ANZ economists believe interest rates will continue to nudge higher and this, coupled with tighter credit conditions, will keep the brakes on the housing market.

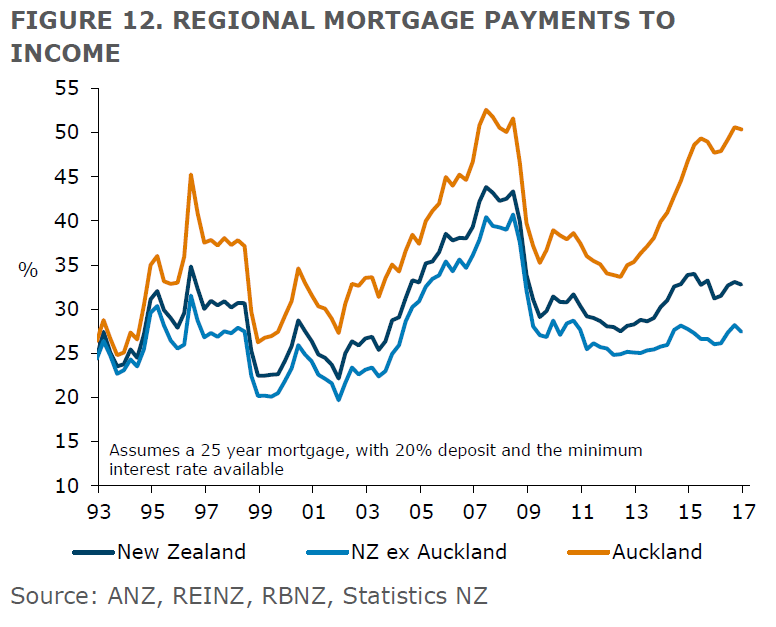

In ANZ's latest Property Focus publication the economists have estimated that mortgage costs on the average house for new purchasers in Auckland are chewing up about 51% of monthly income - and that's at a time of very low interest rates.

"That is on par with the highs reached in 2007 despite mortgage rates being near historic lows currently," chief economist Cameron Bagrie says.

"It highlights how sensitive some recent home-buyers in Auckland would be to even a small lift in interest rates."

And Bagrie says interest rates are going to keep nudging higher.

"It won’t be rapid, and it won’t be driven by the RBNZ, primarily."

A directional change in interest rates has three important implications, Bagrie says.

Firstly, increases in borrowing rates change the economics of the entire borrowing equation and can turn "affordability metrics" sharply, especially when the levels of debt are far larger.

"House prices have risen to such an extent that we estimate that for the average Auckland household to purchase the average house (at a 20% deposit, 25 year mortgage term and at the cheapest mortgage rate on offer), debt servicing costs (principle and interest) would now represent 51% of average disposable incomes.

"A 1 percentage point increase in mortgage rates would see this jump to nearly 56%, which is far higher than in 2007, when the minimum mortgage rate was closer to 9%!"

Secondly, Bagrie says higher interest rates get the market (buyers) thinking about where rates could be a couple of years down the track – "and that’s critical for market psychology".

And finally, higher rates force a shift to the fundamentals and more cash-flow based investing. "It needs to be more of a numbers game and less of a capital gain one. There are still strong expectations for capital gain though; 4.6% according to the ANZ Roy Morgan expected house price inflation measure."

