Tower Insurance has effectively taken out a $30 million loan to prevent it dipping below the Reserve Bank’s (RBNZ) solvency requirements.

It confirms, in its 2017 Half Year results released today, that earlier this month it drew down $30 million on a $50 million “Cash Advance Facility Agreement” it has with BNZ.

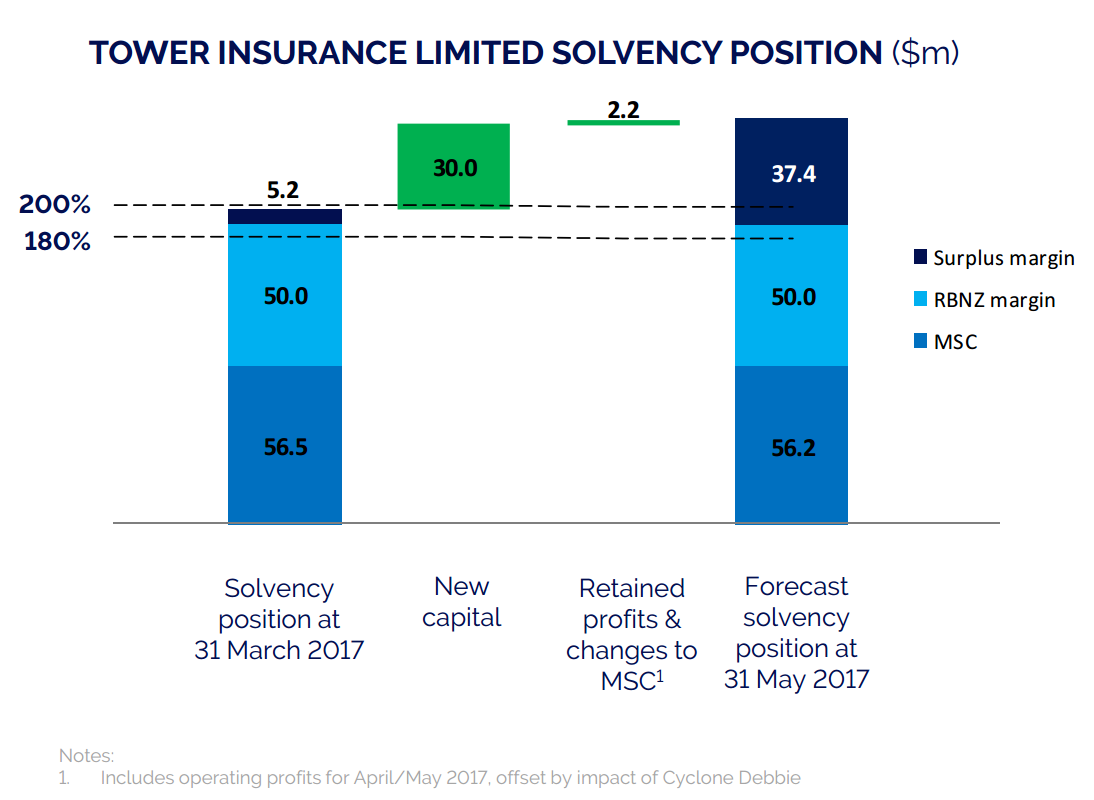

This has seen its surplus margin, or amount of capital above what the RBNZ requires it to have to keep its licence, increase from $5.2 million as at March 31, to a forecasted $37.4 million as at May 31. As at September 31, its surplus margin sat at $14.3 million.

Put another way, the cash advance has bolstered Tower’s solvency ratio to 255%, from 198% in March and 214% in September.

Note: MSC in the graph stands for Minimum Surplus Capital.

$9.8m sting for increased quake provisions

Tower says its solvency capital has taken a knock from its lingering 2010/11 Canterbury Earthquake hangover.

Its Appointed Actuary from Deloitte has asked it to further increase its provisions for the event, reducing its post-tax profit by $9.8 million. The Kaikoura Earthquake also had a $7.2 million impact on Tower's profit.

This has largely contributed toward Tower suffering an $8.2 million loss in the half year. It made an $8.7 million loss in the first half of 2016.

Deloitte advised Tower to increase its provisions due to the potential for it to receive more over-cap claims from the Earthquake Commission (EQC), the potential for increased litigation and litigation costs, and an increase in risk margins.

