By Gareth Vaughan

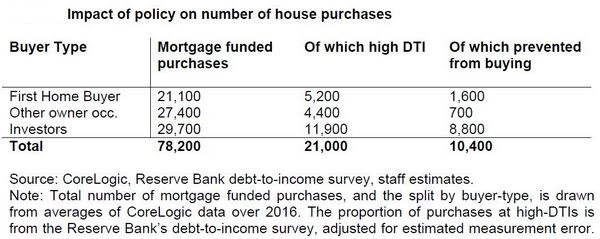

Restricting the debt to income (DTI) ratio of some mortgage borrowers could prevent about 10,000 borrowers from buying a house, reduce house sales volumes by about 9%, trim house prices and credit growth by up to 5%, and shave 0.1%, or $260 million, off Gross Domestic Product, the Reserve Bank says.

These estimates are included in the Reserve Bank's consultation paper Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand. Including a cost-benefit analysis showing benefits outweigh costs with net benefits estimated at just under 0.1% of GDP per annum for the period over which the tool is used, it was issued on Thursday. The Reserve Bank is calling for submissions by August 18.

The Reserve Bank's analysis and estimates, and possibly even its views on the scale of the issue it's attempting to address, are likely to be met with some scepticism given the central bank itself says about a quarter of the high DTI loans featured in its data are reported "erroneously" by banks. This means the Reserve Bank's DTI data currently contains "artificially high results."

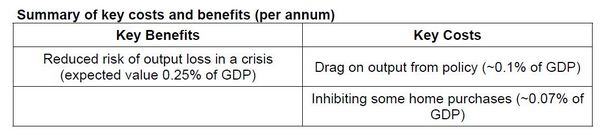

The key benefit of a DTI tool would be reducing the costs of a housing and financial crisis. The main costs would stem from a reduction in short-term economic activity, and the cost to some potential homebuyers of having to delay house purchases. (See more in the table at the foot of this article).

The Reserve Bank says any DTI tool would apply to both investors and owner-occupiers. It reiterates that, whilst it's "desirable" to add a DTI tool to its macro-prudential toolkit, it doesn't see a case for actual implementation at this stage.

"If actual policy implementation was ever proposed there would be a further detailed consultation on the specific terms of the policy proposal, including a Regulatory Impact Statement," the Reserve Bank says.

The prudential regulator of the country's trading banks argues DTI restrictions would reduce the risk of a significant rise in mortgage defaults during a severe economic downturn, mitigate the potential amplification of a downturn due to economic stress and increased house listings among high DTI households, and "lean against" periods of rapid house price and credit growth thus reducing the probability and magnitude of a sharp correction in house prices.

The Reserve Bank says a DTI policy would be introduced at a time when it judged that house price appreciation and high DTIs created a risk of crisis.

"So we consider 5%, one crisis every 20 years, is a conservative baseline risk of housing crisis in an environment that RBNZ would apply a DTI policy," the Reserve Bank says.

A limit on the total debt of the borrower as a ratio to gross income

It says a DTI restriction would be likely to take the form of a limit on the total debt of the borrower as a ratio to gross income (TDTI).

"The total debt of the borrower would include other debts at the bank and other material debts, such as mortgages on other properties at other banks. Banks would be expected, as now, to inquire as to the other debts of borrowers and borrowers would be expected to provide this information to the bank. The Reserve Bank might also periodically scrutinise the approach taken by banks to verify this information when supplied by the borrower," the Reserve Bank says.

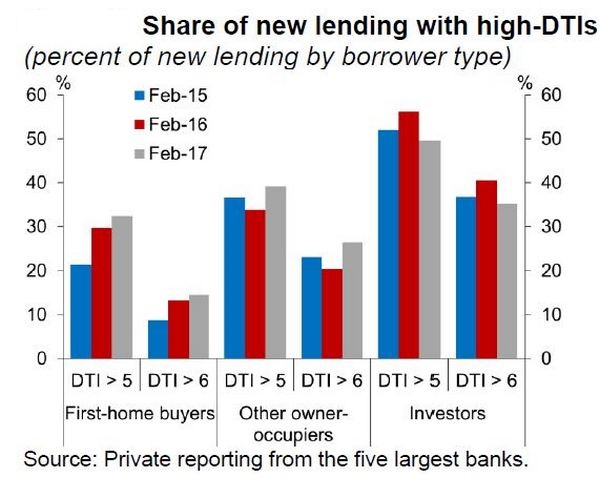

Under a DTI policy banks would be required to maintain their share of non-exempt mortgage lending at a DTI exceeding, say five, to, say, below 20%. Thus a "speed limit" would be put in place, as with the loan-to-value ratio restrictions on residential mortgage lending. The Reserve Bank says the current share of high-DTI lending is reported at about 45%, although it thinks this is an over-estimate that will drop as banks improve their reporting systems.

