Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE/LOAN RATE CHANGES

Harmoney has raised rates today on personal loans.

TERM DEPOSIT/SAVINGS RATE CHANGES

None here today.

FOOD PRICE PRESSURE EASES

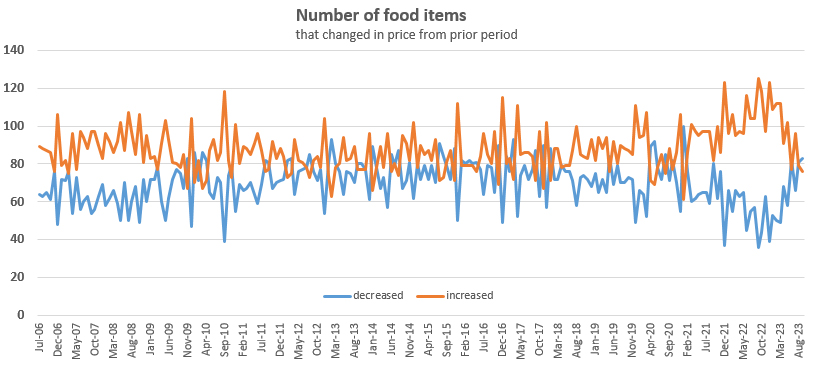

Food prices actually dropped in October, dragging the annual increase back to +6.3%. That is down from +8.0% in the year to September, and they peaked on this basis at +12.5% in June 2023. Stats NZ says food prices 'fell across the board in October'. Tracking food price changes shows that for the first time since 2020 we now have more items decreasing in price than increasing. (A click on that second link shows it clearly.)

{kind=link}

CAPITAL GAINS RETURN

QV says the average value of NZ homes is up by more than +$18,000 in the last 3 months. Property values are slowly rising in most regions with the biggest increase occurring in Auckland, where they were up more than +$33,000 (+2.7% in the quarter).

FOR CAR INSURANCE, SHOP AROUND

Consumer NZ surveying has found premiums for comprehensive car insurance have increased up to +38% since 2021. Cyclone Gabrielle occurred during this period resulting in heavy claims. Shopping around, especially when you are focused on coverage and conditions, may also be able to deliver lower premium costs. Consumer NZ found that switching car insurance providers could result in a family of four saving up to $670 a year on average. But be careful about just targeting premium cost - you may be giving up important coverage for those benefits. (Just for perspective, our largest general insurer's gross written premiums went up +12% in 2023 from 2022 which were up +7% from the prior year. So car insurance premiums rose faster than that overall. In fye 2023 IAG group tax paid profit was AU$832 mln. In fye 2020 IAG tax paid profit was US$435 mln.)

DTI RATIOS STILL DROPPING

Latest quarterly Reserve Bank figures show that ahead of the possible introduction of debt to income restrictions next year, new buyers are, in any case, mostly borrowing on low DTI ratios

HIGH HOUSEHOLD INCOMES REQUIRED

The average gross incomes of borrowers taking out a mortgage in September are rising. In September 2021, owner occupiers borrowing for their own house with a DTI ratio of between 4 and 5 had a gross household income of $144,000 on average. In 2022 it was up +21% to $175,000. And now in September 2023 it is up +13% to $198,000. For first home buyers the increases have been much more modest; the same 4-5 DTI cohort required a $131,000 gross household income in 2021. That was up less than +5% to $137,000 in September 2022. And now it is up to $146,000 in September 2023, a further rise of +6.6%. Those with gross incomes of $65,000 in 2023 got their mortgages on a DTI of 3, obviously having to have large deposits.

UP BUT TO WHERE?

The RBNZ says it is 'building towards a higher level of foreign reserves holdings now.' But Assistant Governor Karen Silk says there is no clear answer to the question of what the right level of foreign currency reserves the RBNZ should hold is.