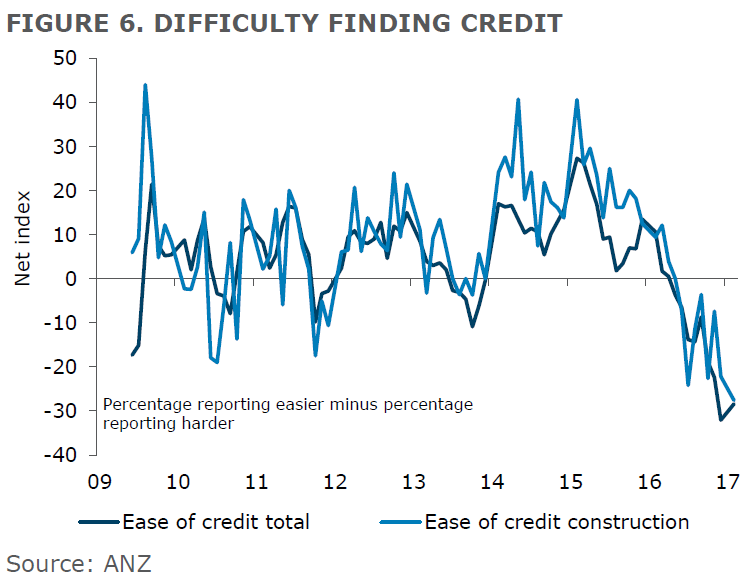

Bagrie notes that the property market has cooled rapidly as the combination of loan-to-value ratio restrictions, higher interest rates (a turn in both the local and international cycles) and "credit rationing" dampen demand.

"That’s provided a near-term hit to recent exuberance, though it’s worth bearing in mind that a demand-supply mismatch will provide support and typically that’s seen the market run away again after previous similar lulls.

"What is different this time around is that interest rates are moving up and appear set to continue to do so, and policymakers are more serious in their desire to quell excessive lending growth. This will reduce the potential for the market to lift in a material fashion from here."

On the actions of policymakers, Bagrie says: "The RBNZ is undertaking a review of bank capital; if banks have to hold more capital that will put more upwards pressure on interest rates. Regulators on both sides of the Tasman are not standing idle; this will impact both the price and availability of credit as they eye curbing the credit accelerator model and leveraging behaviour (growing borrowing in excess of income growth), which are seen as a threat to financial stability."

Bagrie says that previously when the RBNZ has introduced loan-to-value ratio restrictions there has been a lull in housing market activity followed by a resurgence as interest rates have continued to fall.

"House prices can look semi-affordable at a house price to income ratio of 9.5 when interest rates are extremely low, but the key point is that it is not sustainable; the equation can change dramatically when interest rates nudge higher."

