The Reserve Bank of New Zealand (RBNZ) warns it’s likely some insurers are becoming more reliant on their shareholders to keep them afloat if they suffer a major loss.

The RBNZ, in its latest six-monthly Financial Stability Report, says general and life insurers’ solvency margins have “stabilised at lower levels”.

While for some this could “point to greater sophistication” in the way they manage their capital, for others it could mean they’re relying on “shareholder support to maintain solvency margins in a period of material loss”.

The RBNZ explains: “In late 2015 and early 2016, aggregate insurer solvency margins in New Zealand fell, due to dividend payouts being in excess of profits. Profits reported in mid-to-late 2016 were stronger and, as a consequence, solvency margins appear to have stabilised at lower levels.”

For example, Sovereign Assurance’s solvency ratio has fallen from 129% in the 2015 financial year to 118% in the 2016 financial year. Nib NZ’s has dropped from 344% to 202%.

In the general insurance space, IAG New Zealand’s solvency ratio is down from 282% to 147% in FY16, Vero Insurance New Zealand’s from 180% to 157%, and Tower’s from from 225% to 210%.

Kaikoura to further impact solvency

The RBNZ recognises the 2016 reporting period doesn’t include costs for the Kaikoura earthquake, the Port Hills fires and several storms.

“These events are likely to have significantly reduced profits and to have lowered solvency margins in the sector. Affected insurers will be under operational pressure due to the high claims volumes from these events, as well as the remaining Canterbury earthquake claims and business as usual claims,” it says.

Tower’s 2017 half year results show this, with its solvency as at March 31 dropping to a point only $5.2 million above the RBNZ’s minimum requirement.

The regulator says: “The sequence of these recent events serves to remind all insurers of the need to have sufficient capital and reinsurance to cover a single very large catastrophe event (e.g. a major earthquake or pandemic), as well as to cover several smaller unexpected and unprovisioned losses occurring in a short period of time.”

While the RBNZ recognises there is “substantial uncertainly” around how much the Kaikoura quakes will cost, it says this expenses appears well within all insurers’ reinsurance limits.

“Compared with the Canterbury earthquakes, the insurance sector is much better positioned to absorb these costs due to significantly higher levels of reinsurance and capital.”

The RBNZ believes the total cost of the quake to both private insurers and the Crown will be between $3 billion and $6 billion, which is $2 billion more than industry estimates.

As at March 31, $260 million of claims had been paid. The bulk of claims relate to commercial property in Wellington.