SETTLEMENT BALANCES STAY UNUSUALLY HIGH

Bank settlement balances were $49.2 bln as at October, little-changed from the $49 bln a year ago. But that is six times higher than five years ago. They peaked at $56.4 bln as at December 2022. Remember, the RBNZ pays banks the OCR as interest on these balances. Over the past year, that amounted to $2.487 bln or 30% of the profits banks earned in that period

SENTMEMENT SAGS

In Australia, the widely watched NAB business confidence index fell to -2 in October from a downwardly revised flat reading in the prior month, pointing to the lowest level since May. However business conditions edged up.

BACK TO LESS THAN A DECADE AGO

Australia released its September short-stay visitor arrivals data today and they are still not back to 2013 levels yet, struggling to get to levels that existed a decade ago. They were 584,000 in the month, and the largest source was New Zealand (22%), followed by China (10%), then the USA (6%). Interestingly, short term tourists from New Zealand made up 22% of their September 2013 level as well. But tourists from China made up 12%. From the US 7%. So same basic mix, just less from everywhere.

SWAPS ON HOLD

Wholesale swap rates have probably changed little today. The real reaction will come at the close. Our chart will record the final positions. The 90 day bank bill rate is up +1 bp at 5.63% and now just +13 bps above the OCR. The Australian 10 year bond yield is up +1 bp from yesterday to 4.68%. The China 10 year bond rate is unchanged at 2.67%. And the NZ Government 10 year bond rate is up just +1 bp at 5.26% from yesterday, and the earlier RBNZ fixing was at 5.18% which was also up +1 bp today. The UST 10 year yield is now at 4.65% for a -1 bp dip from this time yesterday. The UST 2yr is now at 5.05% so that curve inversion is little-changed at -40 bps.

EQUITIES TURN BACK UP

The NZX50 is up +0.3% in late trade today. The ASX200 is up +0.7% in afternoon trade. Tokyo has opened up +0.6%. Hong Kong has opened up +0.3% and Shanghai has opened up +0.2%. The S&P500 ended little-changed on Monday.

GOLD STABLE

In early Asian trade, gold is now at US$1945/oz and up +US$5 from where we were this time yesterday. Earlier in New York it was at US$1946/oz and earlier still in London at US$1931/oz.

NZD SOFTISH

The Kiwi dollar has moved little today, still at 58.8 USc which is close toe where we were this time yesterday. But against the Aussie we are almost -½c softer at 92.2 AUc. Against the euro we are also a little softer at 55 euro cents. That means the TWI-5 is down -20 bps at 68.6.

BITCOIN FALLS

The bitcoin price is weaker today, now at US$36,387 and down -2.2% from where we were this time yesterday. Volatility over the past 24 hours has again been modest at just over +/- 1.5%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

46 Comments

If you haven't already, buy now folk, it's only the beginning of a steady upswing in prices, 10% in 2024.

Maybe half of that if you are lucky.

HFL will remain a barrier to prices shooting too much higher.

It's a ponzi which wasn't reconciled.

Round two, actually round several, cumulative.

What could possibly go wrong?

If yield curves accurately forecast market movements as they have over the past 50+ years - then I wouldn’t have any certainty or confidence about what direction house prices are going to head in (at least I wouldn’t say they are definitely going up from here! - yield curves would suggest financial problems are ahead of us near term) It’s possible they are still going to drop from here as we head into recession and unemployment rises, businesses fail and incomes drop.

But hey - who cares what the bond markets think when we’ve had 3 months of rising house prices!

Just as well that Harvey did not mention anything about house prices then ! He just said "buy now".

Do you think it was possible he was referring to MFB shares?

According to a few on here, joe public are adjusting quickly to HFL. Further price rises are locked in for 2024 and beyond.

This must imply no downward adjustments to interest rates would be required as this is a new normal of heightened prosperity atop expensive money.

Who would have thought....(chuckle)

Interest rates are influenced by employment and inflation, not whether mortgage holders adjust to the interest rate.

