The Reserve Bank has left the key monetary policy settings unchanged and says the current visible price pressures in the economy will abate over the course of the year.

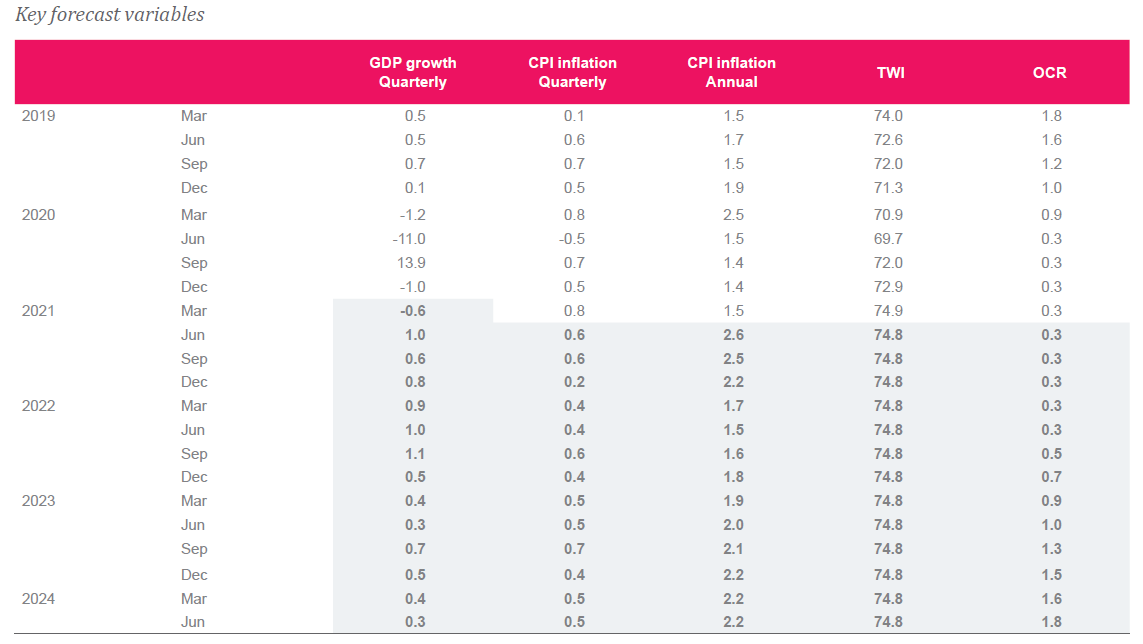

But it has reintroduced forward forecasts for the Official Cash Rate (OCR) in its latest Monetary Policy Statement. And these suggest the central bank expects to start raising the OCR in the second-half of 2022.

It sees the OCR hitting 1.5% by the end of 2023 and then 1.75% by the middle of 2024.

The New Zealand dollar immediately reacted by jumping over three-quarters of a cent against the American currency to go above US73c. Wholesale interest rates also took off. Westpac head of NZ strategy Imre Speizer said two-year swap rates rose from 0.52% to 0.59%, 10-year swap rates rose from 1.89% to 1.96%, and the 2031 NZ Government Bond yield rose from 1.76% to 1.86%.

For now though, the OCR stays at 0.25% (where it has been since March 2020) and the Large Scale Asset Purchases (quantitative easing) programme remains with a limit of $100 billion of bonds to be purchased by June next year.

Capital Economics, the first of the major economic forecasters to predict rate rises next year said, if anything, the RBNZ is "more hawkish than we are" as it believes rates may need to be lifted to around 1.5% by end-2023 instead of the 1.0% level they have currently pencilled in.

"With the RBNZ set to become one of the first central banks in advanced economies to hike rates, we think that the New Zealand dollar will continue to strengthen against the US dollar," Capital's senior Japan, Australia and New Zealand economist Marcel Thieliant said.

ASB economists say they were a little surprised to see the RBNZ "be so forthcoming", with the publishing of a OCR track signalling rate hikes, an acknowledgement that the OCR cannot remain at emergency levels forever.

