Finance Minister Nicola Willis has decided New Zealand's incoming Depositor Compensation Scheme (DCS) will build up a fund size over 20 years equivalent to 0.8% of protected deposits, or about $1 billion, Treasury says.

This key detail is included in a consultation paper issued by Treasury this week.

The paper covers the funding strategy for the (DCS), known as the Statement of Funding Approach (SoFA). The DCS will be established by the Deposit Takers Act and will compensate up to $100,000 for each depositor per licensed deposit taker in the event of a deposit taker failing. The DCS is currently scheduled to launch in mid-2025.

"Following feedback from this first round of consultation, the Minister [Willis] has decided to target a fund size of 0.8% of protected deposits over a 20-year timeframe," Treasury says.

Treasury's prior consultation said the fund that'll be established to back the incoming deposit insurance scheme would be equivalent to between 0.5% to 1.1% of protected deposits, or $600 million to $1.4 billion. Thus 0.8% is about $1 billion.

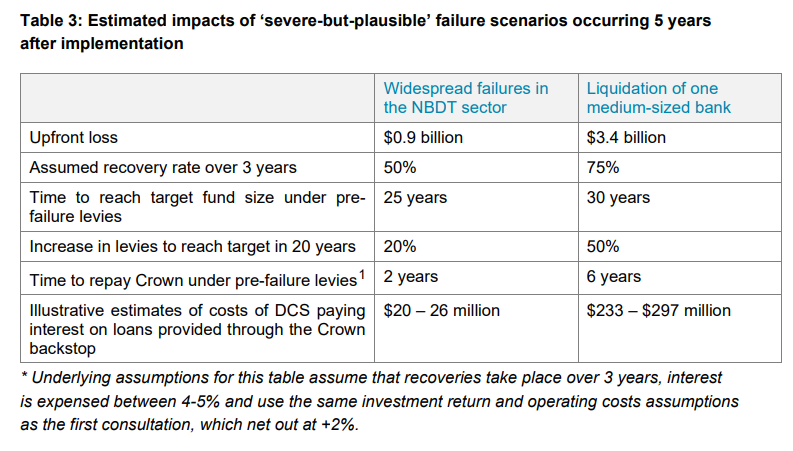

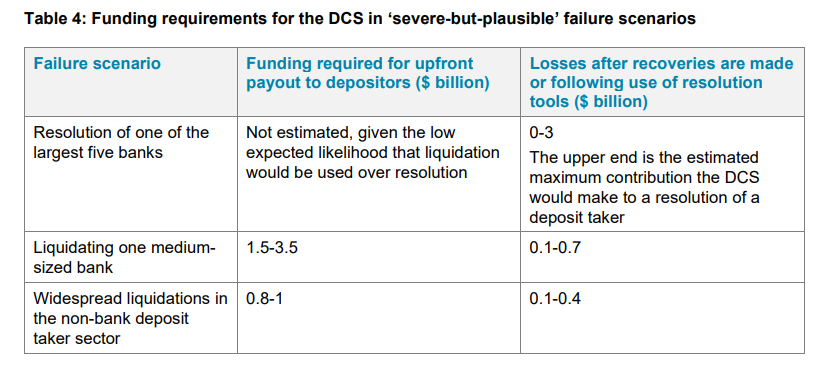

"A target fund size of 0.8% of protected deposits is planned to be adopted. This target is estimated to be sufficient to cover the net cost of the estimated ‘severe-but-plausible’ failure scenarios that Treasury has modelled [see table 4 below]," Treasury says.

"A 0.8% fund, relative to 0.5%, places greater weight on the ‘resilience’ principle and would provide a greater buffer against the Crown bearing the medium-term costs of a failure event (given that the likelihood of the Crown backstop being required after a failure would be lower, especially as the DCS fund nears its target). A higher target fund, ie, 1.1% of protected deposits, would not be consistent with the ‘efficiency’ principle, as there would be a material risk that levies would exceed the expected cost of failure events over time, taking into account recoveries that would likely be made from a failed deposit taker."

