By Gareth Vaughan

The Reserve Bank has formally asked the Government to add a tool allowing it to place limits on debt-to-income ratios (DTIs) for residential mortgage borrowers to its macro-prudential toolkit.

A spokesman for Finance Minister Bill English confirmed to interest.co.nz that a formal request has been made. The Government, however, is yet to greenlight the move.

"The Minister has asked the Reserve Bank for further information and the Government will make a decision in due course," English's spokesman said.

How things play out from here will be very interesting. Because the introduction of a DTI limiting tool has the potential to have a major impact on borrowers, banks and the housing market.

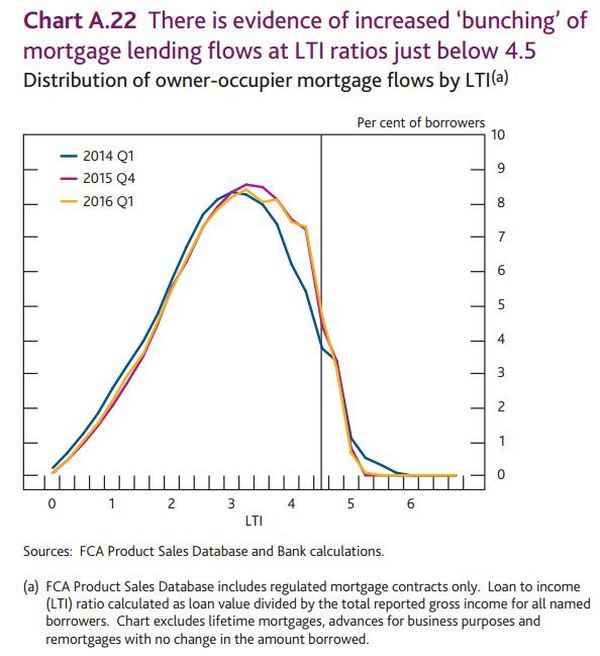

In 2014 the Bank of England introduced rules through which mortgage lenders must constrain their proportion of new lending at loan-to-income (LTI) ratios at or above 4.5 (four-and-a-half times a borrower's income) to no more than 15% of the total number of new mortgage loans.

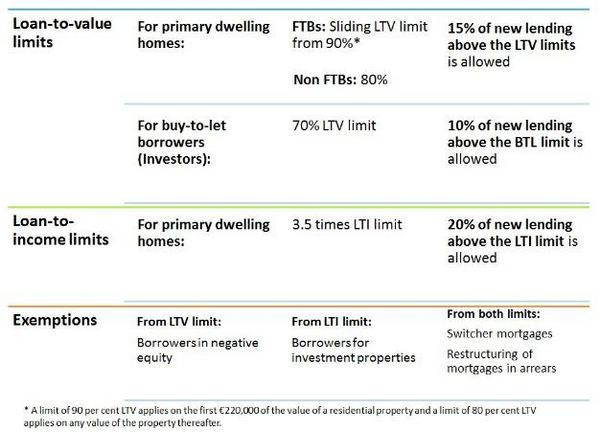

In 2015 the Central Bank of Ireland also introduced LTI ratio limits. Loans on primary dwelling homes in Ireland are now subject to a limit of 3.5 times loan to gross income. For banks this limit should not be exceeded by more than 20% of the euro value of all housing loans for primary dwelling home purposes during an annual period.

Potential game changer

We don't yet know the detail of Reserve Bank DTI ratio limits, should they go ahead. So let's take a look at the impact Irish or British style rules might have in New Zealand.

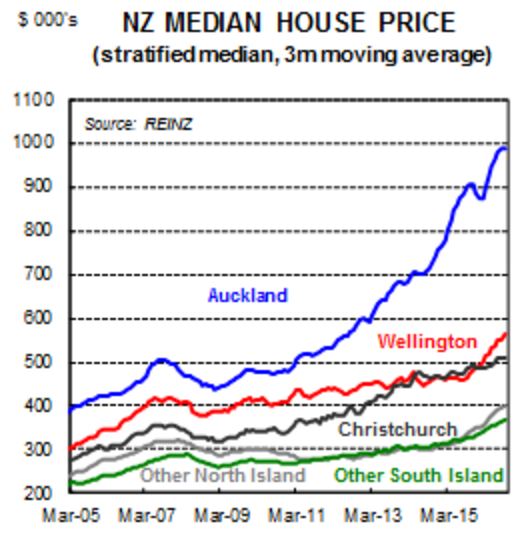

As of September, the national median house price - according to the Real Estate Institute of New Zealand (REINZ) - was $515,000. In Auckland it was $825,000. At the Irish 3.5 times DTI limit a couple earning a combined $100,000 per year could borrow $350,000. That's equivalent to 68% of the September national median price, and 42% of the Auckland median price.

At those levels a DTI limit as strict as Ireland's doesn't seem like a big deal.

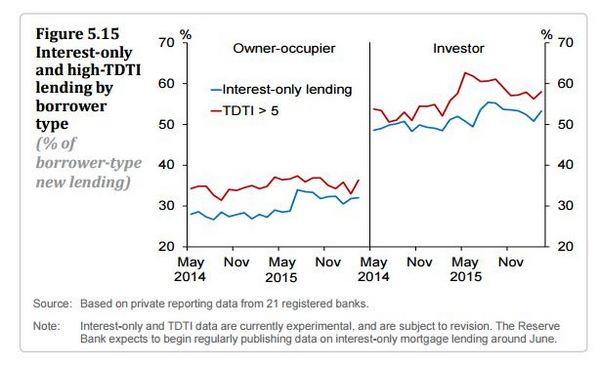

However, the chart below, from the Reserve Bank's May Financial Stability Report, suggests about 35% of owner-occupier mortgage lending in New Zealand is done with debt-to-income multiples of more than five, while almost 60% of investor lending is done with DTI ratios of more than five. And in August last year Reserve Bank Deputy Governor Grant Spencer said 30% of new borrowers were taking on mortgages at greater than six times income, noting; "At these ratios, it would not take much of an increase in interest rates to substantially erode mortgage affordability."

Thus an Irish style 3.5 times DTI ratio limit, or even a British style 4.5 times limit, would change the game for a large volume of Kiwi borrowers, especially in Auckland, at either the 15% of loan volume or 20% of loan value UK or Irish limits.

What are the political ramifications in election year?

