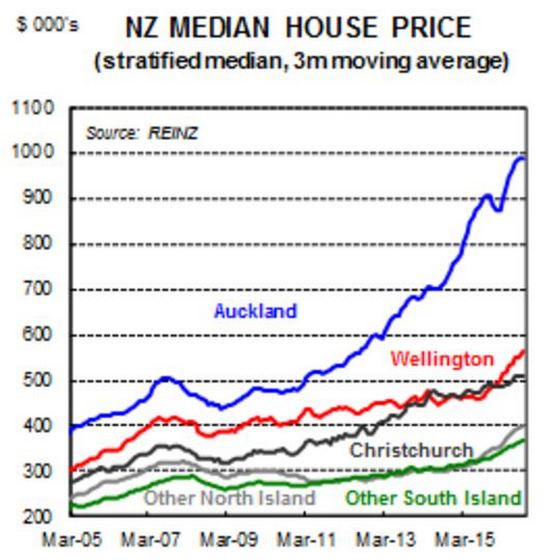

There was a two speed housing market in September, with median selling prices falling in Auckland but rising in most other regions, according to the latest Real Estate Institute of NZ figures.

The median selling price in Auckland dropped to $825,000, down 2.1% from its all time high of $842,500 in August.

However it was still 7% up on where it was in September last year.

Within the Auckland region median prices were down on the North Shore -2.4%, Waitakere -5%, Manukau -4.3%, Rodney -5.3% and Papakura/Franklin -1.9%, compared to August.

Only the central isthmus suburbs (within the boundaries of the former Auckland City Council) recorded a rise (+3.9%) for the month.

Fresh record high prices elsewhere

But it was a different story in the rest of the country, with new record high median prices being set in Northland, Waikato/Bay of Plenty, Taranaki, Wellington, Nelson/Marlborough and Otago (you can see the regional price trends on the interactive chart below).

That propelled the national median selling price to an all time high of $515,000 in September.

The median price for all areas excluding Auckland was also at an all time high of $400,000.

There was also significant differences in market activity in Auckland compared to the rest of the country.

In Auckland 2424 homes were sold in September which was barely changed form August, but down 23.2% compared to September last year, suggesting the usual spring pick up in sales has bypassed Auckland so far.

There was also a sharp drop in the number of sales in the Waikato/Bay of Plenty, which were down 9.5% compared to August and -22.5% compared to September last year. In Otago sales numbers were down 6.8% on a year ago.

But compared to September last year the number of sales was up in Northland +4.2%, Hawkes Bay +1.1%, Manawatu/Whanganui +23.7%, Taranaki +3%, Wellington +12.5%, Nelson/Marlborough +2.9%, Canterbury +10.2%, Central Otago Lakes +10.6% and Southland 33.1%.

Overall there were 7397 residential sales in September which was down 10% compared to September last year.

New LVR rules take some heat out of the market

ASB economist Kim Mundy said the Reserve Bank's latest round of investor-focused loan-to-value ratio (LVR) restrictions has taken some heat out of the market.

"Banks were obliged to start complying with the spirit of the new restrictions ahead of their official [October 1] implementation. We expect to see activity remain subdued over the rest of the year as investors up and down the country come to terms with the new rules. These data have no implications for our Official Cash Rate view. We continue to expect the Reserve Bank to cut the OCR by 25 basis points in November," Mundy said.

Mundy also noted that nationwide, the seasonally-adjusted median days to sell lifted for the first time in five months. In Auckland, the seasonally-adjusted median of days to sell lifted to the highest level since August 2014. Even in Wellington, the tightest housing market for some time, the median of days to sell lifted from 24 to 27.

"The lift in the time taken to sell homes comes off the back of a widespread fall in sales activity over September. Seasonally-adjusted sales fell in all regions over the month of September except for the Central Otago Lakes District and Canterbury. Interestingly, the nationwide stratified median sales price lifted in September to $521,150. The stratified median house price also lifted in Auckland (up 2.1% month-on-month) and Wellington (up 4.8%)," said Mundy.

"Despite the slowing in sales over September, inventory levels remain below historical averages. As a result, pressure will likely remain under house prices until supply catches up with demand. In general, recent housing market activity has been supported by robust demand and limited supply. However, the latest round of investor-focused LVRs appears to be weighing on market activity. We expect this to continue to suppress market activity over the remainder of the year,"Mundy added.

You can see REINZ's full regional sales data and commentary by clicking on the following link:

Median price - REINZ

Select chart tabs

The chart below comes from ASB.