"Currently the data suggests around 27% of lending is above TDTI six and around a further 13% is between TDTI five and six. A rule that limited new lending to borrowers with total debt to income ratios above five, to no more than 20% of new lending, would thus significantly reduce the amount of high TDTI lending that was possible, even assuming, as we do, around a quarter of the high DTI loans in our data are reported erroneously at present."

"This is only an illustrative calibration, and any actual policy could vary from this. For example, the speed limit and level designated as ‘high-TDTI’ could vary based on the circumstances prevailing at the time, and the Reserve Bank’s ongoing assessment of the TDTI data and market risks. The rule could potentially take a different form, e.g. a limit on debt service ratios, but our current thinking is that a TDTI speed limit would offer the best trade-off between effectiveness and simplicity," the Reserve Bank says.

Exemptions

There would be exemptions similar to those available within the LVR restriction policy. For example, exemptions for new builds and for owner-occupiers wanting to buy and occupy a "relatively low-priced" home. The exemptions would aim to eliminate unintended consequences.

"The limit would apply to standard residential mortgages as defined in Reserve Bank’s capital adequacy framework. This includes some loans secured by residential mortgage that fund businesses, but not some larger business loans. E.g. a very large loan where the owner’s home is used as security but is not the key factor behind the lending decision. It does not include reverse mortgages."

"The Reserve Bank considers that an exemption to a TDTI policy that facilitated people becoming or remaining homeowners might not have a serious impact on the effectiveness of any policy, and could reduce the risk of the policy impeding first home buyers and labour mobility. For example, an exemption could allow homes to be purchased for owner-occupation if their value was below the ‘cap’ for Housing New Zealand’s homestart programme, [which is] currently $600,000 in Auckland, $400,000 to $500,000 elsewhere. This is the example we have modelled, but there would be alternatives: for example, the policy could allow first home buyers slightly higher TDTIs. The aim would be to diminish the welfare costs of the policy, as well as recognising that first home buyers had relatively low default rates in the Irish downturn experience," the Reserve Bank says.

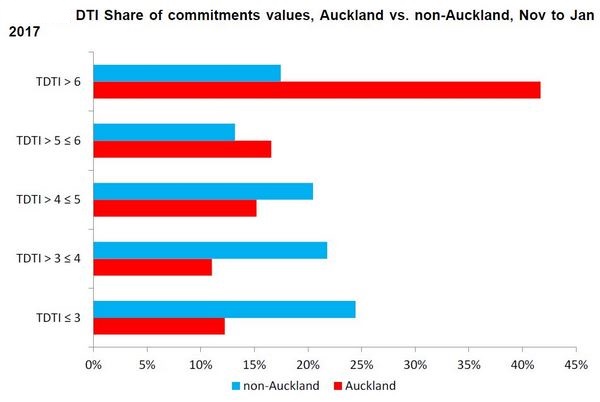

Since last October the Reserve Bank says it has been obtaining "more detailed data" from banks showing the total debt to income ratios of borrowers with "a clearer split" between investors and owner occupiers, and between Auckland borrowers and borrowers elsewhere in the country. This data is, however, described as "preliminary," with the Reserve Bank "continuing to engage with banks to understand their reporting standards and improve the consistency in data methodology."

'Artificially high results'

The Reserve Bank says total debt to income ratios should include debts a bank's borrowers have at other financial institutions, but some banks have difficulty reporting this comprehensively.

"Some banks also report that they do not necessarily capture all sources of borrower income if the borrower has demonstrated enough income to pass the servicing test. Also, some banks have system problems which mean they are unable to capture all the income details used to pass the servicing test when calculating total debt to income ratios. These factors appear to lead to artificially high results."