"While we share the RBNZ’s view that the OCR will move up in 2022, their pace of hikes over the next few years is larger than what we envisage," ASB economist Nat Keall said.

Westpac acting chief economist Michael Gordon says the RBNZ "appears to have been moved not by stories of rising inflation, as the market might have expected, but by concerns that the labour market is much tighter than it previously thought".

"It is forecasting a sustained lift in wage pressures, and is less prepared to accept an overshoot on its employment mandate.

"We’re less sure about such a sustained lift in wage growth, though we acknowledge that it’s an unusual environment. The closure of the international borders in response to Covid-19 has closed off the flow of both skilled and unskilled migrant workers that employers would normally have expected. But it’s not clear that this will spur higher wage growth at a national level, and its persistence will depend on when and how migration flows resume."

These are the latest forecasts from the Monetary Policy Statement:

This is the latest statement from the the RBNZ:

The Monetary Policy Committee agreed to maintain the current stimulatory level of monetary settings in order to meet its consumer price inflation and employment objectives. The Committee will keep the Official Cash Rate (OCR) at 0.25 percent, and the Large Scale Asset Purchase and Funding for Lending programmes unchanged.

The global economic outlook has continued to improve, with ongoing fiscal and monetary stimulus underpinning the recovery. New Zealand’s commodity export prices have benefited from this rise in global demand. However, divergences in economic activity, both within and between countries, remain significant. The sustainability of the global economic recovery remains dependent on the containment of COVID-19.

The near-term economic data will continue to be highly variable. While economic growth in New Zealand slowed over the summer months following an earlier strong rebound, construction activity remains robust. The aggregate level of employment has also proved resilient, while fiscal spending continues to support domestic economic activity.

However, tourism-related business activity continues to be affected by the absence of international visitors, with the recent opening of Trans-Tasman travel expected to only partially offset revenue losses. The extent of the dampening effect of the Government’s new housing policies on house price growth and hence economic activity will also take time to be observed.

Overall, our medium-term outlook for growth remains similar to the scenario presented in the February Statement. Confidence in the outlook is rising as the more extreme negative health scenarios wane given the vaccination progress globally. We remain cautious however, given ongoing virus-related restrictions in activity, the sectoral unevenness of economic recovery, and the weak level of business investment.

A range of international and domestic factors are currently resulting in rising costs for businesses and consumers. These factors include disruptions to global raw material supplies, higher oil prices, and pressure on shipping arrangements. These price pressures are likely to be temporary and are expected to abate over the course of the year.

The Committee noted that medium-term inflation and employment would likely remain below its Remit targets in the absence of prolonged monetary stimulus. The Committee also noted that while the low interest rate environment has supported house prices, other factors such as recent tax changes, the growing supply of housing, and lending restrictions, are providing offsetting pressures.

The Committee agreed to maintain its current stimulatory monetary settings until it is confident that consumer price inflation will be sustained near the 2 percent per annum target midpoint, and that employment is at its maximum sustainable level. Meeting these requirements will necessitate considerable time and patience.

Summary Record of Meeting

The Monetary Policy Committee discussed economic developments since the February Statement, and their implications on the outlook for inflation and employment. The Committee noted the ongoing improvement in global economic activity and the associated rise in long-term wholesale interest rates. Fiscal and monetary stimulus are continuing to underpin the global recovery. However, the varied pace of national vaccination programmes, and the re-introduction of COVID-19 containment measures in some countries, means that the growth outlook remains uncertain, and uneven within and across countries.

Economic activity in New Zealand has returned to close to its pre-COVID-19 level. The increase in economic activity has been supported by ongoing favourable domestic health outcomes. This has led to a catch up in consumer spending, supported by substantial monetary and fiscal stimulus. Improving global demand and higher prices for New Zealand’s goods exports are also contributing to economic activity.

The Committee discussed the key factors underpinning the economic recovery and agreed that the outlook was unfolding broadly as outlined in the February Statement. The improvement in global and domestic economic indicators, such as New Zealand’s terms of trade, have provided members more confidence in this outlook. However, the Committee agreed on the need for caution as domestic activity remains uneven across sectors of the economy.

