By David Hargreaves

ANZ economists say the 'funding gap' between deposits and lending is now closing, which is likely to produce an easing of pressure both on competition for deposits and on the supply of credit.

"Timely measures suggest that the hard work has been done and the ‘gap’ has closed," the economists say in their weekly Market Focus.

"While we doubt this means that conditions are set to loosen significantly, it does imply less intense competition for domestic deposits and a little more wriggle room on the credit front. Tempering at the top of the cycle lessens future vulnerabilities, and we remain constructive on the economic outlook over the coming years."

What had been a growing gap between the amount of funds banks had been taking in and those they were lending out - particularly on mortgages - has been a recurring theme of ANZ economists in recent months, along with reference to 'credit rationing' being undertaken by the banks.

The essential problem the banks face in such an environment is either increasing the amount of deposits they get in - which might mean having to pay higher interest rates. Or by plugging the 'gap' in terms of what they need to fund lending with offshore borrowing.

On Monday - after the latest ANZ Market Focus had appeared - RBNZ Deputy Governor Geoff Bascand gave a speech in which he welcomed improvements in New Zealand's net foreign liabilities (NFL) position since 2009 - but also said the RBNZ was closely watching the behaviour of our banks, and whether there would be an increased reliance on offshore funding.

'It was unsustainable'

The ANZ economists say a burgeoning gap between credit and deposit growth was unsustainable, "especially at a time of increased regulator and credit rating agency scrutiny on the economy’s level of overseas borrowing, and it needed to close".

The gap had pointed to intensifying competition for domestic deposits, higher retail interest rates and credit increasingly being rationed. "It would allow the RBNZ to be patient seeing as banks would effectively be doing its work for it," the economists said..

The said since the end of September, term deposit rates with 12 month terms and longer lift by an average of 50 bps (half a percentage point), as competition for deposits intensified. That’s against a backdrop where the Official Cash Rate fell. Mortgage rates lifted by a similar amount over the same period. If banks were paying more for deposits then borrowing rates needed to reflect the same; credit spreads widened.

At the same time lending criteria tightened, the economists said.

Credit 'difficult to obtain'

"While in part reflecting prudential restrictions, it goes beyond this. Within our June Business Outlook survey, a net 31% of firms reported that credit was more difficult to obtain, which is on par with the highest number since 2009 (when we started asking this question). It is a broad-based message across all sectors within the survey."

Credit growth slowed. In seasonally adjusted terms, monthly new mortgage lending has fallen 23% since June 2016, the economists said.

"New lending to investors has fallen particularly sharply, now making up less than 25% of the total, which is nearly 10%pts lower than 12 months prior. The latest LVR restrictions have obviously had an impact too. Total household credit grew at just 0.4% m/m in May, which is the softest monthly growth in over two years. Overall private sector credit is now growing at roughly a 5% annualised pace compared with over 8% in Q3 last year."

The housing market has cooled. Nationwide turnover is down 25% y/y, the median number of days to sell is up around five days and annual house price growth is now just 2.7% – the softest since 2011.

'Auckland has borne the brunt'

"And while Auckland has borne the brunt of this slowing (Auckland prices are heading modestly backwards and the region is one of only a handful where properties are now taking longer to sell than the historical average), a slowing theme is evident across most regions, highlighting that it is not really about any regional-specific factors."

Building consent issuance struggled to push higher. Despite strong population growth, a housing shortfall (at least in Auckland) and clear policymaker desire to lift supply, dwelling consent issuance has effectively hovered around the same annualised pace of about 30,000 for the past 12 months.

"Capacity pressures will no doubt be playing a role – the construction sector is crying out for staff – but access to capital is capping the upside too," the economists said

Financial conditions tightened courtesy of waning house price growth and slower credit growth, flagging more moderate GDP growth.

'A cocktail for slower activity'

"That’s a cocktail for slower activity growth and a tempering of topside [irrational] exuberance, which is what we’ve seen. To be fair, it hasn’t been the only factor weighing on the market and economic growth, but it is a significant one.