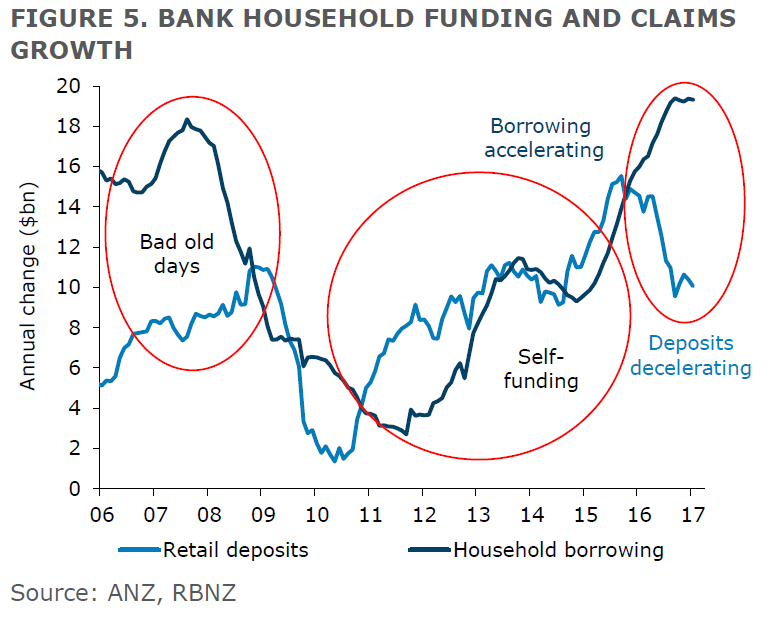

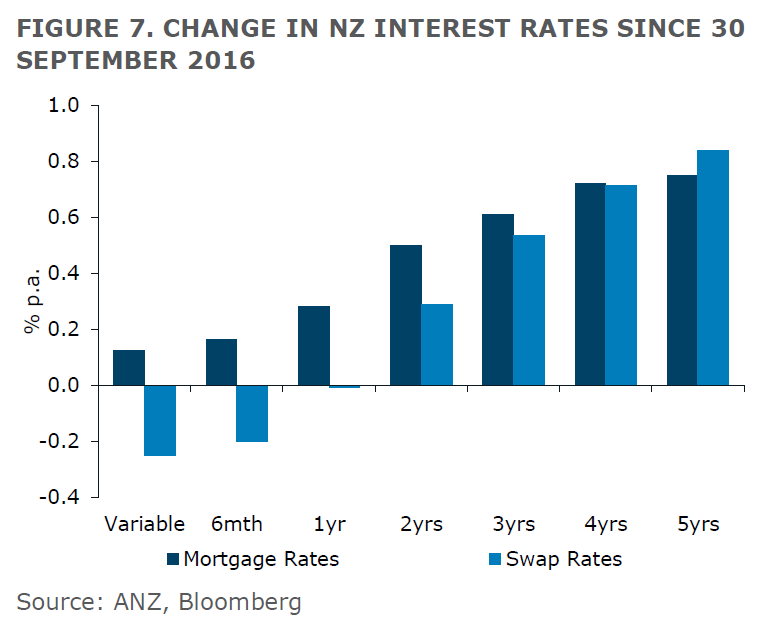

The key driver of the anticipated continuing rises in interest rates, Bagrie says will be the "the massive funding gap, which is forcing a change in bank’s behaviour".

"Deposit growth continues to trail credit growth. In household parlance, that’s more money going out the door than is coming in," Bagrie says.

"Banks can fill such a gap temporarily by borrowing offshore, but it would not be in New Zealand’s long-term interest to let such a gap persist. The current account deficit (and external debt levels) would blow out, New Zealand’s credit rating would likely get reviewed, and inflation would turn up if a spending boom were to join the housing equivalent, necessitating tighter monetary policy and a higher OCR. Credit-driven booms invariably end in a bust as the piper gets paid."

Bagrie says the banks' funding gap portends more pressure on deposit rates to lift and credit growth to slow, "which is precisely what we are seeing".

"...And on top of that we expect a gradual rising bias to international interest rates, which will impact longer-term rates here. Which is going to win out? Rising interest rates and diminished credit or a shortage of housing supply in the face of still-strong migration?

"The former will actually dampen the supply side response, making the supply-demand imbalance even starker. Witness all those stories in the paper about projects struggling to get finance – although a big reason for this is also an explosion in construction costs, which makes it even more difficult to get the deals to stack up (refer last month’s Property Focus). Economics 101 tells us prices will need to lift if an even larger shortage opens up.

"We’re backing interest rates and credit to dominate supply-demand imbalances, or at least buy some time for the latter to catch up. That seems to go against the aforementioned Economics 101 conclusion, but if the supply thesis was really all that’s driving property prices we wouldn’t have seen such a wedge open up between house prices and rents. The latter would have risen more sharply too. This doesn’t mean we discount supply tension. Such tension will still be apparent for a long time yet. We simply need to put it in context and think more broadly."

41 Comments

With 51% household income going to debt servicing there shouldn't be any problems if the interest rates double from the low of around 3.99 to 4.25%.

scary stat 51% and that is on historically low rates, im sure many baby boomers did not have to deal with that level too long as inflation changed that figure quickly of the life of there loan.

Not just that but their loan terms were shorter than the common 30 year loans these days. I know some people that had installment loans instead of table loans. They suffered a lot initially but their cash flow improved with each payment (by choice).

I don't like seeing people pay such a large proportion of their income for housing. It's very risky and no doubt some have felt they had no choice if they wanted to buy a house.

Interest rates are not going to be moving up much at all.

The economists that are saying this have previously stated this and you know what happened?

They dropped substantially to historical lows didn't they.

Yes there has been movement in various rates but have recently refixed a couple of loans from 2 years ago to less than what I was paying then.

I don't beleive that the U.S. population can and will afford a substantial increase in interest rates as we saw previously when there market crashed thru their nil lending!

Time will tell but everything is not that rosy in the U.S.

As I understand it, many more in the USA are able to lock their mortgages at a given rate for the entire term rather than having it floating. I.e. 30 year fixed rate. Thus it wouldn't seem to affect those already in the market that much.

next hike for the FED is supposed be be june, may happen early as they try to keep ahead of the curve.

will be interesting to see how that effects the USA

Those fixing for 15 years also get a better rate. So far all the Fed has done is go from 0% to 0.25% with absolutely not impact and then to 0.5% recently. For those with an excellent credit rating they are paying around 2.5 to 3%. In the US the cost of the money is still very cheap and it's a good option. They are getting huge benefits from their tax advantaged tax accounts and mortgage write offs (both of which we don't get here).