Canterbury claims expense keeps rising

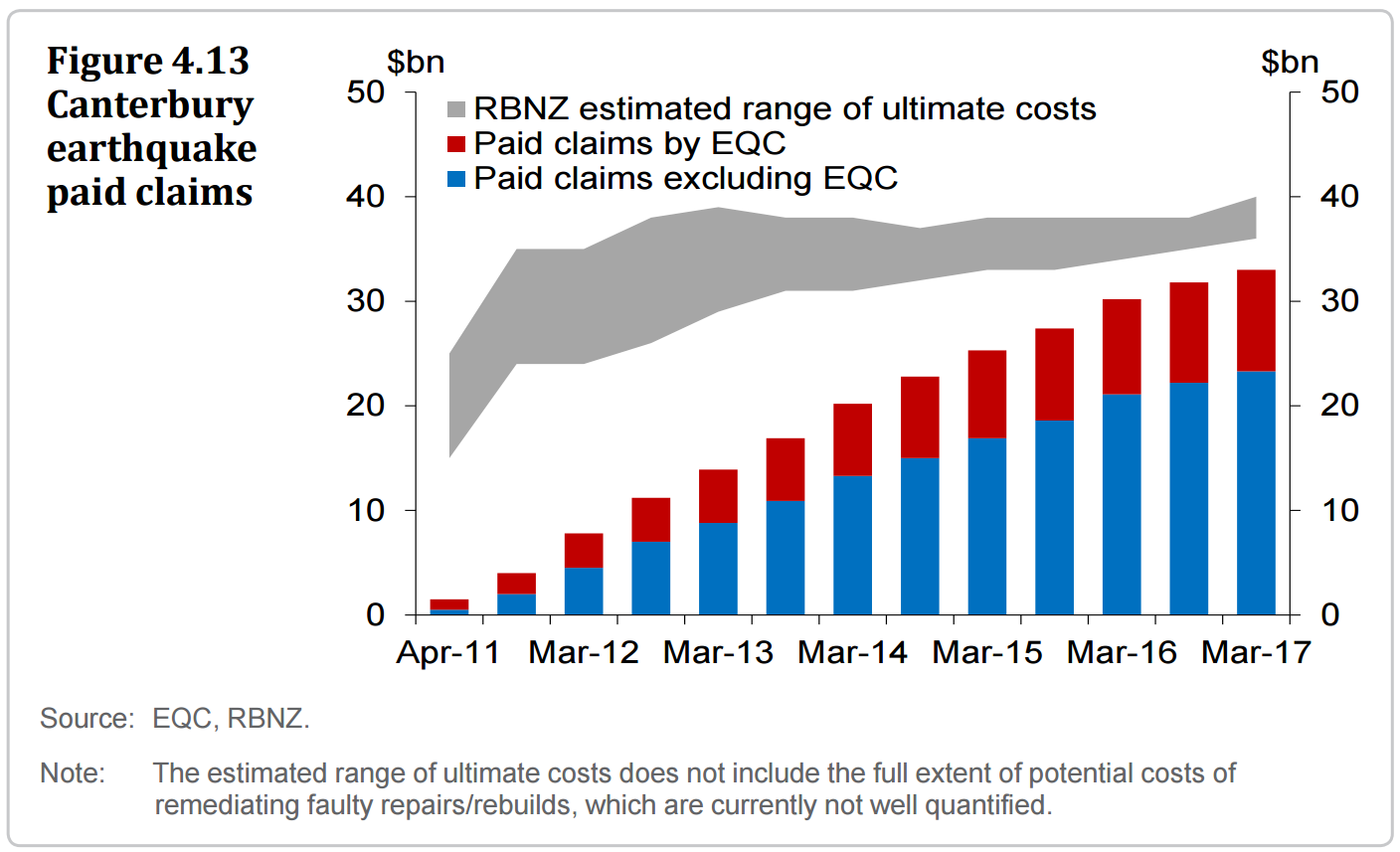

Turning to the 2010/11 Canterbury earthquakes, the Crown and private insurers have paid $33 billion of claims.

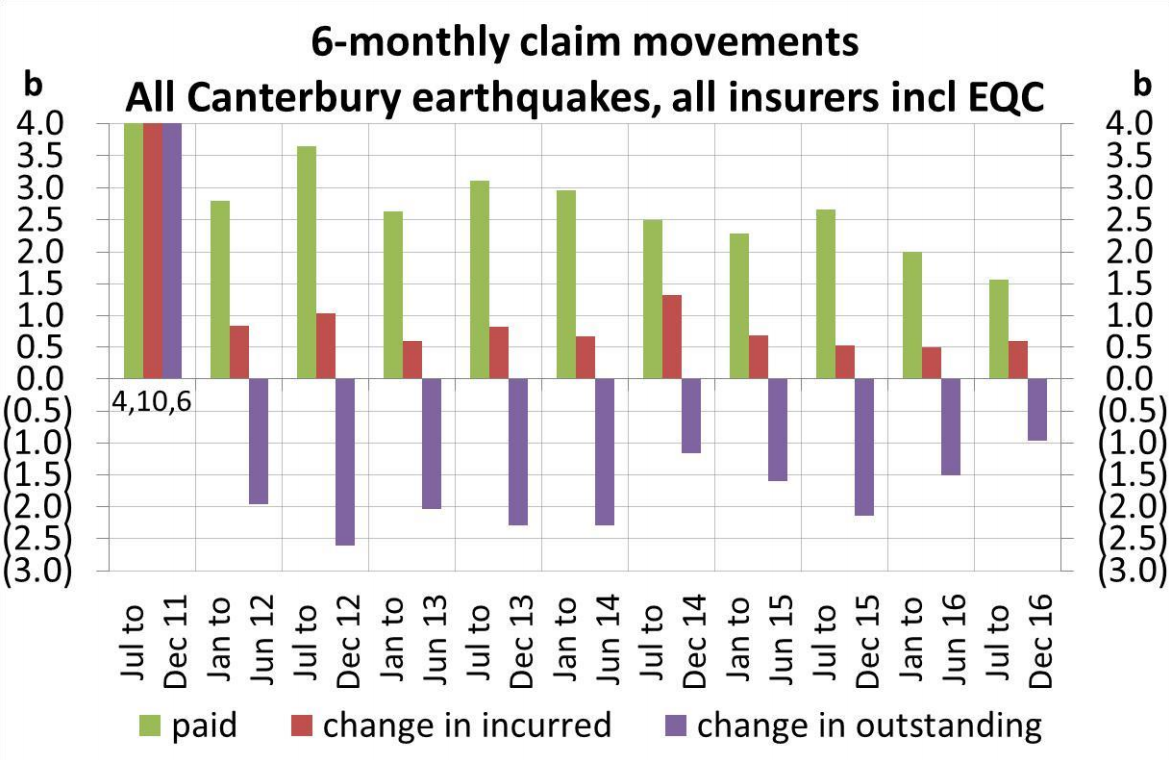

However the regulator warns: “The rate of payment of Canterbury earthquake claims has continued to slow as the remaining claims are generally the most complex and, in many cases, are in dispute or litigation."

