The Government isn’t planning to bail out Tower’s troublesome earthquake business, which the New Zealand insurer wants to ring-fence from the rest of its operations.

Tower last Tuesday announced its intentions to create a new entity, RunOff Co, to deal with its 564 outstanding 2010/11 Canterbury earthquake claims, the legal battles connected to around 100 of these, and its disputes with the Earthquake Commission (EQC) and one of its reinsurers to secure $100 million of quake recoveries.

Chairman Michael Stiassny said Tower was “evaluating a number of potential sources of capital - including strategic sources” for the split.

All this begs the question as to whether taxpayers could end up on the hook for Tower as they have for AMI.

Finance Minister Bill English says: “Tower has not sought any assistance from the Government and it has not asked the Government to buy the run off company it is proposing to establish.”

Asked by interest.co.nz whether the Government would consider a bailout if the alternative was Tower going under and not settling all the claims on its books, English says he doesn’t have any comment to make as the question is “hypothetical”.

The Government bailed out AMI in 2011. Its non quake-related business was sold to IAG, while the Crown-owned company, Southern Response, was formed to mop up the mess from the quakes.

In 2012, Treasury's "best estimate of the likely cost of the AMI support package over its life" was only $98 million. Southern Response’s bill to taxpayers now heads towards $1.25 billion, as another $250 million was set aside for it earlier this year.

Tower expected to sell RunOff Co and ensure New Tower isn’t held responsible for it

If a government bailout isn’t on the cards at this stage, the question is where will Tower get the capital to settle its outstanding claims and satisfy the Reserve Bank’s (RBNZ) capital requirements? What “strategic sources” is it looking to?

Forsyth Barr analyst, James Bascand, believes Tower will sell RunOff Co. He can't say who would buy it, but has his bets on a large reinsurer.

While additional capital would be needed, the buyer would get $39 million of capital from Tower. It would also hope to secure the $100 million of quake recoveries in dispute (explained below).

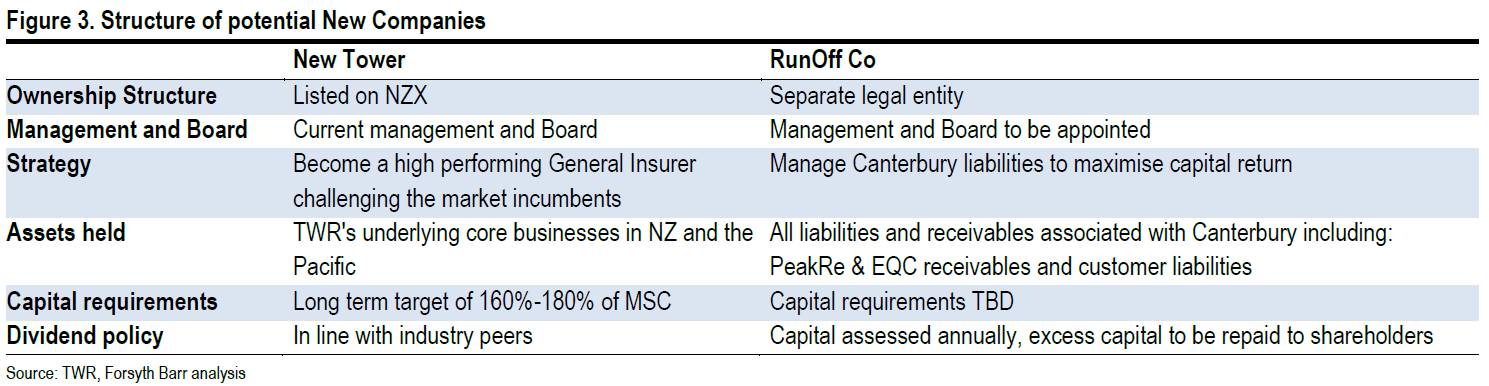

Bascand also maintains Tower's board is planning to “Devise a new structure under RBNZ guidance that creates a no-recourse relationship between RunOff Co and New Tower. This could include a de-listing of RunOff Co.”

He essentially says RunOff Co can’t be guaranteed against Tower’s regular business as shareholders won’t want to invest in New Tower if there’s a risk their returns will be dampened by their funds being used to prop up RunOff Co, especially if the company has to keep increasing its quake provisions as it has up until now.

“For the market to have faith in reassessing the value of Tower’s pure general insurance business without having to account for future Canterbury earthquake liabilities, we believe Tower needs to ensure any split is on a no-recourse basis…” Bascand says.

“Should shareholder capital still be liable for further capital erosion under a split model then we cannot see the merit of the ‘split business solution’.”

Forsyth Barr suggests Tower’s new structure could look like this:

Tower has confirmed its intention for RunOff Co to have a different management team to New Tower.