In May Reserve Bank Governor Graeme Wheeler said DTI ratio limits were something the central bank would look at, adding, "It has been successful in other countries, particularly the UK, which has recently adopted debt-to-income ratios." At that time English and Prime Minister John Key said they were open to the idea of a tool limiting DTI ratios.

But undoubtedly Key, English and their colleagues will be considering the potential political fallout of DTI limits, especially with 2017 being an election year. It's not hard to imagine vested interests in the real estate sector, disappointed would-be first home buyers, and opposition MPs railing against the DTI restrictions, and perceived government housing market failure, on the 6pm television news.

And the Government, of course, will also have its own housing agenda. Especially given housing will unquestionably be a big election issue.

To this end English recently suggested the Government was preparing to ramp up its programme of building new houses on Housing New Zealand land in Auckland, saying up to 30,000 medium-density and medium-priced houses could be built in the coming decade. Then on Wednesday English and Social Housing Minister Paula Bennett said Housing New Zealand lodged 60 resource consent applications in the last quarter. If approved these would see 1297 houses built for more than 3200 people in 20 Auckland suburbs.

The Labour Party, meanwhile, has appointed its housing spokesman, Phil Twyford, as its election campaign chairman. Labour's pledging that, if in government, its KiwiBuild policy would build 100,000 affordable homes and sell them to first home buyers. And Twyford also says Labour would change the law so someone selling a rental property within five years would pay income tax on any capital gain, as well as shut down tax breaks allowing "speculators" to write off their losses on rental properties by paying less tax on other business activity.

Bolstering financial stability

So why is the Reserve Bank keen on DTI limits? The Central Bank of Ireland says the key objective of its DTI ratio policy is to increase the resilience of the banking and household sectors to the property market, and to reduce the risk of bank credit and house price spirals from developing in the future.

Here the Reserve Bank is tasked with maintaining financial stability. At 165% New Zealand's debt-to-disposable income ratio is at an all-time high. As of the end of August housing debt stood at $224.981 billion, up 9.2% year-on-year, the fastest growth rate since 2008. Along with the existing high loan-to-value ratio (LVR) limits, DTI restrictions would further limit the amount of debt available in the economy.

Even with the Auckland median price down 2.1% from its record high to $825,000 in the latest REINZ figures, other parts of the country experienced double digit house price inflation year-on-year pushing the national median price to a record high of $515,000 showing high, arguably unsustainable, house price inflation is spreading. And let's not downplay Auckland. The ASB chart below demonstrates Auckland prices have been on one heck of a run.

Left out

It's interesting to note that no DTI ratio limiting tool was included in the Reserve Bank's 2013 macro-prudential policy framework when it was established. However, it did say although "the case for incorporating debt-servicing capacity in to the macro-prudential framework" was among areas not in scope for initial implementation, it may form part of the Reserve Bank's future work programme.

Aside from the high residential mortgage LVR restrictions already in use, the Reserve Bank also has three other macro-prudential tools in its toolbox. They are; the countercyclical capital buffer, which effectively is banks holding more capital during credit booms. Adjustments to the minimum core funding ratio, which could be increasing the amount of retail funding, longer-term wholesale funding and equity banks have to use to fund their lending. And sectoral capital requirements, or increasing the amount of capital banks must hold against certain types of loans (IE home loans) in response to sector-specific risks.

Based on the push to have DTI restrictions added to this toolbox, it appears the Reserve Bank now views them as a better option than any of the other tools already available.

It's also worth noting there are rules in place for the notice period the Reserve Bank must give banks if it plans to introduce a macro-prudential tool. For the countercyclical capital buffer it's up to 12 months. For sectoral capital requirements it's up to three months. For adjustments to the core funding ratio it's up to six months. And for restrictions on high LVR housing lending it's at least two weeks. Obviously we don't know what the timeframe would be for introducing DTI ratio restrictions, should such a tool be added to the toolbox.

Do they work?

So are the DTI ratio limits in place in Ireland and Britain actually working?

A report released by the International Monetary Fund, Financial Stability Board and Bank for International Settlements at the end of August pointed out that as the broad use of macro-prudential policy tools internationally doesn't yet span a full financial cycle, lessons and empirical evidence based on their use remains tentative.

Of borrower-based tools such as LVR restrictions on high residential mortgage lending and DTI ratio limits, the report said, "Borrower-based tools can support the resilience of borrowers and contain procyclical feedback between asset prices and credit. Limits on LTV [loan-to-value] and DSTI [debt-service-to-income] ratios have been found to enhance borrower resilience and moderate lending growth. However, their effects on house price growth appear to be limited."

In June Central Bank of Ireland Deputy Governor Sharon Donnery said if Ireland's mortgage restrictions had been in place 15 years ago, the scale of Ireland’s post-2008 financial crisis would have been much more limited. Data clearly showed a link between higher LVR and DTI ratios and subsequent mortgage defaults and also between higher LVRs and banks’ losses from defaults, she said. (Ireland also has high LVR restrictions in place).

"The mortgage measures are designed to act as a restraint on excessive repayment burdens and unsustainable increases in household debt and limit the risk of another house price-credit cycle emerging. They are constructed to protect the financial system as a whole across the medium to long term," Donnery said.

"I think a key issue has been that part of the issue previously was around what we call, house price credit cycle reinforcing each other. Where the ability to borrow more leads you to bid more for a house price which leads you to look to borrow more and it gets into a vicious cycle. Part of the purpose of the caps is to try to stop that kind of cycle re-emerging into the future and obviously the other aspect it is very important from a borrower indebtedness point of view but it is also important from a banking sector resilience point of view but those two aspects of the measures both borrowers and banks, I think, are important elements," Donnery said in an interview with The Sunday Independent.

There's more from the Central Bank of Ireland here. And the Irish central bank is due to review the macro-prudential tools in use in Ireland in November. Incidentally, as of June 30 the big five Irish banks still had €45 billion of non-performing loans, which represented 19% of their combined loan books.

The chart below comes from the Bank of England's latest Financial Stability Report, noting an increase in the proportion of new mortgages extended at LTI ratios just below 4.5.

