By Roger J Kerr

How does the shock Brexit result change one’s forecast/outlook for global and NZ interest rates?

The first answer is that it is still too early to form a view on how long the global market uncertainty and turmoil will last as a result of the UK’s exit from Europe. Some say the next 12 months will be volatile and disrupted, my view is that it may all settle down after two to three months.

Naturally, the initial reaction is a flight of global capital to safe-havens i.e. US Treasury Bonds, gold, the Yen and the US dollar – which have all increased in value since Friday.

Other economic and market developments to consider are:-

- UK and European central banks are ready pump in liquidity and reduce interest rates further.

- Banking stocks in the UK and Europe were hit hard on Friday, thus there is expectations that credit spreads in fixed interest bank securities will move higher i.e. increasing borrowing margins for Australasian banks issuing in global markets.

- The UK economy may well move into recession as confidence and investment are eroded by the sheer political and economic uncertainty vacuum they now find themselves in. However, my view is that the Brexit does not disrupt Chinese, US and Australian economic growth too much as it is not going to change the drivers of those economies. The NZ economy is reliant on the aforementioned economies, to a much lesser degree the UK and European economies. The Greek economic/debt crisis in recent years was blown up by the local media here as a major event and risk for the NZ economy. My view was always that it had virtually no impact on us and that proved to be the case. It is far too easy to exaggerate such events and market shocks a long way from us as material for our economy, and they simply are not.

- Janet Yellen at the US Federal Reserve was prepared for such an outcome and has held off from increasing US interest rates for the meantime. The question is whether after two or three months of good US economic/jobs data she concludes that the Fed still has to stick to their plan to return monetary policy settings to “normal”. The US interest rate markets are now pricing no Fed Funds rate increases over the next 12 months. US long term interest rates cannot move higher unless their short-term interest rates are increasing.

- The local moneymarket has now priced the probability of a RBNZ 0.25% cut in the OCR on 11 August at greater than 75%. There is now additional pressure on the RBNZ to drive the currency Trade Weighted Index (TWI) lower from its current elevated 76 level. The TWI is higher due to the sharply weaker GBP and EUR on the cross-rates to the NZD. Only a lower NZD/USD rate for separate and independent NZ reasons can get the TWI back to 70 to be consistent with the RBNZ’s own economic and inflation forecasts. Another fall in wholemilk powder prices at the next GDT auction on Wednesday 6 July would add to that pressure on the RBNZ.

In their last statement the RBNZ stated that undue volatility in the non-tradable inflation rate would be caused by further easing of monetary policy with an OCR cut.

They used this PTA exception clause to justify being continually in breach of the 1% to 3% limits for the last 18 and next 12 months.

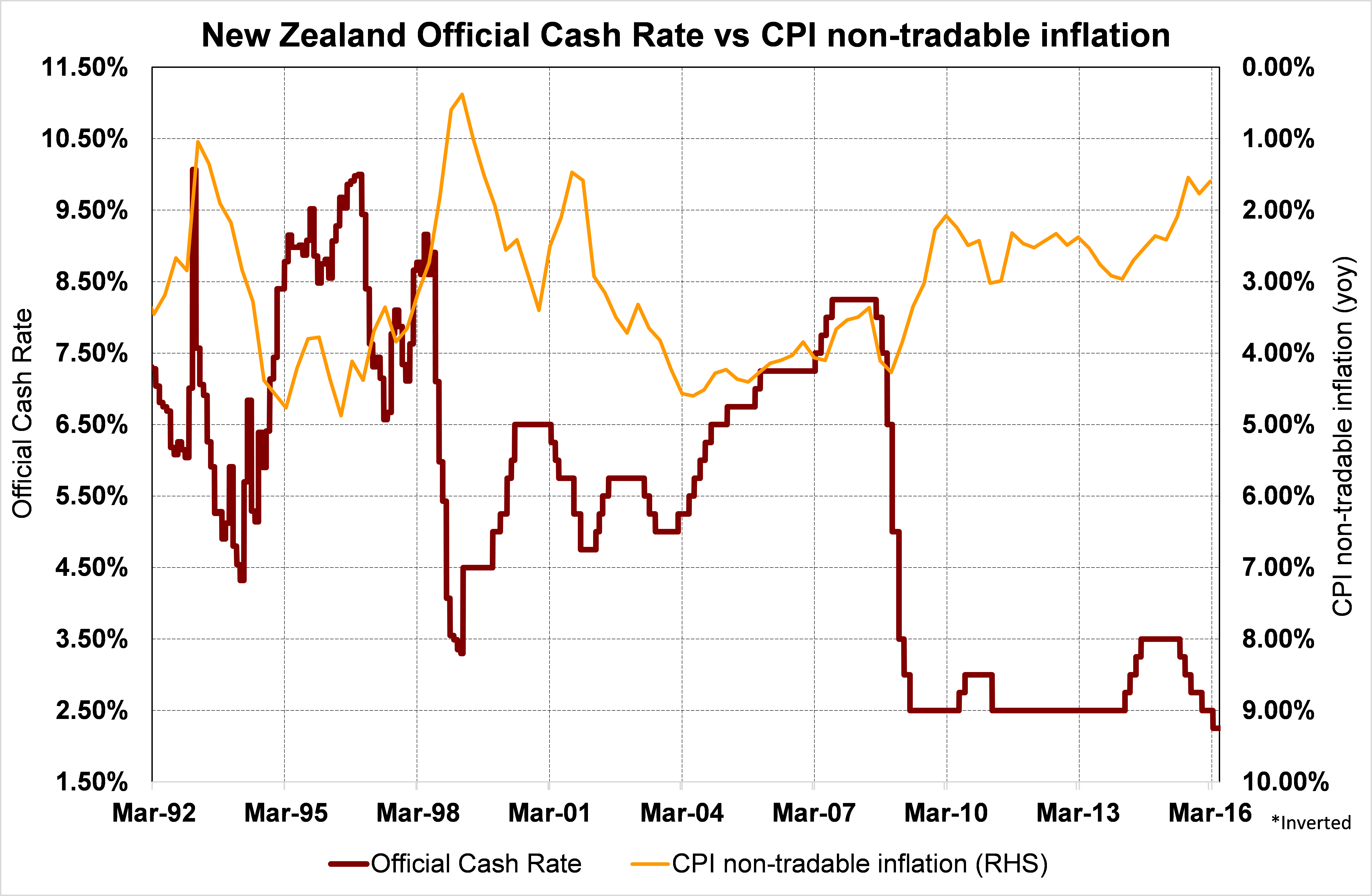

Unfortunately, the rationale for the RBNZ’s case that lower interest rates at this time would immediately drive non-tradable inflation (domestic economy prices) higher is not a strong one judging by the chart below.

There is no cause and affect correlation at all.

Like many other economic indicators any marginal correlation that may have existed has completely broken down since the GFC in 2009. Non tradable inflation in New Zealand is always supply side generated, not demand pushed as the RBNZ seem to think.

Daily swap rates

Select chart tabs

Roger J Kerr is a partner at PwC. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.