So the actual test is whether jobs and the economy can withstand these rates. It's certainly not an environment that screams "good time to establish or grow a business".

Agree IO and PDK. But hay, lets not let financial facts stand in the way of the stamped of greed towards to the nirvana of tax free capital gains.

I was with you until you mentioned CGT. The problem is massive deliberate population growth, not fiddling with accountancy. There's aready a bright line test for speculators, a comprehensive CGT doesn't stop housing bubbles, but it would force more borrowing on those shifting house!

This is where our understanding of the tax system fails. Ideally taxes are used to fund social services that the market can't or won't. It should not be used to manipulate people's actions, buy votes etc. If one wants behaviours modified there needs to be better learning/teaching that encourages and empowers one to change voluntarily. The fact that so many expend so much around not paying taxes is more a reflection of the person and the factors that influence this. It seems to be a massive issue in NZ and elsewhere that there is more upset over taxes paid than happiness with the gains one has. And it would appear it's the wealthier that moan the most. If tax is the biggest factor influencing financial/business decisions then either it's being done for the wrong reason or is not a viable operation. How this can be changed no-one knows.

We do not need a comprehensive CGT, but in order to balance the tax system, to lessen the inequities, the distinction between revenue and capital must be removed. If we're going to call it Income tax should not all income be taxed, no matter how it's derived?

It's a poor assumption capital gains on houses are automatically free of tax. It's the same as shares.

See here: https://www.ird.govt.nz/-/media/project/ir/home/documents/forms-and-gui…

Under the "intent" provision, many speculators have exposed themselves financially. Especially if they swiftly list when/if Brightline is removed.

Yeah - I'm a party pooper!

I was aware of that issue a long time ago. I was a tax professional and it irked me. The industry enables it too advising clients to say differently even though everyone knew for all intents and purposes it was going to be sold for the gain, even if held long term. When the 2 year brightline was initially implemented I had clients admit they were upset having to wait.

The issue seems to be one of evasion and enforcement.

Huge amount of evasion has gone on, but very little enforcement.

This is where our understanding of the tax system fails. Ideally taxes are used to fund social services that the market can't or won't. It should not be used to manipulate people's actions, buy votes etc. If one wants behaviours modified there needs to be better learning/teaching that encourages and empowers one to change voluntarily

Money is the simplest way to influence behaviour.

You can't really educate people to change, it has to be something the individual has a desire or willingness to do. It's why so many of us are fatties, drink alcohol, and behave in all manner of counter-intuitive ways, despite there being an overwhelming body of known information to the contrary.

We are mostly involuntary creatures of habit. Some scientists are now arguing to the point where free will is a complete fantasy.

Heck yeah! I am only two weeks in to a moderate attempt to lose 4-5 kilos, and discipline is already wavering in terms of diet, but the exercise is going quite well. I won’t be too disappointed if I only knock off 3 kilos, get the belly bulge down a bit

I find things have to be binary in order to change my behaviour. Not really able to moderate, so in similar conditions I just have to abstain from sugar totally. Or fast or drop a meal.

Good news is if you can keep doing the new behaviour long enough they often become a new habit.

Hence why I said better learning/teaching that encourages and empowers one to change voluntarily. Or were you just being argumentative for the sake of it because you've said the same thing in different words?

There's also plenty of science that suggests many of those challenges are related to deep seated emotional issues and maladaptive coping mechanisms, developed in early childhood. Much can also be said about the effects of advertising/propaganda that encourages one to partake of unhealthy foods etc. Alcohol is a prime example with the body of evidence suggesting against it's consumption but it's such a societal/cultural norm we don't want to limit peoples right to choose. Much is suggested that the access to technology and entertainment also have a greater impact. Science knows about the dopamine effect and so do the marketers. Free will is also greatly impacted by elements of structure and flexibility in ones' upbringing. Were they taught to exercise free will in an appropriate way that furthers their own self awareness? Do they know if they're acting from fear, shame, guilt, appeasement of others? Much could also be said about rigid authoritarian control structures limiting one's ability to exercise free will plus societal demands and expectations that develop in ones unconscious. Social constructs have a major impact. It takes great courage to go against unhealthy norms and that requires an inner power. I'd suggest the majority of humans are operating from learned behaviour and don't even realise it. It comes back to the nature vs nurture argument. Our "culture" no longer has the "spiritual" teachings/practices and initiations that empower the individual, that enable self realisation. Free will is not a fantasy, it just won't be easily accepted by the few that want to rule the many, hence better to not teach it.