If the Fed goes to 1% it will likely only have a minor impact in the US. Some may have to pay 3-3.5% on their mortgage. So low interest rates and low house prices is not going to be something they struggle with. Compare this to NZ where people are paying 4-6% interest on mortgages that are 3-5+ times larger.

Who's going to hurt more? Someone in the US paying 3% on $150k or someone in Auckland paying 3.99 to 4.5% on $500k-$600k?

That's why I don't get people who use the argument that home owners can't handle higher interest rates. A small rise in interest rates (say 50 to 100 bps) won't really affect you if you've already factored a rise into your house purchase already, and have additional discretionary savings/income to allocate to your mortgage if need be.

Rick you are correct - most people have 15-30 year fixed mortgages and you get an interest deduction on your income tax. It will only be new mortgages that are at a new higher rate.

If rates in the US don't go up as you suggest theman2, how are pension funds going to make their promised return? Are you saying pension funds will default just so borrowing rates stay low?

You can't have it both ways for too long - if rates are low then pension funds get killed. Sooner or later rates must go up or pensions funds will default, which would lead to chaos.

Auckland debt ridden buyers will act as a dead weight on interest rates, making the new 'neutral' for mortgages at around 6-7%, as any higher then we'll see carnage in Auckland.

What all this means is 10 years of 'well below average mortgage rate'... which means areas outside of Auckland represent excellent buying, and over next 5 years will increase 50% or so as mortgages will still be 5% over next 3 years at least, and buyer backlogs still exist post GFC in many of the secondary cities that haven't boomed like auck, ham, tga, queenstown (welly to certain extent now, another 2 years left in that market...) Buy PN.

you are right about carnage in auckland if rates hit 7% , but banks do not care they will increase margin to offset volume.

after all there first duty is to their shareholders not the customers as has been shown by the way they have treated savers who they now need

We'll get that 100 basis points of rate rises I think, even if the US slows it's hiking. All it would take is Australia losing its AAA rating (which will happen), APRA requiring the Australian banks to hold significantly more capital (might happen) and the onshore funding deficit remaining. Say 50bps due to Australasian conditions and another 50 bps due to the FED. For a wildcard throw in some tradable inflation and an early RBNZ hike late 2017.

I think ANZ and Mr Bagrie are on the money. And they have some great charts!

I feel there's at least 50 bps in increases likely in the next year. Unless an event occurs to reverse the direction. Say if the Auckland housing market caved in with house prices dropping 50% then I'd expect an OCR cut.

Additionally, it's not just the Fed 'hiking rates' which people should watch as a guide to rates going up.

e.g. the Fed are quietly rolling over their bond purchasers for shorter terms. Same result as higher rates (bond yields rise) but without actually raising rates.

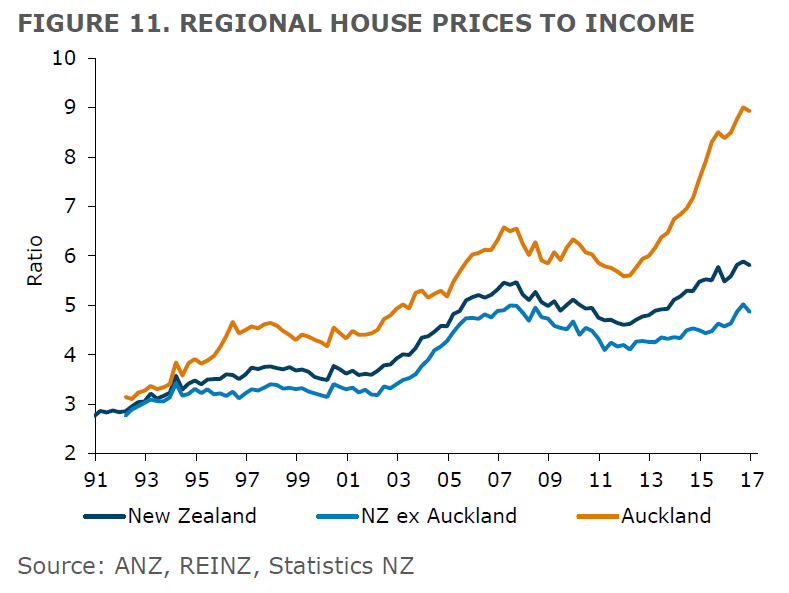

The first 2 graphs really show the massive difference between Auckland and the rest of NZ. There is a real problem in Auckland, the rest of the country is really fine at about 27% mortgage payments to income and house price of 4.8 x income

From people I've been talking to outside of Auckland over the past year they've been enjoying the reduction in interest rates. For some the financial pressure is reduced as their payments have reduced with the interest.