$39 million available to put into RunOff Co

So what will Tower’s capital requirements be initially?

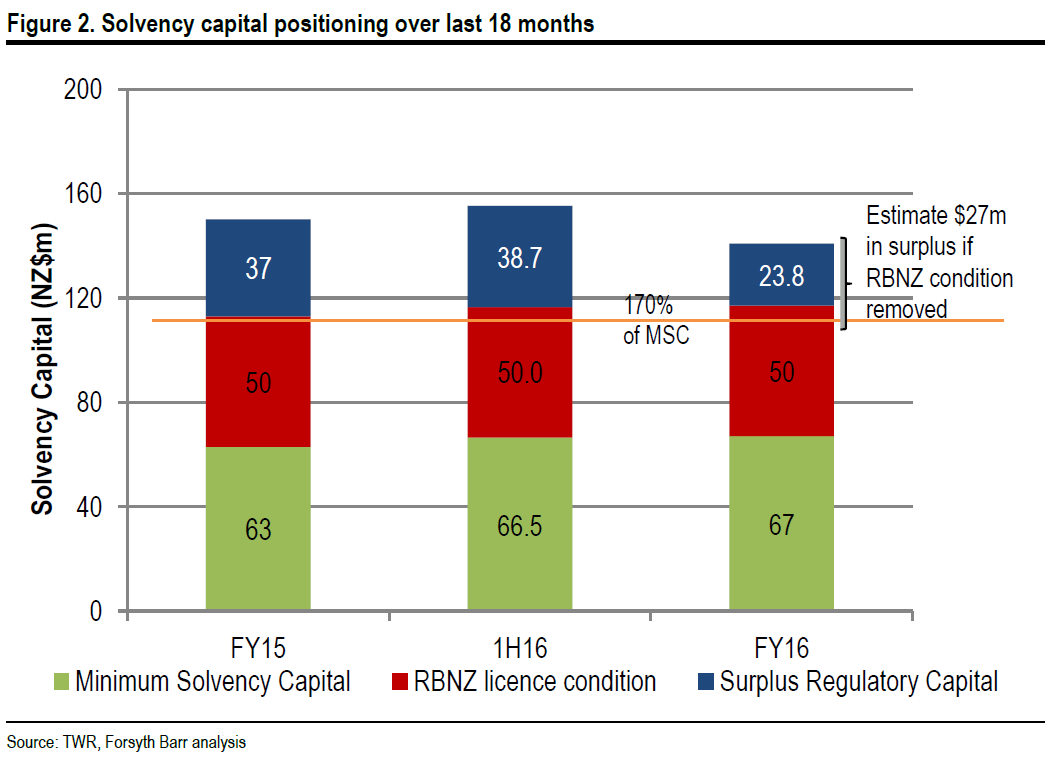

Bascand explains: “The $50 million earthquake related capital buffer that is currently required by the RBNZ is likely to be removed on a split in businesses.

“However, management has suggested that only a small part of Tower’s solvency capital is currently related to Canterbury earthquake provisions, and given the company’s internal target of holding 160%-180% of MSC [minimum solvency capital] there is only $27 million in capital above the mid-point of that range that could be attributed to RunOff Co.

“Management also has $12m cash at head-office level, so a maximum of $39 million could be put into RunOff Co.

“Management has implied that additional capital will be required to split the businesses. No range has been provided as to the potential sum required and the company is still in discussions with the RBNZ as to what the requirements may be.”

$100 million of recoveries up in the air

Thereafter, Tower expects to receive $43.7 million from Peak Re and $57.6 million from EQC. It has already accounted for these receivables in its balance sheet.

Bascand explains: “Tower is currently in arbitration with PeakRe for the reinsurance it is owed, and remains exceedingly confident of receiving the cash within the next 12-18 months.

“The view is that PeakRe is attempting to hold out as long as possible to force Tower into settling for a smaller cash sum.

“Tower has indicated it will be pursuing the full amount regardless and expects to recover full costs including interest as a function of the legal case.

“Recoveries from the EQC are expected to take longer with sporadic cashflows over 2-3 years targeted and the potential for a full legal challenge to be mounted.”

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

15 Comments

So RunOff Co will run off with a claims book worth vastly more than the capital for the company and of that the Peak-re & EQC components are contingent assets at the very best. What happens when RunOff has no money left to meet claims?As the article says there is no point in Tower making this split if RunOff will remain as a drag or weeping wound on shareholders funds. Therefore this surely is a move designed to completely relieve Tower of the financial liability of its outstanding EQ claims. Where does that leave the claimants? Running flat out to their lawyers one imagines to file against Tower before all this happens. [ Comparison with a completely different issue, in a completely different industry, is a smear, so removed. Ed ] If Tower can get this past the Reserve Bank, Treasury, Securities Commission, Commerce Commission, NZX then there is something surely rotten in the state of Wellington.

