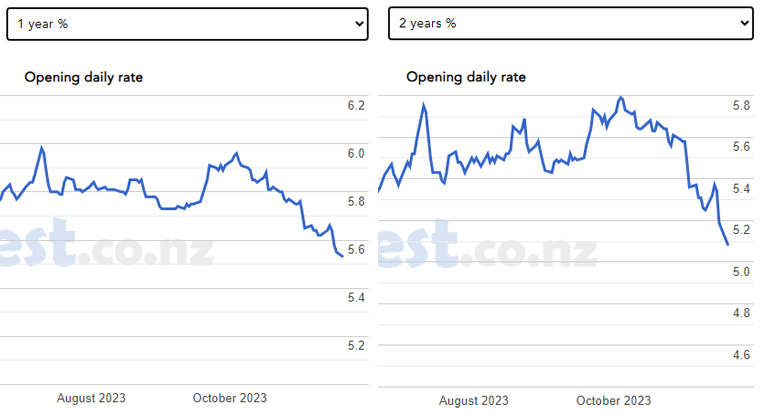

Regular readers will have noticed the sharp recent reductions in wholesale swap rates, especially for 1 and 2 year durations.

But neither home loan rates, nor term deposit rates, have moved in the same direction after the wholesale rates peaked in early October.

Swap rates and term deposit rates both have an influence on the mortgage interest rates offered. Customer deposits (which include much more than household term deposits) are the main funding source for home loans, and the wholesale markets also have a strong influence, especially in their role to hedge the 'borrow short, lend long' risks that banks face.

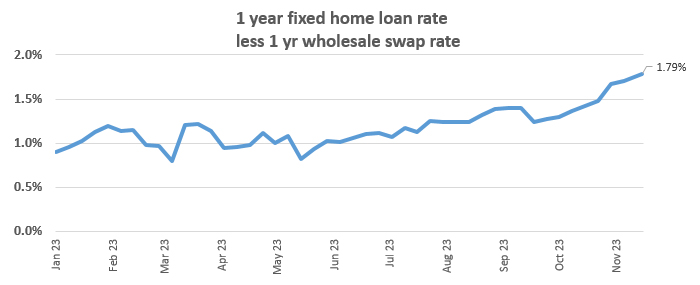

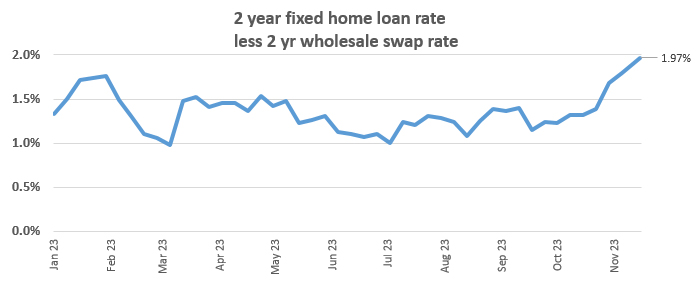

The dive in wholesale rates, driven by global forces especially out of the US where inflation's impact seems to have passed (and the US Fed is no longer under pressure to raise rate), has sharply raised the margins on home loan rates.

Margins to swap have risen to their highest in 2023, and may now be heading back over 2% and the sort of levels that were 'normal' from the GFC to the pandemic. We are possibly coming out of an unusual two year period of low margins to swap.

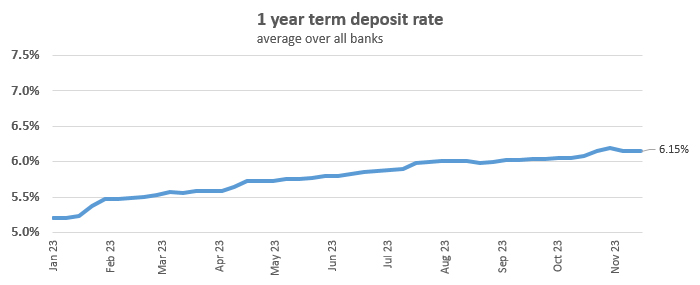

But holding mortgage rates up will be much higher term deposit rates, at levels we haven't seen since November 2008, 15 years ago. These currently have the dominant influence on home loan rates.

But if term deposit rates fall in line with recent global rate shifts, then some chunky opportunities for lower mortgage rate offers could open up.

Wholesale markets currently price in an OCR rate cut in the middle of 2024. Yes, a -25 bps cut. ANZ economists recently abandoned their view that the RBNZ has one more +25 bps rate hike in mind in early 2024 in the face of the money market realities.

Banks will be reluctant to give up the margin improvements. After all, the ASB parent company recently complained about the 'very low' mortgage margins in New Zealand. And the ANZ parent company skited about their dominant position saying they didn't have to offer 'best rates' because of this dominance.

