Today's Top 10 is a guest post from Matt Nolan, an economist at Infometrics, and a contributor at the blog site TVHE.

As always, we welcome your additions in the comment stream below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

Over to Matt...

In the past decade I’ve had the privilege of discussing economic data and concepts with intelligent non-economists and students as an economist. This has shown me there are often subtle misunderstandings that occur when discussing economic concepts – misunderstandings that lead to ideas being misappropriated or misused.

Now this isn’t a question of intelligence, many of the students and interested laypeople I’ve talked to are objectively smarter than I am. No matter how smart we are, however, without carefully working with our economic tools we can arrive at received wisdom that doesn’t tell us the whole story. Furthermore, I’d also be lying if I said I had learnt nothing about my own misunderstandings from this experience.

As a result, here I’ll outline a few common economics ideas with how they are understood – and then note how this matters when considering an issue I can’t help but talk about, income inequality.

By doing this we can illustrate that economic concepts don’t provide some ready-mix toolbox for solving social problems, instead they give us a lens to try and understand issues and outcomes that we are observing.

1. Deadweight loss and efficiency.

Why do people trade? Fundamentally, trade occurs when the buyer values the product more than the seller. Sure we can make an argument when such trade may not be in someone’s interest, or may be based on an unfair situation – but this does not undermine this view of trade.

In this way, if there is a single market price, then as long as trade occurs at a price where the value to the buyer who values the good the least and the value to the seller who values the good the most are equal then we have an outcome we may see as efficient. Graphically, this is our typical supply and demand curves crossing, and the “extra value” created by trade occurring is represented by the area between these curves.

The price then sets who gets this benefit – it either goes to consumers (through consumer surplus) or producers (through producer surplus).

But this “supply curve” comes from a view of competition where firms can sell as much as they want at a given price. If, for some reason, firms sell at a higher price/produce less then we have less surplus to go around – which we may term a loss of efficiency or deadweight loss.

There are two issues that crop up when we think about efficiency in this way:

- The effect on others and other markets.

- Even ignoring other markets, we lose sight of where the loss comes from if we are not careful.

When the first issue is discussed it is with reference to externalities or general equilibrium effects – but to be fair those issues to get a bit of coverage and a lot of people I chat to are comfortable with them. What often goes missing is a check to make sure we are clear at representing what this “loss of efficiency” really means.

Take a monopolist as an example.

Here the monopolist is willing to sell to additional people at a price that is higher than the price additional buyers would be willing to pay. There are fundamental gains from trade, but the monopolist knows that if they want to sell to this additional person they have to cut the price they charge everyone – this loss of revenue leads to them purposefully selling less than they want to at the current price.

So this is not an argument of the monopolist manipulating prices by nefarious means – it is a statement that their choice of output influences the price they can charge everyone. The “market power” in this case is just a statement that their choice of output influences the price, nothing more. And the result of this is a situation where trade that they want, and that some buyers want to occur, does not happen.

2. The problem of monopoly.

Given the above description of deadweight loss I have had a number of conversations where an intelligent person will define monopolies in quite a sophisticated way that can be boiled down to the following:

Monopolies are either natural and must be allowed to exist and should be regulated, or they are not natural. If they are not natural then their existence is the result of some “barrier” such as intellectual property – here there is a trade-off between static deadweight loss and dynamic efficiency from the firm investing in ideas.

This is a powerful definition that captures a lot of things, and with it we could look at the type of decisions policy makers make and make good sense of them. But it also misses many of the reasons we might care about them – or we may not.

- Contestability and substitutability: At some level your corner dairy is a monopoly – it is the only seller of a given set of groceries at that place and time. However, there are nearby dairies and supermarkets that offer close substitutes and other potential entrants that may set up a dairy if the current owner is “milking it”. This discipline on the price leads to monopolists producing more and charging less.

- Price discrimination and equity vs efficiency: Deadweight loss would disappear if the monopolist could just charge each person different prices that were unrelated to each other. But if the monopolist could do this they have another type of power that allows them to take some of the benefit to consumer and give it to themselves. When many people fear market power it is this sort of thing they are worried about rather than deadweight loss.

- X-inefficiency: Finally, none of this discussion actually involves thinking about how a firm functions in reality. If we have a large monopolist, with no comparable firms, and involving managers with a lot of power then are choices going to be made that reduce costs and maximise profit? Probably not. These inefficiencies that come from a lack of competition are called “X-inefficiencies” – and are an additional way that resources are transferred away from consumers to people within the firm.

Making monopolies only about deadweight loss makes us blind to many of the real issues of market concentration – but more on that later.

3. Tax incidence.

All governments enjoy telling us how much of a tax cut they are giving us when they pop one in a Budget. But when they cut income taxes, does the full tax cut actually end up in our hands?