As this RBNZ chart shows, “Insurers’ estimates of their claim costs have recently increased at almost the same rate as claim payments and we anticipate there will be further increases.”

The RBNZ says: “As a result, the Reserve Bank’s estimate for the ultimate claim costs, including EQC claims, has been revised up to around $36-40 billion (from $35-38 billion at the time of the last Report). The outstanding claims yet to be paid are estimated to be in the range of $3-7 billion.”

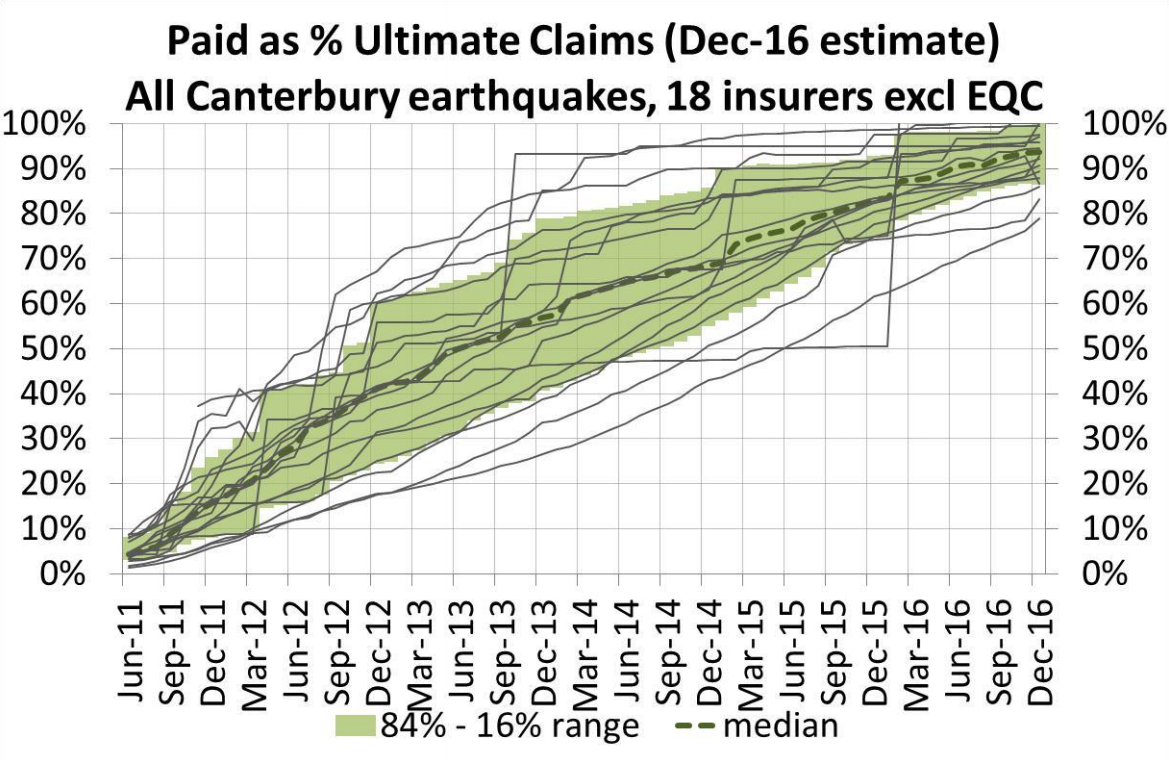

While most insurers have paid around 95% of claims (by value), this RBNZ chart shows there are still some that have only settled around 78-88%.

Risk management frameworks need to be ‘tailored’

Overall, the RBNZ is satisfied with the way insurers are assessing their exposures to catastrophic risks. Yet it notes: “Many insurers’ assessments of catastrophe risk are anchored to the solvency standards, for example, in terms of the types of catastrophe risks that they consider.

“It is important that risk management frameworks are tailored to each insurer’s own circumstances…”

Under the review of the Insurance Prudential Supervision Act, consideration is being given to enabling the RBNZ to “vary or alter prudential capital requirements in response to an insurer’s individual circumstances”.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.