"As our data is improved and we understand cases...better, the share of high-DTI lending in the data is likely to decline. To some degree, these issues may disproportionately affect investor lending, since the systems used to store data on those customers are often more complicated reflecting the complex relationships that sometimes exist within groups of related borrowers," the Reserve Bank says.

"However, we are confident in the conclusion that New Zealand DTIs are relatively high...Given the international evidence in the previous section that high DTIs are likely to increase default risk in a downturn, we consider this a policy concern."

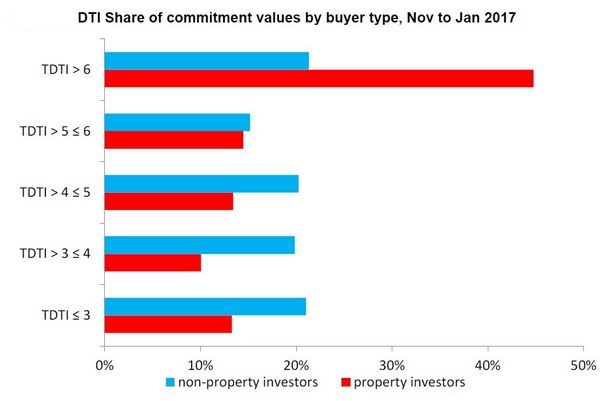

The Reserve Bank says that over the three months to January, about 60% of the new property investor lending across the big five banks was at a DTI of more than five, compared to 37% from owner-occupiers.

"Indicatively, our work suggests that around 2000 owner-occupiers and 9000 investors might be prevented from purchasing each year. The relatively high number of investor purchases that are constrained reflects (i) a greater share of high DTI lending than for owner-occupiers (ii) more limited ability to claim exemptions. The policy would also likely constrain some of the 160,000 or so top-up loans that occur each year, and we estimate that around 14,000 top-up loans could be constrained assuming that the limit binds roughly proportionately on top-ups and purchases."

'No significant impacts on rents'

The Reserve Bank argues DTI restrictions wouldn't have a significant impact on rents. Even though DTI limit would be likely to reduce the number of rental properties over time because landlords are significantly more likely to have high DTI loans, each additional property bought by an owner-occupier would reduce both the supply of and demand for rental properties.

"So the impact on rents should not be significant."

Based on an estimate that about 10,000 borrowers could be stopped from buying a house due to a DTI limit, and allowing for the likelihood some of them would be replaced by low-DTI buyers, this suggests house sales could fall by around 9% following the implementation of the policy, the Reserve Bank suggests. (See chart below).

"This could reduce house prices and credit growth by 2% to 5%."

"To proxy the effect of the DTI policy, we have assumed an increase in mortgage spreads, and a shock to house prices. Mortgage spreads increase by 10 basis points to 30 basis points while the policy is in place, based on an assumed additional cost of obtaining a high-DTI loan from other sources, such as non-bank lenders, of around 250 basis points, and around 8% of new borrowers being constrained by the policy. Additional judgement was used to ensure that house prices fall by around 2% to 5% in the first year after the policy is implemented," says the Reserve Bank.

"The simulation suggests that [economic] activity would decline by a peak of around 0.1% to 0.5% one year after the policy is implemented. Activity recovers fairly rapidly after the first year, as the impact on house price inflation dissipates and monetary policy eases. The average impact on GDP is around 0.05% to 0.24% per annum while the policy is in place, [which is] assumed to be four years). We adopt 0.1% of GDP as an expected macroeconomic cost, per year that the policy is expected to be in place, reflecting that GDP is likely to move above trend further out due to the policy being removed and the prolonged effects of the monetary policy easing."

The Reserve Bank says that if house prices accelerate again it could happen in an environment where interest rates remain low because of weak global economic growth and inflation.

"In this event, house prices would be rising even further relative to income, stretching affordability even further. In the Reserve Bank’s view, this would create risks of an eventual downturn similar to that seen in countries like the US and Ireland during the Global Financial Crisis," the Reserve Bank says.

The charts and tables below all come from the Reserve Bank consultation paper.

48 Comments

Is the aim to keep encouraging foreign & foreign-related property ownership, while reducing New Zealanders home ownership rates?