The Committee noted areas of the economy where business activity levels remained low. The sectors most exposed to international tourism remain weak, despite the recent re-opening of travel with Australia. Business investment also remains below its pre-COVID-19 level, although recent indicators of investment intentions suggest signs of recovery.

The Committee noted that the level of employment has remained resilient. Reports of specific skill and seasonal worker shortages have the potential to put upward pressure on some wage costs. The economy is experiencing pockets of both labour shortages and employment slack, consistent with the economic disruption caused by COVID-19.

The Committee agreed that, in aggregate, the current level of employment remains below their estimates of the maximum sustainable level but expect it to converge to that level over time. They also expect to see wage growth lift as firms compete for labour, in particular given the current low levels of immigration.

The Committee noted that underlying CPI inflation currently remains slightly below their target midpoint of 2 percent per annum. A range of domestic and international factors are expected to lift headline inflation above 2 percent for a period. Members noted these factors are expected to be temporary and include higher international transport costs, disruptions to global raw material supplies and resulting higher prices for many commodities, and administrative charges.

The Committee discussed the risk that these one-off upward price pressures may promote a rise in more general inflation and inflation expectations. However, the Committee agreed that these risks to medium-term inflation were mitigated by ongoing global spare capacity and well-anchored inflation expectations.

The Committee assessed the effect of its monetary policy decisions on the Government’s objective to support more sustainable house prices, as required by its Remit. It was noted that the current level of house prices result from a range of factors including low global and domestic interest rates, housing supply shortages, land use regulations, and strong investor demand.

However, the Committee acknowledged that some of the factors supporting house price growth have eased. In particular they noted the current high rate of housing construction, historically low population growth, increased loan-to-value ratio restrictions, and the Government’s recent changes to housing tax and supply policies. These factors place downward pressure on the longer-run level of sustainable house prices and are consistent with a period of significantly lower house price growth.

The Committee noted risks remain to economic growth both on the upside and downside. However, they expressed greater confidence in their outlook for the economy given the reduced risk of extreme downside shocks to the economy from COVID-19.

The Committee noted that on current projections the OCR eventually increases over the medium term, but agreed that this is conditional on the economic outlook evolving broadly as anticipated. In line with their least regrets framework, members reinforced their preference to maintain the current level of monetary stimulus until they were confident that the inflation and employment objectives would be met. They agreed this would require considerable time and patience.

The Committee discussed the effectiveness of monetary policy settings since the February Statement. The Committee noted staff advice that the LSAP programme has provided substantial monetary policy stimulus to date.

Staff noted that reduced government bond issuance was placing less upward pressure on New Zealand government bond yields. This also provided less scope for LSAP purchases with the limits outlined in the letter of indemnity, specified as a percentage of government bonds outstanding. Based on current Treasury projections for the issuance of New Zealand government bonds, the Committee acknowledged that the LSAP programme could not reach the $100bn limit by June 2022. Members affirmed that this dollar figure was a limit, not a target.

Members endorsed staff continuing to adjust weekly bond purchases as appropriate, in particular taking into account market functioning. The Committee agreed that weekly changes in the LSAP purchases do not represent a change in monetary policy stance, and that any desired change in stance would be made via the usual Monetary Policy Committee communication channel.

The Committee agreed that the OCR is the preferred tool to respond to future economic developments in either direction.

The Committee agreed to maintain its current stimulatory monetary settings until it is confident that consumer price inflation will be sustained near the 2 percent per annum target midpoint, and that employment is at its maximum sustainable level. The Committee agreed it will take time before these conditions are met.

On Wednesday 26 May, the Committee reached a consensus to:

- hold the OCR at 0.25 percent;

- maintain the existing LSAP programme; and

- maintain the existing Funding for Lending Programme (FLP) conditions.

110 Comments

The property show goes on.

Give it up already

Wasn't there going to be a decision regarding interest only loans announced or is that expected some other time?

what a fizzer

Robertson and Orr. A couple of old tools.

Oh no, it was all wishful thinking from my end indeed. What a tragedy!

The price of a bread loaf we buy from the local bakery had increased by 25%, is Orr saying that the bakery will reduce prices in the future? Or does he just not have a clue.