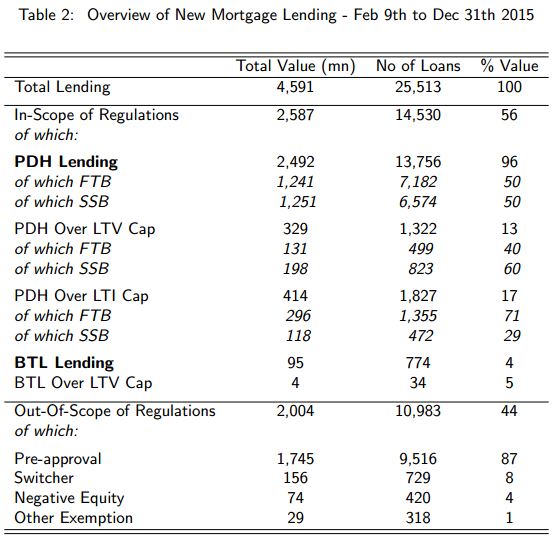

Below is an overview of Irish macroprudential regulations for mortgage lending.

The table below comes from the Central Bank of Ireland. PDH stands for principal dwelling house, FTB for first time buyers, SSB for second and subsequent borrowers, BTL for buy to let, and LTV for loan to value.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

137 Comments

Boom times ahead for Finance Companies?

its been boom time for finance coys over the last few years Roger.

And "The Boy" thinks he controls his housing investments. No the RB does.

Just going to lock more and more ppl out of the housing market. They'll bring it in quickly too just like they did with the 60% LVR. The baby boomers have already loaded up and paid off there properties time to shut the gate

Gordon, not too sure what you get out of your jibes at me all the time.

Very hurtful and upsets me greatly.

If they bring in the DTI it won't affect investors unless they wish to sell for some strange reason.

Most first home buyers will be totally shut out of the market and the only ones buying in Auckland will be the overseas buyers who have access to overseas money.

There will be next to no developers prepared to build as they won't have any buyers who will be able to meet the Banks borrowing requirements.

The Reserve Bank hasn't thought this one out fully.

What it will mean for investors is that they will never be short of tenants as the tenants will never be able to buy their own homes.

While your argument is nice and logical and seems sound - do you have any evidence that this is what will happen or are you just speculating ( and using FUD). Anyone can speculate - I could speculate what will happen if DTI's are not implemented.

Anyone can speculate, and they can then be on either side of the "I told you so" discussion later on.

But, I would say it is safe to assume that any Govt intervention will not have the impact that the Govt planned, forecasted, or expected.

As for evidence, The Mans opinion seems in line with my own, and many a person has been right based on little more than gut feeling. I see no reason why everyone has to back up everything they say with evidence. Accept it as an opinion, and feel free to voice your own.

I agree. The Man 2 has some good advice. The philosophy of this entire web site is speculation. I'd say that BadRobot has not made one comment that is any way remotely useful to a budding or seasoned investor. We all know that the future is not certain so there is no point reiterating that fact. My advice is to back long term winners because they have a history of winning; an idea that is an anathema to BadRobot apparently.

I didn't know I was here to give advice. I am mildly amused why people get so intense about different investment ideas - there are more important things in life. Choose one you are happy with - but understand that other people may not believe the same things you do.

I've never said anything about not backing long term winners - just that long term winners means different things to different people.

I probably shouldn't waste my time but ....I always find your comments hard to decipher. For instance, you write, I didn't know I was here to give advice, yet in the next sentence you write that there are more important things in life and then to Choose one you are happy with.. which comes across as awfully like advice.

Then you write long term winners means different things to different people without any explanation or examples detailing what that actually means. It conveys no useful information to me at all and leaves me feeling vaguely uncomfortable.

Sorry "The Boy" I am not trying to upset you. However I can smell the fear in your comments. The RB is hellbent on rebalancing the economy. They will implement DTI measures that will be harder on investors and will still allow FHBers to buy their first home. You will still be able to buy one or two rentals but the days of large fully leveraged rental portfolios have to be numbered. Except maybe in Christchurch where the odd fool will buy rubbish no one else wants in an earthquake prone city.

Yes there is something else going on here - fear that the winner they backed is not such a a sure fire winner - just speculating.....

I'm just playing devils advocate

I think for meaningful control of housing crisis - national government has to go as they have made it quite clear that they are in government to protect rich and speculators ( they vote). Also when everyone knows that their is a housing crisis - be it people, experts or agencies BUT the national government mindset is exactly the opposite that it is not a crisis but sign of prosperity ( Defenitely for them and the social circle that they move in) and is a good problem and more the better (for all other the more the worst).

In above context even if national government is forced to act or give green signal for agencies who want to act (as election year approaching and in reality housing crisis has become to hot to handle) will do it but with condition to benefit their elite friends and speculators. Intent will be missing.

As someone rightly pointed : Legacy of National : Denial, Lie and Manipulation ( manipulation of data to suit their vested interest and/ or manipulation of policies or action with no real intend)and if nothing works Blame and now with election approaching may say things/policy that people want to hear (also are right and should be done) but with a rider and timeframe of after election so can backtrack.

All this is also possible as media too is very weak in NZ . A issue here and their is raised for effect but is not persued to expose government and this too may be because of self vested interest - If media was strong government will have to think before following their policy of denial, lie and manipulation.

Irony of NZ is that is run by businessmen instead of leader with vision. Think and vote.

How correct - national government denied the role of overseas /non resident buyers and than to justified manipulated the defination of non resident/foreign buyers and data to lie to people to suit their motive.

Bluff is clear to one and all but the media fall or believed them - Raise a question mark on the NZ media.

A DTI limit can be very effective without touching FHBs.

No sane FHB would want to take on a DTI greater than 6, -more than that then the FHB would be spending more than 60% of his after tax income on housing.

The advantages to a FHB of that DTI limit being imposed would be:

- the FHB would not be competing to buy houses with other FHBs on the basis of their willingness to be reckless, but on their savings.

- the FHB would not be competing with "investors".

The Bank of Ireland seems to have exempted investors, but that is the group that fuels prices rises.

It is essential that the RBNZ applies a blanket rule, including investors.

As John Bolton has explained to us, for investors in property “the idea was to buy, get capital growth and then recycle your deposit into the next property.”

That recycling of house price rises into additional house purchases has an explosive effect. Even at current LVR limit settings the credit multiplier effect of this is twice that of an owner occupier.

With a DTI limit of 6 applied to investors, and assuming a rental yield of 5%, the effective LVR limit for investors would be about 30% ( = 6 x 0.05).