At first brush this might seem like a silly question – after all our payslips show income gross and net of tax, and if taxes were smaller this net income figure would be larger by definition. But the gross/market income figure does not just appear out of thin air – it depends upon what the firm is willing to pay in order to hire you. They were able to hire you when you accepted a given net wage – so if taxes are cut why wouldn’t they just scoop up all the gains by cutting your gross wage?

What ends up happening – namely the answer to whether it is a firm or their employee that receives most of the gain of a tax cut/cost of a tax hike – is a question of tax incidence.

Two key things come out from thinking about tax incidence:

- The group that is more “responsive” to the tax will pay a smaller share of it

- The less responsive a group is to a tax the less they reduce how much they buy/sell due to the introduction of a tax – implying that the proportion of the surplus lost in deadweight loss (the loss of efficiency) is smaller.

What am I saying? For our interests we will focus on the first point – the more you would change your behaviour if the price changed (relative to the person you are trading with), the smaller the share of any tax you will pay.

For example, say that you were very willing to change how much you worked based on the wage your received – but your employer has a fixed set of demands from you which don’t vary much based on the wage they are paying. In such an instance, the employer will end up paying most of any tax – and as a result, will also benefit most from any tax cut. This won’t happen instantaneously, but over time the wage they pay will be conditioned on these respective incentives.

4. “The demand curve always slopes down and the supply curve always slopes up” and labour markets.

As the price of something goes up we are less likely to buy it, but more likely to sell it. This is intuitive, matches with experience, and is a concept we all apply whenever we move to think about markets.

But once again it is only half the story.

Unlike many people, I have no problem talking about my work in terms of inputs and markets. I am a labour input. People hire me to do a job – and this acceptance allows me to sit down and think about how I respond to changes in my work life without getting stuck on concepts regarding what I believe to be just.

So I sell myself. That is fine. My price is my wage – but do I try to sell more of my time if my wage goes up? According to our intuition a higher hourly wage makes working more attractive, and increases the opportunity cost of not working, and so I should work more – but something doesn’t quite feel right when I try to apply this to my own choices.

Such a view ignores that there are two competing effects that I wrestle with when I go to work – income and substitution effects. The substitution effect is what we’ve described above. Meanwhile the income effect is the name for the fact that – if I suddenly had an extra 4 hours in the day – I would spend some of it simply relaxing. In economist terms this means we call leisure (not working) a normal good.

On the face of it this sounds esoteric and a bit boring, so why do we care? In fact, a lot of simplified analysis by economists ignores the existence of this effect. But in certain circumstances – such as when considering how much people work – this matters.

5. Inflation, wages, and incomes.

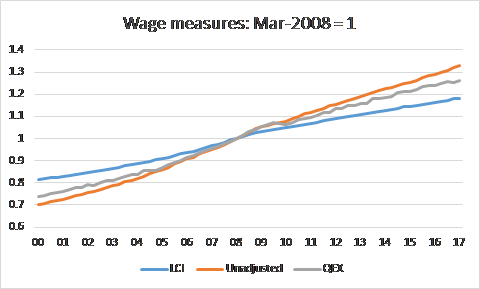

A misunderstanding that has been endemic in New Zealand business reporting for at least the past decade (the period of time I’ve been working as an economist) is confusing inflation measures for wage growth.

Journalists keep reporting the labour cost index (LCI) as wage growth, and complaining that there has been no real wage growth for a long time. However, if we are going to select a measure of wage growth we can see that picking the LCI gives the smallest number possible. So is it the right measure?

No. The LCI keeps the “quality” and “composition” of jobs fixed and asks how much it costs to hire someone to do that job, the unadjusted LCI keeps the composition fixed while allowing the quality to change, while the QEX tells us what actual hourly wages are (such that the quality and composition both change).

If firms are becoming more productive (either through technology or investment in tools) then the quality of work is changing by this definition, and so the LCI is removing wage growth due to productivity increases. If bargaining power between employers and employees was unchanged we would expect wage growth to equal productivity growth plus expected inflation. If employers and employees get inflation guesses about right, that would mean real wage growth is equal to productivity growth.

Using the LCI to measure real wage growth for NZ households is the same as assuming that there is no real wage growth. It might make a good headline, but it shows a misunderstanding of these economic concepts.

6. Putting it all together: Income shares and the role of tax policy.

Ok, we’ve run over some economics ideas and hopefully shown there is more to them than the soundbites that often get thrown out. But how would we apply any of this?

One policy issue that has gotten a lot of attention is changes in incomes shares. Namely, in many high income countries the share of income going to capital owners has increased with the share of income to those who sell their labour falling.

