As the biggest bank in the country, ANZ New Zealand doesn't have to offer the best deposit rates so it doesn't, the CEO of the bank's Australian parent says.

ANZ Banking Group CEO Shayne Elliott made these comments in an analysts' briefing after the Group posted its annual financial results on Thursday.

Elliott noted that deposit rates in NZ have risen to a level where they're now sufficiently attractive to change customer behaviour, with a shift towards "term" and away from "at call." In a rising interest rate environment he added that this is something you would expect to see.

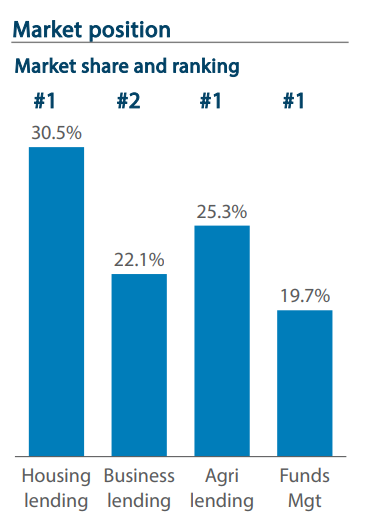

Elliott went on to say ANZ has a "really strong franchise" in NZ as the number one bank with a great customer base.

"We don't have to be the very sharpest on [deposit] pricing and so we're not. We're not leading on pricing, we've been fair and [are] paying in the market. But we don't have to lead," Elliott said.

"And what we're seeing is we are seeing others, some of the competitors, really driving price competition. I would imagine that reflects the liquidity balance within their books."

The ANZ Group results noted the September year net interest margin at its NZ unit rose 14 basis points to 2.47%.

Speaking to interest.co.nz after ANZ NZ posted a 20% rise in annual profit to almost $2.3 billion, ANZ NZ CEO Antonia Watson said "offsets to margin improvements" were "only just starting to manifest" as economic conditions toughen.

"So, for example, we're starting to see people move much more into term deposits and there's a cost to that for us," Watson said.

ANZ NZ's currently advertising a 3.60% interest rate for a six-month term deposit with a deposit of at least $10,000. ANZ's main rivals, ASB, BNZ and Westpac, are all offering 3.75% with lower minimum deposits required. Other banks are also offering more than ANZ NZ. The market leading rate is 4.20% from both Bank of China and China Construction Bank, but that requires a minimum deposit of $100,000.

For a one-year term deposit, ANZ NZ's offering 4.30% for a minimum $10,000 deposit. ASB, BNZ and Westpac all offer 4.50%. The market leading offer is 5% from SBS Bank.

Over its September financial year, ANZ NZ grew customer deposits by $5.621 billion, or 5%, to $107.967 billion. However during the second-half of that year they rose just $247 million.

See all banks carded, or advertised, deposit rates for terms of one to nine months here.

And see all banks advertised, or carded, term deposit rates for terms of one to five years here.

*The table below, from the ANZ Group, is for ANZ NZ.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

65 Comments

Well at least the rates are trending in only one direction....Up. Still on track for 5% rates for the 1 year in early 2023. He is correct with other investments tanking, TD's will be back as an option.

Does anyone here know, when deposit guarantees come in early 2024, will they cover existing TDs, or only new deposits after that date??

The politics of a monopoly.

And another: Exxon Reports Record, Blowout Earnings; Stock Soars To All-Time High

Putin explains Western economic model

The West seeks to capture local markets and resources to maintain global dominance, the Russian president says

I've really got to move accounts from ANZ

Arrogant sob Certainly convinced me. Got a TD to set up up this month and even if they are better they won't be getting it.

Yes openly arrogant, ANZ had the best deposit rates of the big 4 over the last 10 years but this is a change. They will lose customers over this, and I see TSB and the like will get the growth they are looking for. Kiwibank and BNZ also paying under the odds, ASB and Westpac now the best of the big 4. I have some funds at ANZ, am very happy with their service and electronic banking, but wont be renewing with ANZ with this uncompetitive change.

Transfer done, see ya later ANZ

My thoughts exactly. I move TDs upon expiration to the bank with the best rate - gone are the days when customers remain loyal to their banks. I'll make a point to take ANZ off my list.

ANZ doesn't offer the best deposit rates so I don't deposit. Works both ways.

maybe they believe in,treating them mean,keeps them keen as a business model and so far seems to be working pretty well.their TD rates are paltry compared to rabo

They just monitor the competition & set their own rates to no more than what they can get away with. They rely too on their customer inertia to a degree as well, as some can’t and/or don’t shop around. With the money laundering criteria etc it’s not as easy as it used to be to set yourself up with an alternative bank.

Agreed, the AML requirements inhibit retail banking competition.

