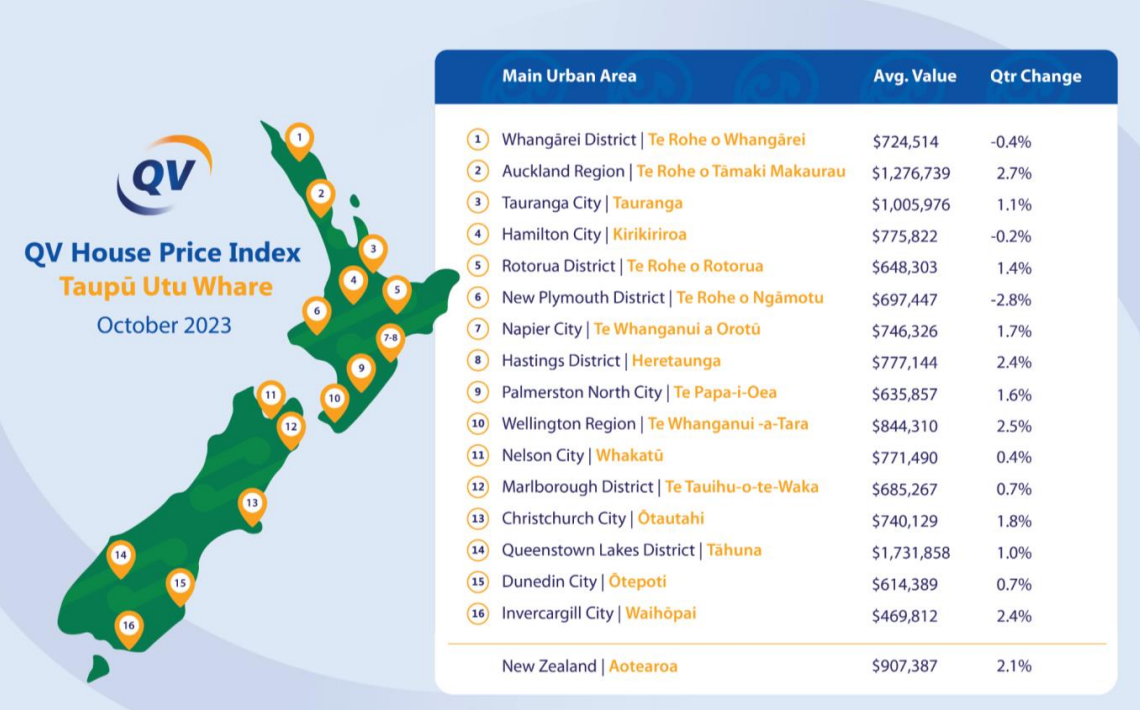

The average value of New Zealand homes increased by more than $18,000 over the three months to the end of October.

According to the QV House Price Index, the average value of New Zealand homes was $907,387 measured over the three months to the end of October, up by $18,388 (+2.1%) from the three months to the end of July.

Average values increased in most regions, with the biggest gains occurring in Auckland 2.7%, and Wellington Region 2.5%, followed by Hastings and Invercargill which both had quarterly gains of 2.4%.

Only three regions recorded declines in average dwelling values: New Plymouth -2.8%, Whangarei -0.4% and Hamilton -0.2%.

The chart below shows the average values in all major urban districts along with their quarterly changes.

QV Operations Manager James Wilson said the housing market was increasingly showing signs of recovery, but against a background of low sales activity and challenging economic conditions.

He expected it to stay "flat to gently rising" for the foreseeable future.

"Interest rates and credit constraints continue to act as a handbrake for the most part, but we are seeing increasing signs of life across much of the country," he said.

"I still don't expect to see a big rebound in house prices given the strength of the economic headwinds we are facing," Wilson added.

"But considering what we've been through since Covid first made its way to these shores, flat is probably the best thing given the current conditions."

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

176 Comments

So much press pumping housing. Fundamentals dont point to a doubling anytime soon unless debt hnsupported by invome is the new black. Debt higher, inflation not tamed, and the financial mess of the last govt not fully uncovered yet because Nact and Winnie can't agree.

Perhaps the industry is just desperate for a paycheck.

How significant is the increased immigration in this? How do you see the fundamentals playing out over time?

More demand = higher rent, higher rent = more attractive to investors. Sadly the nature of capitalism would suggest that those with many mortgage free houses (those that already have) will benefit most as they ave access to more equity to stump up for even more rentals.

The research also found that during the study period, rents increased broadly in line with wages, but faster than inflation.

Yay, substantiation and evidence 🤩

It would be interesting to see how much of that rent is taxpayer funded. A conversation I had yesterday with a solo mum, on sickness benefit, winz footing 600 a week in rent in Ak. Im sure shes not alone. Our tax dollars hard at work socialising the debacle.

She should sleep in her car?

Maybe my comment came across the wrong way. No she shouldnt sleep in her car. But she rents from a private landlord. Rentals need to be socialised en masse.

She also buys bread from a private supermarket.

Not $600 worth a week. And all of us accept the major problems we face as a nation with our supermarket duopoly rort so its odd that you use that as an example.

They already are on a wide scale. But the government can't afford to own them all, and when they do, they're less efficient at it than the private sector.

Unless maybe if it's tenement housing.

