s internationally comparable ratio is currently around five

That is a worry !

Banks have been writing these loans for years and backslaping themselves on year on year record profits. Now their owners call foul, seems a bit rich.

Note dosent mean this is correct. I note no political option is promising to bring in dti to reign in the debt injecting ponzi junkies.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.