Sure do. Try and set up a TD for a Trust with a new bank and you'll be jumping through more hoops than a circus acrobat!

I use Investnow for TDs for this exact reason.

6 Banks to choose from, all from one location.

ANZ, BNZ, Bank of China, China Construction Bank, Heartland Bank and SBS.

It's usually better rates as well. For example ANZ 1yr 4.55% v their carded rate of 4.30%

Who is ultimately responsible for your TD safekeeping ?

I guess this is consistent with the mantra of returning maximum value to their shareholders and their strategy of gaining market dominance allows them to extract maximum value. To hell with their depositers. It is up to the depositers now to remove their funds if they care to do so.

“To hell with their depositors.” Aye, that’s the rub isn’t it. However you look at it, it is a statement reeking of arrogance going on dismissiveness. An unwelcome message to any loyal everyday retail customer.

There is no such thing as loyalty to a bank. That went by the board at least 30-40 years ago. If u want loyalty buy a dog.

I guess this is the mantra these days.

There is a certain benefit to familiarity and issues around the hassle of migrating your business elsewhere though. Devil you know, that sort of thing.

End of the day we've made a society just about numbers and short term results, so everything and everyone is pretty disposable.

let them eat cake...........

Interesting comments on the money laundering ... WOW... didnt see that coming... 'inhibit' ,not as easy as it used to be....WOW . Makes me wonder if the banks are actually doing their forensics correctly ... those comments lead me to believe we have systemic problems still.... changing banks shouldnt be a problem , it should be something folk are able to do with ease...

I had to get 'verified' this week by one of my banks. Been dealing with them for 20 years or so, used to have a bank manager and knew that person for quite some time. But it was like I was a new account and arrival on planet earth.

Ended up going in circles and they do seem to put in quite the effort to validate you, ultimately I had to go see someone in person, ID, address verification, what's the nature of your accounts and transactions, etc etc.

Should only require a "real me" kind of username and password and then you're done. But no, lots of paper work and certified copies of stuff etc. Too hard for people to hunt around for best TD on offer.

Correct me if I'm wrong, but a lot of that $2.3 billion would stay in NZ if people switched to Kiwibank?

It s a great pity the Bolger government did not see fit to bail out the BNZ. Ok there were skeletons in the closet that needed to stay put, but in my book, it would have been of far greater worth than the subsequent bailing out of Air NZ.

Or those community trusts selling Trustbank, or the CcomCom permitting Westpac to buy it, or ANZ to buy National Bank, the list goes on.

Yes but Kiwibank deposit rates are about the worst right now, so much for the peoples kiwi bank.

Try their notice saver accounts

Sadly kiwibank has moved to aorteroa. Just closed off our airpoints card with them as air nz moved there too.

It's weird how the use of 'Aotearoa' is a big deal to some people

How would you feel if some stranger forced you to change your own name, possibly into a name in another language, without your agreement and contrary to your desires.

We have 2 official languages, not 1.

Maori and brail

No, NZ sign language and Maori. English is a defacto official language even if it is not codified in the legislation anywhere. (the fact that all the legislation declaring what the official languages are is recorded in English is a bit.. Ironic)

Pretty bad I reckon.

That's not what's happening here though huh?

As Aotearoa means the NI, it's not very inclusive.

There is no such place

Election winner for next year.. State guaranteed mortgages for residents through Kiwibank - 3.5% fixed for 25-years for owner occupiers (<$1m, Max 80% LTV) - bundle in home insurance too. Bank profits are now $1,750 per adult per year in NZ (>2% of GDP) - it's a disgrace.

I will vote for you

Likewise - JFoe for Prime Minister!

How much will it cost to get off the ground and how are you funding it?

If the banks go to war with you, how deep are the pockets to wage it?

- It is zero cost. You create an asset on the Crown balance sheet with every loan you make. You just need to find a willing commercial partner to handle the retail end - like a state owned bank may be?

The biggest risk would not be banks going to war with the Crown (that would be next level dumb), it would be the chaotic withdrawal of Aussie banks from NZ, some instability in bond markets, and share price drops for companies that profit from the current rort.

If you're guaranteeing interest rates and financing insurance, you need to pay for it some how. Effectively it sounds like you're wanting to bankroll a perpetually loss making bank and insurance company.

Will the foreign banks leave town or just match or better at say 3% for 5-10 years and kill the project before it gets off the ground?

Sounds an attractive idea on the surface but it's nice to flesh out the realities.

Fair challenges. I would fix the long-term state mortgage at OCR + 50pts, making it impossible for the banks to compete (at least initially), and offer the same loan facility to low-risk investments with high social value (e.g. building housing for affordable rent, new hydro and wind etc). The intent here is to make critical, socially-beneficial, low-risk credit a state service - not something that can be rorted for profit by aussie finance companies.