This isn’t saying that wage earners are worse off – but it does suggest that in these countries the benefits of growth have gone to those who own capital. Note: This is different from the income inequality that we often hear about on TV, which is focused on household incomes.

We may believe this is unfair and as a result we may state we want to use taxation to remedy this. This was the issue at the core of Thomas Piketty’s book “Capital in the Twenty-First Century”.

However, as we noted when we discussed tax incidence where the burden of any given tax falls depending on how responsive the behaviour of the buyers and sellers are to changes in the price of it.

This is complicated further by the fact that labour and capital are used together to make output – if you convince a firm to invest less in capital through taxation, then labour has fewer tools to create final output.

As a result, if capital is very responsive to taxation OR capital and labour and non-very substitutable then taxing capital in order to increase the share of income going to labour would be counterproductive – either due to the large output cost, or the fact that it would make the share of income going to labour fall! A more technical discussion on these things and capital tax can be found here.

The key point is that we can’t just take a chunk of capital income and move it somewhere else with taxes – the reality is much more complicated no matter how much some journalists and politicians want to act otherwise.

If you have been following the Piketty debate you may have noted economists bang on about the elasticity of substitution when discussing this. Piketty assumed that this figure was sufficiently high such that taxing capital would increase the share of income going to labour, and he assumed that the response of capital owners would be limited. However, these assumptions are at odds with the data – implying that the mechanism for rising factor income inequality, and the appropriate solution, might be more complex.

7. Putting it all together: Competition and inequality of outcomes.

Above we have discussed changes in the share of income going to different groups, and how its meaning and the ability to redistribute through the tax transfer system are both relatively uncertain.

However, there remains one area we have discussed that can explain part of what has happened with income shares, and suggests that outcomes that are more efficient and potentially fairer are possible. This is with respect to monopoly and competition.

Generally competition discussions are the purview of arguments about inefficiency, or the distribution of resources between consumers and producers. But could a dearth of competition also influence the distribution of factor incomes – namely change the way income generated in the market is split between those who own capital and those who provide labour? As the NY Times points out, a lot of the time economic commentators think not. From their article is the following quote:

Martin Gaynor, a professor at Carnegie Mellon University and former chief economist at the Federal Trade Commission, noted that competition policy was about increasing the economy’s efficiency, not changing the distribution of the spoils. “I don’t think antitrust is a major tool for addressing inequality,” he told me.

But here we like to do a little bit of thinking for ourselves, so let’s try to figure out why it may matter. When we discussed monopoly we noted that they were inefficient even with perfectly reasonable intentions – even if the intentions of the monopolist and the competitive firm are the same, the very nature of the market implies that they will make less at a higher price than the competitive industry.

This doesn’t tell us about our income share – but it will get us part of the way there!

Furthermore, monopolies can create household income inequality. In 1999 Creedy and Dixon discussed the distributional consequences of monopoly with reference to the idea that the lost consumer surplus due to the existence of a monopoly may fall differently on different groups of consumers.

Here consumers who have lower income may suffer disproportionately in the face of higher prices – this is not because lower income people are being targeted, or being charged a different price, because of the circumstances they find themselves in when dealing with a larger markup on consumer good prices.

Sidenote: This is something that should be remembered when people discuss how we need a lower New Zealand dollar to help exporters – by the same logic one of the main losers from this are low income Kiwis.

8. Broadening monopoly and the income share.

One problem with looking at monopoly solely as a competition issue in a given market is that we ignore the type of market power they may have in other markets they trade in. Specifically, if a large firm is the only seller of a product they may also be one of the main buyers of the inputs used to create the product. When there is a single buyer this is called a monopsony.

If we have an economy with few large firms then it isn’t just consumers that end up paying higher prices – but employees that get a smaller share of the income generated by creating the product.

In this way the effect of monopoly is two-fold – it reduces the purchasing power of consumers and reduces the income share of employees. Furthermore, both these markets induce a deadweight loss on top of the change in income shares – implying that such a shift can explain the slowdown in productivity growth as well as an increasing share of income going to capital.

This combination – the larger profits and the lower wages associated with market structure – would explain why the share of labour would fall. The monopolist in this instance isn’t doing anything to explicitly lower wages or increase prices, it is just responding passively to the market structure it finds itself in!

9. Competition, rent seeking, and income shares.

However, the discussion above only focuses on a narrow aspect of monopoly – as we noted at the start the market failures of a monopoly (and some of the benefits of that structure) are larger than our basic understanding of a monopolistic market suggests.

When it comes to discussing income shares the existence of greater market concentration clearly gives us our result – as industry profits, which constitute the return to capital owners, are higher.

