By Gareth Vaughan

New Zealand bank executives believe an ideal debt-to-income (DTI) ratio set by any Reserve Bank DTI tool should be between five and seven, according to KPMG's annual Financial Institutions Performance Survey (FIPS).

The report notes bank bosses are in unanimous agreement that the Reserve Bank's consideration of a DTI macro-prudential tool is happening too late given current DTI ratios have already topped levels that would have been considered ideal.

"According to executives an ideal DTI level would be in the range of five to seven. However, they say that most borrowers are already at levels of nine to 12," the FIPS report says.

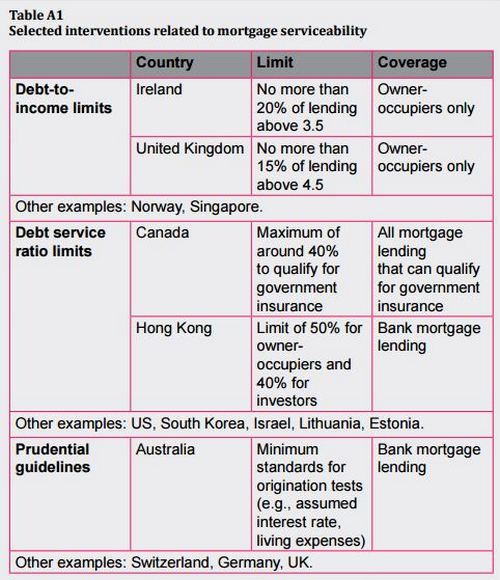

Both the Bank of England and the Central Bank of Ireland have introduced DTI ratios in recent years. The Bank of England's DTI ratio of 4.5 applies to no more than 15% of the total number of new mortgage loans for owner-occupiers. And for Irish banks the DTI limit of 3.5 should not be exceeded by more than 20% of the value of all housing loans for owner-occupier homes during an annual period.

The table below comes from the Reserve Bank's November 2016 Financial Stability Report.

In the November report the Reserve Bank said about one-third of new mortgage lending was being done at a DTI ratio of over 6.

The Reserve Bank says a macro-prudential DTI policy would allow it to limit the degree to which banks can reduce mortgage lending standards during periods of rising housing market risks, in order to protect financial system soundness. It also says an important feature of a DTI policy is that the borrowing capacity of constrained borrowers grows in line with their incomes.

"DTI policies can support financial stability by reducing the scale of mortgage defaults during a severe economic downturn. All else equal, borrowers with higher DTI ratios have less disposable income to draw on as a buffer to avoid defaulting on their mortgage, without selling their home, in a period of lost income or higher mortgage rates. Loan serviceability is a crucial determinant of probability of default, reflecting that many borrowers will attempt to service loans even if they are in a position of negative equity,' the Reserve Bank says.

"Forced house sales by high-DTI borrowers would likely amplify house price declines, impair the ability of banks to resolve distressed loans, and increase loss given default for banks. High-DTI households are also likely to reduce consumption more sharply during a severe downturn, in an attempt to continue servicing loans and increase precautionary savings."

New Zealand's debt-to-disposable-income ratio recently hit a record high of 167%. And household debt rose 8.7% last year to reach $246.877 billion. The latest Real Estate Institute of New Zealand figures show both the national and Auckland median house prices fell in January, hinting at a potential cooling of the hot housing market.

Sympathy for young families

Meanwhile, KPMG says NZ bank executives "sympathise" with young families, arguing the implementation of DTI restrictions could block them from buying a house. This, they suggest, could be an unintended social consequence the effect of which "might not have been adequately researched."

Bank executives also told KPMG any Reserve Bank DTI tool would need a clear, fair and explicit definition of what constitutes income and what constitutes debt, with this being something banks and the Reserve Bank could be at odds over.