64 Comments

The median selling price in Auckland dropped to $825,000, down 2.1% from its all time of $842,500 in August.

Cripes, has a central plank underpinning RBNZ's misguided monetary policy just snapped in the largest metropolitan distrlct?

Persistent inflation, like low interest rates, has become a tool policy-makers use to minimize the burden of debt. As a simple example, assume a household earns $50,000 a year and takes on a $500,000 mortgage. Servicing such a debt will dramatically reduce the household’s appetite to consume and their capacity to take on additional debt. Inflation, however, can change their situation. If the value of the house appreciates 10% per year, then in five years the house would have increased in value to over $800,000, rewarding our borrower with over $300,000 in equity. Even though the household’s income did not increase, the presence of additional equity in the house allows the household to borrow more and increase consumption. Read more

Surely no central bank or self-respecting economist could be so unprincipled or so shallow as to think that this mechanism of wealth transfer by inflation could possibly be a good thing.

Fact is stranger than fiction.

The US is awash in economic data that shows its economy isn’t close to matching the rhetoric of policymakers. FOMC minutes for the September policy meeting show largely what I have been writing for almost two years. Rate hikes aren’t about the economy as it is, they are about the economy that “should be”, the one that “full employment” denotes where it is about to take off into overheating. That is why central banks move toward tightening as a matter of policy; they look at today and figure what that means about tomorrow. Read more

So where to from here for FHBs? Dive in (if you can) or wait? Advice gratefully received

in a market with more than 40% being speculators and at risk of panic selling if the downwards trend continues.. what do you think?

I would wait and see if this is already the bubble burst because if it is there won't be soft landing (although there will be plenty of FHB that were waiting for a breath to make the mistake of jumping in). But media and real estate will soon start repeating "now it's the best time to buy", "finally FHB can get a chance", etc.

Personally I would never buy a house to live in it in Auckland unless prices fall at least 50%. And even then I would be careful to sign a long mortgage given that we are at the end of one of the longest expansion cycles since the WWII and another crisis is around the corner (only this time with less tools to fight it since interest rates haven't increased)..

The Auckland property market is overvalued by a multiplier of 3. This is based on the weight of a sparrow's fart in 1936 compared with the number of fleas on my dog dingo as at 2016. The Bubble Index indicates that peak poppiness has yet to be achieved and should occur in approximately 2,000 years (right before the arrival of the Klingons).

My advice... hold off until 1 April 4,016.

Now entire NZ is speculator's paradise - Tax free.

When House price touched median one million dollar in Auckland was advised by government to leave Auckland and now what and where.................leave NZ.......

Seems like it.

Warning: the following is a Difficult Concept For Aucklanders!

In the rest of the country, when the property price goes up they build new homes. Land prices are much lower, so when the price of property increases they can pay builders way more money and build homes much faster.

Last year, at much lower property prices, Bay of Plenty and Waikato were building more homes per capita than Auckland. Next year, they will build even more.

that's why possibly in those regions the prices will fall even more than in Auckland.

At the end of the current global low interest boom, all prices are going to fall. Tauranga, Hamilton, Brisbane, Melbourne - where they have constructed new office space and homes will see prices fall and rents fall. Auckland will see prices fall and rents stay high. Every corporate accountant from NY to Singapore to Beijing will be looking to cut costs. Which town will have the best track record of economic growth to office space rental costs ratio? Which will have the worst?

I think the town with worst bottom line will have prices fall off a cliff. I think that town is Auckland.

Wow expert1 you are not much of an expert. You are not the only whinger on this site. Very little to Non of the property bought by these property speculators will be tax free. In most scenarios the only property purchased that won't be taxable is property bought either as a home to live in or as a rental. To me a speculator is someone who purchases a property with the intention to sell in the near future at a profit which IS TAXABLE!!! I am sick of reading all of the moaners comments here stating that people are getting away with mega capital gains tax free. Read the income tax act people. Review section CB.....

Auckland has just adopted a Unitary Plan that will allow a city of about 1.1million people to grow naturally over the next 35 years. The only small problem is that Auckland is a city of about 1.3million people currently. So today Auckland's supply restrictions mean high prices, but people can move.

Over the next 35 years about several 100,000 people will be moving away from Auckland to other places. In the short term there will remain high upward pressure on Auckland land price and in the long term there will be large downward pressure on Auckland land pricing. Sometime in the mid term there will be a transitional phase, as house prices in Auckland move towards parity with non-Auckland in probably quite an abrupt manner.