He takes his instructions from The Fed. His mouth only moves when J-Pow's hand does.

To be fair: how much latitude does the RBNZ governor have to move independent of the fed (and other big central banks) without inducing wild swings in the exchange rate?

I am being fair, he is using the exact same 'transitory' guff as his master at the Fed. On the one hand you guys want to make out this guy is independent with great power, on the other we keep hearing about how he basically must do exactly what the Fed does. I see someone moving in

lock-step with his overlord, right down to the language being used.

You didn't address the point.

Moving the needle 0.25% would induce 'wild swings in the exchange rate'?

Just saying he thinks he'll do something in over a year's time has moved the currency by 1%

Lot's of hysteria about the consequences of raising interest rates, and zero thought given to the consequences of lowering them. Fools have lead us into a trap.

He must also be looking through the proposed council rates increases for the next several years in my region (and most others)

Maybe they are saying the 25% rise is it, and it won't increase much more than that. But lack of Supply and high Demand is causing this. What may would stop inflation if people stop buying , and people can't sell, so drop their prices to allow this, but that looks unlikely based on the world gearing up into action post covid, and lots of people with cash to spend. There is a huge waiting list for some types of cars in NZ with long waiting lists. I just can't see inflation dropping.

Queried the 33% increase in my local cafe smoothie - reply input costs have risen and needed to raise costs top stay in business. Inflation genie is out of the bottle Mr Orrrrr.

"Inflation: you will abate" commanded King Canute.

Inflation - "hold my beer"

He says what suits him as no one to ask counter question.

'The Reserve Bank has left the key monetary policy settings unchanged and (drumroll please) says the current visible price pressures in the economy will abate over the course of the year.

This means the Official Cash Rate stays at 0.25% and the Large Scale Asset Purchases (money printing) programme remains with a target of $100 billion of bonds to be purchased by June next year.'

We will see Mr Orr, we will see.

Come on man.

They were bang on house prices falling last year. ;0)

I hope Orr didn’t spend too long on his statement. I could’ve written it in less than 60 mins. So predictable.

The PTB have a great track record on their crystal ball gazing -

'House prices, Prime Minister Jacinda Ardern said, cannot keep increasing at the rate they are.

It was November 12, 2020. In the 12 months ending October 2020, the country’s average property value went up by $55,834, according to CoreLogic data.

One metric showed every region except Canterbury saw house prices increase by more than the average worker takes home in a year.

That one sentence jumped out: “It just cannot keep increasing at the rate that it is.”

But they could – and then some.

In the four months ending February 2021, average property values rose by $74,388 according to CoreLogic.'

Now house prices are up 24 percent in a year according to stuff. The low OCR has a lot to answer for when it comes to this, as it means people can afford to borrow more and pay over the top. Also now there are far less houses coming on the market due to it being winter. But lots of people looking.

Wise decision. The OCR should probably only be reviewed after border reopening.

Get your vaccines today!

We are going to run out ...

Certainly they're going faster at the moment than supply is coming in. See

https://www.newsroom.co.nz/charting-new-zealands-vaccine-rollout

second to last figure.

On the other hand, we need so few doses that pfizer clearly could send us all we need in one go, just about. Only question is if/when they will.

Data here: https://www.health.govt.nz/our-work/diseases-and-conditions/covid-19-no…

At least 300000 doses available since late March, so there is plenty of headroom for now.

Clearly the govt know at some point there is going to be a shortfall, which is why they have been so slow.

Also it is the only logical explanation for the latest contradiction. Govt saying we are on target and yet are pushing out group 4 (general public) to August.

Interested to see if 2.6% CPI prediction is correct when announced on 16 July. Even if it is correct it is still below the 3% top band. Although computer would say OCR up 0.25 %.

Watch all the main banks jack up interest rates IMMEDIATLY. Long term rates will get a hike in the next week im picking.

They already slid up along these lines in the past few weeks.

It was noted that the current level of house prices result from a range of factors including low global and domestic interest rates, housing supply shortages, land use regulations, and strong investor demand.

Misses out the important factor of expansion of the money supply through the commercial bank mechanism.