For the good of FHB's I hope that the Government approves the RBNZ proposal as soon as possible.

The Bank of Ireland seems to have exempted investors

I noticed that too, and thought it was strange. But Table 2 from the Irish Central Bank suggests that investors only make up ~4% of the market.

The settings would have to be different for NZ, where the investor share is much larger.

A lot of people exited property after the last crash, also there aren't the same tax incentives at play.

will not happen before the election, this government will drag their feet, after all their only growth plan is high immigration and house prices both of which could be fixed very quickly if the will was there

The Minister has asked the Reserve Bank for further information and the Government will make a decision in due course," English's spokesman said

Have noted the rapid increase in listings on trademe in Auckland region, continues to rise day after day. I would suggest Auckland market is correcting, and median being held up by weighting now to owner occupied properties in better areas rather than rentals in South/ West Auckland. DTIs at 7 or below will in all likelihood crash the Auckland property market, probably not top of National's wish list heading into election year.

A friend of mine has just sold his property in the DGZ. He set the reserve at the high end of the homes.co.nz estimate and the property sold for 200k over that reserve with six parties bidding. It eventually sold to a phone bidder. I bet there was some applause after that auction!

All part of the long game to eventually bankrupt private property punters and pass ownership to corporate investors, as happened in the US, with taxpayer funded GSE underwriting backstops. BlackRock is a good example.The tipping point is not too far away.

Given the objective of the RBNZ seems to be confirmed that they are only propping up Auckland they are going to keep trying to suppress the servicing percentage for household debt. There's at least 18 months of downward trend in that statistic, but that's just due to the last of the high fixed rates being cleared out. It's increasingly likely that it'll start going up again after that.

Thought you were calling me for a minute ;-)

Yes DGZ is still extremely popular...is this property in Epsom or Remuera?

Cornwall Park Avenue, Epsom. The best side of Great South Road :)

Hmm nice. I know a young couple who live on that street. They bought in 2011 and paid $875k for their house which is probably worth close to $2m now.

Also received an update from my source on 2 properties that were sold in Remuera this month:

4A Lucerne Rd - Sold $4,300,000

6 Lucerne Rd - Sold $5,351,000

Note that they're not within the DGZ and close to Remuera Rd end (traffic & noise) so I thought the prices are a little on the high side.

Homes.co.nz has 4a right on the money and 6 at their high end estimate. It seems pretty accurate that site.

My theory that the whole of Auckland has become DGZ seems to have come true.

Bhahaha love your GSOH Zach ;)

I think it's more to do with location than anything else. For example, an average 3-bed 2-bath, cross-lease property at 1/18 Mainston Road sold for $2,205,000 last month due to its location close to the motorway despite in the south side of Remuera Rd and not in DGZ. CV is only around $1m.

http://rwremuera.co.nz/auckland/remuera/118-mainston-road-7753331/

Thanks DGZ, not everyone appreciates it. That Mainston Road house looks quite stylish though rather than average. Didn't even have a garage! I think chic, immaculate, properties will sell at a premium but of course, yes, location is paramount.

That's why we're the best buddies...we just click ;) Hopefully people aren't accusing us for being the same person this time round *ahem*.

Hey Zac, I am finding Homes.co.nz estimates usually on the lower side. Most recent example is 13 Rangipawa Rd in One Tree Hill which sold for 1065K. Homes estimate - 935K.

Interesting. I guess they just use a simple formula to work it out based on RV and average percentage over RV that properties sell for in the vicinity. Some properties have RVs that are too low although if you are finding most are on the lower side then prices are still increasing in the areas where you are looking..

You nailed it I think...

"if you are finding most are on the lower side then prices are still increasing in the areas where you are looking.."

Kind of market action that keeps or even raises median/ average price while market starts to deflate starting in the low rent areas. Always a few who are a day late and a dollar short, known as winner's curse.

What would this mean for investors?

Have I got this right???...

Joe Bloggs has a day job earning 80K. He has three investment properties earning him gross 25K per annum each = 75K in total.

Therefore, his gross annual income is 155K.

A DTI of 6 would therefore still enable him to borrow over 900K.

Therefore, bugger all impact on an investor like Joe Bloggs...

Similarly, most FHBs probably can't realistically afford more than 6:1 anyway

A DTI of 4-4.5 could, however, have a meaningful impact, so the devil will be in the detail

DTI restrictions are likely to take into account total debt and total income.

So it would really depend on how much debt Joe Bloggs has left on those 3 properties, and how much they're worth. If they're fully paid off, then yes, I'm sure the banks would love to lend him more.

But if he only has 5% equity and interest-only loans on those 3 properties, he might find it a bit harder.

Yes, if Joe Bloggs is at the LVR limit for all his existing properties with total debt of 900k, with say 200K of additional cash at hand, then with the current LVR limit he could buy another 500k property. However, with a DTI limit of 6 also applying, and 25k rent from the new property he would be limited to 150k on the incremental loan, i.e. he could afford to pay only 350k for 25k of rent.

From reading this article ( below) .... ( which I found to be important ) .... we might already be in the early stages of a "credit crunch" ..

http://www.interest.co.nz/opinion/84160/john-bolton-sees-much-tighter-m…

Sounds like Banks are already finding the current environment difficult for both lending and attracting depositors.

If the RBNZ introduce DTI limits now ..., to me , it would seem like an extreme measure.., with unintended consequences... ( eg.. new developments stop... , economic slowdown , shadow banking.. etc.. )

It is possible that efforts to chill capital gain for buyers on some developments out in West Auckland has caused those developments to be completely cancelled. Making people sign contracts that stop them from selling within a certain time frame and then only able to sell to a restricted set of buyers. I only heard this in a conversation. Nobody wants to buy into that.

You are right Zach, I for sure wouldn't want to get locked into that sort of arrangement. To be honest I rather build my own if I have the money. Did you watch Grand Design last night? The owner spent $2.5m building a French house at 6 Hepburn Street in Freemans Bay. I was flabbergasted to see it on TV as I have walked past that house many times in the last few months.

I very rarely watch TV yet I did see that episode last night. One million over budget - that's crazy. Could have bought the real thing in Paris with just the budget over-run. I was wandering around Paris the other week and saw apartments starting at about 250k euros. My whole family prefers Auckland though. I quite like Kent in the south of England.

