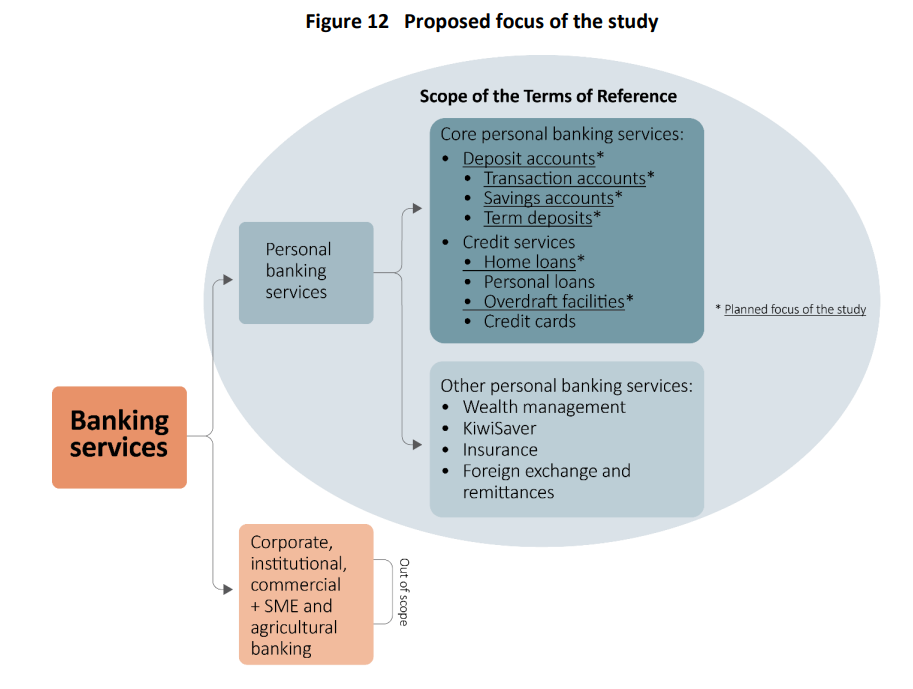

At first blush the Commerce Commission's confirmation its market study into retail banking competition will focus on deposit accounts and home loans, with many other banking products and services ignored or getting a cursory look, is underwhelming.

As interest.co.nz's borrowing and deposit comparison pages demonstrate, there's a good number of financial institutions offering both deposits and home loans in New Zealand. Arguably, these are the most competitive areas of the NZ banking market.

That said, there's certainly room for improvement for both borrowers and savers. And even though it's spelling out the obvious in its preliminary issues paper with the sentence below, the Commission is right to look at this relationship.

"We are interested in the dynamic between the interest rates charged for lending and interest rates paid for deposits."

I mean who, even those with merely a cursory interest in or need for banking, deposits or loans, isn't interested in that?

Furthermore the Commission will; "seek to understand how banks make their interest rate decisions in respect of home loans and deposits."

This is at the very least a useful public service exercise as these decisions aren't well understood by many New Zealanders.

Unprecedented probe with cross selling in sights

And however cynical you are about this market study, the Commission also provides good context on just how significant it is. Although it has previously considered competition in the banking sector in the context of specific merger decisions, this market study is the first time it'll consider and evaluate in detail whether competition in personal banking is promoting outcomes beneficial to the NZ public.

"This study provides the first opportunity in New Zealand’s history to consider and evaluate in-depth whether competition in personal banking is promoting outcomes that benefit New Zealand consumers over the long term. Competition drives businesses to innovate and be more efficient, and to offer New Zealanders greater value and more choice. It is an effective competitive process that ensures prices and profits are not too high for too long," the Commission's preliminary issues paper says.

The competition watchdog is also pledging to shine a light on an old chestnut of banking, cross selling or bundling.

"Services are ‘tied’ if the purchase of one service is conditional on also purchasing another service. Bundling refers to the practice of selling two services together. Tying and bundling can provide benefits to consumers, but in some circumstances can make it harder for consumers to switch, reducing competitive constraint and leading to worse outcomes overall," the Commission says.

"We propose to analyse the extent tying and bundling strategies may be directed at consumers, and the extent to which these strategies may impact consumers’ ability to make informed choices about the personal banking services they acquire."