The Government has kiboshed the Reserve Bank's attempts to get a DTI tool for the timebeing. Finance Minister Steven Joyce last week requested a cost-benefit analysis and public consultation before any decision is made on potentially adding a DTI tool to the prudential regulator's macro-prudential policy toolbox.

Joyce's decision came after the Reserve Bank requested a DTI tool be added to its Memorandum of Understanding on macro-prudential policy with the Minister of Finance.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

118 Comments

Bankers admit they cannot self regulate their lending! They will lend recklessly unless RBNZ prevents them from doing so!

“Executives are in unanimous agreement that the RBNZ’s consideration of DTI measures are taking place a bit late in the cycle”

"An ideal DTI level would be in the range of 5 to 7"

"Most borrowers are already at levels of 9 to 12"

What extraordinary and damning comments for the idea that banks will self-regulate their lending at prudent levels.

It is greed coupled with negligence on the part of lenders around the world. Since the big bailout packages were handed out to banks and insurance providers after the GFC, banks have been more reckless in their approach and their "too big to fail" attitude.

European banks like Commerzbank and Banca Monte dei Paschi di Siena have been showing signs of skepticism towards asset recapitalisation and restructuring in the hopes that the ECB would eventually give up and bail them out.

Totally agree with Peri - the CEOs basically saying they have been lending imprudently but don't want to allow the RBNZ to introduce a meaningful DTI lest it cause everything to unravel (on their watch at least).

The other nonsense spouted is that a DTI would somehow disadvantage first home buyers. Evidence suggests it is investors who are more highly geared relative to incomes so they would be hit more so. But of course it pays the CEOs to use FHBs as the victim rather than investors since this sells with politicians/media. In anycase the introduction of a DTI would almost certainly curb demand, across the board (assuming most buyers use NZ bank loans), this would make houses actually more affordable for FHBs.

Borrowers are at 9 to 12??!!! I'm assuming this is a reference to investors i.e. yields of 8-11% otherwise we are in big trouble when rates go up. Even 7x is too high. A $100k earner (say $75k after tax) could borrow $700k? Rates go to 8% and that's $56k pa servicing costs. Doesn't leave much for.....er.... anything.

Yeah, that bit is confusing as hell. Maybe they are using net incomes to calculate the DTIs? Playing with the mortgage calculator gives a monthly payment for a 30 year $900,000 loan of $4 560 or $54,720 a year. Good luck servicing that on $100,000 gross income. Hell it'd be quite a stretch on $100,000 net....

There are quite a few people in Australia that have 50% of net income going into a mortgage. Not sure how many do that here but it's way too high especially when interest rates are low.

I'm assuming you've used about 4.5% as the interest rate. Imagine the interest rate going up by 10% (of the current rate) and ending up at 4.95%. That would make repayments $4803 that's a scary increase. It would also only take an interest rate of 6.2% to make the payment exceed $5500 per month ($66000 per year). On $100k per year that doesn't leave a whole lot of money for food, clothing or rates.

50% net income to housing is crazy high for my money - I whinge and I'm only at 40% net on my income...

Yes I just ran with the 4.50% rate. If the interest rate go up to 10.6% (unlikely but not unimaginable) the repayments will go over $100k. What are the council rates and insurance premiums on a $1,1250,000 house in Auckland? If we guess a total of $10k total for both, mortgage payments +rates +insurance will be over $100 000 at a 9.5% interest rate. Maybe they have a big vege garden to live off?

You can pay way more then 50% of your income towards a mortgage you just have to pull your head in for years. Fact is there must already be a huge percentage of people paying more then 50% based on the average household income and the cost of housing. It really depends on the sort of person you are, not necessarily how much you earn. If you can control your spending and are a very practical person who can do anything then it keeps your expenses right down. I managed on 80% of my income going on the mortgage for a few years.