However if lower global rates embed and are reflected here, one of the big banks is likely to move lower in their retail offers. We will probably see that first with shifts lower in term deposit rate offers. BNZ's current 6.25% one year term deposit 'special' (which expires on November 26) may well be the high point for a while from a main bank.

And if TD rates start dropping and stay lower while background benchmark rates also stay lower, then lower home loan rates are sure to follow. Certainly, there is no demand pressure in our housing markets to keep them up. And after all home loan lending is where the main demand pressure comes from in New Zealand and that pressure isn't building because the 2023 spring housing market is turning out to be something of a damp squib.

46 Comments

DC - I have been quite critical of your muted view on swaps, so I appreciate this balanced and thoughtful analysis.

LMF 🍿

"the 2023 spring housing market is turning out to be something of a damp squib"

Says it all really....

Currently the market has one flat tire, come Autumn 2024, there will be four.

Those that said it would be anything other than a 'damp squib' never, not even once, had any serious, nor realistic, nor believable analysis or reasoning to back it up.

And the loudest voices talking this nonsense have been those who operate for profit, and therefore far from impartial and yet they pretend to be (ComCom take note), but are reported and echoed ad nauseum. NZ's property information market is a mess.

95% of the analysis in the comments section of this website (and others) is anchored firmly in hopium.

Really? Most seem to say the opposite! Retired Poppy, Dgm, and many others have had opinions predicting drops in home values and sales. On guy (forget his name) keeps banging on about a 50% drop in house values, and many talk about a dead cat bounce or other such idioms.

There is plenty of Hopium on both sides of the argument. The guy banging on about 50% falls is ODing on Hopium that he can pick up a house for $300k.

Yeah, what a fool hoping that NZ society can generally get paid enough wages to afford a family and a house to live in..

And to think, people in India are coming here to escape the caste system! lol lol

No chance. Boom time will make the DGMs blood boil come 12 months time.

I'd love you to stand up in front of a room full of struggling FHB'S or people paying the stupid rents being charged currently... it would be BOOM time, but not the way you think.

Veiled threats of physical violence get upvoted? Stay classy interest.co.nz common-taters.

I meant with displeasure and verbal uproar. Your comment says more about you and your assumptions dude.

Sure ya did

Reminder you do have to live in the society you create, though.

Oh Lord - another one........

Just received a 0.25 > 4.75 increase on the Macquarie transaction account with depositor protection. Though someone has to take that NZD off you.

Am a saver. Different wish list from borrowers.

Why do you hate New Zealand?

That's a mysterious comment Squishy. ? Could you elaborate.

Let's start with bank economists at Australian banks, and then move onto the foolishness and shortsightedness of NZ's voters and the purple parties and their ignorance (real or by pretense) as to why NZ's tax system needs a massive overhaul.

(Should keep us busy all weekend ...)

Swap rates and term deposit rates both have an influence on the mortgage interest rates offered. Customer deposits (which include much more than household term deposits) are the main funding source for home loans, and the wholesale markets also have a strong influence, especially in their role to hedge the 'borrow short, lend long' risks that banks face.

The interpolated mid IR swap rate, for last Thursday's 2.0% 15/05/32 government tender yielding 4.9681%, was - minus 14.35 bps at 4.8246%.

Quite simply, it takes some financial institution’s balance sheet capacity to take on an interest rate swap (the farther the maturity, the more capacity it requires). If balance sheet capacity (the real money in the system, therefore liquidity) is systemically impaired, as in a crisis, or a crisis that doesn’t really end, then to get dealers to give up their precious balance sheet capacity and engage on the other side of a swap someone would have to pay a hefty premium to make it worth it (risk-adjusted) for the dealer to do so. J Snider

Customer deposits (which include much more than household term deposits) are the main funding source for home loans

Or...

Loans are the main source of customer deposits?

Bank money creation hard at work. After all, one person's approved and issued bank mortgage is another person's receipted funds allowing settlement of the sale and purchase agreement - funds which go straight into an interest earning bank account more often than not.

Rates currently appear to be set at the right level to slow inflation. That said I think there will be a lot more restraint exercised in using quantitative easing in future and fiscal stimulus is right off the table.

I agree with the first half,

The second half I completely disagree with, I think we'll see this all happen again within the next 20 years (maybe more than once)

Indeed office. It's what politicians do.

If by "fiscal stimulus" one includes the OCR back below 2.0% then I'm pretty sure it'll happen much sooner. Technically, what the RBNZ does isn't "fiscal" though.

And if you're taking true fiscal stimulus, where governments adjust spending and/or tax settings, I'm sorry to say you'll be wrong by early next year. (I refer of course to the NACT tax cuts.)