By all means I think sacking the builder half way through the build was disastrous, and I think it contributed hugely to the $1m over the original budget.

The land for that address is around $1.7m (as per the Council website) but probably more like $2m in the current market. If you add the $2.5m on top they will need to sell it for well over $5m to make it worth while...it's a bit ridiculous don't you think?

grossly over capitalised

According to the sales history the property was bought for 1.7m so if you spent 2.5m on the build it would 'owe' you 4.2m. Homes.co.nz puts the upper value at 2.4m. However if you could get 4.5m it would be a win, again proving it's hard to lose money in the Auckland property market!

The RA commission for 4.5m would be around 150k. If I were the owner I would not want to sell it for under 5m, especially after all the stress he had to go through during the build process.

The Hepburn Street house seemed to be built to be just what the owners wanted. And what a marvelous house it is. 2.5 build cost is over the top clearly, even if it was a job for love, and especially if it was for profit.

That sounds seriously mismanaged. Grand Designs is often an example of how not to do things so I'm not surprised.

It appears that banks in Australia are facing increasing mortgage delinquency and this I suspect will impact on New Zealand banks and their lending

http://www.businessinsider.com.au/australian-mortgage-arrears-are-at-a-…

" Government wants more information" is it a joke - Do they not know by now -Playing with time or / and need more information about loopholes that can be put in place to save.....

Gordon, you can't contain yourself can you, having a go at "The Man" continually.

If you get something out of it then I can't stop you, but all I try to do is paint the picture that IT IS possible for anyone in NZ to,improve their lot.

Can't see how the Reserve Bank is going to improve the housing situation in Auckland by bringing in Debt To Income ratios unless the ratio is at least 7 times income

Even at that don't think first home buyers will be buying much up there.

NZ is a very sought after country to live in and if our young are locked out of the market (And they will be) it will be the overseas buyers who will buy.

Yes investors will not be able to buy many more depending on current value to debt ratio but there is ways around it if you can be bothered.

Homeowners won't be able to buy that first rental property either if they have a sizeable mortgage already.

For those that for the last few years waffled on about prices crashing then I think you are sadly deluded.

For those that want to get ahead and improve their own situation then I suggest you get alongside successful investors whether it is property or a talented share investor like GORDON.

The Boy you prattle on that you are in complete control of your precious housing investments. In one stroke of the pen the government or the RB can bring in new rules that turn property in NZ upside down. You are not in control especially in Christchurch. You are at the mercy of nature,the insurance companies and Banks. If there is another big one the government might not have the ability or the will to sort it out for you. Just remember that all loans are on demand and pending demand you can pay rent to the Bank monthly. Loan finance is getting harder to obtain in NZ. From what I am reading the Banks are repatriating money back to Australia. The RB might not need to implement DTI rules as the Banks are sorting things out themselves as they are getting nervous, just like you.

Gordon I personally have got control of my rentals.

I decide whenever I want to sell and no one else.

All positively geared and LVR very comfortable and absolutely no fears whatsoever, but it is not about my financial situation that I am concerned about!

Properties insured apart from 2.

Loans are payable on demand but my Business Bank Manager has told me that I am his safest customer, so maybe you know something about me that he doesn't know?

Yes you have to meet the new requirements from the NZ trading banks but the non trading banks are doing a roaring trade and are lending much high per centages.

Anyway, pointless you keep cracking on about property investors being nervous when the sharemarket is continuing to slide and is tipped to dip again this week, which is not good for investors including the Kiwi Saver accounts.

Not nervous. I buy more in dips as the dividends are constantly rising. The shares I own are in a monopoly business that us humans cannot do without. No tenants, no expenses, no government or RB intervention likely, no earthquakes, no other natural disasters, no rising costs and can be easily moved on.

The Man 2 is not claiming he is in "complete control" so your continuing hostility is incomprehensible.

"Gordon I have got personal control of my rentals."

Personal control in that he directly manages the business rather than relying on others to do it. This is appealing for landlords as they have seen people run off with company profits, cook the books or just generally mismanage things.

If you think he meant that Zach it is no wonder you love Donald.

Gordon is that a copy and paste version or did you just type the sentence up?

Yes control Gordon!

We manage our own property.

We decide who we put in them!

We decide how much rent we charge!

We decide what property to buy!

We decide which Bank we can use!

We decide if we want to sell at any stage! not that we want to or need to!

We decide what maintenance or improvements we do!

Got the general?

You do not have the same control with equities!!!!!

I have more control The Boy. I decide which quality shares I buy and sell of course when I want to take some profits. I have no tenants or costs. Just rising dividends to spend when I want to. No government or RB can dictate anything about my shares but the government and RB can certainly control property in relation to price and rental returns if they want to. You are only talking superficial control. Real control in your investments lays in the hands of the government ,RB and nature of course as you are in Christchurch which is winding down as they finish the clean up. For a start you put any tenant in your so called rentals and you face potential P issues. They might turn up in a nice car with great references but as a retired professional I know just how many business people and professionals are using P. Don't get me onto how tenants do not look after their landlords homes. That is another story in itself.

I give up Gordon.

You are right, You are "The Man"

Pointless saying anything to you as you are so tunnel visioned and negative about everything.

Good investing, leave you to it.

No I am not the Man. I would never be so arrogant as to think or say that. I am just an ordinary retired professional who took another route to retirement. I had so many clients who tried your method but they got out as they realised they had no control over their leveraged rentals. In essence they bought an expensive asset with bank loan finance and handed it to a stranger and said, "please look after it and please pay us or rent regularly." Of course for many that has not turned out to be the outcome and now we have the scourge called P. No matter how carefully you vet a tenant it is always on the cards that they or associates manufacture or use P or both. You might be lucky and have great tenants always but that is unlikely. Control. I hardly think so as you are bringing human nature into the equation. You have no control over them when you hand them the key.

You check them out first thru many avenues.

You do regulars checks

You have approx. $2000 in bond that they generally would like back at the end of tenancy.

You are professional and ensure you run it as a business and not the WINZ office.

At the end of the day Gordon, your friends may have had bad experiences and not worked for them, but personally know more people that have had more losses thru equities than property.

I don't think Gordon is arguing from a strictly business point of view. He firmly believes that his way to riches is more moral. He also wishes to be a champion or voice for the shut out first home buyers so these discussions get a bit emotional and repetitive.