Yes thats net income, no point talking Gross, you never see the tax part ever again. You just make do from making sure your rubbish bag is packed down and full not half empty to buying your Levis jeans on Trade-Me for $17 delivered rather than $100 new. It helps if you can service your own car, paint your own house, do your own garden, clean your own gutters, the list goes on. Your expenses can be slashed if you have to. Also helps if your single because then you have total control of the outgoings.

and the same bankers are now claiming the ratio is higher and more risk, so what were their tests made up of and what were they reporting to the RBNZ during the health checks.

I suspect in a rampant market which they helped fuel with credit they could overlook things

RBNZ barely seem to understand what they are doing. We'll find out if their stress testing and checks and balances actually function soon enough. The banks are driven by bulk lending as the risk weighting on mortgages is low compared to other types of debt. RBNZ could have and should have changed that weighting as that forces more control over bank activities but as you have stated they are fueling house price increases.

In other news bank profits are up, actual risk to banks unknown.

Interest rates do not affect a Debt-to-Income ratio. As an interest rate is not debt or income. They would affect servicability, but that is another issue. Debt is fixed, income is (relatively) fixed based on the previous year's IR3, as banks request that info anyway. simple to implement. And the fact is, higher interest rates are no problem if the total debt is also reduced by a chunk.

Property investors with DTI of 9 or so is not a problem for Banks whatsoever, providing they are able to service the debt.

Owner occupiers with that sort of DTI on the other hand would be.

The truth of the matter is that property investors that are financially secure are less of a worry for Banks than owner occupiers and that is why Banks lend to them.

Investors will always have income coming in from rents whereas owner occupiers can lose their job and therefore their ability to service the debt.

Depends on each investors situation of course and there are many investors that will be flying close to the wind due to their tight margins.

that is why in a downturn banks reduce credit to investors first or charge them extra biases for loans.

you should change your name to one eyed landlord man

http://www.interest.co.nz/news/81953/anz-tightens-lending-criteria-rent…

http://www.abc.net.au/news/2015-05-18/investor-home-loans-tighten-as-re…

What if house prices drop? And the 'investor' is in negative equity? Everything still OK? And when the tenants leave and you can't find new tenants willing to pay the same rent? Still dandy?

No matter how you try justify it, a DTI of 9 for an investor is just plain reckless. The banks need to be pulled into line on this, and if the government won't support the RBNZ in its efforts to do so, we should elect a new government.

So if that happened, who would be at fault for letting this happen? 6.5% historically is still low. I remember when 8% was considered a low rate! You go from a 8% down to about 4%, and it effectively means people can afford to double their borrowing amount. eg So the house price doubles. Factor in that most property buyers are now 2 working people families, when 30 years ago, it was more likely that most were single working families. That effectively quadruples what people can afford to pay for a house vs 30-40 years ago.

Really? what regulation governs bank behaviour with respect to lending against property, manipulation of the market etc? The only stuff that I can think of occurred after the situation got well out of control. Banks are as guilty of the cause of the housing problem as the specuvestors because they were willing to continue to lend in an insane market. Essentially we invented our own "sub-prime" market. DTIs over 9 has to be exceedingly risky lending by any measure, and even 5 for many would be too.

Other commentors are correct in espousing peoples vulnerability to rising interest rates, and I strongly suspect TM2 is gilding his own lily

Banks are not at all guilty. They are doing exactly what they are incentivised to do in order to maximise return to their shareholders.

The problem lies in government (and by proxy the tax payer). The banks are incentivised to take unsustainable risk, underpinned by the expected probability and magnitude of the tax payer funded bailout that they will receive when they become insolvent. We are slightly more protected in NZ from this with the lack of deposit insurance, but definitely not with respect to central policy.

It’s simple; you want the banks to be more prudent, then reduce the expected value of a bailout to zero. Thus due to the free market principle, they won’t take as much risk. Regardless of how many regulations you introduce, you will never solve the problem if you don’t remove this key incentive. The problem isn’t with the free market, as you say; it is with a lack of free market.

TM2 suffers from the issue of ‘you don’t know what you don’t know’.