The government predictably do a terrible job at it. Until fairly recently the state houses in Auckland were undeveloped (tiny houses on quarter acre) and in bad condition, much worse than the private sector. Had the government sold all those state houses and stopped interfering with unnecessary planning rules, I can almost guarantee we would be in a better place right now.

re ... "... and when they do, they're less efficient at it than the private sector."

Prove it. I can wait.

I believe the net loss on each state house is $35k a year.

And Im commercially involved with construction, and see the government build or renovate properties, and compare that to the private sector.

"I believe the net loss on each state house is $35k a year."

Social housing is not a profit center, it is a cost center for the benefit of society as a whole (e.g fewer homeless sleeping on streets, sleeping in cars, sleeping in tents in inner city areas, sleeping in ghettos areas, etc, resulting in increased crime, etc).

There will always be a need for social housing and that demand for social housing changes as market conditions change - more social housing is required in recessions and when rents in the private market are unaffordable for households.

There is such a shortage of affordable housing now that there are long waiting lists at Kainga Ora and there are large subsidies being paid by government in the form of accommodation supplements (which are ultimately paid to suppliers of long term rental accommodation in the private rental market i.e landlords)

Profit oriented businesses are not financially motivated to provide such social services which operate at a loss, so government steps in and fills that need.

The solutions to more affordable housing are complex and political and need the political will of policy makers who are focused on winning their popularity contest every election cycle who also need to meet the vested interests of their supporters.

Edit: resulting in decreased crime above

That's an operating loss though - i.e. the tenant is already receiving the $600 a week or so for the actual rental component, and the government is making that loss over and above that.

It'd be like if the government provided loaves of bread, but they spent 10 bucks to procure it, when you can go down the supermarket and get one at the market price of 3.

"That's an operating loss though"

Kainga Ora had 64,870 residential dwellings in public housing as at July 2022. - page 138 of https://kaingaora.govt.nz/assets/Publications/Annual-report/Annual-Repo…

A loss of $35,000 per residential dwelling would mean a total of $2,270 mn in operating losses (i.e expenses after revenues)

Yet based on the numbers on page 173, I calculate a total EBIT loss of $128mn (or approximately $1,973 per residential dwelling, rather than the $35,000 above).

Are you just looking at the expenses without the offsetting revenues?

Total operating expenses (i.e excluding interest) before any revenues is $2,200 mn (as per page 173) - in line with your number calculated above.

Thanks CN.

re ... EBIT Loss of "$1,973 per residential dwelling"

Which would probably be an amount less than the unpaid / un-expensed work that landlords put into their properties each year.

Thanks CN. I appreciate how you offer the forum figures rather than just rhetoric. It's refreshing.

However, I am not sure EBIT/operating loss that excludes interest expenses is an appropriate measure. As interest is the major expenses in the property market. I did the calcs myself, albeit a year ago, and including interest as an expense, Kainga Ora made a 21k total loss per household. When a private landlord excludes interest as an expense, which he has to for tax purposes, his books look considerably more rosy. EBIT is a useful tool for valuing a business.

You could also look at it another way in terms of opportunity Cost. How much is the taxpayer losing by having 60000 state houses leased at below market rates?

"I am not sure EBIT/operating loss that excludes interest expenses is an appropriate measure. As interest is the major expenses in the property market"

The rationale for focusing on EBIT is that this isolates the operating performance of the business before financing costs.

A profitable EBIT can become negative due to a separate decision on how to finance the business operation.

Take two extremes in financing - a residential property purchase can be:

1) 100% equity financed or

2) 120% debt financed (as was the case in Ireland during their property bubble)

Each person can choose to finance their property purchase anywhere on that spectrum and have entirely different after interest expense and after tax cashflows.

But if the tenants of those 60000 state houses can’t afford market rates what do you suggest?

"But if the tenants of those 60000 state houses can’t afford market rates"

Assuming that Kainga Ora is charging market rates on their properties, the tenants already are unable to afford market rates.

Look at page 173. In 2023,

1) Tenant related rent received was $469 mn

2) Crown income-related rent subsidy was $1,151 mn

That is before any income related rent subsidy paid to the private landlord market.

Looking only at Kainga Ora, if you remove the Crown income-related rent subsidy of $1,151mn (from WINZ), then the EBIT loss would be $1,279mn (or $19,716 per residential dwelling)

So if housing was more affordable overall in the country, then the EBIT loss would be reduced from total government spending (i.e Kainga Ora and WINZ combined) and the income related rent subsidy paid to the private landlord would be reduced and this money could then be used elsewhere in government spending.

Private landlords typically view the world from their perspective and financial interests. They may be unaware of the total impact on the country and government finances (and many may choose to prioritise their own financial interests over the overall benefits to the country as a whole).

Put another way, when there is increasing unaffordability of housing to a larger number of households in the country, the government is going to have to spend MORE money on income related rent subsidies - either to Kainga Ora or to the private landlord market.

For me I am all for a big pool of state houses to home such people. The start of the discussion though was about making all rentals in the country state owned. I think that is an extreme that will have major fiscal consequences. Private landlords and kainga Ora. We need both.

Question would be why does she have to live in Auckland? If she is a solo mum then why not move out to the regions, better standard of living and cheaper rent. Not entirely sure how all this works but it seems extreme that someone on a benefit gets to choose where they live when the rest of the tax payers have to compromise based on need for work and affordability.

Sluggy ...been saying this for ages ! Scrap the accommodation supplement and let the so called "free market" set the rents . If you as a slumlord, have to get the taxpayer to pay the rent for your Clendon shitbox, rather than the tenant, the freaking govt is setting the price of rents ...not the marketplace !