Further, are you suggesting that they'll never be an event, in the next 20 years (remember we live on a fault line) that will require it? Huge call.

If you're saying that there won't be another event that requires the scale of quantitative easing and/or fiscal stimulus we saw as a response to an event like covid, you may be right. ... Methinks all central banks consult the text books that refer to the RBNZ's actions that threw money into a massively supply constrained economy and they'll conclude that it'd be pretty dumb.

Still, other events, GFC 2.0?, could warrant it. Likewise a collapse of the internet. Or an alien invasion ;-)

So the Taylor Rule proved wrong again, ay? Who'd have thought? (LOL)

Yes ANZ made a good early call on this big shift in swaps last week. If these swap rates do hold lower over the next month or so then the 3 to 5 year TDs could be the first to move down. Short term at the 1 year, it all comes back to the RBNZ. I think they will be very reluctant to move the OCR until at least March next year knowing well New Zealanders addiction to the property market and wealth effect spending.

I think the RBNZ will be watching the coalition discussions closely, too. If GST were increased to redress the potential cancellation of the foreign buyers tax, then that would obviously create some inflationary pressure.

Is there a suggestion that they will raise GST? That would be a nail in the coffin for the construction sector. Without new build exemptions GST is one hell of a cost.

Markets were pricing in falls way before a week ago. More like a month ago ... and 3-6 months ago if one were reading the right tealeaves.

Which markets were pricing in the falls?? Not the swaps or banks.

Dan Brunskill did a great article on what the market was predicting ... Published 2nd Nov 23.

https://www.interest.co.nz/bonds/125053/market-expectations-official-ca…

The graph at the end of the article can be created at any point of time.

re ... "I think they will be very reluctant to move the OCR until at least March next year knowing well New Zealanders addiction to the property market and wealth effect spending."

Maybe. Maybe not.

Don't forget that the RBNZ focus is on financial stability and controlling inflation. Thus they only move when either, or both, are threatened. If neither are, the OCR can come down as it costs NZ Inc a fortune to hold it high. Further, DTIs are on the cards to be implemented, if Prince John allows it that is. And a DTI will have a restraining effect (at the right level).

I'd agree March is probably the earliest we'll see an OCR cut. (Jfoe is picking May and I think he's most likely to be right.) A small cut before then is a remote possibility (but IMO a small cut earlier, possibly followed by another, is an absolute necessity). By March the info for a woeful Christmas will be stark. Alas, a small cut then will be too late and a larger cut will, as you say, send exactly the wrong message.

Interestingly, a UBS economists is predicting a whole 1% cut in the last four months of 2024, from 5.5% to 4.5%. That would be a signal that the RBNZ has, once again, got it badly wrong.

I think a 0.5 cut at Feb is more than reasonable to believe would happen, the fire is too hot, they need to slow it down.

How about 0.25% November, and than another 0.25% in Feb, and then a long pause to let the spuikers exhaust themselves, and then some further presents before Christmas? ;-)

My guess is RBNZ are going to use DTI, LTV etc to try and steady the housing market (a key driver of our financial instability), while dropping rates to ease pressure on households and businesses. Two tools for two different jobs is an improvement.

Could well do.

Alas for the RBNZ though ... If the LVR and/or DTI are set at levels to be effective, FHBs will be screaming "Unfair!". (Dare I say it again? I will. Tax system changes would work far better and would be far fairer.)

Yes if they had had a DTI of 5 in place in 2017 we would not be in this mess now, and other non-housing loan borrowers having to pay so much.

RBNZ are going to use DTI, LTV etc to try and steady the housing market

The main catch is to reduce the leverage of investors, ie. How they use their unrealized valuation of existing properties (equity??) and using it as deposit for next purchase

Need better restrictions to stop this ponzi. If they have enough bank deposit, let them go and buy more, no problem.

Agree Greg, if these people want to buy more family homes to turn into rentals let them pay cash rather than leveraging.

And that's exactly what the wealthy will do - and enough to maintain price. Noone else will be able to afford to buy - the rich get richer. DTI will not have the desired effect.

Rates are set at the right level to slow consumer demand, increase unemployment, and basically stop house building. However, the slowing of inflation can be completely credited to lower import prices.

Hahaha. Yeah wage pressure to keep staff and servicing stupid house prices are the two greatest engines of inflation.

The system is now so unstable , the smallest of inputs can set it off in most unexpected ways.

Making predictions in this environment is truely heroic. The sane thing now is to manage the risk that swap rates may have another leg up.

But housing always wins. Because they hv new FHBs and wanting to be FHBs as the front lines to take the hit first and make news :-(

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.