Today's Top 10 is a guest post from Matt Nolan.

Economists have a reputation for being two-handed and refusing to “take a position”. Although this is often used as a stick to beat us, I see it as a good thing – and thought I should start the year being as two-handed as possible.

As a result, this week’s Top 10 is in fact two top fives – one list saying why the New Zealand economy is going to tank, and another list saying why it is going to reach new heights during 2015.

As always, we welcome your additions in the comment stream below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

Top 5 reasons to be bearish about the outlook for New Zealand for the next year

1. Oil prices

First up in the bad omens for the New Zealand economy is oil prices.

As a net oil importer (importing $7.6 bln of petroleum products and crude oil in the November 2014 year, while exporting $1.6 bln) New Zealand would be expected to do quite well from lower oil prices, but this involves ignoring why prices have fallen.

The rout in oil prices began when OPEC lowered its forecast for oil demand in the 2015, and then refused to commit to any cut to supply. With stockpiles already growing since the middle of 2014, and the demand for oil notoriously unresponsive to changes in the price of oil (in the short term) this led to a sharp decline in oil prices.

Lower global demand for oil over a short period of time implies that global economic activity is likely to be lower – and the chance of financial market repercussions in oil exporting countries is significant. New Zealand is a small open economy, and so is easily pushed around by the ebbs and flows of the global economy. Softer global growth will lower export returns, make credit harder to come by, and reduce confidence in the New Zealand economy – all factors that point to lower economic growth.

2. Export prices and competition from the Aussies

And the decline in the price of some of New Zealand’s key export commodities heading into 2015 has been pretty spectacular.

Even after the slight rebound in dairy prices over the past month, according to Fonterra’s Global Dairy Trade platform the price of auctioned dairy products in late January was down 46% from a year earlier, and has fallen 50% from its recent April 2013 peak.

This decline in dairy prices can also be seen in the ANZ commodity price index, with prices in December down 42% (in world price terms) from a year earlier. Combined with a 7.6% drop in forestry prices these declines pushed down overall export commodity prices by 20% between December 2013 and December 2014.

Furthermore, there is an increasing risk that this isn’t just a temporary decline – with growing competition on the dairy side.

Australian farmers have become significantly more competitive over the past year – with a number of free-trade agreements (especially the one with China) and a falling Australian dollar both factors giving them a boost.

European dairy farmers will soon see maximum production quotas removed, while the ever depreciating Euro makes them more competitive.

Finally, US production has been able to pick up after several years of drought – allowing them to more easily fill their significant domestic demand for dairy products.

Should global production remain elevated, and should growth in demand for dairy cool, New Zealand’s white gold will become no more than run of the mill milk.

3. Proximity to China, and potential Chinese financial crisis

One of the big news stories of the past week has been the slowdown in Chinese economic growth, growth in energy consumption in China hitting a 16 year low, and the concerted push by authorities to rebalance the Chinese economy towards consumption.

China is a major trade partner of New Zealand, accounting for 21% of the value of New Zealand exports in the year to November 2014. However, in recent months the value of exports have fallen sharply – with lower dairy and forestry prices accounting for the entire decline.

There are arguments that the current slowdown in economic growth in China, and shift towards consumption, is necessary to prevent political instability. However, Chinese officials are walking a tight line in trying to balance growth in economic output, financial stability, and political stability.

As part of China’s rebalancing initiative there has been a push to deal with the shadow banking system. However, this is a significant regime shift from what has been occurring – with an IMF blog in September 2014 stating:

At the same time, investors appear to have been largely protected from the inevitable losses that should come with risky lending. It is hard to find a case, for example, of investors in a fixed income trust or wealth management product incurring any losses. This perpetuates the perception that the trust company and/or selling bank, perhaps for reputational reasons, is implicitly guaranteeing the investment. Meanwhile, investors may not appreciate the underlying risk of such products and invest too much of their saving in them.

I haven’t mentioned Europe and the advent of QE by the ECB in this piece (a purposeful oversight) as the key risk stemming from events in Europe is how it impacts upon the trade relationships New Zealand has built up in recent years – especially with China.

The combination of further financial weakness in Europe and fragility in the Chinese financial system leaves a distinct risk of another financial crisis. And even if matters remain contained within China, a domestic financial crisis would lower their demand for Kiwi goods and services – reducing average incomes in New Zealand.

4. Drought?

This time of year it is traditional for newspapers to start writing about a drought in New Zealand. I’m fairly certain that there must be a reminder in ever business journalists’ calendar to start writing about drought in the second full week of January every year.

However, we have had a sunny summer – and this time around there appears to be real cause for concern according to NIWA’s soil moisture deficit information.