"The banks are incentivised to take unsustainable risk, underpinned by the expected probability and magnitude of the tax payer funded bailout that they will receive when they become insolvent." Therein lies my issue. The banks are private business's. what right do they have to expect to be bailed out by the tax payer? Why isn't every private business afforded that right?I expect them to act responsibly, to have to respect the fact that it is my money they are messing with not theirs, and have a duty of care that any other business is required to meet when dealing with a customers property. As it is Banks have weaseled their way into a privileged position, are treated uniquely and although I have money deposited with them, in reality it is not my money but theirs, and if things go south i have to wait on their good graces to MAYBE get some of it back. Doesn't matter what colour you paint that picture, it just doesn't look right to me.

"The banks are private business's. what right do they have to expect to be bailed out by the tax payer?"

Exactly. However, the tax payer gives them that right by choosing the government.

"I expect them to act responsibly, to have to respect the fact that it is my money they are messing with not theirs"

That's the point, they are acting prudently with your money - they are maximising benefit within the governed constraints.

"I have money deposited with them, in reality it is not my money but theirs"

Don't think of it as a deposit, then. Think of it as investment and that the return you receive is commensurate with the risk you face.

Nymad, banking regulation has never been a part of election policy platform that I can remember. Instead the current situation has essentially occurred by stealth, without the majority of the population being aware. Thus it was never voted for. If given the facts and a choice I believe that most people would reject the current stuation out of hand because ....

They are acting to maximise profits for their shareholders not their depositors, thus from my perspective they are not acting prudently. Indeed as has been highlighted many time lately, their business practices are fraught with risk.

Think of it as an investment? I would if I had it in an investment account, but instead it is simply there for safe keeping, as I invest elsewhere, because investing through the bank does not deliver the returns.

See my other comment re margins before you suggest they are paying what they can afford.

Of course it is policy. Just because it hasn't been campaigned on, it doesn't mean it isn't inherent policy.

Post GFC there was significant uproar about bailouts from capitalists and the topic was campaigned on in most regions. The only place it got traction was Iceland. So, before you say no one campaigns for it, they in fact do by implication arising from not demanding that political parties categorically rule out government bailouts. The truth of the matter is that the average citizen wants their money to be protected by central policy, and more importantly they want to socialise that risk. It's a self perpetuating cycle.

So if they are not seeking to maximise the position of their investors (you call them depositors), how do they survive?

Investing through the bank does produce returns and what's more, they are commensurate with the level of risk you face. Ironically, they are likely comparatively lower on the basis that you support them socialising their risk.

RE your comment on profits. Again, it is misguided. Why should a company be embarrassed about making profit? It's not as if the company is rent seeking, it is just leveraging its market. Plus, when you look at it in relative terms, the profits aren't grossly high in margin terms. You get too caught up in the rhetoric of whimsey and what should be right which blinds you to the logic behind the things you talk about.

"inherent policy" so you agree that it occurred by stealth. Inherence basically means never publicly debated. It is implied because the Governments we voted for on OTHER platforms, bought into the banks position without overtly disclosing it publicly, in a manner the majority would recognise, and especially get picked up and publicised by the media.

They are not seeking to maximise the position of their DEPOSITORs (do not confuse this term with investors), they are seeking to maximise the position of their shareholders. Their survival is the profits they make and pay to their shareholders. At $4.5 billion profit per year in this country, the four big banks can clearly afford to pay better interest rates to their depositors.

The returns I get from buying shares on the share market gets 10+ times the returns the banks offer. And there is plenty of publically available information about their business practices and the risks associated. Why would I bother?

A company shouldn't be embarrassed about making a profit, it is the level of profit in the size of the market that is the concern. The banks are in a protected and privileged position and tell us their survival is at risk (because their margins are barely affordable) and then declare a profit that is better than $1000 for every man, woman and child in this country. What is reasonable about this?

Nymad, you distort comments to suit your own blinkers, and clearly cannot see the view of the average man on the street. Are you a banker?