In terms of financing, just do it like we did in the 1940s - Govt deposits newly created money into the borrower's account, and takes a loan agreement onto the balance sheet as an asset. Exactly the same operationally as the current student loans approach actually.

The insurance part is more interesting. Large housing associations in the UK (with thousands of homes) don't insure their homes any more because it is far more cost effective to use their revenue budgets for rebuilds and repairs. So, Govt would take in 'insurance premiums' like they do any other revenue - knowing that they will always be able to pay for repairs and rebuilds (and would end up doing so if there was a truly catastrophic disaster, which would wipe out the insurance companies).

White collar crime

3.5% could end up looking very expensive over 25 years!

Refinance breakpoints every 12 months (with 3 months notice). Fixed rate being OCR + 50 pts.

How is OCR + 50pts a fixed rate? That would make it a variable rate, which means it could still get very high (higher than taking a longer term fixed now perhaps). The bank would still need to make a margin to cover overheads, capital costs etc, otherwise that's just my tax dollars going down another drain.

ya.... dont make best deposit rate.. .... increase mortgage interest rate...

and go for a salary hike for all in anz......enjoy luxury and push half the population to poverty.

The “ yes” bank . Remember ?

Arrogance and stupidity don’t go well together

They're usually pretty good mates though.

True. Sadly, arrogance & ignorance are common bedfellows and greed lies in between.

No appreciation on cash reserves anyway.. buy a building. Get high 4s and more soon... and get capital gains.

Really should be able to depreciate cash reserves...it is an asset, isn't it? It is subject to depreciation based on bad monetary policy and QE.

Even if you got 4 at bank your still losing 3.2 every year depending on what you buy.

currently , No capital gains and going down 10% is even worse at millions of dollars

This is where TD's come in

You only losing if you spending it at current inflation rate/

Well I hope everyone shifts their deposits. Personally, I've gone to buying bonds simply because if I have to I can liquidate if I need the money, whereas banks simply don't allow you to break term deposits. (And holding bonds is better than bond funds because worse case scenario on a bond is hold to maturity and get your coupon rate back, whereas in this environment bond funds have been a disaster with no bottom.

But another reason the banks can do this is Orr's ludicrous Covid/QE 'relic' policy of still funding banks at OCR rate for them to lend out to commercial, giving them premium margins there.

Someone needs to ask Orr what is the reasoning for the continuing QT which we now know is simply deepening recession, the job layoffs start soon, while giving this great cushy QE deal to the banks, still, to make super profits again at their depositors expense.

It's fraudulent frankly.

The more you understand the finance/monetary system the more fraudulent you realise it is. Lucky the average person on the street has no idea.

But it becomes more and more visible the closer to the end of the long debt cycle you get. As bad debt/risk continues to get bailed out by the tax payer.

Just watch out - yes bonds are more liquid than term deposits, but bonds may be subject to potentially significant price fluctuations depending on interest rates movements (if you buy a bond and then interest rates go higher than expected by the markets at the time of the purchase, the price of your bond will decline). Having said that, buying bonds now might not be too bad, as markets are already pricing in significant interest rate increases in the future. But, if you think (like I do) that there are still significant upside risks to interest rates in the future (not fully reflected by current swaps), you might want to be a bit careful.

Yes I know all that ... but end of the day, unlike in a bond fund, if you hold your bond to maturity you get the coupon rate back. However, sometimes you do need the cash - say, when you wife finds a house she wants - and at that stage you at least have the option of taking a loss (or profit) and cashing up.

Have banked with the TSB for some 27 years - paid no fees and given a free visa - how good is that.

Interesting, may I ask is this for personal banking or business banking or both?

Also how are they when you need support?

You normally get no fees if you have a mortgage with your bank anyway and most banks dropped charging monthly fees a while back as well. The only place you stand to get stung is by not paying off your credit card every month or even forgetting to pay off the minimum and getting hit with a $25 fee.

TSB spent $136 million in the last year upgrading systems, a good move as people move to do everything online. I read here recently about 86% of their loans are NZ property, a real mortgage bank by the looks. Good luck to them, they seem to always be at or near the top of the Canstar awards.

my bank does that that too on Mastercard

As a shareholder I'm happy to see the bank finally giving the lemon a good squeeze. Customers had it too goo for too long, it's time for some chunky bottom line growth.

1611, King James Version of the Bible, Book of Proverbs, 16:18, Pride goeth before destruction, and a haughty spirit before a fall - add my name to the list of those removing deposits from ANZ. Already moved a small part and when the rest mature you won't see my funds return. Oh and for those sticking around for the meagre increase to call account interest rates that take affect from 1st November you should have moved right after the RBNZ's last shift to a more responsive bank by now

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.