Hyperinflation of Auckland house prices won't be stopped by a RB imposed DTI. We are up against a global issue.

thats exactly the reason why we need a change of government that recognizes that there is a housing crisis and the average kiwi is hugely impacted by this, and a government that recognizes that Foreign ownership of our homes is again having a huge impact on the average kiwi

Yes totally agree that National need to go. We very much need a Foreign Buyers tax to prevent this false economy from happening again.

I absolutely agree that this party of elites has no interest in the financial well-being of the average Kiwi. What's worse is their so-called "capitalistic" policies are so short-sighted that any benefit to the general economy shall barely survive after the next cyclical recession.

George Bernard Shaw - A government that robs Peter to pay Paul can always depend on the support of Paul.

What makes it more interesting is when Paul is also in government - make it a self-licking ice-cream cone. So you have Paul robbing Peter to pay Paul. Certainly a less than ideal arrangement.

Agree. Election not too far away.

Except that Labour also doesn't support DTI's either, so a change in government wouldn't fix that.. Also their policies don't seem to offer any silver bullets and new ideas that I can see.

Any alternative will be better than the current one.. they have screwed us enough

Could have said the same thing 10 years ago though when the last government were voted out for pretty much the same reason. I don't want to vote them back in again, and this time as a far weaker version with an addon party to boot. I would almost prefer a combined National/ Labour party, as both quite centre anyway.

I'm not pro labour.. and agree with you about them 9 years ago.. it's a case of a change helps to reset things

DTI implementation will be great news for FHBs, from the RBNZ's estimates there will be 8800 more homes available for their purchase rather than being sold to highly-geared state-subsidised speculators.

RBNZ's reasons for delay are weak and timid, - it should be implemented now.

you will have the government smirk and says its a stupid tool to use

I agree Peri, however I would make one comment; can the RBNZ please be more specific when referring to DTI -should this mean debt to NET income ratio? Because clearly that is what FHB's have in their pocket to spend.I can recall banks telling me years ago when I was looking to borrow that it was on your gross earnings-Go figure!

Yes but I heard on the radio this morning the DTI for FHB would be 5x so if your on the average household income of about $70K thats a $350K "Affordable House". Please show me 8800 of these that exist.

Essentially with the current cost of housing, its impossible to set the DTI at a sensible figure for FHB to get a "House", they will have to consider buying an apartment.

Much like the rest of the world then, when the first housing purchase is usually a flat, even in non-urban areas.

NZ cities will intensify housing. They have to. Flats will become normal for FHB.

But 'not in my backyard'....

Yeah, and the rest of the world had those problems during their city intensification phases too. Still happened though.

They are already going in all over the place in Albany. They are all going in at the right place, right next to the major bus terminal. This is the common sense thing to do, head North and build satellite towns comprised exclusively of apartments with big green common areas and also put in a major bus transfer station with buses every 10 to 15 minutes.You need a 3 to 5 minute walk max to the bus that is 90% undercover all the way. Don't build shoeboxes, build a livable space with plenty of carparking and make it an attractive option to the now impossible quarter acre dream.

Fully agree. It makes sense, especially with the gradual movement of young people favouring 1/2 bedroom flats/apartments over McMansions. Personally, I'd much rather own and occupy a 2 bedroom 40/50m2 apartment with an adequate sized balcony than a 3 or 4 bedroom house on a quarter acre section.

The problem with that is there is a generation of 'young' people who have not had the opportunity to buy, but who also now are reaching the age where having a family etc either happens or it never will. That's a little difficult to do in a 50 square metre apartment.

What you will find, Carlos67, is that the DTI will affect house prices and (hopefully) bring everything down to affordable levels. Wasn't so long ago that you could pick up affordable homes for $350k or less. And by 'long ago' I meant a mere 2 years ago.

A good example from today would be this Papakura shack with an asking price of $500k - with the DTI I fully expect it to go back down to its July 2014 RV of $300k.

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

last sold in April 2015 for $386k, now back on the market (just after the 2 year brightline test, how convenient)

What you'll probably also need in conjunction with some limitation or disincentive on foreign purchases. This discussion of DTIs is seeing older Kiwis moaning about foreigners buying up all the land and houses from under them, something that didn't seem to matter when it was only young Kiwis being affected.

The $350k is the amount you can borrow not the maximum cost of the house. You still need a 20% deposit on top of that. So the house you can buy is worth $440k - which is easily obtainable everywhere other than Auckland. If you need to spend more than that, you would need to save up for a higher deposit.