Depositors v Investors - two widely different groups. Depositors put their money in a bank because they have little choice. Banks have manipulated the system now so that people cannot get their pay in cash, need to have a bank account just to be able to function, and most of all have received assurances that their money is SAFE in a bank. The majority are unaware that once deposited, that money becomes the property of the banks, and depositors are the last in the line to get it back if things go south for the bank. Depositors are wooed by the bank by being told if you leave your money with us, we'll put it to work and pay you a little interest for it. They not told how it is used, given and easily understandable explanation of the risk, or if the interest they get even compensates for the risk, or that if the bank gets into trouble they can be given a "haircut" - in other words lose some of their deposit to protect the bank's shareholders interests!

Investors take a wad of money to the bank and ask the bank to invest it. Sometimes they are told how it will be invested or are given a choice and they usually get a better return. There is a big difference between them and depositors!

See here we go descending into the irrational, again.

You are saying that Banks are not focused on maximising the welfare/utility of their customer base - illogical.

The returns you get from buying shares returns you 10x more than the banks offer - a categorical lie/misrepresentation.

Yes, the banks are in a protected position. But, as I say, they are only protected by the tax payer/voter. So don't blame the banks. Blame the tax payer collective. Again, you get caught up in rhetoric, though. What is $1,000 per capita in NZ? You have absolutely no relative understanding of what that means. It's just affixing an arbitrary number to the situation in order to suit a narrative.

Again with this dribble about needing a bank account to survive. The fact of the matter is, you only need it for very few transactions. Go to TSB and they will even charge you zero fees. You are always welcome to withdraw all the money the second it enters your account. The fact of the matter is that a bank account provides you with a greater level of utility than the alternative. As such, you offset this with some level of risk.

In terms of the control of the funds, ignorance is not an excuse. The arrangement is well documented and published. Again, you want to socialise the risks of the individual.

I can't see why it matters whether I am a banker, or not. Likewise, it is of no consequence if you are a 99% campaigner marooned on a traffic island somewhere. The fact of the matter is that the issue is not with the free market, as you first proposed, but in fact that one does not exist.

Nymad, it is not irrational, it is a fundamental truth that private business is focused on returning value for the shareholders. it is true that they should also look at the their customer base, but in this day and age it is extremely difficult to function without a bank account. Try doing what you suggest, take all your money out of the account as soon as it hits it and see what the fees do. I'd bet the terms and conditions for the TSB account would prevent that from happening at zero balance.

The bank protection has come about by stealth. I was discussing the banks with an individual the other day. He has a double degree, earns good money but was entirely unaware that his money in the bank is the banks money and he is an unsecured creditor, that the banks can give him a "haircut" under the OBR with no recourse if they get into trouble, and he doesn't know what his alternatives are. This guy is intelligent and educated, but i believe he is typical of the average man on the street. As for the majority who happily buy into getting into debt with the banks. Although the terms and conditions clearly spell out the costs and what can happen, it is widely acknowledged by all that the vast majority don't read the T&Cs in detail, probably couldn't understand them if they did. To say the tax payer supports this position is at best disingenuous. I doubt even most Government ministers fully understand the power that banks have manouvered themselves into.

As to Free Market - it has never really existed because the players, especially the banks have manipulated it. Regulation is required to remove the power imbalance, prevent manipulation and control greed.

well, based on mortgage calculator here and 20% deposit, if a $700k house drops to $600k, then if interest rates rise from 4.5% to 6.5%, you actually pay the same mortgage. Also, based on other commenters on this site, Banks do not earn higher margins when interest rates rise... if others comments are accurate, but I would not know about their profit margins related to interest rates.

Bank margins i suggest is a subject where misinformation rules the day. The ASB has just reported as cracking the $500 mil profit in 6 months, the big four combined report their annual profit has FALLEN to bellow $4.5 billion. All this from a country of about 4.5 million? Where does this suggest to you that their margins are marginal?