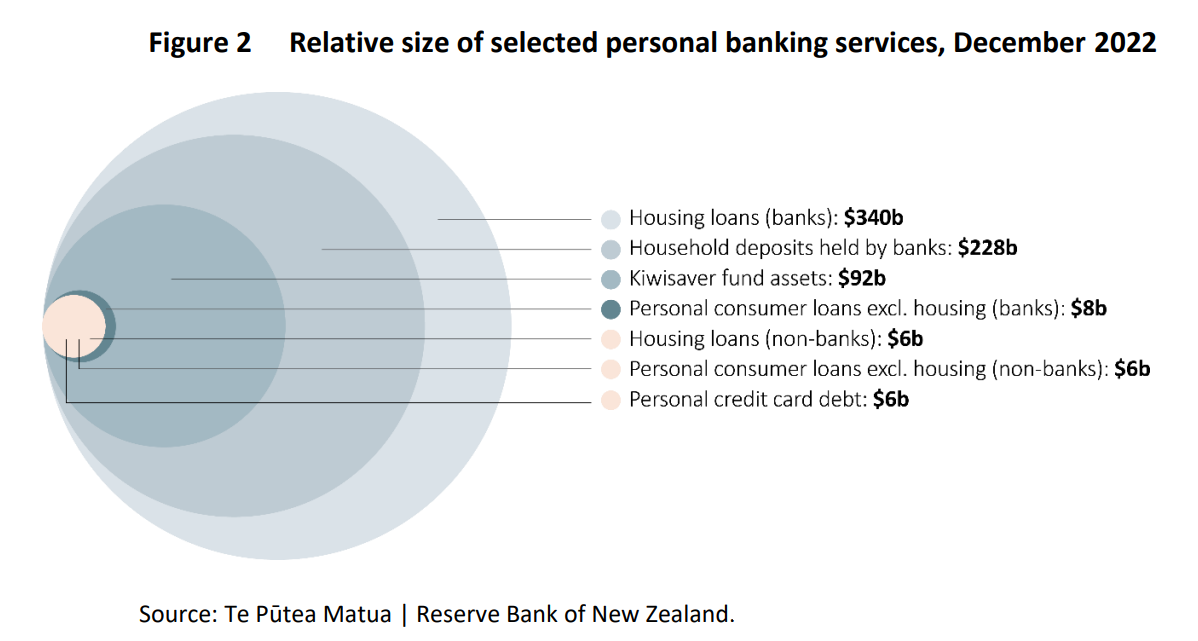

As figure two below shows, deposit accounts - transaction, savings, term deposits and overdraft facilities, are where the bulk of New Zealanders' money within the banking system is held, and home loans are easily the biggest source of our debt.

Following instructions

The Commission is also, by and large, following the direction given to it by the Government via Minister of Commerce and Consumer Affairs Duncan Webb. Unfortunately this means corporate, institutional, commercial, small and medium sized business (SME) and agricultural banking are excluded from the market study. Nor are credit cards, unfortunately, likely to get much of a look in.

And other areas may only get a cursory look.

"In keeping with the Minister’s intended focus for the study, we do not propose to focus on insurance, KiwiSaver, wealth management and financial advice, or foreign exchange," the Commission says.

"We are also not proposing to focus closely on credit cards, personal loans generally, or other types of personal banking service that are not deposit accounts (including overdraft facilities) and home loans. Although these out of focus services fall within the broad definition of personal banking services, focusing on them would materially increase the scope of the study due to the extra markets, market participants and (in the case of KiwiSaver) other regulatory regimes involved."

"In identifying the proposed focus of the study we have also taken into account that supply of home loans appears to be particularly concentrated compared to, for example, personal loans generally," says the Commission.

"We may, however, consider other personal banking services to the extent that they are relevant to understanding competition for the services we are focusing on. For example: we intend to consider the extent to which other services (such as insurance) may be bundled with or tied to deposit accounts or home loans; and some aspects of our analysis, such as seeking to understand bank financial performance and the nature of competition between personal banking service providers, may require us to take a high-level view of firms’ activities across a broad range of services."

In deciding to focus on deposit accounts and home loans, the Commission says it considered how best to promote the long-term benefit of consumers, and what's in the public interest, including how these concepts were articulated by Cabinet.

"Our intent to focus on deposit accounts and home loans is informed by our understanding that those services: are a focal point for competition within the personal banking sector; are relevant to a large proportion of New Zealanders (deposit accounts), or are of particular significance to New Zealanders who acquire them (home loans); and where effective competition is most likely to deliver long-term benefits for the most consumers; are of strategic importance to the New Zealand economy or businesses or of significant importance to consumers; and are where close consideration is likely to reveal any factors affecting competition for the supply or acquisition of personal banking services," the Commission says.

Transaction accounts & cross selling opportunities

An interesting aspect of the Commission zeroing in on deposit accounts is that it highlights their "important role in how banks attract customers and sell, or cross-sell, other personal banking services."