"The Minister has also decided that the funding strategy should aim to reach the 0.8% target over a 20-year timeframe. A build time of 20-years supports the ‘equity’ principle with the costs spread over a larger cohort of potential beneficiaries relative to the alternative options of 10 or 15-year timeframes that were consulted on. A longer timeframe also allows more time to recalibrate the targeted size of the DCS fund over time based on new risk information, including any failure events that occur during the build-up phase," says Treasury.

"The 0.8% fund combined with the resilience of the NZ deposit taking system provides confidence that ‘severe-but-plausible’ failure scenarios could be managed."

Funded by levies

The DCS will be funded by levies, set out in regulations, collected from licensed deposit takers including banks, building societies, credit unions and deposit taking finance companies. Money from the levies will be held in a statutory fund with a Crown backstop to meet payout requirements if the DCS fund is in deficit.

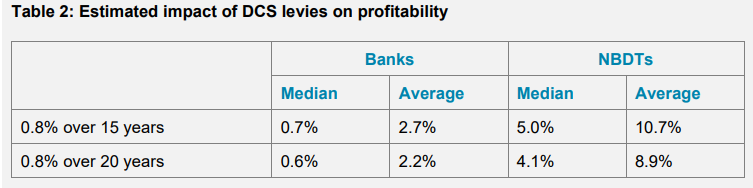

In the previous consultation Treasury says larger banks were supportive of a 0.8% fund with smaller banks and non-bank deposit takers more in favour of a 0.5% fund. Most submitters preferred a 20-year timeframe, with some support from larger banks for a 15-year timeframe. Smaller deposit takers were particularly concerned about the impact of the DCS levies on their profitability and competitiveness (See table 2 below).

The DCS fund will be administered by the Reserve Bank.

Treasury says Inland Revenue has advised the Reserve Bank the DCS fund will be exempt from income tax, thus reducing the levies required to be collected annually to meet the fund targets, compared to what was assumed in the first consultation when it was thought both the payment of levies and the investment returns from the DCS fund would be taxable.

"The impact of DCS levies on the profitability of deposit takers is likely to be unique to each deposit taker and will depend on several offsetting factors," Treasury says.

These include the deposit taker’s ability to; pass on the levy costs to depositors without losing deposits, attracting deposits that result from deposit-splitting (ie, the likelihood depositors with balances exceeding $100,000 at a single deposit taker will split that deposit across multiple deposit takers in order to maximise coverage under the DCS), and attracting deposits by offering insured deposits at competitive deposit rates, which might be lower than those they offer now.

"The Reserve Bank is currently consulting on its preferred levy approach. A different levy approach would change the impact on profitability."

"The estimates in Table 2 [below] assume that the cost of additional levies is fully absorbed by deposit takers through lower profitability...It is possible that the cost is instead passed on to customers. Illustrative estimates suggest that levies could impact deposit rates by approximately 5.5 basis points for the 0.8% target fund built over 20 years," Treasury says.

It goes on to say it's likely some degree of levy will be needed even after the 0.8% DCS fund target is met, to account for growth in deposits, which is estimated at 6.2% annually, and the fund's operating costs.

"Following a failure event that results in the funding of the DCS being drawn on, the Minister of the day would need to make a judgement about whether to adjust the targets for the DCS fund. This would be expected to trigger a review of the SoFA."

Such a review would focus on whether and by how much to extend the timeframe for reaching, or returning to, the target fund size.

Treasury says the SoFA's target fund approach will take into account "the likelihood of significant recoveries made by the DCS during a receivership or liquidation."

The Crown backstop

Treasury notes if the DCS fund doesn't have enough money to meet its statutory obligations, the Act requires the Finance Minister to provide public money to the fund on terms and conditions agreed by the Minister.

"This statutory obligation is known as the Crown backstop. The Crown backstop will provide public assurance that compensation will be provided in a timely manner, following the failure of a deposit taker."