So much smoke and mirrors.

Yeah, let's keep the housing Ponzi running for a little longer....

Somebody pop this bubble already!!!

Maybe someone is waiting for a global pop or trigger, such as Crypto popping, causing a chain reaction? Then it can be blamed on that? The last one was blamed on the GFC, but NZ house prices didn't drop too much, they mainly went sideways. No one wants or expects to sell their house for less than they paid for it.

Bad luck Crypto popped last weekend - canary in the coalmine just flew the coop!

True, and only real markets pop. Artificial ones explode with a resounding crack-up boom.

On that we agree upon Ezy...up tick..

It seems to have bounced around since then and it wasn't a total crash. Still well above pre covid levels. The volume traded a day is a huge percentage. I fear at some point people will take their profits, and many people will be just left with a few cents. Such a huge gamble.

I am all for affordable houses, and increasing OCR. But we can not actively pop the property bubble as too many people being involved, it will bring a crash on our economy and we might not be able to recover it for many years. Good solution is gradually increasing OCR to discourage people taking on endless debts and mortgages so one day we might be able to see our economical productivities catching up with housing price.

That’s an incredibly simplistic wish and ain’t going to get you a house millennial woman.

But dreams are free

Dowding

Agreed.

Both Treasury - as stated in the Budget (and supported by Robertson) - and RBNZ comments today is that current house prices are expected to remain static for some time.

So rather than claims or wishes of the keyboard warriors on this site of a high probability fall in the market or a bubble burst is simply flying in the face of a consistent expectation from Treasury, the Government and RBNZ . . . and they have the expertise, tools and some influence. So the outlook seems a stable market with some minor growth.

It is also worth mortgage holders noting the likely increase in the OCR by 1.5 in the next three years . . . time to look at discretionary spending and paying down debt (especially any high interest debt).

Potential FHB need to consider the signals and implications very carefully.

All things being equal prices will remain steady.

The problem is, in this world things aren't equal a lot of the time.

We have financial cycles and arguably the world is overdue for a financial correction / crash.

When it comes, probably in the next handful of years, a property correction or crash is likely.

Because unlike after the GFC, the RBNZ doesn't have the ability to make repeated deep cuts to the OCR.

HouseMouse

We live in a world full of risk. We factor in those risks by being prudent - for example we wear seatbelts and look before crossing the road - but we don't go around full of doom and gloom and let those risks dictate or curtail living.

Yes, there is risk of some possibility of a significant economic correction and equally there is need to be prudent . . . but likewise we can't let it curtail living.

Actually the reality is that personal risks - loss of job, a serious accident, a serious medical issue and matrimonial issues - as well as natural factors - earthquake, flood, volcanic activity - are arguably more likely.

So agreed, there is economic risk and at the moment I would be prudent looking at my discretionary spending and paying and balancing that with getting on with life and living.

Agree with all that.

I certainly don't think the risk of a significant correction in the next few years should dominate decision making, but it should inform it.

HM

Agreed

FHB are currently facing not only very difficult times, but also considerably uncertain times.

Probably never previously more so in recent times, potential FHB face acute need for very carefully considered decision making.

I don’t envy them.

Ah that sweet feeling of disappointment

Sweet, make another few hundy this year lol

Beats working ;)

Always next year ..

Can someone please check on Stuart!!! I hope his heart can take this!

Stuart might be doing what I am - "looking through" the MPS.

I think Tom V is right - just watch the Fed. NZ Govt pronouncements are noise produced by people with no good options and clinging to hope of a miracle.

Just another day in teletubby land..... lala.

Another catch phrase for Orr to add to his repertoire, "it's transitory" can join "we need more data".

Hang on, doesn't he need to see more data before declaring that inflationary pressures will definitely abate??

"it's transitory"

So is diarrhea.

Crazy times. Hope banks are increasing their stress test on people .Some banks stress tests on people seems really low. Not sure why different banks have different stress test rates. Some seem to be in the 5's , others in the 6's. Even though historically 8 percent is a low rate. Any FHBs buying at these insane prices and getting into huge debt need to be very careful with rising interest rates a possibility. Hope they are getting good financial advice.