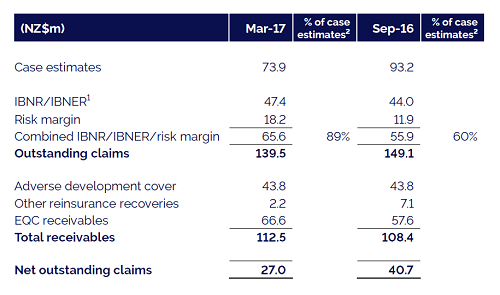

“The net result of the Appointed Actuary’s recommendations is that Tower’s IBNR [claims incurred but not reported] and risk margin allowance have increased from 60% to 89% of underlying case estimates,” Tower says.

$43.75m of reinsurance in dispute substantial in the scheme of things

Adding to the uncertainty, Tower has accounted for $43.8 million of reinsurance recoveries for the quakes, it doesn’t yet know whether it will receive.

It has recognised Adverse Development Cover (ADC) from Peak Re in its net claims expense calculations for the Canterbury earthquakes, even though it will begin arbitration with the reinsurer over a dispute around these funds later in the year.

While Tower says it’s confident it will recover all the money, it warns “the process of legal redress has risk and collection of the $43.75 million receivable cannot be certain”.

This figure is substantial given Tower’s forecast solvency position at May 31 is $143.6 million, with $37.4 million of this being above the RBNZ’s minimum required amount.

Tower’s dividend payments also continue to be suspended.

Potential takeover plans on hold pending ComCom decision

Tower says any equity raising it may do to “ensure a prudent level of capitalisation and solvency” is on hold until it knows whether the company will be sold to Canadian giant, Fairfax.

Shareholders will vote on Fairfax’s proposal to buy all of Tower’s shares for $1.17 each, at a yet to be determined date after the Commerce Commission on June 30 releases its decision on Suncorp’s non-binding indicative proposal to buy the shares for $1.30 each.

Tower says its board continues to “unanimously recommend” the Fairfax proposal, “in the absence of a superior offer”.

Salt Funds Management and ACC, which collectively hold 18.1% of Tower shares, have also committed to voting in favour of the Fairfax Proposal.

Yet Tower, in its results says: “There is considerable uncertainty surrounding the acquisition proposals from Fairfax and Suncorp.

“There is uncertainty around completion and timing of either acquisition proposal – specifically satisfaction of conditions precedent including regulatory approvals… and shareholder approval and in the case of the Suncorp proposal, any contractual agreement.”

Suncorp (or its New Zealand arm, Vero) has since February paid $1.30 and $1.40 per share to acquire 19.999% of Tower’s shares.

If it chooses to further increase its stake, it has to either make an official takeover bid and offer all shareholders the same share price, or enter into a scheme agreement like Fairfax has.

Tower’s Chairman, Michael Stiassny, at the company’s AGM in March said: "My job, as I see it in the very short term, is to ensure whomever is the party that is lucky enough to be successful here, has got to pay $1.40, or more than $1.40, for the shares in Tower before we will engage with you again.”

Tower's share price has today increased 3.11% to $1.16.

Its results show its underlying profit after tax was up 7.6% to $8.1 million in the half year compared to the same period last year.

Tower's gross written premium was down 0.2% to $145.8 million.

11 Comments

Based on the last dozen or so articles on this website this lot (Tower) is nothing but a third rate rotten circus, and who pays the ringmaster? Never ever enough re-insurance. Hate to say I told you so but I told you so! As the Australians would say "WHITE ANTED." $5 mill from insolvency. Would expect 10 of their outstanding EQ claims will eat that for breakfast.

A large part of the problem is that Tower, as a New Zealand company, does not have the backing of a robust group like IAG and Vero do. Tower is by no means the only insurer that's run out of reinsurance. IAG at the end of last year bought another $900 million of reinsurance for the quakes for example. Getting this ADC is costly stuff, but hasn't left IAG anywhere near as exposed as Tower. Nonetheless, I think it's fair to ask Tower's directors about the role their management has played in seeing the company come so close to essentially losing its licence. Its chairman has continuously attributed Tower's position to the failings of the EQC model.

Fair enough but if the lack of reinsurance was this critical it should have been, or worse perhaps it was, recognised and reacted to at a much earlier time. Actually think from a large number of contacts with EQ claimants that Tower would have saved itself millions on millions if it had correctly and fairly scoped EQ damage, particularly in the hardest hit suburbs, and quickly settled on rebuilds rather than trying to force settlement for repairs. Many of those rebuilds if costed in 2011 would be half of what they finally outturned as. As a matter of fact if you talk to the claimants just about all of Tower's claims that fell into this category were scoped and held to, invariably at $320 -390K to start with and therefore, as per you comment some months ago re the Young case " how many more cases like this can Tower stand" or something like that. Your question was well chosen, perceptive in truth!