I recall saying recently that now was a good time for the speculators in Auckland to take some money off the table and get rid of those rentals that needed repairs and maintenance and/or those rentals where those pesky tenants did not stay for long. Am I being proved correct in my predictions? Time will tell. One thing for sure some FHBers are staring down the barrel at reducing equity to the point that they might need to inject capital into their homes to keep the Banks at bay. Banks are really just landlords using another name and they can get nasty when their tenants do not follow their rules.

One thing for sure some FHBers are staring down the barrel at reducing equity to the point that they might need to inject capital into their homes to keep the Banks at bay.

Or ultimately, unsecured bank liability owners (depositors) staring down an RBNZ triggered OBR haircut to match the write down of grossly over valued bank mortgage assets.

No bank will call in a loan if your property is in negative equity. NEVER. So long as you're making the mortgage payments it's not in their interest for the house to be sold.

.

Depends on how hard the market falls OU. If the Bank think it is going to keep falling are they just going to sit there and watch their security position deteriorate. They are ruthless bastards when it comes to looking after themselves. Us peasants who pay them rent always come off second best.

of cause banks will call in loans, they have to adhere to tier requirements so they will liquidate positions to ensure they stay inside the requirements.

at the end of the day the bank works for the shareholders not the customers. either depositors or borrowers

Why would they call in the loan when they can instead do a margin call and just get you to top yourself back up to positive equity instead?

Just think about that question for a minute, in the context of things...

A liquidity crisis is called a liquidity crisis for one reason.

So your saying if I continue to pay my mortgage the bank Wil still take my house off me?

[Quit the insults. Stick to the issue. Ed]

When the banks experience "liquidity difficulties", they'll liquidate you. They entrench this possibility in their loan documents for a reason. Your good custom means zilch to them. When it's in their interests, they'll destroy your family. For more information, refer NZ Farmers, circa 1985.

[insult edited out. Ed]

[I know it was provoked, but insults are verboten here. Ed]

Sweet as sorry☺☺☺

Not like you are in Aussie anymore mate.

@gordon - "Am I being proved correct in my predictions? "

No.

Another case of "premature speculation" [ insult removed. Ed]

Time will tell whether the tide is turning. JK will turn the screws even further than 40 per cent if he thinks it will help him win a fourth term. Or bring in DTI rules. Will American and European interest rate increases allow us to increase ours. Time will tell.

the signs are all there, a crack down on immigration (reducing demand), banks reducing credit (reducing supply of money) and cutting staff, wage growth low

a government losing support and may be changed within a year

all you need is to restrict oversea purchases which could happen under a different type of government and POP down she will go

..and interest rates at or near their lows.. (falling interest rates generally translate to increasing capital growth).

I bet a lot of the increase outside Auckland is being fueled by Auckland equity.

Still one months data (esp one month where the LVR rules effectively changed) I wouldn't rely on to make decisions. It does seem like the double digit % growth of Auckland prices is a long way off now though.

One month, people.

Just look at the trend to see how crazy it is to be speculating on the fate of the housing market after the release of one month's worth of data.

From what I am seeing and reading the 40% deposit requirement has stopped speculators in their tracks in Auckland. JK and his MP's know the election will be won or lost on housing affordability issues. If the 40% rule does not cut the mustard they will impose even stricter rules. Politicians will do anything to keep their seats. And their perks also of course.

Purely anecdotal.

I can understand where you are coming from, but look at the trend relative to the introduction of other restrictions.

Buy location, location, location. Central Auckland prices will probably hold. Those who bought in the more peripheral areas will probably get burnt.

On the basis of what are you making this assumption?

closer to work places is one reason.

I was more referring to timeframe - short/medium/long.

I don't think that it is fair to say that in the case of a downturn only the peripheral suburbs will be impacted. Especially without giving a term indication.

"Only the central isthmus suburbs (within the boundaries of the former Auckland City Council) recorded a rise (+3.9%) for the month." I wonder what happened to the commentators like Nick Arand who gloated about how they managed to sell their Mt Eden villas for $700K in 2008 and everyone who held on to theirs was a fool?

Congestion is only going to get worse and people will pay a premium to be central to be closer to work. Also in the central areas you will see the greater intensification.

Sales for 2.5m+ seem ok at the moment due to wealthy immigrants. The mass market is overpriced and has peaked imo.

Yea, that doesn't support your notion.

True about congestion, but I don't think that will have as much of a premium as it has had due to new infrastructure coming on board.

Intensification will result in lower average/medium prices.

"Sales for 2.5m+ seem ok at the moment due to wealthy immigrants. The mass market is overpriced and has peaked imo."

Doesn't that just say that the prices will decrease, also?