Agree 9-12 is CRAZY. National should be ashamed for letting this happen. Specuvestors...to quote the bad guy on star wars "wipe them out....all of them". Will be voting for DTI. NZ needs this to protect the averageman. Specuvestors are all about debt based tax offset and tax free capital gains.

Prudent investors can spell ROI and positive cash flow, and will have already addressed this risk by cashing in a few over the last 18 months Probably building equity to be ready to jump back in after correction. Anyone that's is crying after the correction is either stupid or greedy or both.

With such lax lending regulation in clear evidence, where is the moral authority for the RBNZ to recommend OBR impositions on depositors in the event of a bank failure?

There is none! Because of the RBNZ's failure to manage lending, the RBNZ must alone be responsible for bailing out the banks, there is no basis for placing the burden on depositors.

I'm confused by this - the article says:

"In the November report the Reserve Bank said about one-third of new mortgage lending was being done at a DTI ratio of over 6."

but also quotes the report as saying

"According to executives an ideal DTI level would be in the range of five to seven. However, they say that most borrowers are already at levels of nine to 12"

Are they talking about different measures? It seems extremely unlikely that things could have changed so much in a couple of months

Mathematically plausible, but the RBNZ November report doesn't support it:

"The share of lending at DTI ratios over 5 has increased for all buyer types since 2014 (figure 1.4). For example, the mean DTI ratio for a first-home buyer in the top half of the distribution has increased from 5.2 to 5.7, and has increased from 7.5 to 8 for investors"

So, the Bank of England's DTI limit is 4.5, the Central Bank of Ireland's is 3.5, and our banks think ours should be 5 to 7 ... why exactly? Because they think we're dumb enough to be willing to sustain that for eternity? Or because they know that if it was 3.5, pretty much every household they've loaned to over the last 10 years will be in negative equity?

Slow immigration, stop specuvestors and stop overseas owners and the problem is significantly reduced. How about an empty house tax like some other places. Water rates tracking makes this easy to work out.

Alternatively limit overseas and specuvestors to new builds...?

That's a good question, and it should be the responsibility of the author to provide a definition.

Presumably it's the same as http://www.rbnz.govt.nz/financial-stability/financial-stability-report/… where the ratio of total debt to annual gross income is discussed. There, it is called the Total Debt-To-Income multiple, or TDTI.

That is not to be confused with the Debt-to-income ratio that is the percentage of a consumer's gross income that goes towards paying debts, as in https://en.wikipedia.org/wiki/Debt-to-income_ratio

I think the article refers to the first meaning. For example, a loan of $500,000 with a gross household annual income of $100,000 would have a TDTI multiple of 5.

Any FHB that is considering DTIs of the current levels mentioned here need to run for the hills.

If they don't then the wrath the market will dump on them at some stage in the future is fully on them. I lived in the UK during a long period of negative equity for many households and divorces, bankrupties and deaths were very common.

Everything at some point reverts to the mean.

Nymad,The inept investor here!

Not too sure how you can possibly call,me that, as you have no idea of my borrowing compared to loan repayments etc. and assets.

The reality is that most seasoned property investors financial situation is no problem for the Banks so that they should not be subjected to ridiculous constraints.

The fact is that obviously there will be many in Auckland that are flying close to the wind, but the rest of the country should not be panalised due to their situation!

Personally speaking our rental returns bring in a significant surplus and yet we would be outside the DTI of 7.

The DTI being applied to property investors as well as owner occupiers is stupid, as each rental property that the investor has doesn't have the same living costs that owner occupiers have!

Seriously dude, what don't you understand about the concept of total debt to total income?

Let's run some ridiculous numbers here: let's say you have 10 properties all worth $500k, all generating rental yields of 5% ($25k/yr) (we'll ignore maintenance/rates/insurance for simplicity). You have no other income. You own 9 outright, and on the remaining 1 you have a 90% mortgage. Your debt ($400k) to income ($250k/yr) is obviously fine (1.6).