You're right in saying Tower would've saved a lot if it settled these claims from the get go. As for whether or not the lack of reinsurance was known earlier... This is a good question. Stiassny may say no, as the flow of new over-cap claims from EQC has pushed claims costs up and up. But on the other hand - you'd think Tower would've had a better grasp on the situation.

Well there was ducking and draking all around, but it didn't really start in earnest until about 6 months after the Feb 2011 event and one would think if the gong hadn't already sounded, the June event certainly got the jungle drums well into earshot. There are many instances of Tower abetting with EQC to keep claims under cap and it obviously suited them to do so as they could say quite truthfully, that they had no actual liability for any claim still held by EQC. Tower it would seem decided to play for time in respect of cash flow, and embark on a policy of little more than attrition with the claimants. Delay, delay & delay again just like the highly ironic situation they find themselves inwith Peak - Re. Boot on the other foot, or better still, hoist by their own petard, to my mind that is, of course.

And who paid out past dividends that should have been retained to protect against this. Follow the money in reverse.

Oh well, time to look for another insurer (I used to be with AMI lol)..

Any recommendations on which of the alternatives suck the least? Or which one you want to doom by having me as a client?

Stiassny has extensive insolvency experience at Korda Mentha so has no credible excuse for his failure to recognize the potential for a serious cash problem which has been pretty obvious for 2/3 years and where has the regulator been - asleep on the job again??

You would have to wonder what collateral BNZ has required for this advance and/or what guarantor would be prepared to back it? A long time ago a company called Fortex got its bank loans confused with its receivables. Obviously that is not at all likely here but it would seem that there is more than a hint of similar desperation in trying to find cash flow to keep the operation going on a day to day basis. I am not an accountant and therefore I am completely baffled as to how the unknown quantity of the Peak re reinsurance can appear on the balance sheet as current assets. Please could some expert explain?????

The slow-moving train wreck that is Tower Insurance is painful to watch. The vulture that is Vero has descended from the updraft and is now sitting on the whitened branch of the tree that once was the third force and only foil to the oligopoly that’s the NZ general insurance market.

Tower’s problems don’t lie in claims going ‘over-cap’, i.e. past EQC’s $100,000 limit. Tower’s home insurance profile is on the margin with high-end homes and challenging architecture that were never likely to get away with lesser repairs. A quick look at the High Court Earthquake list gives a good feel for where Tower is at the moment, and it’s not pretty. These claims must range from $1m to $5m plus and there’s plenty of them.

Tower’s actuary, Deloitte, must be very peeved to have virtually doubled the risk margin on their latest estimate of Tower’s future claims liability on top of an almost 50% increase the incurred but not reported/enough reported ratio. Actuaries are smart data analysers and mathematicians but they’re only as good as the information they have to work with. It seems they’ve finally realised that they can no longer rely on what they’re being told by Tower. That Tower’s Chairman is no longer beating the “EQC’s at fault” drum tells me there has been some pointed conversations around the Board table over recent months!

So, after 6 years, Tower is down to the rump of their Canterbury EQ claims. They will be the most complex and expensive. If they’ve taken a $10m hit from the Kaikoura earthquake, and other claims account for, say, $4m, that leaves $60m for Canterbury earthquakes. At an average cost per claim of $1.5m that represents 40 claims remaining. I don’t think so! Perhaps Tower could release their latest actuarial report and let us make up our own minds?

On the face of it, while an increase in the solvency ratio percentage sounds OK, it’s the amount of dollars that represents which should be worrying everyone. It will just take another one or two adverse court decisions and Tower has nowhere to go other than into the arms of Vero. Vero gets its return from excising Tower’s overhead by simply absorbing it into their existing structure. Canada’s Fairfax Holdings, the other bidder, will know it doesn’t take much in the way of capital to set up on their own in NZ. Why would they take the risk of further contamination given this latest development?

The Commerce Commission (considering Vero’s bid) and the RBNZ (responsible for insurer solvency) are between a rock and a hard place. Let Tower fold or extend the Suncorp/IAG duopoly? Perhaps the answer lies in allowing Vero to buy Tower but addressing market imbalance by an immediate move to fully socialising disaster insurance via the current EQC review and providing a ‘Kíwibank’ insurance option for the mums & dads and small businesses of New Zealand.

Despite NZ’s risk exposures and scale issues there are ways to achieve this. It would complete a full circle which is so ironic given Tower’s origins and IAG’s ownership of the State brand.

There it is.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.