If they had to build houses to a certain price, it is possible. The fact that building materials are so high in NZ, is an area that could allow the costs to come down, if he government starts to import materials diretly (eg similar to how pharmac works)

The government cannot directly fix the housing cost problem, what it can do is reduce demand through immigration control and this clearly would have a massive impact elsewhere in the economy or it would have been done already. DTI is a good idea as it starts to protect the banks from stupid people borrowing too much. You could also argue the banks are stupid to over extend their lending but it would appear everyone has got on the housing band wagon some 10 years ago and sensibility went out the window so now everyone needs to be controlled.

That's incorrect Carlos67. They could have introduced policy that would have limited housing price growth, but they elected to not do so because it would have been politically unfavorable. There's a big difference.

For example, we could have reduced immigration significantly when it became clear that we couldn't build as quickly as we could bring people in on planes. Did National do this? No - they did the opposite. Floodgates open..

They could have introduced DTI limits years ago to prevent banks/individuals over extending themselves - Did National do this? No - they allowed people to become excessively indebted.

They could have put restrictions on foreign purchases and limit foreign capital/debt from inflating house prices. Did National do this? No - they allowed foreigners to continue to purchase NZ properties - often with cheaper credit.

They could have introduced land tax to prevent investors from land banking. Did they do this - no they didn't.

So to argue the government cannot directly fix the housing cost problem is a bit of a lazy position to be honest. There was ample opportunity to regulate the issue - which would have limited the damage. But they chose (it was a choice) not to because Kiwis liked the capital gains.

National have made their bed - now it's time to sleep in it.

The government cannot introduce a policy to directly control house prices, your dreaming. Whats next a policy to control new car pricing ? its called a free market. If you want a system where the state has control over housing then move to Russia. Unfortunately all political decisions are weighed against popularity and essentially its about staying in the job. Like it or hate it, National are still ahead in the polls so its a case of looking after the majority and ignoring the minority.

Yup and eventually the minority will outnumber the majority and they'll vote for change. So long term - it's dumb, dumb, dumb....

So what's the point of having a government if they're not responsible for anything? (i.e. they can govern on mass immigration policies but have no responsibility for the outcomes of their actions?) Don't get it.

Put me in power now Carlos and I'll show you how a government can influence house prices.

My language used would shift sentiment and I'd followed that through with regulation... I'd openly acknowledge that we have a housing crisis and I'd also say's its most probably a bubble. That will unsettle market confidence. I'd stop immigration in it's tracks and what do you think will happen to demand? Negative gearing will go, subsidies will be reduced - darklodism would fall from favour. What do you think would happen to demand? As a country we'd probably fall into recession for a time - but that probably needs to happen - I mean how long can you live a lie for? It's just incredibly uncomfortable not addressing the elephant in the room.

So to claim a government can't introduce a policy to directly control house prices is just lazy. It's more that you just want to think that they can't - so you can justify their inaction.

No one has suggested outright control - that's a strawman.

If you want a system where the state has influenced the price of houses then look at the house you live in. Housing was affordable for earlier generations in part because of earlier government policies around land tax, government builds when there was a massive need (like now) and other devices such as cheap government leasehold land for new builds, and cheap Housing Corp loans.

A high rate of home ownership in NZ was achieved by the 1980s and early 90s in good part because of such earlier government efforts. Had these measures never taken place it's most likely you would not own a home today.

If you think you did it all on your own two feet without benefiting from any government actions (like you're advocating for young Kiwis today) you're sorely mistaken.

For the government to fix or find a solution, first has to accept that their is a crisis. For National government it is not a crisis but a sign of prosperity.

In a way they are correct as they see things from their and their friends perspective who are benfiting by this so called prosperity and who cares about the country and its people.

I too am with vote for change.

Anything in extreme is bad.

Government that turns a blind eye to the voice of the people should go.

9 years of power makes them feel invincible. Proud and arrogant behavior will lead to their downfall.

I agree IO, this election will be the most important one in ages.

Support the Status quo (stupid prices due to factors outlined above) v.s. protecting the averageman wage earner born/earning/contributing to society in NZ.

Seems an easy decision.