As a taxpayer (yes one of the stupid 20% that pay 80% of the tax) its just ridiculous ....if a population can't afford to pay a certain rent - so be it !

New Zealand has and still is living "beyond it means" .....always make me laugh just how much lower financially NZ's standard of living is, compared to the US, Canada, Australia. The media would have you believe we are up there with those countries - I can tell you, we are not.

For AKL - go HIGHER and NOT outwards !! ....who gives a frig about that shadow that diminishes your sunlight from 3pm to sunset, in the backyard of your leafy Ponsonby villa.

They do it in Sydney ......where they learnt this years ago ! but not NZ , the people here are one the most miserly, penny pinching people I have met in the world, and follow others ie the uncle or whatever the financial MSM feeds them like sheep, while I have never seen so many "shortcuts" taken in the residential building industry.

And get your thieving hands out of the taxpayers pocket, to financially support a tiny group of the population, being multiple owning property investors....and before you "astute" property investors say "but we are providing a home for those who can't afford it" , think about the cost of your rents to the average income, bleeding the rental population and taxpayer dry ! While, if you have to be "in business" be enterprising and resilient and stand on your own 2 feet without govt support. You would be the one that yell at the guy at the traffic lights asking for loose change "get a job", while the same govt that pays the dole, tops up your rents ! ..... absolutely hypocritical.

Agree with you in principle. But I now fear that letting the free market dictate would lead to hundreds of people homeless within a few months. The government must share the same fear and hence the accomodation supplement/landlord subsidy.

The effects of 120k immigrants on NZ's existing population of some 5.5 million is vastly overstated. It's fodder for spruikers and the property class only. The actual effects are pretty trivial over most of NZ and tiny in Auckland where most immigrants start off.

Further, because so many kiwis are as dumb as dirt, they're sucking up this overstated impact as truth, and accepting dwelling and rental price rises because of it.

Wrong. 70% (84,000) of new immigrants go to Auckland (pop 1.5m). That may be, say, 20,000 families. Definitely impacts housing demand, owning and renting.

While the borders were closed over Covid and Auckland's population stable to dropping, so to were rents.

As soon as they open up, rents skyrocket.

The interest rates also went up.....

Housing Technical Working Group report said that interest rates have affected land prices, and not rents, which are more related to willingness to pay (wage inflation)

Rents in some places skyrocketed, around universities especially so. (Great yields to be had now - if you were wise back then.)

And as pa1nter explains, interest rates and tax changes account for much more of the rise than immigrants do.

Might I suggest you look at these recent immigrants more closely and where they live on their arrival, then where they live after a year, and then where they live in 5 or 10 years after that? Your numbers do not reflect the reality of who they are, nor what accommodation they require/accept.

Interestingly, the last time I heard the same equation you use was last time I was listening to a group of real estate "gurus" selling "property investment" to novice "investors". (I was in the room in an academic capacity only.)

In 2018, Auckland Council suggested there were some 550,000 dwellings in Auckland. Obviously that number is much higher now after the frantic building over the last five years. Note that Council's number does not indicate whether a dwelling is in fact "full to capacity" (most aren't btw).

Were your number of 20,000 correct (it's not, it's way too high) that's an increase of about 1.04%. So what is being built per year? ... https://www.interest.co.nz/property/125203/record-1927-new-homes-were-c…

So much press pumping housing

Uhhh, it's also the subject of about 90% of the discussion on here.

Yes, sadly…

@Averageman, give it a rest, you been predicting doom and gloom for over a year now.

Increased house prices IS doom and gloom.

@redcows, would you like your house price to go down? Or just other peoples?

Recycled talking points over again.

I own a house mortgage free, more than happy for it to go down in price. I am not brainwashed with greed.

I am happy to go to work to contribute to society, and in return expect society to provide for everyone fairly.

People like myself are the majority. Greedy speculators and ticket clippers are the minority.

@the Joneses, Your argument is interesting, Tell you what if I win lottery I will give you half? That way we are both not greedy or speculators and we roughly contributing the same to society, which is 0, just kind words.

Strange flex. Winning the lottery arguable does more for society than bidding up the price of housing. The Lotteries Commission distributes all profits to community grants.

A lotto windfall is the incentive for people to buy the tickets.

I wouldn't call it the minority. Almost every kiwi is hoping and sees their home as their vehicle to wealth and retirement, even though its delusional, that's how they view property.

Why else would you be taking out a 20x leverage buy to get on the ladder

Which highlights the propaganda narrative that has set in over the last 40 years, enabled by greed/fear of never having enough. It can be seen in the use of words and the meanings given to them. And in most cases those words and meanings have been distorted over time. It's a literal programming that most aren't aware of.

Prior to that there was no ladder. People bought homes to raise their family and the general concept was to pay off the mortgage thereby freeing up income to save/invest for retirement. That in itself was a relatively new concept as well. And now nobody "wants" to work, instead the aim is to retire as early as possible. It used to be work to live and now it would appear for many it's live to work. (There's some deeper paradoxes and paradigms to this as well but difficult to put into language here).

This is where economists, economics and capitalism fails. It fails to acknowledge that economic environmental conditions influence human behaviour, instead assuming that the behaviour comes first. Economics/capitalism in it's quest to monetise everything have actually deprived/repressed the human, the inherent "goodness" to be generous, kind, compassionate, giving and sharing. It reduces all life, human and planet into commodities. It can be seen in the values/labels assigned to people - consumer, worker, taxpayer, investor, wealthy, poor, elite, winner, loser, etc. It purposely creates and values scarcity thereby limiting the natural abundance that exists for everybody. It's ultimately a zero sum game for humanity.