If we flip it: 1 property owned outright, 9 at 90% mortgage, DTI = $3.6million / $250k = 14.4 <- then we have a problem!

Would love to know your numbers TM2.

Well, you are a troll then..

On multiple occasions you have disclosed your confusion in the areas of gross and net yields, margin, and optimal leveraging.

You often fail to understand your market and the dynamic implications of your asset class. You also don't seem to grasp the concept of risk.

The other day you even alluded that you pay interest only loans on some of your properties.

Today you said that investment properties are a safer bet to banks than occupiers, on the basis of nothing.

I'm not saying you aren't successful in what you do. All I am saying is that it's by some miracle that you manage to do it.

Nymad, you can call me anything you like, if it makes you feel,good.

Never been confused about net or gross anything, not sure where you get that from?

Of course I understand market implications and I have said that many times that I beleive Auckland will drop,at some stage as it is overpriced and rental returns are poor!

I wouldn't touch it with a barge pole now as an investment property is one that gives a positive return.

Yes I do pay interest only on more loans than I do on P and I.

Yes a positively geared property is a FAR safer bet than an owner occupied property as I have stated why.

It is no miracle that I am successful and if you knew me you would know how,Imoperate.

I have also assisted several people with many property deals and they are very appreciative and far better off financially now.

Obviously not... how many friends do i have that have been to rich dad, poor dad seminars and rushed into buying properties using equity from their family homes on interest only mortgages. What happens WHEN house prices cool (to whatever level) and interest rates rise with no Chinese money coming in to mop up? Their incomes will not rise, i head the same thing from investors over and over that they will raise the rents - good luck with that if people literally can't pay anymore... I believe there must be many many people in this situation banking on capital gains.

You would have to be some special kind of fool to not believe their is a higher potential for there to be big trouble in the land of the long white cloud than not....

Gregonomic,

Seriously dude, don't really think you have much idea as to how the Banks lending policy works!

Firstly there would be no way anyone would be in this situation as the Banks would not have lent to anyone under the basis that you have stated with 90 per cent on 9 properties or anything like that.

The thing is that the Banks previous policy had them happy with the servicing requirements for borrowers and it is the Reserve Bank that has brought in the LVRs at 60 per cent and thinking about the DTIs which I doubt will come in anytime soon if at all as it will affect First Home Buyers.

Obviously there is no way I would be disclosing my financial,situation on any public forum but take it as,gospel that property has been an ideal investment for us, and a good lifestyle

It doesn't suit everyone but the secret is you make the most money when you buy, and not have to wait for capital gain.

Positive returns plus potential is also required to be successful at it.

And the next 10 years? >4% yield (and rising) with a 10% capital loss per annum? Perhaps we might see residential property being treated like any other income producing "asset", with real depreciation rates and a major reversion of capital value to the long term historical mean.

In the U.K. The figures are based on people's gross income. Is that the case in NZ? I hope not as if it is the case then there are a lot of people out there earning 100k a year with 1m mortgages. The interest alone has effectively gone from 40k per annum to 50k due to the rising yield curve over the last 5 months.

To me it just highlights the fact that there needs to be much greater taxes on secondary home ownership to rebalance the equilibrium.

If it isn't going to be your prime residence then charge 15% stamp duty or some equivalent tax.

I say that as a second home owner. WE NEED TO HELP THE YOUNG.

I know a lot of young people who don't want your help and are more than capable of getting on the property ladder. only costs $350k to buy a good 3 bedder in Hamilton...but now with 40% LVR has totally screwed young and old people...20% LVR's was fair for everyone, maybe push it to 30%...

The blinkered approach to property that's leaving everyone wanting is that houses are for investment not homes, to the point they receive advantages over other investments and are pumped up by foreign investors.

Remove those advantages, levy foreign ownership - watch how many people are no longer left wanting.