This is where the language gets a touch ugly. These extra profits are called “economic rents”. But this is NOT rent seeking – rent seeking behaviour is another important motive, but even without that increasing market concentration should be related to a rising capital income share.

Stiglitz stating that rent seeking is likely to be a major determinant of many of the things we view as unjust. As a result note that this isn’t due to the existence of monopolies itself, but the way they set up and protect their market position.

However, as the Economist points out this isn’t a simple issue – there are a variety of competitive issues spanning market concentration to occupational licencing which are all contributing to an environment where someone with the fortune of becoming an “insider” ends up benefiting while those on the outside lose out.

Such rent seeking does not imply that labour incomes share falls. Instead, it suggests that people who are inside a firm that has such a position extract some of these gains for themselves (eg excessive compensation for CEOs). This is really a form of X-inefficiency, and if we used our pure model of monopoly this is not something we would capture.

This restriction of opportunity – making the outcomes of those who do well or poorly more based on luck than on merit – suggests a place where policies that help to stimulate competition don’t just improve efficiency, but are also just.

Sidenote: If these are indeed the motive for rising capital income shares, then there isn’t any reason to expect these shares to keep rising – as Piketty does.

10. Monopoly, competition, and policy.

By separating out our issues regarding monopoly, taxation, and the way consumers respond we’ve been able to illustrate how the issue of “market power and concentration” isn’t just some single thing. Instead, it is a phrase that captures a large range of different potential problems.

What policy makers will want to do depends on which of these issues of competition are most important. Is it the lack of efficiency in a strict sense, the X-inefficiency associated with a lack of competition, or the excessive rent seeking that is creating situations we see as unjust?

What policies? Strict inefficiency? Either break down barriers to entry or regulate the price! X-inefficiency? Recognise it is due to principal-agent concerns within the firm, so increasing information and effective competition is necessary (along with an admission that it limits the ways you can regulate price)! Excessive rent seeking? Work on intellectual property laws and electoral funding transparency laws to reduce the scope for such rent seeking!

This doesn’t necessarily mean breaking up monopolies or targeted taxes on capital. If monopolies are indeed the result of scale, and technology is such that the burden of taxation falls elsewhere, then this doesn’t work. However, if that is the case is supports more active regulation – and more active market regulation in turn would, if this is the reason, also reduce the dispersion of earnings.

In the end it is not the inequality of incomes or the motives of the monopolist that we fundamentally see as unjust, but the disparity in opportunities that are the result of a given social structure. Careful use of economic ideas to identify this, as we have discussed above, gives us a starting point for figuring out what policies should be done.

3 Comments

Well well where do I start ?

Firslty , monopolies are in my view fundamentally evil , and while a necessary evil in some instances , they should never be allowed to go on for too long .

The worst example that affects us in Auckland is the charges by Watercare for a water connection at $14,000 its beyond ridiculous and its a monopoly . It is simply passed on to the price of housing exacerbating an existing cost problem .

Then I have issue with the price of milk , when Fonterra sells milk in countries like South Africa through its associate there called Clover , for less than it does here . The reason milk is cheaper there is because there are 100's of milk producers/ processors all vying for market share , unlike here where there is a single price maker and a handful of price followers

The next is the unhealthy state of the building materials market , where there is protectionist rules in place for example (GIB) that favour the dominant player , but the pricing of just about all materials is opportunisitc and smacks of collusion

Then look at the price of petrol , this is likely the worst form of collusive behaviour because we are all forced to pay oligopoly prices that go up or down in near perfect unison

The concentration of power in the retail food sector ( supermarkets ) is extremely unhealthy for New Zealand

There are way too many examples of monopolies and oligopolies (or other forms of market concentration) in New Zealand and the net result is we pay over the odds for a lot of stuff .

I order to avoid being sucked into paying monopoly prices in a small way , we use tank water at home , restrict the consumption of milk , and use hybrid and diesel cars.

I hold shares in Woolworths (Countdown) because I figured if you cant beat them , you might as well join them .

It is always a challenge with monopolies in New Zealand. For instance, we have commonly seen airlines come to New Zealand, attempt to compete on regional travel, but eventually collapse. This raises the question whether a 'benign monopoly' may be more efficient. The issue of building supplies is interesting, and particularly in the face of the recent media coverage of builders using 'unaccredited cheaper products from overseas'. I remain suspicious that the entire issue is reported and brought to the media by firms who are at risk of losing market share.

It's a tricky one.

But specifically for building supplies, it's of such significant concern that the govt. should seriously consider setting up a govt. owned supplier. Won't happen under National but maybe Labour/Greens?

For the rest, I think we should criminalise cartels and formally recognise oligopolies and monopolies at which point we could monitor them intensively and consider windfall taxes.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.