Although Canterbury and the Wairarapa are experiencing the driest conditions, it is my home region of the King Country that is experiencing the most significantly “drier than usual” conditions. Unless rain shows up soon, the number of drought stories – stories involving most of the country this time around – are likely to increase significantly. And as we saw in early 2008, a nationwide drought combined with a negative terms of trade shock (rising oil prices then, falling dairy prices now) can have a significant negative impact on the New Zealand economy.

5. Debt and house prices: The RBNZ’s rock and hard place

No list of nightmare scenarios for the New Zealand economy could be complete without including house prices, and the large stock of household debt.

The key risk is, as always, Auckland. No offence to Auckland, you are just such a big place!

As my work colleague Benje Patterson has been at pains to point out, many other regions do not look like they are at risk of a house price correction. However, the disproportionately strong growth in house prices in Auckland has pushed prices to the point where some type of adjustment is necessary – the key question being whether this is a painful adjustment, or a long period of slower house price growth and increasing densification.

In 2015 there is a distinct possibility of the following events occur. A slowdown in net migration from its current high rate, a pick-up in building in Auckland on the back of the Housing Accord and planned activity due to current high prices, and a slowdown in income growth stemming from drought/weak commodity prices. In such a situation a sudden drop in house prices, and an increasing in bad debts for banks (where household gross debt relative to income remains very elevated), could easily occur.

The RBNZ is concerned about such a situation, but they also realise that chasing such financial stability concerns with their monetary policy instrument (interest rates) could be foolhardy – the deflation experienced in Sweden when they attempted such a manoeuvre offers a clear warning. How the Bank handles this challenge is a big, and important, question – I don’t envy their burden at all!

Top 5 reasons to be bullish about the outlook for New Zealand for the next year

6. Oil prices

Headlining our positive links is exactly the same issue that headlined our negative links – oil prices.

While we focused on the idea that it is weaker world demand driving down oil prices in the first set of links, this does not seem to be the whole story. VoxEU has an article where economists estimate the unexpected drop in demand expectations accounted for between 20-35% of the decline in oil prices – leaving a significant unexplained component. Furthermore the drop in “demand” they discuss is not just due to a weaker world economy – but can also be attributed to swifter increases in fuel efficiency and the improving cost effectiveness of non-oil energy generation.

Growth in the supply of oil, improvements in fuel efficiency, and the rise of substitutes for oil are all good things for an energy importer like New Zealand – by reducing the scarcity of energy it is possible for people to have more.

If these supply/scarcity based factors are more significant than any slowdown in global economic activity then it will be a substantial boost for the New Zealand economy in the year ahead – reducing costs for businesses, lowering the price of fuel at the pump, and sustainably boosting consumer spending (if it has the opposite impact to the 2008 shock).

7. Cheap imports and our income boost

Oil isn’t the only import that is looking cheap at present. Wednesday’s Consumer Price Index release by Statistics New Zealand showed that, in December 2014 the price of audio-visual and computing equipment, household textiles and appliances, glassware and tabletops, household tools, and package holidays had all fallen from a year earlier. Furthermore, we can’t “blame” the dollar for these declines – the New Zealand dollar Trade Weighted index was down 0.9% from a year earlier in the December quarter, and the NZ dollar had fallen 5.5% against the US dollar (which is the currency many of these products are initially denominated in).

Fundamentally, imported good prices have bucked expectations (at least my expectations) and just kept getting cheaper.

You may question my logic here, noting that falling prices are driving down inflation below the Reserve Bank’s target - which is often in turn treated as a bad thing.

However, not all reasons for annual growth in the CPI falling below the Bank’s target are created equal. The key concern of the RBNZ is if CPI declines because domestic demand is weak, but when the price of what we trade – specifically what we import – falls this implies that the overall supply of goods and services is greater.

Although we often talk about export prices and New Zealand’s record terms of trade it is important to remember that the terms of trade is essentially the price of exports divided by the price of imports. The cheaper imports are, the more we can buy with the same export income. As a result, falling import prices are a very real income boost for New Zealander’s.

Whether this can be sustained through 2015, as China rebalances, is an open question. But the sharp decline in hard commodity prices has lowered input costs for manufactured goods, implying that if global demand genuinely is weak, import prices could continue to remain favourable for New Zealanders.

8. Proximity to China and growing ‘middle income’ Asia

New Zealand’s growing links with China, and the rest of Asia, do mean that we are vulnerable to a slowdown in these regions. However, they also mean that there is significant scope for mutually beneficial trade over the coming years.