"Real pain" is just around the corner!

Yawn. People should consider the pros and cons of a sustaining yield return, vs a speculative capital gain spiced with tax avoiding holding period.

Yawn

I'll say. You've been making essentially the same comment for going on 2 years.

Agreed. As have your and the crew of debt gathering middlemen.

Based on your endless "prices to the moon" mantra and how much you back yourselves on here with 100 posts plus a day, perhaps you could detail how many extra houses have your purchased since the election...?

Don't listen so good do ya.

I'm an observer of things, I'm not a property investor.

Unless the economy terminally shits itself, or some other world changing externality, I can't see most components of generating a new house declining. Whether that's compliance, production, or local fees. That's not a call of "too the moon", just a sad observation of what's going on.

It's obviously easier for you to paint me as something than have a big boy pants discussion.

Wait to the Ponzi really gets going.

Or maybe not in rides WP.

ABSURD.

we already have massive homelessness and some of the highest real house prices relative to income in the world.

Here we are bidding up land prices yet again. Totally unproductive use of capital.

Totally unproductive use of capital.

what is the productive use of capital?

Manufacturing.

Capital is productive when it creates something new. So using capital to build a new dwelling is productive whereas buying an existing dwelling is not.

Capital is productive when it is used to reduce input costs that result in higher production, lower prices, or better quality, or any combination of those.

(NZ Inc is crap at using capital in a productive way. Our tax system ensures we're crap at this. Have I mention this before?)

so anyone who bought a existing house is just doing meaningless nonsense activity which is not part of an economy?

if that's the case, a shop buying selling cloths, or food, or fruit are meaningless because they didn't grow them or make them, are they not adding productivity to the economy?

No. The point is all that is changing is the land price. It doesn’t add to our economy and will eventually fall back to realistic values, even if that is a long way in the future.

The capital used buying the elevated land price will be destroyed with little net gain to the economy, if any.

The counter factual is constant land prices and the capital going into businesses, shares or any other productive enterprise.

Successive governments Javed caused the problem by running excessive immigration rates and tight land use controls.

NZ population is growing, like it or not, and need roof over their heads. in short, housing market needs more capital to it.

You cannot call unproductive when it provides roof over their heads.

It has nothing to do land or values or prices.

It has everything to do with land prices.

The counter factual is enough land and housing supply. (And a tax system that doesn’t offer lazy tax free capital gains)

100% correct.

But I'd qualify to say land prices are established based on a huge number of factors, typically around current and future "returns on capital" which obviously differs depending upon what the land can be used for ... (And thanks to our hopeless NIMBY dominated Council's - what it is allowed to be used for). The rule of location, location, location isn't just a throw away term - it's very real over the longer term.

Because the land value is subject to numerous interpretations of "value" the relationship is seldom clear, except over the longer term. Land bwankers know this. And they know the tax system well enough to know what a tax free gain is. Thus billions of dollars in "capital" sit around idle waiting until land bwankers cash in their tax free capital gains.

You're right that our housing market needs more capital to build more dwellings.

But 100% wrong that "investors" need more capital to buy existing land and dwellings.

Stats are showing more FHB getting a larger share of the transactions. Looks like Tony's spruiking has put the FOMO back. Would an immigrant be classed as a FHB? If so.... the stats may not be so good for actual FHB's.

A much larger share and much less bang for their buck.

When we bought a new build townhouse only 4 years ago, it was a 3 beddie, 2 baths, 104 sq m, heaps of storage, a 25 sq m courtyard, two car parking spaces in an ok location - for 750k.

At the moment, even with price falls in the last one year, a FHB is lucky to get a 2 beddie, one bath, 75 sq m, little storage, a 12-15 sq m courtyard, and one carpark in the same location for 750k. And higher cost of finance.

Everything is maxed out. It’s vulnerable out there.

Auckland really is terrible in what you get for the money, you get twice that for the same money in the regions, its not even comparable. Pretty much the reason I left Auckland all you can get is massively overpriced property so you can sit in a traffic jam all day.

Are you going to mention Palmerston North?

No I'm in the place where all the cashed up Aucklanders go after their prison sentence is up.

Your point is meaningless. Try New York and the costs in your example multiply by 10 and the house U get probably shrinks by 10x too. And NY has lots of taxes and CGTs too. That's the reality of life. The people with good education, good incomes, hard working, get ahead types, prosper. The whiners who leave school early, don't study, get low paying jobs end up struggling. NZ is not immune in its own wee way. It's much easier to not live in Auckland.

You can't compare NYC vs Auckland City, Auckland City is just a hick town compare to NYC.

Auckland should be compared something like Phoenix or Austin, one can buy a nice 4br in those two cities in the region of 400-500K.

https://www.bizjournals.com/austin/news/2022/05/11/austin-housing-affor…

You can, because both of them are constrained areas where a large portion of the nearby population are proliferating.

Texas is a large open plain.

I had a stint at Auckland Council, that land constraint is a myth - They have a shxt load of designated land for residential developments, some inherited from the old Waitakere and Manukau councils. Just that they can't get their A into G to set up infrastructures.