Have we reached Peak Tribute? Meaning the maximum that kiwis can afford in yearly payments to the foreign banking system?

http://www.rbnz.govt.nz/statistics/s7

This shows the total banking system debts as follows:

Year to Aug 2014 Total debt $365,562 million Interest Rate 5.96% Interest Paid $21,787 million

Year to Aug 2015 Total debt $390,264 million Interest Rate 5.66% Interest Paid $22,088 million

Year to Aug 2016 Total debt $422,046 million Interest Rate 4.92% Interest Paid $20,767 million

The last column is strangely not present on the RBNZ site. Presumably because we might conclude that their only real function has become to modulate the interest rates to a level that kiwis can afford. What else can a regulator responsible for a country captured by the shear weight of debt overhead do?

It looks like the maximum kiwis can afford in interest payments per annum is about $21billion.

There is the delusion that lowering interest rates somehow mysteriously helps inflation wipe out the real value of debt. Instead what we are seeing is that the debt just rises to keep the interest paid as tribute at the maximum.

Yep that is about how it works. Interest rates keep dropping to compensate for the growing debt, until they can't. The market will always find the maximum extractive value, call that the natural interest rate if you like :-)

"Peak Tribute" That's a great term Roger. It seems nuts to me businesses, eg the 'investors' eg dairy send a vast portion of their income away as interest.

Imagine if we worked from a well capitalised basis, sending no interest out of the country.

The nation would be rolling in cash, incomes would be high, and when spent that cash would make business boom. Magic.

I rather liked Scarfie's " maximum extractive value".

Thanks for posting those figures - they make for interesting thinking.

Peak Tribute = Impending Punishment (or abandonment to our fate).

All consistent with the RBNZ C16 data. Mortgages are not increasing in size , without which Auckland prices will fall , as there simply is no such thing as a plateau in a speculative market. The media will only headline price falls in yonder time , by which time many will realise its too late to remove their profit from the market, as the door closes. Delusional economics, its all very simple, particularly the human mind .

Your call on C16 was noted the first time you brought it up, good work on that. Note also that the rate of change in the M3 money supply has also been dropping for 12 months now.

Scarfie , have taken your comments on board. Like yourself I am not one for hyperbole and simply post my views as I see them although (occasionally I will throw in a curve ball). I like to plonk snippets every now and then and see where they go, particularly currencies/ hard data.

I think the door to exit the Auckland property market, will morph into a cat flap as it begins to close.

Banks would be unlikely to ask for an equity top up from owner occupier making mortgage payments. But, reasonably normal with investment properties to review and state below equity requirements (if purchased at 80% LVR will require top up to keep LVR at 80% or below). If investor does not have adequate funds, typically requires sale of investment property/ properties to get portfolio back to target LVR. Banks have twitchy trigger fingers if prices correct, especially if negative cash flow properties. As most large losses occur with failed investment portfolios. They will also carefully review portfolios owned by those who derive income from property sector eg real estate agents, mortgage brokers, house stagers etc.

Yes I'm not going to hold my breath about the Auckland property market cooling. Just looking at the Bayley's auction results a few days ago (Quote from article):-

In Auckland Bayleys took 21 homes to auction and sold 16 of them, achieving a clearance rate of 76%.

Of those that sold, only six sold for less than $1 million, and the cheapest auction sale for the week in Auckland was a one bedroom apartment in Parnell that went for $523,000.

The most expensive sale of the week was a house in Mairangi Bay that sold for $2.45 million.

What we really need to know is "who" is buying in Auckland, I'm guessing it isn't the locals not at these prices.

Any chance we could get some stas on Auckland's foreign buyers David, or is that information strictly on a need to know basis? According to Mr Key we don't need to know.

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11728095

Not all well in NZ Housing....

I'm not sure whether to laugh or cry at that news about the Government running out of money for housing?? That's crazy!

Quote from article: The Government's state housing agency is set to run out of money by February, ministers have been warned.

Housing New Zealand has also told Finance Minister Bill English that it will have no cash for developments or to maintain houses past 2017/18.

Well perhaps if we actually TAXED foreign property buyers they wouldn't have this problem!?

CJ you do realize that these overseas property buyers will have to pay tax on the capital gain on the sale of any property they bought within NZ if sold in under 2 years? also if they didn't purchase it as a rental which a lot of them bought and are currently holding empty it would be hard to argue they bought without an intention to sell for profit therefore they will be taxed. Infact if you apply the brightline test if they sell the property in under 10 years it is highly likely that the property sale would have been taxable. Of course there are a lot of mitigating factors that exclude a property sale from being taxable but it would be very hard for overseas buyers to get around it legally.... Im not saying that just because overseas buyers legally should be paying tax on the sale of property that they actually are... No one but the IRD could work that out.