As Einstein said "the intuitive mind is a sacred gift, the rational mind a faithful servant. We have created a society that honours the servant and has forgotten the gift." In many ways our education system and especially now the information age has simply filled the minds of many. Data and statistics is ruining the intuitive ability of many.

Money won't influence any of the above. For money to have become such an influence just highlights a greater issue with humanity. We've given our power and sovereignty away to an external god. It's been corrupted and used as a tool of power and control. For many it represses and limits their ability to make worthwhile changes.

Hence why I said better learning/teaching that encourages and empowers one to change voluntarily.

Do we want to ensure or greatly increase the likelihood of changed behaviour, or just make it a vague notion?

It has been said that much of our distinctive human frontal cortex is put into action justifying the more primal parts of the brain, that is guiding the bulk of our behaviour. We have advertising and social influences over our decisions, but underneath it all is the base hardware that is going to gravitate towards sugars, fats and salt, and the same addictive behaviours we succumb to are easily replicated in our less conscious relatives.

The leap you are talking about, where one is putting conscious effort into self awareness, is something humans have had extreme difficulty with even in far simpler times - hence the need to make maps to them in the form of religious text and ritual - and even under those unreplicable conditions in present day, for the most part the common layperson really struggled to adopt them, for most, it was reversion to blind faith, rather than genuine personal inquiry and awareness.

Essentially we are on a similar page in terms of personal philosophy. I dress in rags and my commercial peers consider me a street urchin, because I am not playing the same game of appearances and appeasement. I let the fruits of my labour speak for themselves.

But from a practical perspective, the ideal you're promoting is impossible to implement in this society. Most of us are operating in a far more rudimentary manner, hence the carrot and stick approach to guide behaviour. We knew smoking was bad for decades, but what's really decreased consumption is taxing the arse off it.

Money is the easiest way to do that, because it's the most universally accepted format - it could be ice cream, flowers or a new pair of shoes but it'd be impossible to have a centralized way of catering to each individual golden goodie.

Free will is not a fantasy

The notion of a separate self is in itself a questionable premise. Essentially what we consider the individual exercising free will is really just neurons flying about in a small corner of the universe. Anyway, might be of interest:

I agree we are on the same page in some ways. Where we differ is believing that conventional science, thinking and means of doing will solve the issues or create a better environment that encourages positive change, both individually and collectively. Rome wasn't built in a day so the question becomes do we encourage a transition or do we allow the institutionalised ways to keep holding power. Signs suggest slow progress is happening but the old ways are also fighting to retain power. There are some suggestions that we are going through a natural cycle, one that is far outside our human ego awareness.

Price may influence some to quit smoking but it doesn't necessarily solve the underlying cause. The addiction will most likely be replaced by another more acceptable one. Note the rise in vaping that is hooking many youth who would never have smoked tobacco.

Conventional brain science may hold some truth re wiring, but doesn't seem to want to acknowledge the intricacies of environment and life experiences, and wants to adopt a one size fits all approach. It's the nature vs nurture theory. There are many influential medical practitioners who have worked in the field of addiction, mental health etc highlighting that much is caused by ones childhood environment and by the societal and economic environment. Many addictions, maladaptive behaviours/traits have been stigmatised but more have been normalised, become socially acceptable. It's suggested that most people are simply trying to full an internal void through external means, and our current ways enable this. It would appear that our economic environment encourages an imbalance in unhealthy traits. Much that we are taught to emulate, to revere and epitomise about the "successful wealthy elite" are actually people with a greater void, a greater imbalance of unhealthy shadow traits.