During 2015, and absent the potential financial crisis in China I discussed above, demand from Asia looks set to help New Zealand continue to outperform Australia – and potentially most of the rest of the world.

As mentioned when talking about the risks with China, there is a strong focus within China on rebalancing away from export manufacturing and towards consumption. Australia and New Zealand both export a significant amount to China, but we focus on different products. Australian exports are focused on hard commodities used in export manufacturing, while New Zealand exports consumer goods – predominantly food.

This can be seen by looking at the Reserve Bank of Australia’s commodity price index alongside the ANZ index mentioned above. Between December 2013 and December 2014, the world price of export commodities sold by Australia fell 20% - the same decline as that experienced in New Zealand. However, although New Zealand prices had been booming the year before, Australian prices were already on a downward leg – between December 2012 and December 2014, export commodity prices faced by New Zealand rose 4.2% but dropped a massive 24% for Australia.

The sharp lift in the New Zealand dollar against the Australian dollar is largely a product of this shift – when people discussing “relative growth” or “relative interest rates” much of this difference is the product of the divergent fortunes for commodity returns for the two countries. After two years of falling export prices, and continuing signs that China is rebalancing away from subsidised manufacturing, the Australian terms of trade boom increasingly looks over.

Even with the drop in dairy prices during 2014, the fact that New Zealand sells predominately consumer products to China implies that, at least relative to our big brother across the Tasman, we are well placed.

9. Labour market

One thing that can’t get enough attention is how strong the New Zealand labour market is at the moment.

In September 2014, the unemployment rate fell to 5.4%, the lowest level since March 2009. Furthermore, while many other countries are replacing their unemployed with discouraged workers (who simply leave the labour market) employment rates in New Zealand have risen significantly.

The strong labour market is helping to draw in skilled labour from overseas, leading to fewer people leaving the country, helping to drive increase labour force participation among those over retirement age, and is leading to a significant increase in household incomes.

Having people working, and the confidence and security that employment provides, is a factor that will support economic activity. With the labour market expected to keep recovering, households willingness to borrow and consume is likely to return – boosting economic activity during 2015. Given concerns about debt, house prices, and what will happen to construction work post-rebuild this may not be seen as a necessary plus in later years – but for the 2015 year it is a pillar of growth.

10. A lot more building to go

Although portaloos may be pointing to a peak in the residential rebuilding in Christchurch, there is still a lot to be done.

Not only is residential work in Canterbury unlikely to decline from its current high levels during the next year, non-residential building work is set to pick up further, while demand for new residential buildings climbs across the rest of the country – with high prices and the Auckland Housing According both factors demanding more building in Auckland.

In this way building construction, and the investment that this entails, will continue to buoy economic activity in New Zealand over 2015.

-----------------------------------

* Matt Nolan is an economist at Infometrics, and an author at the blog TVHE. He specialises in looking at the household sector, and household economic data, but will offer an opinion on pretty much anything related to business and the social sciences.

11 Comments

It is better to read these top 10 lists in reverse, from the bottom to the top.

The first thing I note about these two lists are that the bull scenarios are all real events happening right now and likely to continue. The bear scenarios all involve a fair amount of ifs, buts, maybe, could happens.

Low oil prices are a direct benefit to NZ; as a net importer it's more money in our pockets and less going overseas. The Saudi's played the same game in the 1970s/1980s after the oil embargo of the 70s pushed prices too high and helped spawn the nuclear and coal industries. In the 1980s, when prices dropped, they let the price stay low to put pressure on their new competitors. in this decade they'll keep the cost low until the new entrants to the market (green and fracking) are starved out.

I can't help but have the overwhelming feeling that all the hand wringing about deflation is merely driven by those who draw large salaries based on the figures they carefully select, collate and present to show "growth", will no longer be able to do so.

The down stream effects for real people are often lower costs, who would complain? Those who have made their bed in the financial sector and get bitten are parasites anyway so who cares about them.

And what if, just maybe, the high LVR tool was not a bank protection device, but a scarecrow to prevent young entrants to property taking on potentialy unservicable debt and negative equity in the event of impending deflation and possible rate rises? Once again those speculators in that market are parasites and who cares if they take the reality check.

Like the redefinition of employment, In Aus. 1hr per fortnight of work, paid or unpaid, means you are employed and non-permanant residents out of work just dont count at all. Eventually you run to the end of the ability to fudge the numbers to make yourself look good, as police found with the road toll. I suspect economics does not differ and the wall has been reached without raising the foot from the accellerator.

