Mortgage affordability for first home buyers continues to improve as mortgage rates and house prices at the bottom of the market both continue a slow but steady decline.

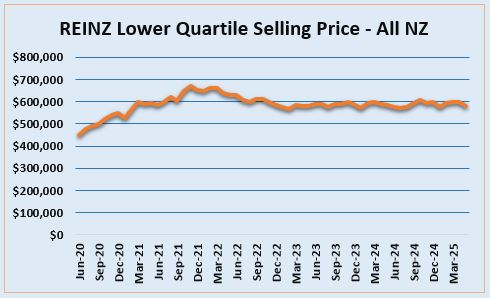

According to the Real Estate Institute of NZ, the national lower quartile selling price was $580,000 in May, down from $599,000 in April.

The lower quartile price - the price point at which 25% of sales are below and 75% are above, representing the most affordable end of the market - has declined by $90,000 (-13.4%) since it peaked at $670,000 in November 2021 - see the graph below for the monthly trend.

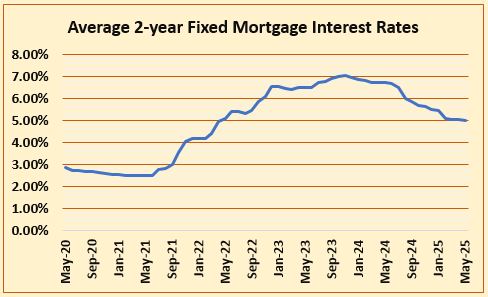

At the same time mortgage interest rates are tumbling, with the average of the two year fixed rates offered by the main banks dropping to 5.01% in May, down from more than 7% in late 2023 - see the second graph below for the monthly trend.

That combination of lower prices and falling interest rates means the mortgage payments on a lower quartile-priced home are now at their lowest level in almost four years.

Interest.co.nz estimates that the mortgage payments on a home purchased at the national lower quartile price of $580,000 with a 10% deposit, would be $738 a week (at 5.01% plus a loading for a low equity loan with a 30 year term), down from $886 in May last year, a saving of $148 a week (-16.7%) over the last 12 months.

Those mortgage payments have declined by $197 a week (-21.1%) since they peaked at $935 a week in November 2023 and are now at their lowest level since October 2021.

If the same property was purchased with a 20% deposit, the estimated weekly mortgage payments would be $575 a week, down by $165 a week since the November 2023 peak and also at its lowest level since October 2021.

Of course, affordability is not just affected by changes in prices and interest rates, it is also determined by income levels.

Interest.co.nz tracks how much a couple would earn (after tax) if they were both paid at the median rates of pay for 25-29 year olds and were both working full time.

Since mortgage payments peaked in November 2023, that estimated, combined after-tax income has increased from $2053 a week to $2195, providing an extra $142 a week (+6.9%) in take home pay.

That increase in income, combined with lower mortgage payments, means the percentage of income eaten up by mortgage payments (the most important measure of affordability) has declined from 45.5% in November 2023 to 33.6% in May 2025, assuming a 10% deposit.

If the home was purchased with a 20% deposit, mortgage affordability has improved from 36.0% in November 2023 to 26.2% in May 2025.

A general rule of thumb is that mortgage payments are considered unaffordable when they chew up more than 40% of after-tax income.

By that measure, mortgage payments for homes at the lower-priced end of the market are now squarely into affordable territory for couples earning pretty average wages.