@ bgballz: Well evidently it seems that CGT isn't enough to help support our coffers for urgent Government programs such as building new homes. It's fish in a barrel time and I hope the political opposition really tear in to National for this oversight.

Also we need to tax all the empty homes that foreign investors tend to sit on, they should be taxed if they're empty for longer than a year - follow Vancouver: http://www.cbc.ca/news/canada/british-columbia/vancouver-vacant-home-ta…

.

CJ why do we need to copy other countries taxation policies? That makes us Sheep...... And reactive. Why plug holes in reaction to buyers habits for short term relief when you can fix put in place mechanisms that will be effective for a long period of time. I Agree those empty homes are wasted sitting empty when they could be housing people who are living in cars and garages. Do i believe if those empty homes were rented out they would reduce rent values in Auckland.. Not likely. and those people living in garages and cars would not be able to afford the rent charged on those properties anyway. It looks like government is never going to try discourage foreign investment maybe due to free trade agreements and our relatively weak bargaining power when it comes to trade. Tools within our control are government should look at every property transaction and assess the taxabiity of that property before funds are sent offshore or spent (Imagine the revenue pay back per employee the IRD commits to chasing these tax dodgers). The government should also encourage growth in the regions (Especially Big business) and promote it better as there are plenty of jobs in the regions that immigrants have to fill because everyone wants to live in the city.

We're only sheep if we do nothing!! And it's idiotic not to utilize standard revenue generators that are used globally. Even more idiotic to let the housing market to run out of control and beyond the reach of most NZ residents as it clearly has been doing and with continue to do without any standard safe guards.

Taxing empty homes has a huge impact in freeing them up for rental or sale - either way it puts less pressure on the housing market. And there's really no excuse for leaving a home empty for longer than a year unless you're going through probate in which case they can be classed as a special case.

I think your missing the bigger picture... There are multiple stakeholders here investors NZ based, Investors overseas, FHBs already in the market, FHBs looking to buy, Renters, Exporters, Tradesmen etc Some of them are are happy with the increase in pricing business is booming and they are providing jobs, some cannot afford a property crash, some have been priced out of the market for now (I'm picking you are one of them?) your suggestion will create unnecessary instability in the market and affect more than one of those stakeholders. You need to take a step back, chill and realize that there are other measures the government can implement to help FHBs and renters. Remember there is more than one way to skin a cat.

Really; so your answer is to sit back and do nothing, how very National of you. Well I'm not like you, I'm very pro active and yes I have been through a property crash before, and you know what those trades people you mentioned come up smelling of roses, they survive quite well.

The ones that do suffer during a property crash are the Estate Agents - sorry but I can't feel any pity for them.

And by the way, there are no first time buyers in Auckland any more not unless they have very wealthy parents.

Foreign Buyers and empty homes need to be taxed it's as simple as that!

Please feel free to list any schemes that National are bring in to help FTB’s?

I think we will never agree on anything. You're too emotionally involved.

Don't worry im sure you should be fine as you, me and the rest of the FHBs will be able to buy our first home once this property bubble bursts that alot of people on here is predicting. ;-)

I'm actually an Auckland home owner but would still welcome a property crash.

Don't you see we need FTB's that's a healthy property market if they can still afford to buy without having to rely on the bank of Mum and Dad. Otherwise allowing the property market to become decoupled from wages is very foolish and it's not you that I'm angry at, it's the do nothing National party.

If I seem emotionally involved, it's because I can see how extremely high house prices are killing my industry and a lot of others in Auckland. Skilled and well educated migrants won't move here unless they can afford to live here and unfortunately we're now having to export our young kiwis too.

CJ great comments..... madness doing nothing while others act

Vancouver tax 15%

Foreign buyer = student + temp workers + off shore

New builds exempt

Apply to foreign buyers and 2nd home purchase by nz citizens.

Vacant home tax on empty properties

Loan to income ratio 4 to 1

Prices up 500k under john key in auckland

More than all former pms combined

Debt 250bn and growing at 8.8% pa

Foreign students and tenp workers bought 13,500 homes last year. 30% of resident buyer total.

2007 john key called it a housing crisis

2016 prices up 500k in auckland

He failed to solve the crisis

Govt debt 2007 10bn

Govt debt 2016 over 100bn

Yep Key is a failure, a 'loser'

Why? because he failed big time on his 2007 promises

'

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.