Zach you probably have a point. My buying of shares has not shut FHBers of homes. I am not trying to be moral. When someone calls himself "The Man' you have to wonder about his intellect and how he expects people to take him seriously,especially when he trolls about the virtues of property investing and Christchurch investments. Seriously I thought I was a bit focused on one share which has its benefits and downsides. When people get on this site and talk about how clever they are when in fact they were just lucky enough to be born in the right generation who could buy cheap assets before they got more expensive. Just like myself. I am not the man. I am not clever. I am a lucky boomer who found a share, threw the kitchen sink at it including borrowed monies and got it right in terms of timing. I have been lucky in real estate also and now can help my children get into their homes.

$2000 will really cut the mustard when one of your rentals has used for P manufacture or consumption or both. As I said you might just be suprised by the number of P users and their backgrounds. It is getting into epidemic proportions in NZ. And I know more people who have made far more out of shares than property. If there is any more risk attached to equities it is reflected in the higher returns over time compared with property. Anyone can buy a house but not everyone has the knowledge and the means to buy good shares that consistently return growing dividends.

Doesn't your last sentence endorse the buying of houses? I fall into the group 'anyone' but I may not be in the group 'not everyone' so houses are indeed the safer investment as anyone can do that.

You can get extra insurance for P, costs about $350, tax deductible.

Anyone can do it and the small returns reflect that fact Zach.

Anyone can do it and the small returns reflect that fact Zach.

Still seems like an endorsement for property especially as you said the higher returns reflect higher risks especially for noobs.

Does it matter what you choose to invest in.

Personal insults are very close to the line here. Please refrain. Deletion imminent.

The Reserve Bank will probably announce a half a percent OCR cut in November and at same time announce a DTI commencing 1 December - the serious price correction that will follow across NZ will put many investors in breach of the 40% equity requirement, particularly those who purchased in Hamilton, Bay of Plenty, Whangarei, Dunedin & Wellington. What will a DTI impact be on the thousands of investors who have purchased apartments that are currently under construction? Many will not be able to settle the purchase.

It is the Reserve Banks previous crazy rules that have lead to 25% to 30% price gains in cities and large provincial towns outside of Auckland,which now means they are about to instigate a DTI to compensate for their prior errors of judgement. None of this will be a problem for Chinese buying in Auckland or investors with massive equity and string rental income streams - the unintendedc onsequences of a DTI will be interesting - any predictions?

The more important question is what if the RBNZ does nothing, and is forced to implement OBR on savers as a result of the inevitable crash?

If the RBNZ and the Government have not done everything possible to prevent a financial boom and crash, then they cannot implement an OBR, it would be immoral, a dereliction of duty of the Crown and directors of RBNZ.

They would been better to have done nothing - Reserve Bank totally stoked the fire in the Waikato, Bay of Plenty etc - prices would still be around 2010 levels in those areas if the Jafa investors had not hit town due to the first batch of Reserve Bank meddling

It is always better to do nothing as intervention for social reasons generally leads to disaster. Like Red Guards forcing landlords to go and live in the countryside or even something seemingly benign such as providing accommodation subsidies. Just let the market sort itself out.

Markets fueled by credit are not ordinary markets,: -regulation of credit supply is essential else the markets explode with huge damage. Unless of course this time is different in which case it will be a first in the history of the world.

It is the first time in history that property markets have gone so global as well as the more or less sudden arrival of thousands of rich Asians and others seeking to leave their homelands. This is unprecedented.

so is the amount of credit created. what a pickle if they decide to restrict credit and flow of money, assets would decrease in value and those leveraged would crash and burn.

will it happen unlikey RB's have lost the will and are losing the battle.

it will take another big event that they can use for cover to reverse QE

"Just let the market sort itself out."

So remove rent subsidies to landlords and negative gearing (or apply it to ALL asset classes) so the market can sort itself out?

most landlords likely wouldn't care either way about abolishing rent subsidies (go for it I say). Negative gearing already does apply to almost all asset classes. Negative gearing property has just had a little more time in the media spotlight recently.

It is the interest obviously that makes a property negatively geared!

It would be great if the removed the interest cost as being able to be claimed and therefore no one would be able to claim the net loss from other income.

On the same basis though the owners of property that was positively geared wouldn't be able to claim the interest cost either and therefore by that reckoning the rental property owners wouldn't need to pay tax on the rental income.

You can't have it both ways can you.

If the interest is no longer claimable as a deduction then highly likely a profit is being made, tax is payable and there is no loss to offset.

The owner of the positively geared property would have a higher profit without the ability to deduct interest. What makes you think they wouldn't need to pay the tax?

Good idea though would be to abolish interest altogether and bring about return of investment rather than return on investment. Lenders may have to be more responsible as well. The 30+ year debt binge doesn't get solved by making it easier to borrow.

The reality is that if they say that owning a rental,property is a business and it has to pay tax, then clearly you are allowed to claim ALL expenses that belong to that business. INterest is clearly an expenses so that makes it able to claim a tax loss if it is negatively geared.

Maybe they should just ringfence the loss so that you have accrued losses rather than offsetting against other income.

Doesn't personally affect me either way as all,positively geared and I pay tax on all profits

I foresee an erosion of renter rights as people move toward a motel/ book a batch model instead of traditional long term rentals if hotels, motels, etc remain business with deductions but not long term rentals.

A flurry of faction-based trolling in response to a well constructed article by Gareth Vaughan.

Interest.co is a website that states that it is to help you make financial decisions.

Mine and several others on here are putting our personal opinion on financial investment, whether it be equities, property or term deposits etc.

The fact that some like to push insults at us like calling "The Man" "the boy" etc. is irrelevant and it is up to the readers as to what they want to take on board.

I personally have put a few ideas forward from my personal experience and I assure you it has been a winning formula whether you take any notice of what I say doesn't affect me.

What I will confirm is that if you are willing to take advice from knowledgeable people with a track record then you are more likely to prosper than from listening to negative speaking people who always find fault with everything.

Of course, you wouldn't want your opinions to be perceived as trolling. That would be just plain....negative.

Back to topic.

l think a DTI of 4-4.5 could be really effective.

But as someone said higher up, hard to see the Govt accepting it as it will slow their vote winning ponzi.

Sadly, we have 'leaders' who are more worried about re-election than the country's future.

Gordon, it has nothing at all to do as to when I was born.

