The housing market was searing. Now it is merely hot.

According to latest Reserve Bank figures, mortgage borrowing in April was down around $2 billion in April compared with March.

But March had been white hot.

In April the total advanced in mortgages was $8.486 billion, down from the all-time high of $10.487 billion in March.

The latest figures are, however, a record for an April.

And it is worth remembering that until the mad closing months of last year the record for any month had been only $7.3 billion, back in mid-2016.

With the official reintroduction of RBNZ lending clamps on investors, the first home buyers are strongly re-asserting themselves.

The FHBs borrowed $1.574 billion in the month.

That gave this grouping some 18.5% of the total advanced, which is the highest share for some time and well up on the 16.9% share of the March lending.

With the fast rise of investor borrowing in the second half of last year, the FHB share of borrowing had been dropping after hitting a peak level of 20.4% in July last year.

As mentioned, the investors are cooling off. This group borrowed $1.668 billion in April down from $2.325 billion in March.

More pertinently, the share of borrowing by investors dropped from 22.2% in March to 19.7% in April.

In terms of the total borrowed in April, there's not much validity in comparing it with April 2020 - because that was lockdown month, with only $2.749 billion of borrowing.

But the $8.486 billion borrowed in April this year is over $3 billion more than the total borrowed in April 2019, which was $5.452 billion.

Of obvious interest looking forward will be seeing how much more the market cools from now, which can naturally be expected at this time of year - but more so with the various headwinds now facing the market, including the reintroduction of the loan to value ratio (LVR) limits and the Government's housing policy changes.

The extra curve ball that has now been thrown is the Reserve Bank's indication as of Wednesday that it expects to start raising the Official Cash Rate in the second half of next year.

27 Comments

No deduction for interest will take 4 years before the full impact is felt by investors who purchased pre-law change. Investors definitely feeling the headwinds.

So we will have 4 years of crazy house price rise, before seeing a downward trend.

Jay Lin

So you clearly can’t understand or think you know better than what Treasury, Robertson and RBNZ are saying.

Maybe I cannot understand clearly.

So. If I were in Robertson's chair, I would have not at least removed LVR restriction around this time last year, as I have no idea what's going on.

I guess that proves knowing nothing makes better decision maker.

Jay

For a starter: LVRs are nothing to do with Robertson's responsibilities.

Cheers

P.S. A couple of points;

- Treasury, Robertson and RBNZ see the market slowing considerably over the next 12 months and then slight 2% annual increases after that. If I was a potential FHB making decision including considering the market direction, I would be putting a some weight on that. There is no certainty, but they have considerable collective expertise, have the modelling tools, and have some influence on what they see as desirable in terms of the wider economy.

- RBNZ reduced the LVRs last year, knowing it would provide support to assets (including housing) and consequently stimulate the economy during Covid protecting businesses and jobs. In that they were pretty successful. Asset inflation (including housing) was always going to be a consequence but not a priority compared to the wider economy.

If you are a potential FHB I wish you well in difficult and uncertain times.

For a starter, RBNZ did not reduce the restriction but removed the restriction.

https://www.rbnz.govt.nz/news/2020/04/reserve-bank-removes-lvr-restrict…

And If I am an FHB, I am doomed as not many decent homes left in the market.

Auction clearance rate is still 50% even with a hideous reserve price and sellers' expectations.