Still wait and watch even when all data or report suggests that market is hot and touching new heights :

https://www.newshub.co.nz/home/money/2021/05/house-prices-lifting-faste…

Real Shame to all, who are running the country and taking average Kiwis for granted.

It all comes down to greed.

“The Committee noted that medium-term inflation and employment would likely remain below its Remit targets in the absence of prolonged monetary stimulus.”

If prolonged monetary stimulus reaches a state of semi-permanence then it will probably no longer truly function as “something that stirs or urges to action”.

Eventually the existing stimulus will no longer be stimulus, it’ll be baked in – at which point however the market simply says “more stimulus please” – and the CB’s merrily reply “coming right up!”

Tell the people of Wgtn (recent water and rates increases) that inflation is a temporary blip.

But peoples houses have gone up so much in price, that they should all be feeling a lot richer. Guessing equity release mortgages are going to become more popular. Very popular in UK at the moment.

There is a quiet wisdom in that. Calculate when you think your quality of life is going to be such that you will be unable to get out and about. Then budget to spend almost all your equity on lifestyle etc then when you have only a little left, pop over to the Nederland and pop your clogs.

If NZs population drops, like has occurred in Japan, as less people having kids largely due to the high costs in NZ and having to leave having a family later, I wouldn't be surprised if house prices fall back. This would be due to an oversupply of housing. It is possible housing in more fringe areas and not close to cities could drop in price over the very long term. But that could be decades away. But maybe they will just continue to import people to make up the shortfall.

Better to spend it that way than let the govt get their filthy hands on it through estate duty.

It will be in H1 2022 I feel. Pricing is increasing out there. In my business I am hiking prices beyond the difference in input costs (commodity prices are increasing) to reflect higher costs of doing business. Min wage does not affect me directly, but indirectly where people employ MW workers they have increased costs 3%.

It's sad how Interest's comment section has changed from a forum to exchange ideas between business people a few years ago, into a endless complaint about everything and everyone.

Don't worry yvil, when property comes off the boil we'll have something else to talk about then.

We'll need to. Lol.

Agree. A few years ago it was very good with a lot of knowledgeable people.

Now it’s just a whinge fest (some of it valid) with people who want to buy homes

By knowledgeable do you mean people were saying things that your mind resonated with because it aligned with your own confirmation bias...

Just curious - did you change accounts, or did you only feel the urge to comment once it has devolved into a whinge fest?

I must admit, the housing debate only seems to get more rabid on both sides, unfortunately.

By business people exchanging ideas, do you mean property investors stroking each other’s egos, confirmation and decency bias?

Who talks about business on here? You post anything not relating to houses, mortgage rates or shit coin and there is no discussion/response..

Yeah good question.

It's been dominated by housing discussion for more than a decade.

I think Yvil is throwing his toys out of his cot because some of his old house spruiking mates like The Man etc have gone.

Also there are plenty of non housing business articles which he doesn't seem to comment on.

Odd comment.

Goodbye!

Yvil we thank you for your ironic complaint but this is actually more of a forum for knowledgeable people to exchange ideas regarding the subject at hand. Could we keep unrelated complaints to a minimum. Thanks :)

Though I too miss the good old days when the landed gentry could meet and discuss business behind closed doors at our favorite country estates. Back then the great and the good wouldn't have to share our forums with any old miserable god forsaken plebeian off the street with their sad tales of woe and misguided notions of a fair society with affordable housing for all. What business do they have amongst distinguished gentleman such as ourselves! Back to the workhouse with them I say!

I say hear hear good fellow.

Yvil,Everyday news and data released, suggest that market is hot ( even report below on same website suggest and this report is for April - after housing announcement and LVR) still denial by Mr Orr and Robertson with fimsy excuses is irritating.

https://www.interest.co.nz/property/110563/april-mortgage-borrowing-has…

This is putting salt to wound of FHB, so are bound to comment. Let this people stop giving silly reason for their excuse as many times hard to digest, not their action /inaction ( as know, where they stand and with whom) but hard to fathom their reason for inaction, which have to be countered.

alittle

In the mean time 50,000 FHB have moved into their homes in the past year.