I have never once proclaimed how clever am I?

I have just pointed out how you can get ahead by putting In effort and by basic common sense.

Even today I could get ahead financially with property and with the interest rates as low as they have been and WILL stay low for the next few years at least.

I have always stated as well,that Auckland prices to my mind are overpriced in regard to rental return compared to Christchurch.

Everyone is entitled to,their opinion and I don't personally believe that over the past 20 years or so,that more people have made money from shares rather than property.

If you look at the average wealthy person in the world I would suggest that more of them would favour owning property over shares anyday.

The returns on property has been phenomenal when you consider you haven't had to put any money in to buy.

Bill Gates and Warren Buffet mostly own shares.

2 people. Wow!

They are just two example's - I could go on......

I think you will find they hold shares in their companies or public companies or both. They will have nice homes to live in but they will not have rental homes. They seek big returns not the mediocre returns of rental homes. As I said earlier anyone can borrow money and buy boring rental homes. People with good incomes and the ability to save some of it invest in equities, currencies, commodities, art, motor vehicles, jewellery and alike. They would view buying a run down home in Christchurch as getting close to watching paint dry or train spotting. It stimulates you. It would not stimulate them.

I think it would be very difficult to amass large personal wealth ( and by large I mean multi- billion) by holding only property - not impossible , just difficult.

Excellent article

Look forward to DTI ratio's being implemented hopefully with a ratio of 4.5 or lower. Not sure what would justify having rates higher than UK or Ireland.

Key will probably stall it just enough so it doesn't impact the election. Stall tactics are what they are best at.

Remember Key saying a few months ago he needs to look into Stamp Duty and whether it is allowed under the FTA. I wonder if he has instructed his legal team to look yet or is he waiting to use that line again.

The graph above shows what a poor job the Reserve Bank and Government have done. Debt at record levels and growing at 9.2% p.a. incredible.

The problem with DTI's is that they will work...my self interest does not want to see DTI's introduced as i wont be able to continue property investing for probably 5 years. Also my vote will switch to ACT who are more free market than National...am hoping National flip flop this until after the election so i can reconfigure my portfolio. My view is that DTI's will bring any normal earners (i put myself in this category) quality of life back 10 years as we wont be able to afford any upgrades or the house we want. As usual the proper rich with 8 figure net worths' will just sail on by like they always do. government policy only really fricks with the white collar to working class anyway. the top 1% remain unaffected...and may have to at worse downgrade to business class or give up the sunroof...

Auckland teachers struggling to afford housing... forced to move

Congraulations key on creating an Auckland brain drain......

http://m.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11734…

Bring in DTI 4 to 1

Vancouver tax 15% on all foreign buyers (include foreign students and temp workers )

Vancouver tax on investors and companies buying residental property

Never trust everything you read in the media, especially those from NZ Herald.

John Key is a great leader for many Kiwis who don't post in here.

JP, a good start might be to pay our Auckland teachers more than those that work in the provinces...(and police, nurses, etc)

KW. Paid for by special taxes on Aucklanders I hope. We are told what a success the place is. They can afford it.

Aucklanders tend to earn more than in the provinces hence probably pay more in income tax per capita. The flip side you could argue is that we subsidize the rest of the country...i suppose.

This has been flagged on this site for ages, and is the culmination of years of bad policy. So the solution rather than fix the policies and let it correct is a subsidy, I think not that is another backward step

DTI as we know sounds silly. I hope it's not implemented. It will be the single worst thing that can be done to FHB and Builders. On a long run it will increase house prices even more as it will stop new supply coming onto market. Pretty much opposite of what should happen.

Any rules with exemptions e.g excludes FHBs will be hard to manage.

Most of all, one new macro prudential every few months sends wrong signals to everyone. People don't know what to expect next and once again will has adverse effects.

Exactly right. A lot of people will rush into supporting what appears to be a solution at face value without thinking about the unintended consequences it will create in the long run.

So lets say JK and his cronies are right. Foreign buyers are virtually non existent. Introducing a loan to income multiple will quell every market.

It will reduce the number of new ford rangers being bought, it will lessen the number of new pools in the ground, the koru lounge wont be as full, the Cuban holiday will be put on hold, new residents will run off to Australia, house prices will fall (assuming foreign buyer data correct), businesses that dont think ahead will fail, people will lose jobs

The governments focus will move back to SME's as they suddenly realise that housing produces nothing except debt.

Its called a downturn, and it does happen. The wheel is still round and sometimes it gets a puncture.

Investors often sell to buy better iproperty that gives better returns. If this rule comes into place for new borrowing investors will not be able to Re-buy so will just sit on thier investment properties which will not help first time buyers.

If they're still within the DTI limits, that's not really a problem. Remember, this is as much a financial stability issue as it is a housing affordability issue.

If investors are over the DTI limit when it comes time to refinance, they might find that they need to pay off more of their debt, and/or sell their properties - if the latter, it would improve housing supply.

Whats the alternative do nothing and watch auckland prices hit 1.5m

How much worse can it get???

People claiming it wouldnt work are greedy investors...

Any investor buying a property is doing so at the expense of first home buyers

Investors should pay a vancouver tax unless they buy new builds

Investors can provide a service by increasing supply

investors buying exitsing homes are adding no value. Often kicking out tenants so they can reno then flip....

Investors are the problem for sky high prices not the solution.... they need to have incentives to buy new builds. Best way is to tax them 15% for buying existing properties

Dti

Vacouver tax on investors

46% of buyers are investors. is that the worlds highest ratio?

I think it is the government responsible for not having right policies/ tax / restriction in place. Infact they are supporting and promoting investors/speculators being one themselves are able to identify more with them than common average newzealanders.

I see in the NBR this morning that Century 21 are asking the RB to not implement DTI's. That the market is already correcting and they are not needed. Wow!! Talk about making sure they are implemented as maybe they will work.

Smoke cover again ..... target investors, overseas buyers and non-residents!

hit them really hard and the unnatural demand will be fixed!

Also foreign buyers that are resident ie students and temp workers

Why does the university classify foreign students as foreigners and charge them extra

yet for some reason foreign students buying properties are not classified as foreign buyers ?

In australia foreign students buying properties are classified as foreign buyers.

"What I will confirm is that if you are willing to take advice from knowledgeable people with a track record then you are more likely to prosper than from listening to negative speaking people who always find fault with everything."