I'm fine with people paying around 25-33% for housing as it gives plenty of room for coping with interest rate changes. For 51% not so much.

You're not really comparing apples with apples Yvil. It's showing the median national regional statistic to Auckland City, not Auckland City with Christchurch, Wellington, Dunedin and Hamilton (the largest NZ cities with the highest house prices and largest inventory). For example, Canterbury would include Rangiora, Kaiapoi, Selwyn, Banks Peninsula and Christchurch City. All of the constituent areas would have different median and mean house prices, with the primate city in the region having the highest prices.

Wildcard, I said "The first 2 graphs really show the massive difference between Auckland and the rest of NZ" and they do, they read graph for "Auckland" and graph for "NZ ex Auckland". Not sure what you're talking about

Yes, it's "NZ excluding Auckland;" i.e. lumping 4 other regions with differing house prices (including cities) all together and with house prices in rural parts of the region being lower than in the city. When you say "...the rest of the country is really fine at about 27% mortgage payments to income and house price of 4.8 x income..." it is not representative of the individual cities or individual parts of the region. I meant (somewhat ambiguously, sorry for that) you are not comparing apples with apples when you use the NZ excluding Auckland statistic and say the rest of the country is fine.

Interesting how ANZ is trying to "prep" people for rising interest rates even though it's not substantiated by swap rates or the OCR

Yvil, so you don't think the massive disparity between deposits and lending is a concern for banks, the economy or NZ as a whole? And not even a little twitch when you look at the graph timeline of deposits v's lending, peaking right before the GFC, dipping again to more healthy levels after and then recently peaking to even greater heights than before the GFC? Do you not think banking stability is a concern?

gingerninja, it's your choice to be concerned for the banks, I was talking about interest rates and I was simply stating that neither swap rates nor the OCR warrant interest rates rises

I'm a bit confused by this. The Fed is signalling that they are going to hike at least another 2 more time this year. You don't think that will impact swap rates?

Maybe the Fed will, maybe they won't... I prefer to deal with facts and the swap rates have gone nowhere in 2017

It is not clear in the article if it is 51% of household income or 51% of personal income. I suspect the latter. If so it is not as terrible as it first appears. Most households have two incomes and some people rent out a room too.

Can this vitally important detail be clarified?

Household income. "the average Auckland household ...."

Full paragraph quote:

"House prices have risen to such an extent that we estimate that for the average Auckland household to purchase the average house (at a 20% deposit, 25 year mortgage term and at the cheapest mortgage rate on offer), debt servicing costs (principle and interest) would now represent 51% of average disposable incomes.

Agree. It's household

Seconded. It wouldn't make any sense to compare average household debt to a portion of the households income.

That's a bit of a strawman statement. It's regional mortgage payments vs. income, so the percentage will be higher in cities as the house prices there are higher. Also, not every home buyer is in a relationship or wanting to buy a house with their girlfriend/boyfriend/partner/husband/wife. Renting out a room would only work if the property had more than one bedroom, and the demand for one and two bedroom properties over McMansions means that this would become less likely. In addition, a FHB couple with children/planning to have children would not rent out rooms.

Would also be nice to know how many households are actually paying that 51%. It only shows that the average Auckland household can't afford to buy the average Auckland house. Does ANZ really lend on that basis?

According to interest's own data (from March 2017) median household income in Auckland is around 90k Median house price is around 800k so it really depends on mortgage size.

http://www.interest.co.nz/property/house-price-income-multiples

90k after tax income around $5500 per month (with some variation depending on who in the household earns what). 500k mortgage at 4.5% over 30 years is $2558 per month. For the 90k household income 51% would be a mortgage payment of $2895. Obviously, it's hard to know what sized mortgage people have, but if it's more than 500k then it's very possible that the average percentage of household income is 50%+

It's definitely household income. Can't really be bothered doing the sums but if you take the average lower quartile house price in Auckland and compare to average income for Auckland based 25-29 year olds it's clear mortgage payments work out at around 50% based on a double monthly income.