Rather than the whining and slagging off maybe it would be better if those on this site who are affected could look at some constructive discussion and consideration of the reality of the outlook.

The focus of many of the posts on this site is that any comment by bank and other economists regarding the outlook is totally rubbish as simply as being by charlatans or soothsayers, and those with expertise such as Orr and Robertson are slagged-off. It is not about "Helping to make financial decisions" as is interest.co's by-line.

Yes, it is tough for FHB and they like others have been adversely affected since the GFC and especially by Covid.

Arguably never has there been a time to consider the reality of the current and future situation. Whining, blames shifting and slagging-off achieves absolutely nothing other than making one bitter, simply digging a bigger hole, and inclined to doing nothing . . . such posters will not likely to be among the 50,000 FHB over the next 12 months.

blame shifting?!?!

Orontogosh

Yes, blame shifting.

A common trait in many posts. A trait in which one doesn't face reality and acts constructively . . . rather just blame and slag off everybody else.

printer8

But nobody is blaming and slagging off everyone else. Some people are being critical of the central bank and government but why is that any different to when landlords and investors are critical about anything they are opposed to?

Are you suggesting anyone critical of the RBNZ and government are themselves responsible for the housing crisis? And what exactly is facing reality and acting constructively? What option is there right now for people trying to buy their first home other than borrow more money? Is pilling on the debt really the most constructive solution?

Plus you seem to assume anyone concerned about any of this madness are either a FHB or want to be a FHB. Not everyone here wants to buy one of NZ's damp grotesquely overpriced third world hovels.

Well put. I am a home owner but very concerned about the housing debacle. It's not good for the country at all, the gap between haves and have not is widening and distress is growing. Also concerned about my kids and their ability to own a house in the future

It's a fact that we have had decades of policies which have effected a massive wealth shift from younger people (and younger people's future earnings) to older asset owners. This has been because of decisions made by those in power. I don't see why it should be unacceptable to point that out. And of course people are upset about it. It has had disastrous effects for a lot of people. A lot of people I know will either never be financially secure now, are unlikely to ever able to own their own home, or have had to make enormous sacrifices to do so (like not having children, for example). It's unreasonable to castigate people for complaining about the conditions and decisions which have had such a negative impact on their lives. If you've benefitted from those conditions and decisions I suggest you count yourself lucky. If you don't want to listen to the people whose lives it has ruined then you don't have to read the comments. There's no such easy fix for those who've been shafted by decades of bad policy.

Because the boomers have done well now they pull up the ladder.

Orontogosh, there you go - Bruni has just given you an example of blame shifting.

"Its all the boomers fault, its all the boomers fault, its all the boomers fault" - the level of a five year old having a tantrum.

Really constructive and addresses problems of housing affordability.

Cheers

Why do you think it's 'blame-shifting' rather than just 'blaming'? Sometimes it's appropriate to point out that something bad has happened and that a certain person or group of people are at fault.

You seem to think that not only should people put up with the disastrous housing market, they are not allowed to point out the fact that younger generations have been shafted in favour of older generations. It's entirely unreasonable to expect people to just swallow a massive injustice and then tell them they aren't even allowed to complain about it.

If you only want to read constructive comments, then I suggest you start your own website where you can moderate the comments in the way you see fit.

printer8

Bruni can speak for himself but I don't think he is shifting the blame to "boomers" at all. To me it sounds like he is just suggesting older generations who bought homes when house prices were relatively affordable are less concerned with the crisis as they are now the beneficiaries of high house prices. They are obviously less likely to voice their criticism as they don't have to deal with the issues. I am genuinely sorry you might be offended by that but it seems to be a fairly legitimate observation although admittedly not particularly constructive. Personally I think the fact more and more frustration is making itself apparent in forums like this is a reflection of how alarming and unbearable the crisis is becoming. We should all take heed.

I wish you all the best printer8 despite our differing opinions.

Printer, it is good that 50000 FHB or moved into house but are many who are not able to afford million dollar plus ......see in auction room, how they struggle.

It is lies and manipulation that has to be pointed out.