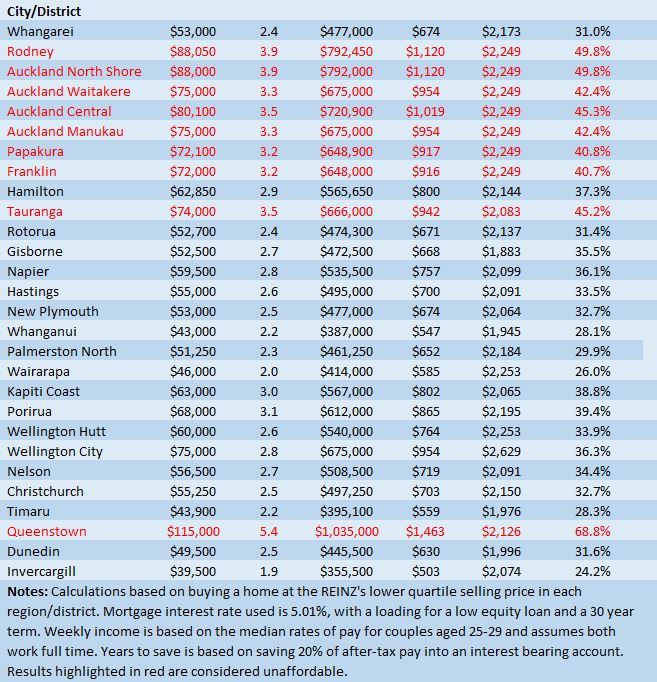

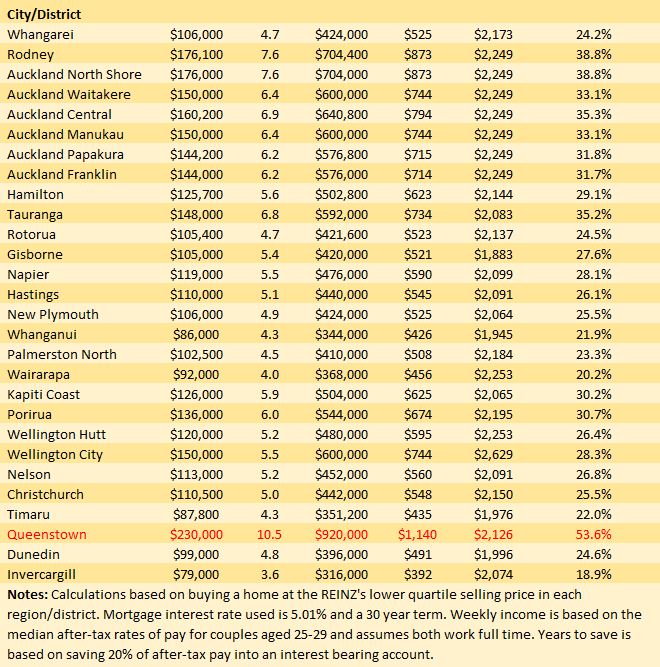

Of course the calculations above are based on the national lower quartile price, and this varies greatly around the country.

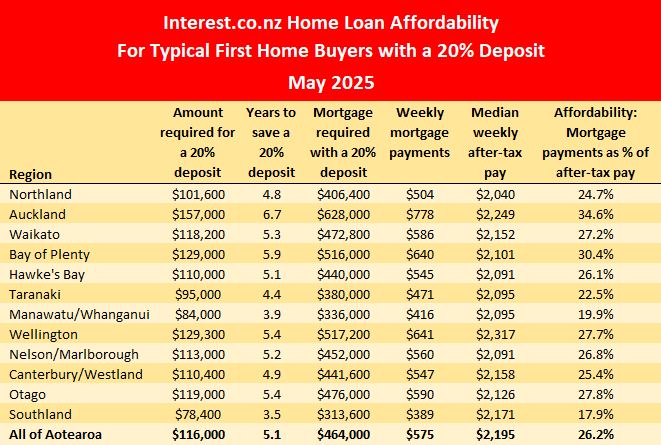

The tables below show the main affordability measures for all the main urban centres around the country.

These show that if the buyer has a 20% deposit, then mortgage payments would be affordable in all parts of the country except Queenstown, where astronomically high prices put home ownership out of reach for all but the most highly paid.

However if the buyer only has a 10% deposit, then all of Auckland, from Rodney in the north to Franklin in the south, plus Tauranga and Queenstown, remain in unaffordable territory.

That suggests that scraping together a sufficient deposit is now the biggest obstacle to home ownership, rather than the size of the mortgage payments.

At the regional level, the amount needed for a 10% deposit on a lower quartile-priced home ranged from $39,200 in Southland to $78,500 in Auckland and you can double those figures for a 20% deposit.

The tables below show how long it would take to get that deposit together if the aspiring home buyers were able to save 20% of their after-tax pay each week - using the median pay figures described above.

For a 10% deposit this would take less than two years in Southland and almost three and half years in Auckland, and double that for a 20% deposit.

Of course saving that amount of money each week is not an easy ask, especially when budgets are already being squeezed by high living costs.

But there's no way around it, getting that deposit together by whatever means remains the key to securing home ownership.

The comment stream on this story is now closed.

10 Comments

So 5% further fall in prices and a 5% increase in wages will make Auckland affordable again.

5% wage increase is tied directly to the engine of inflation. This drive up rates go and with it the cost of debt. Aka a zero sum game with FHBers. This only bails out the leveraged and set the Banks up to suck another geneation dry.

Aka a zero sum game with FHBers.

Unfortunately, it's not zero sum. That would be a best case scenario. Any income increases are neutered by the greater increase in the loss of purchasing power (broad inflation metrics are worthless), particularly among the profiles of marginal house buyers. It's not just these people who need to understand it. Other people need to understand it too as the behavior of marginal house buyers ultimately adjust the entire market, except among the absolute top end of the market (even though it indirectly impacts them).

Technically no it isn't zero sum, but politically yes it is.

NZ could both lower house prices and increase wages anytime it wants to by lowering non-wage building costs - land use restrictions and building type restrictions.

This is of course remains extremely unlikely to happen, given how invested our economy and our politicians are in housing.

NZ could both lower house prices and increase wages anytime it wants to by lowering non-wage building costs - land use restrictions and building type restrictions.

Yes. Non-market distortions.

BTW, City of Sydney BANS gas appliances for all new homes: 'Dirty fossil fuel that has no place in homes'.

https://www.dailymail.co.uk/news/article-14839979/City-Sydney-BANS-gas-…

didnt labour try that for new commercial kitchens?

NZ could raise wages by changing it's generational culture of paying pittance and failing to invest in their workers upskilling. Upskill workers and they feel valued, they stay, they they get paid more after a time due to the level of skill, and bring in more income for the business. Sadly the tendancy in NZ is to use the worker as long as possible and suppress wage increases to increase profit, then get another worker when they leave for better prospects.

Ex socialist, I bet you didn't expect so much resistance to your good news post.

Look at that REINZ selling price graph, the line is dropping so steeply down, it's falling into the abyss, truly the crash of the century.

Still slowly but steadily falling in inflation adjusted terms, which is probably ideal given the circumstances

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.