The beginning of the article says this:

In ANZ's latest Property Focus publication the economists have estimated that interest costs on the average house for new purchasers in Auckland are chewing up about 51% of monthly income - and that's a time of very low interest rates.

While later we read this:

..debt servicing costs (principle and interest) would now represent 51% of average disposable incomes

Perhaps the first paragraph should be mortgage costs?

Also I would wager that most home buyers get above average income while those below average probably rent. The statistics in this article are not that useful as it claims it only applies to the costs on the average house for new purchasers. It applies to only a small subset of bank customers, not everyone.

In the interests of clarity, have now changed that paragraph to talk about 'mortgage costs'. Fair point. Thanks.

an average skilled worker and their spouse will earn a lot more than 90k combined income, by skilled I mean someone in a profession, say teacher, policeman, fireman, builder, nurse etc hence housing ownership is in reach for the median of the adult population

Single people need not apply, obviously.

So the article is talking about the average household income. Income distributions are skewed towards higher earnings, meaning the median is lower than the mean. I'm not sure how you make the leap to housing being affordable to the median household, when it will be less affordable than to the average household discussed in the article? Perhaps what you mean is 'ownership is in reach of the median of high earning couples'?

Are you basically saying in Auckland you need to have 90K per household to own a house. Is this good or bad? This is a tonne of money to live on and to own a basic house. So if you have a wife whose not working looking after kids or single your s..t out of luck. Not great.

The kiwi dream was that you work hard, in normal jobs it could be manufacturing, save some money, and then buy a quarter acre section and house. Most people could do this. But now you have to earn 90k before you can get on the ladder and save for years for a deposit, if your lucky.

NZ seems to me as if its gone backwards, and its getting worse, what kind of country do we have. I lived in London where house prices are high, but their was a population of 8 millionish in a small space. Plus wages are high if you can get it. In NZ we have a country the size of UK and a small city Auckland where some house prices are comparable to London. It makes me despair, for me, my kids and New Zealanders on a whole.

Im doing what I can to get ahead, but the problem with this are the goal posts keep shifting and house prices keep growing quickly. Not everyone is putting their eggs into the property basket. I have a business to run.

Auckland is becoming too expensive to live in now so we have been looking at sunshine coast, as there are some good houses with swimming pools, at good prices. I dont want to leave family, but life in Auckland is becoming a burden (11 dollars a beer, which you cant afford because 50% of your income goes to mortgage, rest on bills). I preferred life when average income was $30K and beer was $2. You need to earn 6 figures to be average and afford a beer now. Who would have thought that, and thats called progress.

I bring glad tidings swapcrate! Lion Brown beer (Not to be confused with Lion Red or DB Double Brown) can be bought for $1.44 a can. Large 440ml cans too. This is a great beer and a Kiwi classic, kind of a lager/ale and very drinkable. Was the beer of my youth which has recently returned.

I just did a quick search of TradeMe and you can buy places in Papakura, Pukekohe, Manurewa, Tuakau, Wellsford and so on for around 400K. This will cost someone around the same as rent if you have a reasonable deposit.

Thanks for helping find me somewhere to live, I will tell the wife, someone on the internet is helping me out. Im originally from Waiuku so I know my way around thank you. Especially Manurewa/Papakura/Pukekohe, Im a counties manukau supporter. So may know more then you.

Thanks also finding me what kind of beer I can drink as well, never thought to go to the bottle store before, soon I will be brewing hooch, and moonshine, I hear pure alcohol is great as well. So I suppose craft beers out ay.

Mate are for real (I wont tell you what Im actually thinking), your trying to tell me where I should live and what I should drink , and that for 100K all I can do is go backwards to where I was as a child there is no hope in dreaming for a better life, and have a nice cold beer on the waterfront when I want to have one. Dont get me wrong I love Waiuku, but I live in Auckland now.

I think Australia is looking the better option, swimming pool, and and nice style of life. Im trying to start up a company, if the NZ government doesnt want businesses in Auckland or NZ created by NZers, employing NZers then its going the right way about it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.