The price paid for runoff co that Tower received, would reflect the claims liability escalation risk the buyer perceived runoff co to have i.e. it is likely to be depressed due to ongoing uncertainty. Shareholders would receive a one off equity haircut but their future risk from Canterbury would have been eliminated.

If the buyer is a large deep pocket reinsurer, claimants would have no fears of runoff co running out of money.

On the basis of that, and given that Tower apparently has no idea of what their ultimate financial exposure for outstanding EQ claims amounts to, Tower has nothing to sell. Rather, it would seem, they would have to pay someone to buy it.

Yet....

Tower is the most appalling insurer and this move is clearly intended to escape its full liabilities, [ over the top, extreme association is just not called for, so is deleted. Keep it reasonable please. Ed ] I am nor have been a Tower policy holder but know many who still battle with this odious company and their equally odious Lawyers, [ no need for the type of epithet used, so removed. Ed ]

They cannot 'escape their liabilities'. One way or another Tower shareholders will bear the cost of inadequate claim reserving or surprise cost escalation. Unless of course they can't find a buyer for runoff co - you'd then have to be concerned a bailout was one possibility. Govt would then probably look to grab some of Towers equity but not to the point they'd want the only remaining independent insurer of any size to fall over, assuming a big bad Aussie insurer is not already running the measuring tape over them. If a bailout happened you'd think they would deliver runoffco's remaining claims to Southern Response's tender care.

Tower do not care about their shareholders anymore than they care about their claimants. Even if it may be that the former includes the like of ACC & NZ Super. What they care about, the executive that is, is their jobs and income. Tower claim 96% of EQ claims are done and dusted. This is therefore an extraordinary venture to contain the balance, after all this time how is it that financial liability for these remaining cannot be accurately quantified. Perhaps it can. Perhaps that's the problem. Agree totally with the analysis in this article that this is a measure designed to seperate Tower from this liability. Why else bother for 4% of claims? So it seems that one way or another Tower, misguidedly hopefully , definitely see this as a way to escape their liabilities!

We are told that claim cost escalation for the remaining 5% is mainly caused by people seeking a windfall and new claims from EQC.

Other explanations are possible including 'catch up' to address previous under reporting of losses arising from poor information, failure of assessment processes or cost increases due to a higher level than already factored in, of inflation in building costs.

A conspiracy theorist might also question whether insurers reported honestly at each of the various stages on what they knew their actual claim estimates to be.

i've seen claims escalate and it truly seems unbelievable but the numbers just get bigger and bigger as various experts pontificate on the issues creating tension in the settlement.

Have some sympathy for the insurance companies. The earthquakes were over five years ago and the claims from EQC just keep dribbling in. However, they were foolish to offer the total replacement/peace of mind thing as it was just asking for trouble. Have just opened my latest premium notice and there is yet another nasty shock. Still their parlous financial position tells me they are not gouging, it was just they had been underpricing the risks (to our benefit) for years.

I believe there are some that still do offer full replacement. Also I think that prior to these recent EQs, one or two more started offering it. I don' think total replacement is a bad idea,but maybe they weren't charging enough for it. But the fact is that with agreed value, it puts more risk on the owner, and they have to keep it upto date, and many people will now be very under insured, which is a major problem after an earthquake. Potentially it could mean ghost towns if large numbers don't get enough money to rebuild.People who previously had freehold homes, will likely need to get big loans. But it will be great for banks.

We recently got one of those estimates from our insurer for a full replacement policy when we came up for renewal. Given the premium was ridiculous (the revaluation being way above what we could sell the property for in the market), we decided to go for an agreed value that was way less than what they claimed it would cost to rebuild our existing dwelling. We wanted to rebuild much smaller. It took some convincing our insurer - they still wanted an independent valuation of our existing home. We re-emphasised that we didn't want to rebuild our existing home in the event of being a total write off. After more to and fro and being put on hold while the sales person consulted their internal valuer - they came back, offered us our previous sum insured under the old regime (roughly the current market value for the place), for a slightly lower premium.. Go figure.

yes exactly, one cant reserve for a liability one doesnt even know one has. Oh Hi Mr EQC , you've just dropped another million dollar claim on me, and you'll pay the first hundred thou, oh cheers Mr EQC.

You can't blame Tower for pulling the same stunt as AMI and the Aussie predators (runoff may yet end up on the public's hands). It's all about precedent. If the Crown is to step in in such circumstances, it should only do so if it takes 100% and expunges ALL other equity.

a runoff can be a wise buy for a farmer but I dont think anybody will buy into this one.sidestepping their obligation to fulfil their part of the contract between insurer and insured.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.