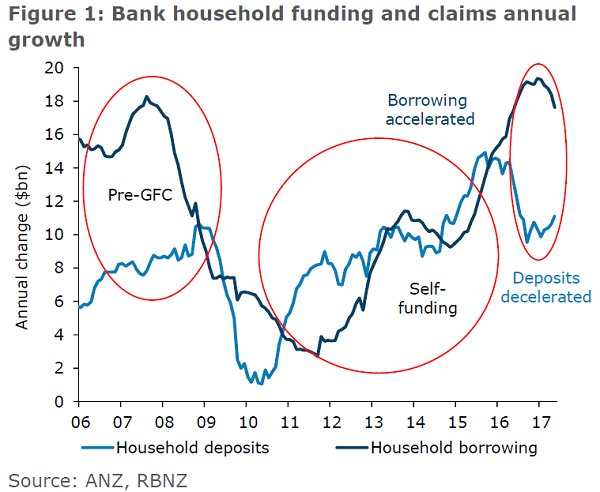

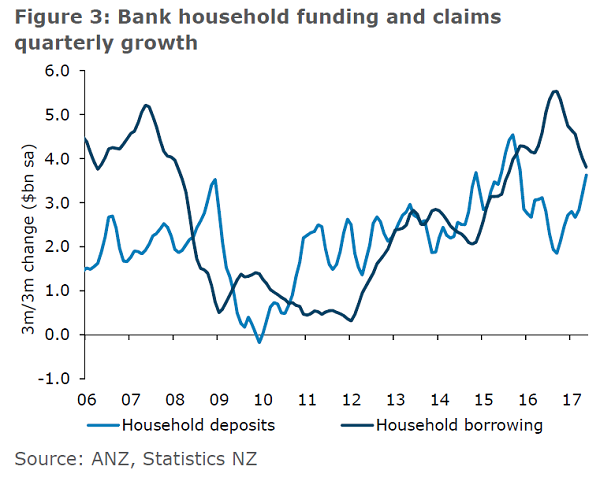

"But timely measures now show that this ‘funding gap’ has narrowed considerably. A gap remains when comparing annual household credit and deposit growth (figure 1), but over the past three months credit and deposit growth have actually run at a very similar pace (figure 3). So much of the hard work appears to have been done.

"This doesn’t mean some of the themes described above are set to reverse. We’ve simply seen the level adjust to a new equilibrium.

"However, it does suggest competition for deposits could ease a tad and there is a little more wriggle room on the lending side of the equation. We’ll certainly be watching for any signs of stabilisation in upcoming credit growth figures and how firms report overall ease of credit access going forward.

"Even if credit growth doesn’t accelerate from here and only stabilises, the drag on growth from the earlier tightening, together with the introduction of the latest LVR restrictions, should now start to wane. It leaves us comfortable with our expectation that GDP growth momentum will accelerate after the sluggish late-2016, early-2017 performance," the economists said.

7 Comments

"...The said since the end of September, term deposit rates with 12 month terms and longer lift by an average of 50 bps (half a percentage point), as competition for deposits intensified."

I cannot confirm if that is correct. I do not bank with the ANZ. However in my experience, the shorter term "special" rates eg 240 days at some other banks have been dropping for at least 3 or 4 months. One example: BNZ early June, 240 days 3.65%. Now 270 days 3.6%.

Also, Westpac 3.6% for 270 days in April. Now nothing like that.

Sure, they are talking about longer terms, but in general, I am sceptical when the banks say that competition has forced them to increase term deposit rates up to now.

Toronto House Prices Crash 192k since April.

https://www.youtube.com/watch?v=hGL0ysImPCo

Auckland Albany House Prices Dive 13.5%

https://www.stuff.co.nz/business/property/94154549/house-prices-dive-in…

The Crash Is Coming.

Term deposit rates have been trending downwards for at least a few months. However I noticed in the MSM papers, that they sad that they were trending upwards. Maybe they just publish old stories.

"ANZ economists say 'the hard work has been done' on closing the funding gap between deposits and lending; competition for deposits could now ease and there is more 'wriggle room' for lending"

Lol! What a load of BS. Anyone could see the funding gap easing as macro pru kicked in and credit demand dived as a result.

and an extra THUMBS UP for hitting the nail on the head MikeM

Well, there is a recent steady stream of NZD Kauri issuance by highly rated supranational borrowers looking to swap the locally underwritten/monetised IOU's for foreign sub-libor equivalents raised by our domestic banks. View most recent example here.

It wouldn't matter if the banks relaxed their LVR rates for investors it wouldn't change the current property correction situation. If Auckland's massive over inflated property market was due to local property Investors then we would have seen the Auckland market drop when the banks first brought in the 40% deposit required for an investment property in the latter part of 2015.

Instead the opposite happened, prices kept going up rapidly since it has been foreign investors buying in Auckland and National pushed out kiwi local investors into the province's.

It has only been since China more seriously clamped down on their capital flight for January this year that has put the breaks on Auckland's massively over inflated house prices.

So far we've seen a drop of -4% in Auckland. Letting the bank's allow more debt levels is not the answer. Allowing the market to recorrect its self to more affordable levels is the right thing to do.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.