You're clearly out of touch with the Hamilton market (regardless of whether or not you own property there). You can not get a 'good' three bedroom house in Hamilton for $350k, unless you are wanting to contest the generally accepted meaning of the word 'good'.

I also agree with MisterB's point - to 'get on the property ladder' implies buying one's first property, which for most, is an owner-occupied dwelling, subject to only an 80% LVR limit.

And don't even get me started on the nonsense that is 'a FHB wanting to buy their first investment property'. A first HOME buyer is someone buying their first HOME, to live in.

Gregonomic, I have previously stated on here that our returns on purchase prices are between 6 and 15 per cent.

As I have said you make money when you purchase property and that is why there are investors that are able to be fulltime positively geared investors and other ones that think they are property investors but have negative returns and rely on capital gain.

I don't buy property that requires financial propping up each week and needing to rely on tax refunds to make it a successful investment.

Quite the opposite, I pay tax on every property to different degrees.

Renting or owning there technically arguably is no difference, when you own you have a title deed from government that allows you full rights to the property, when you rent that's just usually to a private individual for an ongoing fee, find the right landlord and you can rent for the next twenty years, find the right house to own and the government can redzone it or build a motorway through it, one thing for sure it's not going to be the place you sleep at night in heaven

I did a couple of years as a mortgage broker in the early 2000's. Back then banks were strict on serviceability. Formula was 30% of gross house hold income available for servicing debt. For example if you earning $100K then you had $30K to service debt. From that they would deduct student loan repayments, 10% of your credit card limit per month and any other debt commitments. So if you had a $5K credit card limit it would reduce your $30K to $24K. They then grossed up that figure by the floating rate plus 1%. So if floating rate was 6% then they would make it 7%. So $24K / 7% = $342K or 3.4 x income. Seemed quite logical at the time. Mind you in 2003 we could buy a decent house in Papatoetoe for under $300K and a section in Hamilton East for $80K and build for $1100 per sqm.

Given the interest from readers in the 9-12 figure I asked KPMG's John Kensington for further detail/clarification. Here's what he said;

"It was very much an average type comment, talking about a range of borrowers across a range of property and a range of prices and incomes. The point that was being made was a general one that in NZ we tend to be paying more compared to our income than the ideal range for DTI observed elsewhere, it was very much an industry wide comment not specific [to a type of borrower or a region]."

And were gross or net figures used in the DTI calculations?

"This is one of the issues around DTI. The fact that definitions of what is debt and what is income are open to wide interpretation. The real point is that we are in many markets nearly double what would be an appropriate rate so whether its net or gross income doesn’t really matter, because we are already so much over what would be a sensible setting."

Cheers.

1. He doesn't say it's double, he said it's ''nearly double''.

2. What does ''nearly double'' mean? 1.9x? 1.8x? 1.7x? 1.6x? 1.5x?

3. What does ''nearly double'' mean again, did they measure or calculate something? Hard to say, as the Partner at KPMG doesn't know if net or gross are used in the calculation (if there was a calculation) nor is he even willing to say what debt and income are.

It is hard to know whether the conclusions presented by KPMG are true or false, and how seriously to take them. Their argument is significantly weakened by statements such as

''According to executives an ideal DTI level would be in the range of five to seven. However, they say that most borrowers are already at levels of nine to 12"

which is unsubstantiated at best, bogus more likely, and definitely not to be taken as a true or accurate measurement.

ANZ economists said in their January 2017 report that " the average mortgage payment to

income in Auckland is around 52% for new purchasers".

Now, using that figure and applying a simple calculation assuming a 30 year loan and 4.8% interest, suggest that the debt to income for such "new purchasers" is 8.18.

Given that the UK DTI limit is 4.5, then "nearly double" means about 1.82.

I would say that ANZ economists have corroborrated KPMG in its assertion.

Kensington seems justified in saying that NZ banks are lending " much over what would be a sensible setting."

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.