Yet, on a world scale Auckland is consistently considered a highly desirable place to live, it always ranks way up in the nose-bleeds of these most liveable cities type studies.

"We don't know how lucky we are." - F. Dagg

https://www.bbc.com/travel/article/20230725-the-worlds-most-liveable-ci…

BBC doesn't know the hidden image of Auckland as "Ram Raid City"..

Last chance for many to exit housing market before rates and inflation cause next tumble in house prices. If average house cost is over 900k and average wages is 70k thats around 13 x income, with these huge imbalances just a matter of time before the implosion which will make the last 15-20% crash seem small.

Except we work on household wages these days. So 6.5x household income.

I don't agree with the measurement but it's reality.

Over coming months more and more will be refinancing from low 3% or 4% to over 8% in many cases. I believe many just making payments before refinancing will have to exit market before monthly payments get out hand. Even at 6.5 x household income the crash is unavoidable, anyone over leveraged will be hit hard as debt levels goes past ability pay.

Most of thats already happened though, and mortgage arrears are trending down.

Where can I find and monitor this info?

At a glance, repayment deficiencies appear to be up: https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/residen…

It was on this site, last week.

It's not just those refinancing from low 3% or 4% to over 8% ...

It's also those that have already re-financed and their covid-buffers are exhausted or near exhausted. Read the bank's annual reports carefully and you'll see references - albeit couched positively - to these buffers. Alas, they'll not last forever.

At present, banks are either ignoring this risk, or sucking them up, but it can't go on for ever. If HFL becomes real (it won't) banks will have to fess up.

Replace your word "many" with "a few".

….and 6.5x is still a crazy high number in any international comparison. Shows how completely detached from normal things have become

Is a price vrs income ratio done on a household’s income or an individuals. I’m not sure?

edit

Just read an above post: it’s household income

You should try the "random" option on your playlist rather than repeat.

I am adding recession on to playlist as most of the western world is heading that way, Higher for longer is staying in top ten with NZD tanking,and you can’t pay mortgage with FOMO.

You realize "average" people will be hurt way more in such a scenario, right?

Almost impossible to have a surgical strike that'd crush asset holders that wouldn't have a commensurate effect on the worse off.

If your house price crash by 50% how would that make life worse it’s just a number until you sell. The people who are worse off as you put it could see a future with the possibility of getting own house. The people who have money to invest should buy businesses that produce goods not just pushing up house price’s and rents. The point is debt is now costing more to fund and something has to give and in New Zealand it will be property market as it is so overvalued compared to income.

Houses are generally of more importance to people than most other things they spend money on. So we are already seeing reduced spending in other areas of the economy in light of higher mortgage servicing costs, which will have a commensurate impact on the people engaged in those other activities.

So it'll actually be jobs and incomes first, and then property. The inverse of what you're hoping for is much more likely, the average person will be in a worser position to afford a house.

You can’t get money off people with nothing but the average punter who purchased a investment property with borrowed money will be the ones who get clobbered,the banks are sitting pretty with not much skin in the game if property speculators go belly up they just sell house cheap and pocket proceeds. Billions are invested in property and each million costs 70 to 80k per annum to service now rather than 30 - 40k a couple of years ago with average wages being only 70k the crash will be huge and hopefully prompt the government to put policies in place so housing cannot be used as a tool for speculators to abuse

Remember though, even though the median house price is nearly $800,000, the median "new loan" mortgage is just $360,000, so most will be fine with servicing their mortgage.

Which highlights the consequences the property ponzi has on the wider economy. More and more into the mortgage reduces the needed flow of money into goods and services. The result being those relying on selling said goods and services cannot service their mortgage or their landlords commercial rent, or . Either the RBNZ steps in with more failed monetary policy to pump it up or we accept that property prices and the banks have to have a massive reduction in $$ values. The problem there is with the psychological loss and the inability to see that it could be a massive societal gain, a reset to real values. It would appear that it's a lesson we're unwilling to learn. We really have created an extreme situation in NZ.

Here's an interesting observation. It would appear over the last 2 decades it hasn't been the importance of having a house. For many owner occupiers it's been the importance of capital gains and resale value rather than having a home. For those FHB's buying in FOMO they've had to potentially give up important experiences conducive to their wellbeing and personal growth.

I don’t know, NZ obsession with property and forever rising prices is insaitable and ripe for manipulation and FOMO. Anything is possible.

Had a chuckle to myself last night - house in Wellington - sold in mid 21 at the peak for $1.87M- listed a few weeks ago for $1.8M, then last week price reduced to $1.7M now yesterday listed at $1.6M

If thats not a warning to buyers to be careful - then nothing will be.

Meanwhile a house valued at $1.6M in another nearby suburb was listed at $2.2M - I'm assuming to take advantage of a proposed foreign buyer policy - that is not actually law yet and is looking unlikely to be law.

Well *if they get $1.6 mill then that’s only 12-13% down on what they bought it for. Given prices tanked more than 20% in Wellington, not too bad?

No way the foreign buyer policy survives the NZF negotiations.

In fact it was so badly thought out and the math behind it so sketchy, that part of me wonders if that was the intent all along. I.e. the Nats cooked it up so they'd have something to distract Winston and an easy bone to throw him in negotiations. That's probably giving them too much credit though.

Auckland leading the way.

Current annualised increases @10%+

When rates trend down from 2024 expect 15% yearly increases in the main centres.

Translation - "I won't accept anything less"

'When rates trend down '.. you'll be an old person by then..