If some good experts questions him and counter him, will not stand a chance.

I have never recalled it being about exchange of ideas between 'business people', whatever you mean by that...

House prices have dominated the website for a long time.

This could get ugly for labour and their public servant voters. A friend told me all staff had been told they were getting 1.5% salary increases for those under 100k and nothing for over $100k. A 1.25% rate increase will mean on a $500k mortgage -$300 more a month - or $3600 more a year- or twice the salary increase of these public servants

x2 workers, so still ok

Have you seen their front bench? How could it get any uglier?

I just walked out of Bayleys auction room, out of 10 houses, mostly in the greater Ponsonby area, 9 sold. An incredible 90% sales rate! Clearly the expensive end is still selling well

I wonder if these are investors who have an accountant with a solution to the interest deductibilty issue or those funded by offshore funds looking for a safe haven. Or is it possible they are FHBs with deep pockets. What was your impression Yvil?

Investors transitioning to non-active trusts. If the Government doesn't like you may as well drop out of the tax system.

https://www.legislation.govt.nz/act/public/1994/0166/latest/DLM6661704…

Philby, I think they are just home owners, the houses seem too expensive for FHB and investors, most sold between $2.65 & $4.45 Mill

So in all likelihood just 9 people buying and selling in the same market. Would be doing the same if houses were $10 mill or $100 mill.

This is a very niche end of the market. Not represtative. I forgot the exact figure but google how much the average billionaire has made in the past year. Most normal people are worse off and will continue to be so as the inflation works its way through.

All this money printing and credit is designed to plug a gap until borders open and the world economy kicks back in. But we (globally) are not healthy and currently living on credit.

House prices in nz are not the main show.

I don't think many people care about the 'elite' end of town.

Did you bid or just went for fun and hanging out with 'the elite'

Perfect example of a comment devoid of any value

Would like to have seen at least a token 0.1% increase to show they believe in what they say and to send a message other than words that recognises inflation is here.

What will Mr Robertson do now. Mr Orr, once again on public platform confirmes that it is not their job to worry about housing crisis.

When asked questions on housing, was not very comfortable but when asked what is his definition of sustainable house price by a journalist, went on a monologue with no answer.

To response from another journalist on house price, went on to give lecture how all asset class move up and down but again no response to question on house price.

On another question on house price sustanubility, his reply it seemed was that house price will plateau for number of years so after few years the current price will be justified....really....what a advise...current insane house price will be seem normal after few years......

Another conclusion was that they are of the opinion that house price cannot go up forever (rightly) so wait and watch as it government has announced some policy and also they have done a favour to FHB by reintroducing LVR.

Did anyone noticed, how many time the entire team of RBNZ mentioned "will take time and need to have patience".

Yes. It was an execution of

1. Weasel words and Kafkaesque public announcement

2. Passing the parcel of responsibility to the other office

3. Avoidance of saying words like 'fall' and 'bubble'

All his bravado and swagger from past times have gone. He comes off like an apparatchik, not a leader with things under control.

I kind of want to read Kafka again but kind of don't, because it's too depressingly familiar..

Immigration gone. Foreign students gone. NZ youth to Australia resuming. House building at record levels. Tax offset gone. New tenancy rules and restriction on rent rises and cant randomly exit tenants etc. Minimum rental standards. And now interest rate formally pitches as heading back up.

Other than it being a very lazy form of investment, why is interest only stack to the moon housing a good investment again?

It's the only game in town. Near enough anyhow.

Agree there are other opportunities out there. FBU announced a $300m share buy back today.

The trend has been that rising RBNZ rates portends an economic slowing that necessitates further cuts. Consequently I'm going to "look through" this hostile and aggressive declaration of ill intent towards New Zealands investment

property owning class. Housing is our economy, what's good for housing is good for our New Zealand.

The house i live in, has an empty house next to it, the house i moved out of last year had an empty house next to it, the house i rented in 2016 while between houses is now empty and has been for 12 months. Nope, i cant see any solution to the lack of houses. I know, lets go on about supply, supply, supply so the NZ Economy (eg housing market) can keep going.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.