What to do to prevent the greedy sods from missappropriating your life savings in their ass-covering rush?

and peak antibiotics bites the dust. Cursed innovators ruining good scare stories.

http://www.telegraph.co.uk/news/science/science-news/11331174/First-new…

Profile, I'm sorry to hear about the shale bust. I hope you weren't too invested in the scheme, it can be difficult to resist with so much hype. Hopefully the fed bails the companies out like the good capitalists they are. Stay well and chin-up!

Pluto, sorry to disappoint - not a cent - I'm in a completely different industry.

Not sure why you think I would have invested in oil shares if I thought the price was going to go down?

Yes all that "hype" sent the oil price down 55% and made petrol the cheapest its ever been. Hype would be all the comments pontificating oil would never go below $110... The derision when I posted links here 6 months ago suggesting oil could go below $75 was more in the hype department.

https://www.aei.org/publication/oil-gas-prices-fall-historically-low-le…

"Yes all that "hype" sent the oil price down 55% and made petrol the cheapest its ever been"

Yep, that hype is now in the process of wiping out the industry. Boom-to-bust indeed. Global deflation through economic weakness is certainly playing an important role as well. Here's to happy motoring.

Just like the "hype" that low gas prices would wipe out the shale gas industry?

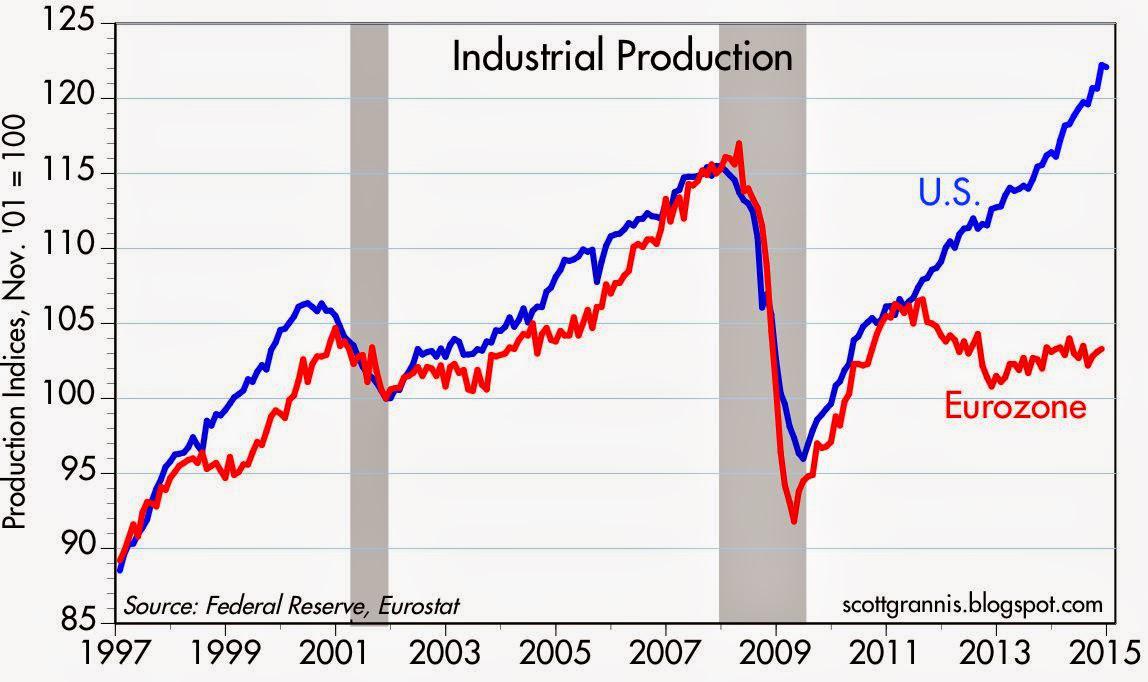

Check out US industrial production. Busting? Economic weakness?

http://static.cdn-seekingalpha.com/uploads/2015/1/19/saupload_Global_2B…

{kind=link}

Some of course are not happy as its costing jobs or their investments. Just how long it stays low and the fallout from that (national budgets, junk bond market losses etc) is going to be interesting to say the least.

regards

I've checked and oil price drops don't really equate to global recessions et al. Sometimes they do, but in recent history they have actually been more linked to new supply comming online. North sea, Alaska, Deep sea GOM, and now fracking. OPEC hasn't cut production in those ssituations. We have similar issues with many commodities at the moment, which is a boon to the consumption side of the economy, but many producers will suffer if this lasts longer then June this year.

a) We are past peak poil so looking at the past for the future isnt the best idea, maybe.

b) There is more of a link that high prices send the US economy into recession, then the price of oil can drop, aka 2008/9.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.