If you put in DTI's then foreign buyers really will walk over you, they are not a problem now but wait until you screw all kiwis over with DTI, not only will foreigners win but the rich will remain richer and even more powerful than before

Yeah, but young Kiwis have been complaining about that for a while and have been told to stop whining and let it be.

Maybe it's time for older Kiwis to say "Ok, yes, we probably need to put some limits or disincentives on foreign investment".

Indeed there should be some control over who is allowed to buy houses in New Zealand, whether it is a complete block or tax disincentive can be argued.

A DTI of 5 (or less) is necessary to rebalance housing prices and would significantly benefit society, they should also remove the current tax subsidy for negatively geared investors which will help to accelerate the rebalance.

Both Labour and National should include these elements in their housing manifesto's then it won't matter who is in power as all of NZ will win.

Average joe on 80k a years is going to live where exactly in New Zealand, te puke?

Your average Joe is in the top 20% of income earners,

http://www.stats.govt.nz/Census/2013-census/profile-and-summary-reports…

2013 figures, but I don't think things have changed that much.

I was looking at some housing affordability videos yesterday of John Key and saw this one from July last year where John rejected reducing housing/infrastructure demand by reducing the immigration boom, instead John demanded/pleaded/begged the Reserve Bank to introduce loan to value ratios for investors.

https://www.youtube.com/watch?v=AvDiJIH5fh8

Which the Reserve Bank duly complied with in its September announcement http://www.rbnz.govt.nz/news/2016/09/reserve-bank-confirms-nationwide--…

I think it is interesting that in the 2000s to control inflation, a housing bubble and immigration boom the Reserve Bank ratcheted up interest rates to 10%? just before the GFC -which actually crashed the economy before the GFC really put the boot in.

Now in the 2010's to control a housing bubble and a immigration boom the Reserve Bank is ratcheting up ever more restrictive Macroprudential lending restrictions.

Surely what is needed is for governments to stop abdicating their responsibilities and address the root causes of the problem -excess demand from immigration, foreign investment, speculation.... and unresponsive housing supply?

But first you would have to acknowledge there is an issue - then take responsibility for it. The grown ups in this country aren't even at that stage yet which is a little concerning...

Yep you can't fix a problem if you deny that the problem exists.

{kind=link}

Funny.....

Third term blindness.

Not dissimilar to the blindness of the smacking legislation, which has done nothing to halt those that use violence as a parenting technique. Should have focused on increased penalties for assault on children.

Former Reserve Bank economist comments on this ratcheting up of Macroprudential restrictions here. https://croakingcassandra.com/2017/06/09/bank-capital-some-thoughts/#co…

He is not in favour and thinks the Reserve Bank is possibly overstepping its legal power.

Labour does not support DTIs for first home buyers;

First home buyers shouldn’t carry the can for National’s failed policies

The introduction of tighter limits on lending to first home buyers would see them paying the price for the National Party’s failure to recognise or fix the housing crisis, Labour’s Finance spokesperson Grant Robertson says.

“Nine years of denial and inaction by National have seen an ever-growing housing crisis. New Zealand now has the lowest home ownership rate in 66 years, our biggest city is one of the most unaffordable in the world and the flow-on effects are being felt through spiralling rents and increasing homelessness.

“In the face of this, the introduction of across-the-board debt to income ratios for home lending would punish first home buyers struggling to get into the housing market.

“Thousands of young New Zealanders would be shut out of the security of home ownership, and the fault would lie squarely at the door of the National Government.

“Labour does not support debt to income ratios for first home buyers. There may be scope to introduce limits that focused on speculators who are responsible for the vast bulk of high debt to income borrowing.

“Steven Joyce is hedging his bets on the imposition of these limits. He needs to tell New Zealanders if National is on the side of first home buyers or not. All the evidence of the last nine years shows that they are not.

“Only Labour has a comprehensive plan to start to fix the housing crisis by building more affordable homes and cracking down on speculators who are driving up prices,” says Grant Robertson.

What so you think voting Labour will somehow reduce current house prices by 50% and make them affordable for more people ? If Labour get in then nothing will change except what they will then call "Affordable". Last time I heard it was now up at $650K. Face the fact that the government cannot change the house prices now and move on, its the home owners that are in control of the pricing and we have all got pretty greedy selling them to offshore owners with plenty of cash.

Aha!! So is it Labour or is it National prepared to look at the whole business of selling houses to foreigners?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.