Yet you refuse to do this for equities based purely on your own admitted previous poorly advised experience. If property investing is working for you as you are so adamant then fine, but you need to recognise that it isn't right or appropriate for everyone and rubbishing share investing then posting statements like the above is making you come across as a hypocrite.

Here's a press release from Labour Finance spokesman Grant Robertson on DTIs.

Government failure on housing crisis drives Reserve Bank to add tools

If the Government was delivering a comprehensive plan to fix the housing crisis, it is unlikely that the Reserve Bank would be continuing to pursue debt to income limits for lending for housing, says Labour’s Finance spokesperson Grant Robertson.

“A Labour Government would be implementing our plan to fix the housing crisis, including building thousands of affordable homes through Kiwibuild and the Affordable Housing Authority, and cracking down on speculators through taxing the capital gains of those who sell investment properties inside five years and banning offshore speculators.

“The National Government is failing to act in these areas, and has effectively outsourced housing policy to the Reserve Bank. The Bank is now pushing ahead with a desire to implement debt to income ratios, but the government has asked for ‘more information’.

“This looks like National stalling for time as it desperately searches for a response to the crisis. “We have concerns that blanket debt to income ratios will exclude even more first time buyers from getting into a home. More than a third of lending to owner-occupiers in the year to May was at a debt to income ratio of five or more. This includes many first home buyers. If ratios are applied across New Zealand that will also shut out those in regions without the over-heated market we see in Auckland.

“The Reserve Bank is rightly concerned about the effect of the housing crisis on financial stability but they are being left alone to deal with it by a Government that has simply lost control of the issue.

“It is clear they do not have a plan, and the only answer is to change the Government and see the implementation of a well thought through set of policies that will give New Zealanders the security and opportunity of stable and affordable housing,” says Grant Robertson.

43 percent investors over DTI 6, only 9 percent of FHB over 6, 75 percent of FHB have DTI levels under 5. (RBNZ.) . A DTI measure will blow investors out of the market , prices will fall. Possibly the RBNZ should adjust the percentage of servicing on interest only loans too kick investors while they are down.

I recall some horrendous percentage of investors being over 20% LVR and then 30% LVR and then 40% LVR, etc. The thing about fiscally prudent people is that they tend to be prudent enough with money to not waste more of it than necessary on something that doesn't need it. Should the need arise they generally have the resources to meet it :)

Investors tend to take greater risks than fence sitting FHB's...why would you live in a house you own anyway? Much cheaper to rent than own a house I can assure you.

Houses are meant to be HOMES something they are increasingly less becoming. People want somewhere to settle, raise families, have decoration they choose, gardens, keep up their own maintenance, not have to go begging to a greedy landlord.

I look forward to a brave government that will put all this ridiculous stuff to rest, that will change legislation so once again home ownership becomes the norm and rapacious investors are set back where they belong!! Those words of yours have cemented my determination to see an end to all of this!!

Good luck with waiting for the government to sort things out. Actually the government is filled with people just like you in both houses. Have you considered the Alternative-Right?

Alternative right, sounds like left to me, might give it a look.

Yes the classic Left/Right thing is an outdated dichotomy. Just stay away from Libertarianism, they're crazy mofos.

Libertarianism is the ultimate goal, the nirvana if you like, and if we all lived by the mantra of "do unto others" libertarianism would happen all by itself.

The problem with the word libertarian is that is has been hijacked by the crazy right.

No, left and right are not outdated, it is just people no longer understand what they mean. I'll give you a chance to define them before I do. It can be done in one or two sentences.

The true Right is nationalist while the Left is globalonian (I want this word to go mainstream -global/baloney). Both can be socialist as, after all, we live in a social environment. I don't see how you can achieve what you want without embracing some nationalism.Trump is an alternative to the classic Right who are sellouts.

Wrong, left and right are economic terms only, right is the economy of the individual, left is the economy of the collective. That is it, nothing more, anything else is an add on. Left and right can live quite happily together, at its simplest, an individual going out to work who then brings his/her income home to share with the collective (family). Beyond that it is just how many it applies to, from one family to a whole country and everything in between. A mixed economy in a nation is simply left and right economies being blended together. Everything else is just an add on, most often in terms of personal freedoms, at one end libertarian at the other totalitarian, these two things live less comfortably together than left and right.

The globalization thing, if we were all on the same page, especially where personal freedoms go, would be just fine with a few protections in place for locals in any one country or another, like say, housing, and border protection where nasties like foot and mouth go. The human race is simply not ready for globalization with so many variations on the theme of what is right or the truth. Much, much more acceptance of each by ALL is required before we can go down this track.

Your definition of right is far, far more warlike than your left. The right that you define is turning pretty damned psychotic.

It should come as no surprise that people who identify with the left are more open to a global world, we just have to recognize that we still have lots of work to do before we are ready for it. War, sadly, may well precede that.

From this week's Listener, from a study published in Scientific American "People who are open to new experiences tend to be left-wing voters, and those who prefer structure and certainty tend to be right-wingers".

Feeling pretty good about being lefty after reading that.

I would agree with the Scientific American study. What's the next stage? Neo-Feudalism? I'm rather looking forward to it.

I'll just bet you are.

OK had a look, should have known better, has the word "right" in it, looks pretty bizarre and racist to me, not really prepared to look any harder than that. Are you a card carrying member, then?

Many many people actually have homes whether they own it or not. Most of my colleagues own their own homes but they don't post comments here announcing to the world they own homes. All the noise we hear are from a small fraction of the society who are either jealous or unhappy in their lives.

It looks like you are trying to marginalise peoples opinions because you disagree with them. Denying problems doesn't make them go away.

If thinking that others are just jealous of you or are unhappy helps you through the night, who am I to argue, but I will tell you, you are wrong.

Keywest. In Auckland and some other parts of te North Island is cheaper to rent than own.

However in Christchurch providing you buy right, with interest rates as low as they are and likely to stay low, you can own for less than renting!

Just listening right now to Paul Henry interviewing Linda Surtees about fostering children and how the government is seeking about 1000 new foster parents and the difficulty they are having finding them and the cost. I am going to put it to you that fostering and renting are very likely to be incompatible, given the precarious nature of renting in this country and the need for stability for children being fostered.

I have just found another reason why turning NZ into a nation of renters for the advantage of a few, MUST be greatly curtailed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.