So prices go exponential? It's impossible to sustain.

But it's property, so it can! Anything is sustainable when you hold a roof over desperate people.

This country is shameful

Is rising house prices the very best we can do to ‘generate wealth’ in this country? Especially in the face of rising unemployment and interest rates?

No wonder so many are opting out of reproduction when basic human needs have been turned into a vulgar form of speculation.

Can anyone inform me how this could possibly end well? Because the only explanation I see for this is that we are living through a bull trap.

Love your comment especially

No wonder so many are opting out of reproduction when basic human needs have been turned into a vulgar form of speculation.

There really seems to be no end in sight to the greed which drives FOMO which drives greed…

The end result may be young "entitled" people continue to leave the country for better pay and living conditions in Australia. We plug the gap with hard working but unempathetic migrant workers to care for retirees too old and frail to live in their old 4 bedroom homes on 1/4 acre. More stories come out of elder abuse but mainly from the victims capable of stringing a sentence together.

Well, we voted for it. So I conclude we love it.

We voted Labour and the Greens out. I don't think many are excited about what is coming in, but as long as Grant, Marama and their ilk no longer old any sway I am happy.

I’ll believe the housing market is going up once investors are back. The FHB demand is not going to be enough to kick off another boom. Will people start investing when they can get 6% in the bank - stranger things have happened. The tax incentives are on their way back, 4% yield with no tax is about equal to the bank, so if you believe in endless capital gains it might still be a good investment.

The investors will be back once the government is clarified. Until then rents will continue to shoot up. 51 rentals available in Rotorua, pop 75,000+

Well done Labour, you fixed this.

How does giving tax advantages to existing houses fix the problem? Why build a new rental when you can buy a 70 year old house and get the same tax perks?

Funnily enough, being a landlords not a 100% altruistic decision.

$33,600 increase in average Auckland house price in the last 3 months. That is more than I earned in my job.

And it’s tax free.

Oh dear....except one is banked, the other is not. This figure should be treated as no more than a statistic until the day you sell yours. Homes are for living in and not speculating and salivating over. There are other games in town for you - surely?

Can anyone say with full conviction that this minor bounce in prices is sustainable given the economic challenges ahead in 2024? The kind of conditions that warrant interest rate reductions are still ahead.

Agree with you on liquidity and risk. While i'm happy to see 20% of my mortgage inflated away in the quarter I understand the concept of realisation so I am certainly not salivating. I'm not sure i get your last sentence though. Are you saying that interest rate reductions, whenever they happen, will lower house prices? Or are you saying that a financial crisis is inevitable and will lead to both house prices and rates coming down?

"I'm not sure i get your last sentence though.

You could start by being an honest Baptist :)

Being honest. I don't understand your point. I wanted clarification. Nevermind.

Not aure why it wasn't clarified. Generally, houses going down further after intereat rates have been lowered is that something majorly bad has occurred in the economy to force the interest rates down. This bad 'thing' usually hits employmentband people's ability to service mortgages and buy houses.

Not aure why it wasn't clarified. Generally, houses going down further after intereat rates have been lowered is that something majorly bad has occurred in the economy to force the interest rates down. This bad 'thing' usually hits employmentband people's ability to service mortgages and buy houses.

Historically, housing price declines in economic downturns tend to accelerate after the rates have dropped…lots of lag.

The same goes for paper losses RP, which you've been so gleeful about... it don't really matter unless you sell. Are you going to admit that you've been wrong about the 'dead cat bounce' aswell?

I was expecting you to turn up :) Nifty1, like I've said here to ad nauseam, if by Autumn 2024 rises are still occurring - I will happily admit I was wrong and you can jump for joy.....

It all makes little difference to my finances. I'm more concerned about FHB's overpaying and paying 8% for the "privilege" of home ownership.

Lol how about push it out another year...just incase.

I'd say you're more concerned about your TD returns than FHBs.

It speaks volumes when you make stuff up. Best not take what I comment too personally.

If I was concerned for my TD's wouldn't I simply take out a 5 year one to protect the rate of return? What a silly thing to say....

Edit

In fairness, you had been pumping Poppy's January 2024 House Sale Bonanza.

Bungalows in Grey Lynn, 399!

Townhouse in Epsom, 449!

Buy one of our mansions in Paratai Drive for 500, we'll throw in a flat in Glendowie for free!

Come on down, there's a sausage sizzle and balloons for the kids.

Now - now Pa1nter settle down....

Actually, the more I think about it, it does sound like fun. There's nothing like a good ol' sausi :)

edit

Can anyone say with full conviction that this minor bounce in prices is sustainable given the economic challenges ahead in 2024? [Retired-Poppy - above]

Let's be perfectly straight and unprejudiced, Retired-Poppy, if the house price index had fallen by 2.1% you wouldn't have labeled it as "minor". 🤭

Suggest you have a careful think about your own convictions.

TTP

Ha-ha :) - the irony of you posting about "convictions".

Anyway, this must mean you're unable to answer if this bounce is sustainable either. BTW, house prices have already fallen more than 2.1%.

And that says it all. If that's what you earn in your job then you are not representative of a successful NZer and no wonder you complain about house costs. Should have stayed at school when U were young a got a better paying job. The winners in society can handle the relentless cost pressures put on property by inflation, Council costs, Govt costs, rising development costs, rising tradie costs, imported materials costs, always weak NZ dollar. Buy land/house coz it will never be cheaper...unless you want to live in a tent.

