Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE RATE CHANGES

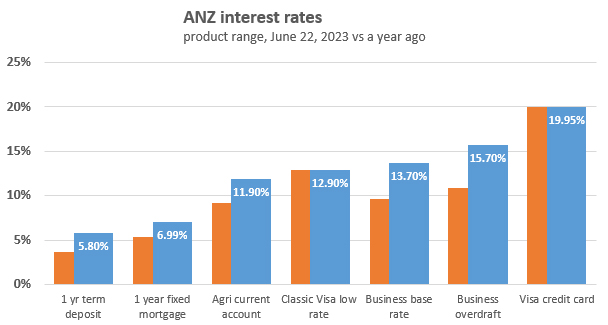

First Credit Union rated floating and fixed rates today. And ANZ raised some non-mortgage rate for business clients taking their Business Indicator rate to 13.7% and their business overdraft rate to 15.7%. Home loan borrowers, especially investors, must feel like they are getting a great deal. See this.

{kind=link}

TERM DEPOSIT/SAVINGS RATE CHANGES

ANZ raised most TD rates from 1 month to 1 year late yesterday. Their new 6 month rate is up +10 bps to 5.65% and their new 1 year rate is up similarly to 5.80%. Unity Money raised its 9 month TD rate to 5.60%.

PAYING OUR WAY?

Despite our export values exceeding the value of imports by +$46 mln in May, the running annual deficit hit a new all-time high of over $17.1 bln. The monthly surplus is more than -$100 mln less than we had in May 2022.

$1 BLN PAID SO FAR

Our $3 billion weather woes may linger for some time says the Insurance Council. They report a little over a third of claims have so far been paid out for the twin weather events early this year; warns some claims could take over a year to settle.

HOT DEMAND

Today's Government bond tenders were swamped with demand. And that drove yields lower (in contrast to recently rising secondary market yields). The May 2030 $200 mln offer got 50 bids totalling $820 mln, and the ten winners bid a yield of 4.50% and very similar to what it was in the equivalent tender two weeks ago (4.52%). The May 2023 $150 mln got 52 bids worth $739 mln and only 7 were successful. They took a yield of 4.52%, down from 4.58% two weeks ago. And the April 2037 $50 mln attracted 29 bids worth $199 mln. The 8 successful bidders here got a yield of 4.63%, down from 4.69% two weeks ago. So all up 25 bidders won something out of the massive $1.758 bln from 131 bids. That is 3.4 times oversubscribed.

IMPROVING THE FRAMEWORK FOR SHARING DATA

MBIE is seeking feedback on the Customer and Product Data Bill. This proposed new law will govern the sharing of consumer data. They say it "will give customers more control over their data, allowing them to safely and securely access, manage, and share this data with others. When businesses like banks, power companies and mobile phone companies provide us with services, data is created – for example, account histories, transaction records or information on usage. This is ‘customer data’. It is held by businesses and is protected by business security measures (as well as the Privacy Act 2020 in the case of personal information). Customer data holds enormous value and opportunity, but only if customers can make full use of it by choosing to share it with applications and people they trust." This summary isn't that helpful to understand what they are on about, so perhaps this will help? It seems it is creating rules so businesses can use the data 'safely' in the hope consumers will benefit. Anyway, it does deserve closer inspection, and now is the time to give feedback.

GOING FLAT

Although actual domestic credit card billings rose +$530 mln in May from April, on a seasonally adjusted basis they were lower and the trend isn't positive. Considering year-on-year inflation levels too, the longer term billing levels also tell a story of spending exhaustion. Keeping spending up is what we are putting on them overseas. More here. We've stopped paying down our balances now, ending a long 3+ year period of this virtuous behaviour. And in 2023 there hasn't been the drive to pay off interest-bearing debt that there has been since 2001 (pandemic excepted).

SWAPS RISE

Wholesale swap rates are likely ending today firmer especially at the longer end. However, the real action in swap rates comes near the close. Our chart will record the final positions. The 90 day bank bill rate is unchanged at 5.68% and +18 bps above the 5.50% OCR. The Australian 10 year bond yield is down -1 bp from yesterday at 3.96%. The China 10 year bond rate is up +1 bp at 2.72%. And the NZ Government 10 year bond rate is at 4.57% and up a sharpish +9 bps, and that is still much higher than the earlier RBNZ fix which was up +5 bps to 4.48%. The UST 10 year yield is now at 3.73% and down -1 bp from yesterday.

EQUITIES FALL

Wall Street was down another -0.5% on the S&P500 at the end of its Wednesday trade. Tokyo has opened its Thursday session down -0.1%. Hong Kong is closed and on holiday today (Tuen Ng Day). Shanghai is also closed for the same Dragon Boat Festival. The ASX200 is down a very sharp -1.5% in afternoon trade. The NZX50 is down its own -0.7% in late trade.

GOLD LOWER AGAIN

In early Asian trade, gold is at US$1932/oz and down another -US$6 from this time yesterday. It ended in New York at US$1933/oz, and earlier in London at US$1926/oz.