"If the DCS fund is in a deficit position, the Treasury expects that a loan would be provided to the DCS to cover the deficit. Any earnings from the DCS, including recoveries from the failed deposit taker, would be used to repay the principal and interest on the loan."

"The Act sets out an expectation that the costs to the Crown in connection with the backstop, including the costs incurred in holding additional liquidity, and the costs of repaying any money provided to the DCS fund (eg, any interest, or other charges) are to be fully met out of the fund," Treasury adds.

Under the Act, the Reserve Bank will be able to invest DCS funds not immediately required for expenditure.

OBR to be 'modernised'

Meanwhile, the Reserve Bank says it's looking to "modernise some aspects" of its Open Bank Resolution (OBR) tool for responding to a bank failure, and integrate the DCS with it.

"The Deposit Takers Act introduces a new regime for resolution, including making the Reserve Bank the resolution authority and requiring us to publish a statement of approach to resolution. The OBR policy is now over 10 years old and we have a new statutory framework for resolution we need to consider. For example, we are reviewing the scope of depositor haircuts in light of the upcoming DCS, which will protect depositors up to $100,000 per depositor per institution. We are also considering the implications of industry developments, notably SBI 365 [365 day-a-year payments]. Alongside these updates to the OBR policy, we are also considering the broader way forward for our approach to resolution under the Act," a Reserve Bank spokesman told interest.co.nz.

The Reserve Bank will set out its proposed approach to OBR-DCS integration in its Deposit Takers Act non-core standards consultation around mid-2024, the spokesman says.

"The updated OBR prepositioning policy will be a Deposit Takers Act standard, and will follow the general timeline for Deposit Takers Act standards. We currently expect to issue these standards in January 2027, with standards expected to commence around mid-2028."

Following this Treasury consultation, Willis will make final decisions, with the SoFA will be published before DCS regulations, including levy regulations, are implemented.

"We will consider all feedback to inform publication of the first SoFA. The Act requires the Minister to take all reasonable steps to publish the SoFA before 7 July 2024, and at least every five years thereafter," Treasury says.

The GFC-era guarantee scheme

Although there have been no bank failures in New Zealand in recent years, there have been banking crises in the past, and much of the finance company sector dissolved between 2006 and 2012.

During that Global Financial Crisis period New Zealand had deposit insurance through the Crown Retail Deposit Guarantee Scheme, for 38 months from October 2008 until the end of 2011. It cost the thick end of $1 billion, largely due to the demise of South Canterbury Finance.

In the wake of South Canterbury Finance's collapse into receivership in August 2010, Treasury announced the Government would cover all depositors of Crown guaranteed finance companies that defaulted, including those that had already defaulted, regardless of any previous eligibility criteria in place for the Retail Deposit Guarantee Scheme.

The late Michael Cullen, Finance Minister when the 2008-2011 scheme was established, told interest.co.nz in 2012 the New Zealand government of the day was "forced into" a much more comprehensive, open ended scheme than it had been considering by the "panicky" actions of the then-Australian Prime Minister Kevin Rudd.

In 2013 Treasury said any future retail deposit guarantee scheme would incorporate lessons learnt from the previous scheme and would be tougher.

*There's more on depositor compensation in this episode of our Of Interest podcast here.

**And see how the OBR might work, if it was used, here.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

5 Comments

For comparison, under the earlier deposit guarantee scheme, $1.6 billion was paid out on the collapse of South Canterbury Finance, and nearly $2 billion overall, and that was more than 10 years ago

Thanks for the reminder of that GFC-era Crown retail deposit guarantee scheme. I've added some detail into the story about it.

What has happened to the Cullen fund - is the government contributing or drawing down?

Nothing from here on, is a 'fund'.

That assumed 'money' to be a 'store of wealth'.

That in turn assumed future underwrite.

This is where all such discussions fall down now - without accounting the underwrite, we're in cloud-cuckoo-land.

PDK - not sure I understand - can you explain further please.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.