The concept of self has layers. The ego self programmed by many factors, the true authentic higher self and ultimately there is no separate self but a unified oneness. It was taught by many through the ages. Much has been distorted by those in power over the ages too. Ruling powers don't want everyone to be operating from an inner place of sovereignty and self governance, otherwise the established narratives and institutions of power and control have no place.

There are many going through this transition and many that might need assistance with their wiring to be the examples of change. Unfortunately for many current practices and institutions would rather mold them to fit in rather than be agents of change.

I commend you for being strong in yourself with regards to not playing the appearance and appeasement game. Unfortunately for every one of you there are probably a dozen or more that weren't allowed or guided appropriately to find that power in themselves.

Is an increase in the dollar value of a block of land income? While people can leverage, trade leverage, trade and on and on, profit from this activity is obviously income, but there comes a point in the short span of a human life where the gain in value is actually a depreciation in the value of currency, not income. Land is the one investment that has most intrinsic value though time that currency can be measured against. Not gold, not bitcoin, not equities. 10 years ownership is a good line in the sand for property transactions resulting in a gain, to be considered non income.

Of course there's many other factors in play especially around our measurement system and the factors causing that increase in "value". It's also dependent on the perspective of intrinsic value and can't always be looked at in "economic" value. Some would also suggest that much of the gains come from external societal factors and therefore some of that should be given back to society.

I was simply highlighting the inconsistencies within the tax law itself. It's something very historical, is constantly tweaked and yet it's intent and purpose is not something that has been looked into as to whether it still aligns.

Thanks for the financial advice, not.

Has anyone had experience with Cove Insurance?

Thanks

Looked into them at one point. they are underwritten by Aioi Nissay Dowa, who you can directly insure with.

End of the day using trademe insurance as the broker was about 20% cheaper with State than Cove.

Yes and had a recent claim which is dragging on for over a month - (other party admitted full liability). Saved $100 over AMI but probably cost me more in time.

The U.S. top banking regulator FDIC has an out-of-control party culture rife with misconduct going back decades. “If you haven’t puked off the roof, were you ever really a FIS?”

These are the people protecting the free world in the next banking crisis.

A male Federal Deposit Insurance Corp. supervisor in San Francisco invited employees to a strip club. A supervisor in Denver had sex with his employee, told other employees about it and pressed her to drink whiskey during work. Senior bank examiners texted female employees photos of their penises.

All of the men remained employed at the agency.

A toxic work environment at the FDIC, one of the nation’s top banking regulators, has for years caused employees to flee from an agency they say enabled and failed to punish bad behavior, according to a Wall Street Journal investigation based on interviews with FDIC employees as well as legal filings, union grievances, Equal Employment Opportunity complaints, emails, text messages and other internal documents.

https://www.wsj.com/us-news/fdic-toxic-atmosphere-strip-clubs-lewd-phot…

I guess you send a banker to catch a banker......

Following on from the 80,000 net people who arrived in NZ in October, are the 30,000 net people that have arrived in the first 12 days of November. What's the Rent contribution to CPI again?

Gee KW, 80'000 net arrivals in October alone! That's close to a million per annum ! Are you sure you understand the meaning of the word "net" and that you're not including temporary travellers, like tourist ? LOL.

Yes I asked this question of K.W. on another article

It does seem a bit extreme, adding basically a Palmerston North each month

Rounded figures, 551k PAX arrived and 341k depared in Oct.

Is on StatsNZ website.

Running net 31k up to 13th Nov.

You'd almost think more people visited NZ in the warmer months, and less Kiwis want to leave.

All says it in the latest Stats data

A record NZ citizens leaving and significant amount of non-nz citizens arriving.

https://www.stats.govt.nz/news/record-net-migration-loss-of-new-zealand…

Both cars both premiums went from circa $650 to circa $975. And cars had decreased slightly in market price over the year of course.