The Commission notes the role of transaction accounts in retail banking competition was probed by Britain's Financial Conduct Authority (FCA) in a 2018 report.

"The report described the benefits that the major banks enjoy as a result of their size and established presence, and the competition and consumer outcomes that flow from those benefits. Its findings largely related to the large number of PCAs [personal current accounts] of the major banks, which provide significant funding benefits compared with smaller banks, as well as cross-selling opportunities, and income from fees and charges, particularly overdraft fees."

"Engaged consumers that actively search the market for the best offers and switch providers in response to that offer can play an important role in the competitive process," the Commission says.

Spotlight on switching banks

The Commission goes on to say, however, there are some indications that searching for, and switching account providers may be difficult.

"Features of some deposit accounts, particularly transaction accounts, may mean switching providers is complicated. For example, transaction, income, and payment card arrangements may need to be re-established."

The competition watchdog notes the bank-owned Payments NZ offers an account and recurring payment transfer service to facilitate switching banks. However, this does not appear to overcome all transaction costs with the Commission citing the example of there being a five-day timeframe for the service, incoming payments not being redirected, and customers' need to change account numbers remaining.

"We are planning to investigate the extent to which customers engage with the market for transaction accounts. Our current understanding is that, as a generalisation, it may be that it is significant life events, such as taking out a first loan, or starting wage earning, buying a house, marriage or separation, that prompt consideration of banking arrangements and the prospect of switching providers and that overall switching activity may be relatively limited, although some consumers will multi-bank," the Commission says.

"If there is a tendency towards consumer inertia, this could result in significant incumbency advantages."

It goes on to say that consumers may face barriers to selecting a transaction account that best meets their needs. It notes Britain's Competition & Markets Authority (CMA) found customers’ ability to access information and identify the best-value account for their needs is likely to be impaired by the complexity involved in comparing different personal current account pricing structures. The CMA also found consumers need to be able to access and assess their expected account usage in order to choose the best-value personal current account product.

"These findings, if applicable in New Zealand, suggest there could be material challenges for consumers in trying to assess different options."

Home loans 'particularly profitable portfolios for banks'

In terms of competition for home loans, the Commission is also taking some pointers from overseas. Studies by the Australian Competition and Consumer Commission have highlighted a number of competition issues that have dampened price competition for home loans, it says. These include; unnecessarily high search costs created by opaque discretionary discounting by some lenders, unnecessarily difficult and lengthy discharge process for switching between lenders, and the existence of gaps between prices paid, interest, for new home loans relative to existing home loans.

"Home loan interest rates have significant effects on household budgets. For those households with a home loan, around 32% of households in 2021, repayments are a significant, if not the household’s largest, ongoing expenditure. Home loan borrowing costs are likely to also flow through to the cost of rent for non-homeowners, at least in part; and overseas studies have identified home loans as being particularly profitable portfolios for banks," the Commission says.

"We expect that focusing on home loans will help to identify and better understand any factors potentially affecting competition in personal banking. Our initial understanding is that competition for home loan customers is a central arena for retail banking competition more generally, and has an important role in attracting and retaining personal banking customers. We are also aware that mortgage brokers play an important role in matching home loan providers with consumers, and we intend to study the role they play and the impact they may have on competition."

Meanwhile, the Commission says analysis and potential factors affecting competition it plans to explore includes: The nature of competition, including how competition is working for different population groups; the conditions for entry and expansion in the sector; the factors affecting consumers’ ability to search for, and switch to, alternative providers; and impediments to disruption and innovation in the sector. It also plans to explore the effect of ownership relationships on innovation by NZ banks.

"Some initial questions we will seek to answer include: How do banks compete to establish relationships with their customers? Does this differ by the size of the bank, large or small, or the type of customer? How do banks compete to provide different types of services?"

The Commission expects to focus on understanding banks’ strategies for acquiring and retaining personal banking customers, including understanding how banks decide the set of service offerings in order to meet customers’ evolving banking needs over their lifetimes.

"We will seek to understand trends in prices for home loans in New Zealand, including whether new customers get better rates than existing customers, the role of mortgage brokers, and whether price competition is clear and transparent, or pricing comparisons are made harder by discretionary discounting from advertised lending rates."

"We also intend to examine whether there are tools in the market to support consumers in their search," the Commission says.

"We propose to undertake a detailed assessment of the conditions of entry and expansion in the banking sector in New Zealand. Our preliminary understanding is that low switching rates may be a barrier to expansion and that the regulatory landscape (for example, capital requirements) may also have an impact, particularly for smaller providers of personal banking services for which the same set of regulatory requirements may impose proportionally greater compliance costs. We intend to initially focus our analysis on these conditions of entry and expansion."