33k/3mo = 132k / yr

Someone has to be the lower 80th percentile. What are you saying exactly? They are unsuccessful and don't deserve homes? Not everyone can be at the top.

Literally blames anything but over valued ponzi property market.

By this comment, teachers, police officers, even pilots until their 30s, marketers, the list goes on, are all fools for not studying harder, and the reason they can't afford a home is because they're uneducated.

God get a grip.

House prices do a lovely dance with mortgage rates. When mortgages rates reduce year-on-year, house prices increase year-on-year (and vice versa). Generally speaking, over the last 20 years or so, when mortgage rates are flat year-on-year, house prices increase by a few per cent. Mortgage rates have jumped about a bit this year but on current data it looks like we will be back positive year-on-year around Christmas.

This is true when all other factors remain largely the same.

But what happens when supply increases? I've posted recent history (post 2016) to show prices flat-line. I could equally go back to the 70s flatline in Auckland which lasted for more than decade where huge tracks of land were opened up for the building of cheap 3-bed/1 bath houses. We can't do that again, even though many think we can (and should), because transport options are nothing like they were back in the 70s, i.e. our roads are full.

(But you knew this? LOL)

Be quick! (to not enslave yourself).

House prices driving inflation seems like an RBNZ headache.

Where I live ( a North Island regional capital) we don’t even have a dead cat bounce. The FHBers are buying the rough overpriced badly maintained rubbish. Once you get to seven figures it’s dead unless it’s a standout. Over $2m forget it. Retail is dead. Look at the terrible figures out from the Warehouse this morning. The local food bank is asking for help as it has limited food supplies. People are struggling to survive financially. And we have silly old Winston holding up the formation of a government when we need one in place. Many of those who voted for him might regret it.

i don't he is doing the job i voted him to do and stopping foreign buyers coming in for 2 ml , if they had made that level 5 Ml, he may not have got my vote.

like bernard hickey says NZ's economy has become a housing market with a few bits tacked on, its time we started to produce better things to sell offshore rather than just our houses that are also funded by offshore banks

Winston is only about Winston. He will say and do anything to get your vote. It says a lot about NZ when a little bully gets 6per cent of the vote.

I would say it says more about Luxon than NZ. Open goal, how the hell did he mess up so badly?

its time we started to produce better things to sell offshore

So what's stopping you?

So blame the messenger is your style, huh?

Forward: Hickey

Good luck with that. The boomers with multiple rentals will never support any moves or taxes that will affect their capital. New Zealanders love property as a wealth creator and that will never change.

Retail is really dead. If stats NZ report GDP growth in the next quarter I will start to question it.

So... still not down 50% ?

And a long way from 3x income

It continues to amaze me that so many, are so focused, solely on prices.

Price is what a seller and a buyer agree to at a point in time. Nothing more. Without looking a volumes and understanding the aggregate supply and demand factors they tell you nothing when taken in isolation.

And yet, we see screeds and screeds on columns filled with "analysis" based almost solely on short term price movements with only passing references to factors affecting aggregate supply and demand - with the most common one being interest rates. (Interest rates are largely a demand side factor but has some bearing on short-to-medium term supply (1-5 years)).

But what of supply? What is happening there?

Once again, dwelling supply gets a passing mention (occasionally) but never any in-depth analysis that would affect the market - especially to the buyer's mistaken belief that dwelling price rises of 7.2% per year are assured.

Once again, I'm going to remind people of Auckland's flatline in prices following Auckland Council's Unitary Plan of 2016. Further, I'm going to remind people of the NPS-UD, the MDRS, and the fact that most Councils have now followed Auckland. Together, these policy changes, that enable far, far higher densities, are going to continue to have a massive effect on the supply of dwellings. Basically, supply will be far, far less constrained than it was prior to 2016 (and somewhat earlier for ChCh thanks to the earthquake).

Focus on price all you like. But you're being sucked in by spruikers.

If you want to know who is selling stuff, if they don't mention the supply side effects of the 2016 UP, NPS-UD and MDRS then they're selling stuff, and the 'article' becomes nothing more than an infomercial. (interest.co.nz excluded obviously as they're a news aggregator providing a constant stream of what's pushing the market.)

As my son used to say when he was young, "So long, suckers". :-)

Unfortunately most of the supply improvements have been undone by immigration craziness, and with National and ACT elected that will continue (unless Winnie stops it which he didn't last time).

See my post above where I comment about the real effects of immigration. Summary: vastly overstated.

"It continues to amaze me that so many, are so focused, solely on prices."

Seen much analysis of historical house price changes and forecasts of future house price changes.

Need forecasts of upward house price increases to increase confidence of potential buyers to buy and borrow, thereby benefiting those with their financial self interests. Many of these financially self interested need to earn money to maintain their lifestyle.

"Forecasts may tell you a great deal about the forecaster; they tell you nothing about the future" - Warren Buffett

REINZ data out tomorrow!

Yvil, given your views on the economic challenges that lie ahead, come autumn 2024, do you think house prices will be still rising or resume falling?

Its just that you recently commented that despite the appearance of a "floor" you believed house prices had further to fall - or at least something along those lines....

Personally, I think this "bounce" will prove to be temporary.

House prices are going up from here, be it slowly. Too many things happening that only push prices higher, immigration still pumping, inflation still not under control and Wars all over the place. People say what about interest rates but the majority of people have already rolled over and the sky hasn't fallen. Don't forget the RBNZ is now in a position to CUT rates if it wants to, none of this going below zero bullshit the instant the market stalls.