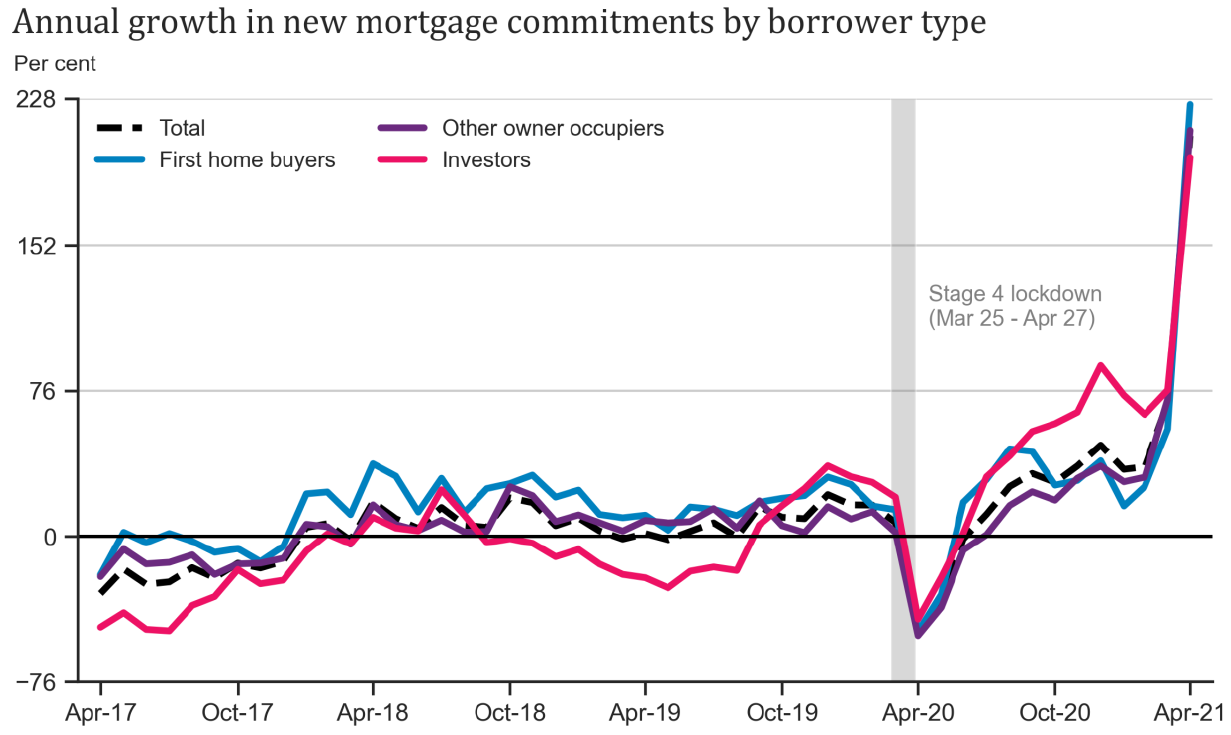

The graph above shows how the RBNZ 'protected' those jobs and businesses (for now).

Massive amounts of printed debt.

Anyone can borrow money and pretend they are successful - why you would credit the RBNZ for somehow being smart to think of this?

Most of the bottom end lives on permanent debt and financial stress ...perhaps they should join the RBNZ as advisors?

Yes HeavyG ........the only ones who are going to win are the BANKS , RE agents (some) , builders etc (some) , building suppliers etc, Councils (forever holding things up as well) conveyancing lawyers, mortgage brokers, long term property investors with no or very low debt .....so if you are in the property game now, with big debts, I truly hope there is nothing "untoward" is on the horizon, that is going to cause interest rates to rise.

As I have said on this site for years now, this whole property game in NZ is controlled by " vested interests" - see above..... and remember the banksters are in business "to make a buck" - they are NOT your friend.

In reality, how many people in numbers are in the above groups vs. the rest of us (vested interests again) ......this is just like the late 1920's, just before the stock market crash.....but this time its houses, not stocks .........hold onto your hats boys and girls !!!

anything untoward that happens will make the government and RBNZ more causitous about lifting rates, they'll protect the homeowners just like they have this last 12 months, as homeowners feeling wealthy thorugh asset inflation is what drove the economy and protected jobs. Despite all the pathetic flapping from Ardern and Robertson, this was intentional.

Perhaps it helped their narrative and enabled them to introduce tax and restrictions to control the market to fit their agenda But if this was part of a plan, then they are much smarter than I think. I suggest they didn't know what the impact of their actions were, and now politically have to be seen to be doing something to fix it.

That graph really puts things into perspective, doesn't it? Wow.

Sure does. You thought wow. I thought WTF?

You guys may have misinterpreted the graph too. The real interesting feature is the investor line tracking around 50-70% for much of the past few months, showing investors jumped into the market significantly after lockdown.

The obvious feature of the big spike right at the end is an artefact - it reflects an annual change compared to the April 2020 lows when the country was in lockdown. We'll see another similar, probably smaller, point next month reflecting still low May 2020 data, and then the line will fall dramatically again.

This is a rate-of-change graph, not an absolute value graph.

...and Mr Orr said that he has just received data / information that suggest market is cooling........

Hold on - I'm trying to figure out what the hell I'm looking at in that chart! That looks insane.

To the moon...

BTC to the moon ......and beyond !!!

Looks like recent data is year on year change from the extremely low numbers during lockdown, so looks a lot more dramatic than it is. This spike is the inverse of the dip one year ago. Will no doubt return somewhere closer to equilibrium in a couple of months.

The graph goes back to 2017? It's a dramatic increase, don't know how one could argue this...

The start of the series doesn’t affect the comparison interval, no argument needed. Comparison of absolute figures would be rather less sensational, but tell the same story.

It's quite easy. Last April the graph hits around -50%, as mortgage lending halves during lockdown. This April, we hit +200% as lending has doubled from the April low.

There will be a whole load of misleading data doing the rounds for the next few months as people compare to the lockdown data a year ago, be on the lookout. A graph of actual mortgage values rather than year-on-year change would be much more useful.

Where does it state the graph is based year on year?

The title is 'annual growth in new mortgage commitments', and the scale is percent. Follow the link in the article to confirm the numbers.

April 2020 total lending 2,749 million. April 2021 total lending 8,486 million. ~210% increase on the previous year, but the April 2020 numbers are exceptionally low. The graph is very misleading (not Interest's fault - it comes direct from the RBNZ release).

Another way to show the data would be just the raw total lending numbers i.e. April 2020's 2,749 million, April 2021's 8,486 million being plotted straight onto the graph. This would be much easier to interpret, but less shocking.

You are looking at the pointy end of the wedge that is being driven between the haves and the have nots. Orrs hand is just out of view.

Ridiculous for the average incomes nationwide ...... while we have the highest house prices in the world vs incomes......keep those interest rates down, as this is the only escape hatch .....but no matter what Mr Orr, Robertson et al do they can not control overseas inflation.

Mr Orr is always right even if one gets screwed and if Mr Orr says is good, start enjoying.

FHB borrowing reduced from $1.772 billion to $1.574 billion. So FHB borrowed less, not more, since the measures to reduce investor borrowing.

A reasonably interesting article. I however disagree on the conclusions. My casual observation of the market in a small provincial city is any drop of sales and mortgages is entirely related to lack of supply and has nothing to do with comments from politicians and bankers. A movement of 1 or 2 percent on such a steep curve is not anything to comment on. If is like debating how many angels can dance on a needle.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.