'Comprehensive consumer survey' promised

The Commission is also pledging a "comprehensive consumer survey" on a large, representative sample of personal banking customers. The survey, it says, will aim to obtain descriptive statistics of personal banking customers, the services they acquire, and the extent to which they engage with the market in managing their personal banking needs.

"The survey will seek to understand consumers’ perceptions of the potential benefits and costs associated with switching between providers."

The preliminary issues paper has a short turn around with feedback sought by 4pm on Thursday September 7. That's less than a month away.

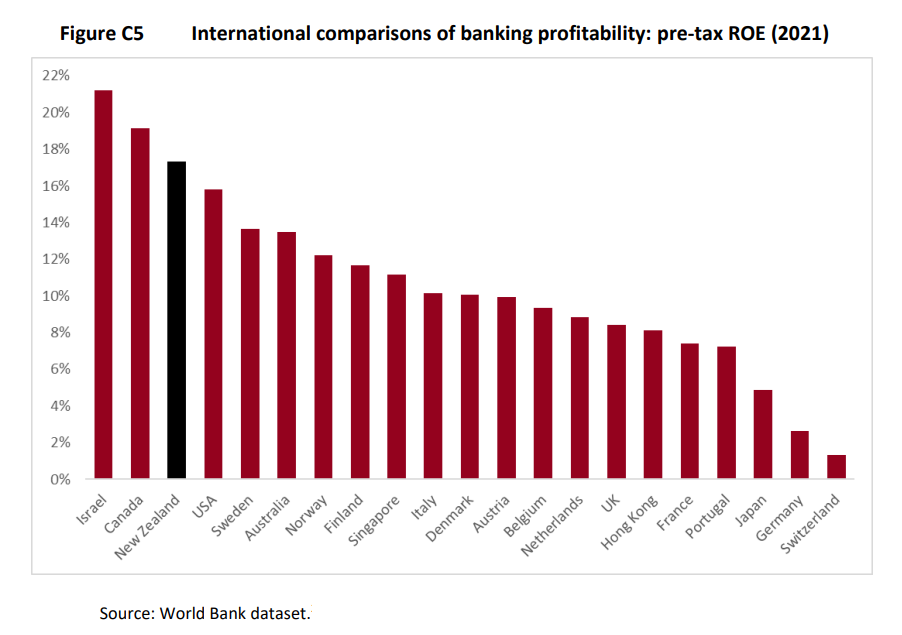

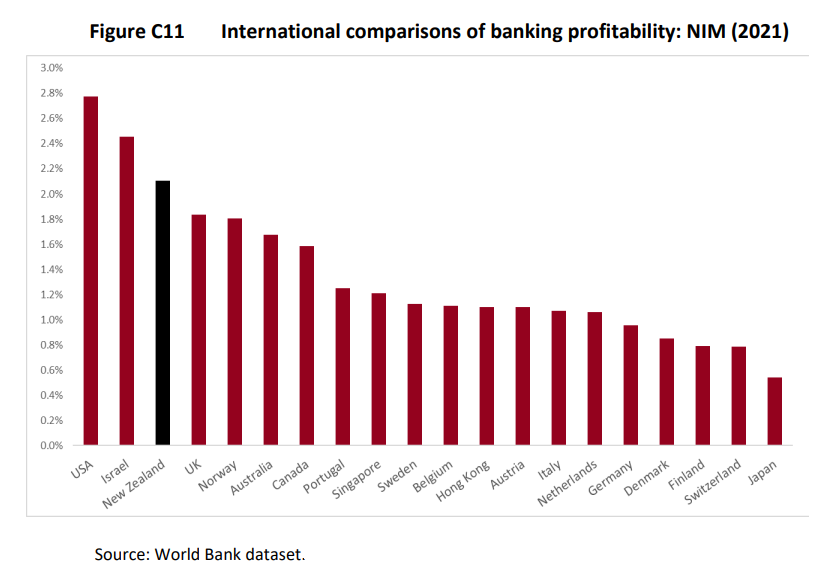

It has been well canvassed for years, including on interest.co.nz, that NZ's big banks are very profitable by international standards. We also know that NZ has been free of bank collapses over recent decades, albeit finance companies fell like dominos in the Global Financial Crisis era.

In terms of profitability the Commission says it'll focus on return on equity (ROE), return on assets and net interest margins (NIM). See more on ROE and NIM comparisons in the charts below.

Weighing up the direction the Commission's preliminary paper is pointing in, there could ultimately be some easy wins for the consumer here. They're likely to be the low hanging fruit and incremental. We're talking about evolutionary not revolutionary change.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.