"Don't forget the RBNZ is now in a position to CUT rates if it wants to"

Wrong. If the RBNZ were to cut rates now, what direction do you think our currency would head especially given Australia is still raising theirs Zwifter?

It amazing how some here find it so easy to trivialize the misfortune of others. It's premature to celebrate how people have adjusted to the doubling of their mortgage payments. What would happen if rents doubled in a year? Would people simply adjust to that too? There is considerable time lag before the stress presents itself in reported statistics. It's not going to be pretty.

Just watch them cut rates from mid 2024 if they need to.

But you just said they were NOW in a position to cut if they wanted to. Anyhow, if global circumstances/conditions permit it - then sure. The RBNZ will look at the bigger picture. If you cast your mind back to COVID era when global rates collapsed. If the RBNZ had stood pat and kept the OCR at say 3%, our currency would have soared to unsustainable levels. Put simply, the global tide of money can not only float boats, it can easily sink them too.

They are NOW in a position to cut rates tomorrow if they needed to because we are no longer sitting down at 2% mortgage rates with nowhere to go but up.

Rates can still easily go up from here too. Suggest looking at the global influences - the bigger picture. Were you around in the seventies/eighties Zwifter? There were times back then too when it looked like rates were headed down and went up instead!

Or they could plummet 275 bp as predicted by UBS yesterday

https://www.bloomberg.com/news/articles/2023-11-13/ubs-strategists-see-…

....yes they could. Considering that equities are currently pricing in a super soft landing, this prediction coming to fruition would mean a rude awakening is in store.

Pretty much on track for the 3 to 4% house price gains in 2024 then. The NATS need to get into action fairly quickly however to keep the ball rolling, this MMP thing could turn into a total cockup.

So a loss of -2% or -3% in real terms then? Seems about right.

My mortgage does not increase with inflation. Therefore, nominal growth is a more important measure for me than real growth.

If the real value of my house is decreasing, so is my mortgage.

"My mortgage does not increase with inflation"

What about the repayments?

In times of outright falls in house prices (like post Nov-21, the outstanding debt increases against the secured asset. That's how the bank would see it too.

repayments go up because of interest hikes. But then that is covered by tenant rents that are also inflated. My ability to service the repayment does not change.

The people who really suffer in inflationary environments are the poor souls who lock in term deposits at rates roughly 1-2% below inflation rate, only to then pay 20%+ tax for the privilege of watching their wealth diminish through the year.

Probably want to check the math, there is a reason everyone is running around these days screaming that housing is unaffordable, its because wages have never kept up. The situation is not going to change, in 10 years house prices will have doubled again.

Is there ever a limit to this doubling every 10 years phenomenon in your eyes..?

When I'm 60 is a south Auckland townhouse going to cost $14,000,000? Is it then going to increase in value by 1.4 mil every year for the proceeding 10 years in order to double yet again..?

re ... "The situation is not going to change ..."

Wanna bet? See my post about about the potential increase in supply above.

There was a very valid reason why Auckland house prices flatlined through much of the 70s. It came down to a massive increase in land supply thanks to Auckland Council re-zoning land. In 2016, they further changed the game to increase supply by changing the zone definitions to allow much greater densities.

You can ignore the economic fundamentals as much as you like by quoting dogma & pub economics and/or conventional wisdom. The economic fundamentals won't change, supply will increase, and I'll be proven right.

Upward phase likely to last in the order of 5 years

Sure, commencing somewhere around 2027.

The average value of New Zealand homes increased by more than $18,000 over the three months to the end of October.

Given that most people don't really understand how the Index is comprised and the margin of error between the Index and actual value, the claim that the avge value has increased has no real meaning outside the parameters of the Index's construct.

So have values really increased by $18K over the past 3 months? Or have sales prices increased of an unknown sample size that is weighted accordingly to get the $18K number?

Doesn't matter as long as the way they measure things have not changed, its all you have to go on. Lets just call it a ""Trend" for now, prices are increasing and not decreasing that's pretty much all you need to know.

"Lets just call it a ""Trend" for now, prices are increasing and not decreasing that's pretty much all you need to know."

That is how many form their expectations of future house prices in the short term - similar to technical analysis techniques of market prices used in financial markets.

As many say "The trend is your friend"

Here is the other part that no one mentions.

"The trend is your friend ... until it ends" - that is how highly leveraged buyers of residential dwellings got caught out at the peak.

Little point picking trends in data points that you can't understand what it is you're looking at. Data analysis 101. Limited methodologies are not worth much. Companies like Nielsen are finding that out at the moment.

I said months ago here it was great time to buy, and I purchased bare land on the outskirts of Auckland to back it up.

Quod Erat Demonstrandum.

But was it? (See my post about supply above.)

It may be dead money if buyers want to live closer to amenities and don't want the cost in $$$ and time of driving everywhere. Those down in Pokeno - being well and truly on the outskirts - aren't feeling quite so chipper now and their dwelling value reflect it. Still, wait 20-30 years and you'll be able to crow then I guess.

It certainly was ....local highway and intersections being upgraded, massive retirement village been approved, in between 2 major highways, road widening through local township on the drawing board, a Fletchers consortium wants to build 1,800 houses.

Who wants to live in a box in the city? I'm going to build on it shortly.

Not very good news to most here who were expecting a crash

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.