NZD RISES

The Kiwi dollar has firmed today from this time yesterday, up +40 bps and now at 62.1 USc. Against the Aussie we are up +60 bps at 91.4 AUc. Against the euro we are unchanged at 56.5 euro cents. That means the TWI-5 is higher at 69.9.

BITCOIN RISES FAST AGAIN

The bitcoin price has risen very sharply again today and is now at US$30,139 and up another +4.7% from this time yesterday. Institutional interest is said to be behind the move. And volatility has been high at +/- 3.6%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

18 Comments

The bitcoin price has risen very sharply again today and is now at US$30,139 and up another +4.7% from this time yesterday.

HNWIs and institutions front running on the 'good news' IMO. Few observations:

- Huge short positions taken out yesterday. TBH, no matter how much you think the ol' rat poison is garbage, shorting it is stoopid. Chances are you're going to get whacked at some point.

- The degenerates appear to be taking some profits on BTC and recycling into sh*tcoins. Some noticeable moves in all the junk. Bitcoin Cash was flying in Asia y'day for no apparent reason.

- Jerome Powell has partially thrown in the towel and mentioned at a House Financial Services Committee y'day that BTC and crypto asset class "appears to have some staying power" in the U.S. economy. That means more pressure on Pocahontas Warren and the SEC Chair Gary Gensler. Powell's comment is something of a rug pull on the Democrats' jihad against digital assets.

PEPE the frog coin was up 50% today.

I have a bit (up 400% I think plus earning a huge yield on it via liquidity pools - which I convert into BTC)

Quite a few fairly smart people happen to hold it. Next doge coin maybe? Worth having a tiny bit just in case maybe

Yes that Powell speech was quite something - WAY different to Glensler

Total credit card billings in NZ up only 3.3% YoY (not adjusted for inflation). Interest rates staying higher for longer will be more painful for households than the rapid tightening cycle itself.

Perhaps time for investors to make their money work harder in the productive economy than putting easy bets on housing.

Increased credit card spend is a 2nd-order effect of the bubble through the wealth effect. That's one of the reasons why housing bubbles are tolerated in the first place.

Also, a nice little earner for the banks.

Everyone says that w/out the Fed there will be no one left to buy USTs so rates will explode. Yet, there's an unending ocean of demand for safe and liquid assets. You can't get economists to understand what their central bank salaries depend on them not understanding. Link

It is amazing how much people still believe the Fed and central banks are tremendously powerful. Even mainstream studies show, for example, QT has such a pitifully underwhelming effect on interest rates. It underpins the idea many have USTs are toast w/out Fed purchases. Link

Curve inversions are really nothing more than these fundamental differences, LT rates pricing actual fundamentals as they are versus central bank policies that are set by non-economic sophistry. Like a "hawkish pause." Link

Perhaps the penny has dropped that we can't keep running our economies on a never ending cycle of Debt backed Asset Speculation.

Productivity leap needed to tame inflation, ANZ warns. Productivity will need to increase at a pace not seen in almost a decade for the current rates of wage growth to be sustainable. (AFR)

Investing in productive enterprise and industry would be a good start.

Edit: sorry, I mean "Change!"

Wage growth running faster than productivity gains - bad, authorities please intervene!

Growing business margins without productive investments or innovation (as in the case of ANZ) - good, let the free market run its course!

well its hard to get productivity improvements when banks lend for property speculation and not business operation

Would you lend money to some dude who thinks he can start a business? The risk profile is significantly different to property.

Absolutely I would. How else do you encourage innovation. Real innovation...not the kiwi ingenuity that we pride ourselves on (p.s it's not real). I know a young guy that's arranging a loan on a machine because he is passionate and the best young engineer I've done business with. Unfortunately he's financing his machine at 10-11% interest. He could be the next Elon Musk... who knows. With a solid business plan and a vision.. he should qualify for a very low interest rate on his loan and be encouraged to go big. It's your mindset that's holding this country back... no offense.

If the machine is genuinely an innovative productive winner with a sound business case,then 11% is small potatoes. A good piece of plant should be returning multiple times return on investment. It's not the interest rate that kills it, it's getting the money in the first instance.

The harsh reality is the path to profitability in a new business is very fraught. Failure rate for new businesses is 80-90%. Despite all the optimism in the world, that's a massive risk profile you can't overlook, and why there's not really a cheap way to get to a more productive economy.

Effectively for every dollar you subsidised new businesses in, you'd lose most of it for a handful of winners.

Unless you could pick the winners with a high degree of accuracy, good luck there.

I would and I do - both personally and via organisations like Icehouse which backs startups

Quantitative peopling doesn't have a good history of improved productivity outcomes.

Yup, let’s encourage productive investments in our economy before we worry about importing high skilled people. If the well-paying jobs are there, the right kind of people will come.

Fmr minister Wood, as his name suggests is as thick as two short planks. His missus isn't any better

Michael Wood’s reminders to divest his shares: A timeline

https://www.nzherald.co.nz/nz/michael-woods-reminders-to-divest-his-sha…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.