Shopped about New price circa $625. Same cover details.

In September 2021, owner occupiers borrowing for their own house with a DTI ratio of between 4 and 5 had a gross household income of $144,000 on average. In 2022 it was up +21% to $175,000. And now in September 2023 it is up +13% to $198,000

If we use our head (and a bit of basic maths) if the "I"ncome goes up significantly but the DTI stays the same, it must mean that the "D"ebt has increased at a similar rate to the "I"ncome. Since house prices have not gone up since September 2021, this makes one wonder why the increase in borrowing?

The Economist suggests Aussie has the most entrenched inflation among developed nations, followed by the other Angloid nations. Bailing everyone out is identified as a problem.

In Australia, our worst performer, the labour market is on fire. Over the past year labour costs, measured by how much employers pay workers to produce a unit of output, have risen by a chunky 7.1%—faster than in any other country sampled. Nor does anywhere else have more “inflation dispersion”, which we define as the share of consumer prices across the economy that are rising by more than 2% year on year.

This stickiness of inflation may reflect the fact that fiscal stimulus across Anglophone countries in 2020-21 was about 40% more generous than in other rich places. It was also more focused on handouts to households, such as stimulus cheques, than on measures to keep businesses alive, which may have further stoked demand. Indeed, a new paper by Robert Barro of Harvard University and Francesco Bianchi of Johns Hopkins University finds evidence for a link between fiscal expansion during the covid-19 pandemic and subsequent inflation.

https://www.economist.com/finance-and-economics/2023/11/12/what-can-inf…

ANZ CEO Shayne Elliot suggesting there is a problem (without really accepting any responsibility).

“If you want a loan you have to be better off, and essentially rich,”

“There’s big social consequences and political consequences.

“Is that a society we want where people can’t get a home loan or get a loan to start a business?”

Mr Elliott said strict lending regulations — including assessing loan applicants based on a 3 per cent increase to interest rates — risked containing lending to wealthy borrowers.

“No one is suggesting we want to be irresponsible,”

https://www.news.com.au/finance/economy/interest-rates/home-loans-only-…

Shayne - thats what happens in a recession.... and banks have credit losses.

Lol. Is there a way we could do it without getting loans from private banks? Is there a way people could have homes without the need for prices to rise the way they have, without price gains being the influencing factor?

And from today's Interest article:

Meanwhile ANZ NZ has $12 billion in its settlement account with the Reserve Bank, which is paid interest at the 5.50% Official Cash Rate, the equivalent of about $1.8 million a day.

"in a way we'd much prefer to be lending that money than leaving it in the Reserve Bank, and we'd be getting a more positive return on it if we were lending it," said Watson.

"Even though we've reported an increased profit, our profitability is down because of that capital impost,"

Yep. The banking top brass speak as if their privilege and fail-safe status is a given and that the public understands that. It's quite bizarre. And weird. No other business can really operate like this.

A colleague who works for ANZ in Asia sat in on the earnings presentation. Future layoffs were smoke signaled and the question coming from staff was 'if we're making so much profit, why are there plans to lay off staff?'

Underway in Aussie already.

ANZ will make up to 60 roles redundant, which includes 30 positions sent to India, as part of a restructure that will affect more than 200 employees.

Cheers for the tip. NAB has opened a tech innovation center in Vietnam. Similar action it appears. Cut and past from your link:

The announcement comes after the big four banks have already made more than 2000 workers redundant this year in response to growing cost pressures.

FSU analysis conducted in October revealed that Westpac led the pack with more than 1080 jobs cut, while Commonwealth Bank had cut more than 600 roles and National Australia Bank had shed about 340 staff since January.

If David Cameron was the answer, the Tories again asked the wrong question.

For once we agree. https://www.gq.com/story/why-is-everyone-saying-the-uk-prime-minister-h…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.