The Reserve Bank will be forced to slash interest rates in the second half of next year in the face of a tanking housing market, independent global researcher Capital Economics believes.

Capital, which has been forecasting since January this year that falling house prices will force the RBNZ's hand, is now predicting New Zealand house prices will drop 20% by the middle of next year.

And it says the reaction will be three cuts to the Official Cash Rate, totalling 75 basis points, in the second half of 2023.

Capital Australia & New Zealand economist Ben Udy, who was early last year first to forecast that the RBNZ would need to start raising the OCR, says house prices in New Zealand "are tumbling and all signs point to a further deterioration in the months ahead".

"On that basis, we are revising up our forecast for the peak to trough decline in prices from 10% to 20%. That’s why we expect the RBNZ’s hiking cycle to go into reverse earlier than most anticipate.

"We were one of the first to forecast a significant housing downturn in 2022 when we made the prediction a year ago. REINZ median house prices have been generally falling since November last year and are now more than 5% below their peak. Prices are still higher than they were a year ago but the weakness in sales indicates that the downturn is set to intensify. That suggests that our forecast of a 10% peak to trough fall in prices is far too small."

Udy said since making the earlier forecast of house price falls, the outlook has deteriorated.

"First, we now expect the Reserve Bank of New Zealand’s policy rate to peak at 3.5% instead of the peak of 1.25% we had anticipated last year.

"What’s more, the government introduced responsible lending laws that contributed to housing credit growth slowing from 12% [year-on-year] in the middle of last year to 8.7% in March.

"Admittedly, our previous expectation that the RBNZ would implement DTI [debt-to-income] restrictions now looks unlikely. But we were right that housing affordability was set to become more stretched than ever before. And in the months ahead, rising interest rates will more than offset the impact of falling prices and stretch housing affordability even further."

In a global outlook on houses in March, Capital economists had singled out the NZ housing market as one of the ones they were most worried about.

Udy noted that New Zealand has experienced just one significant housing downturn since the 1990s, which occurred in 2008 following the global financial crisis.

"Our forecasts for interest rates would be consistent with prices falling 15% y/y before long and keep falling until the around the end of 2023. (See Chart 1.)

"That suggests the downturn may result in a 20% fall in prices.

"Even such a large drop in prices would only restore affordability to its late-2021 level or its pre-GFC peak, which would still be very stretched. (See Chart 2.)"

The RBNZ recently indicated that house prices would become 'sustainable' if they were about 5% to 20% lower than they are currently.

Last week, when hiking the OCR to 2% and signalling the OCR would hit nearly 4% by the middle of 2023, the RBNZ said it saw house prices falling, from peak to trough by about 15% by 2024.

Udy still expects the RBNZ to continue hiking rates until the end of this year.

He believes the housing downturn will be a "drag" on the NZ economy.

"...And the hit to construction activity will grow as both the length and the depth of the downturn increases.

"But the deeper downturn will have more severe implications for recent home buyers.

"The RBNZ estimates that if house prices fell by 30% then 10% of mortgage holders would be underwater, that is, they will have mortgages that are larger than the value of their homes. That situation can lead to an increase in defaults.

"Admittedly, a 30% price rise would be much larger than we anticipate. And defaults are currently very low, so a small rise wouldn’t be a significant concern for the financial system.

"But we suspect that even those underwater households that avoid default will tighten their belts considerably.

"That’s another reason to expect a slowdown in consumption growth in the years ahead," Udy said.

By the middle of next year, he thinks the impact of the housing downturn "will be painfully clear".

"And we think house prices will be at the bottom of the RBNZ’s estimated ‘sustainable’ range.

"On that basis, we think the Bank will cut rates by 75 basis points, starting in the second half of next year.

"That should be enough to stabilise the housing market and support a rebound in GDP growth."

172 Comments

you see RBNZ does what FED does.

it sounds independent but not.

As always, "as safe as houses".

Only wish I wasn't renting.....

TTP

A bit early but expected.

Also keep an eye on the coming “special offers” as banks are looking to attract businesses.

The next 2 years or so provides great opportunities for those who are looking to buy, more stocks to choose from and be able to negotiate in a less competitive environment.

These people should wait till crash has finished before talking up market again, will probably take till 2025 till we hit bottom of market downturn and will stay their for years.

The headline is misleading. The RBNZ has never identified a specific range where prices are sustainable - they've simply estimated the drop required to get us to a vague level of "sustainability".

The housing market could easily be lower than that, yet still be above the threshold where they would consider easing was required to prop up prices.

What they do keep mentioning is the "pre-covid peak" which suggests that's the level below which they'd start getting concerned. And there's a long way to go before we get there...

Politically sustainable. People view the additional paper equity as theirs by right. Whoever is seen as responsible for its removal will not be popular.

Demonstrating it's really a welfare scheme for the wealthy, not a free market where downward price discovery is allowed.

By the end of next year it wont matter what they do with the OCR, we will be in the thick of it. A 20% is a bit optimistic I wouldve thought, unless you are talking next month.

'Sustainable' for whom? In 2016 Don Brash reckoned house prices needed to fall 60% to be affordable. And house prices (no, land prices) have soared between 2016 and 2022. Property prices would need to fall 80% now to return to the internationally recognised affordability ratio of the median house price being three years' median net income.

https://www.stuff.co.nz/national/politics/81926709/don-brash-auckland-h…

internationally recognised affordability ratio of the median house price being three years' median net income.

In what market and century did we have this ration? I don't believe this ever existed!

1.5x to 2.5x income was normal in NZ until the 90s.

Even in the 90's. 3 brm onehunga 123k (circa '93), I was earning 40k, plus a car.

In '93 house buyers in major cities around the world didn't have to compete with 140M Chinese (top 10% of the 1.4B population, very affluent) and their cash printing machine.

I tend to agree with the predictions here but am a little more circumspect around the RBNZ's ability to start OCR cuts if the US and Europe are still going up or are static and high. The NZ dollar would tank.

Other countries will be cutting too…

I wish I could share your confidence - Germany's data today is eye watering.

Wait until they shut down their remaining nuclear plants at the end of the year. 12% of electricity generation in the middle of winter.

Bet you they don't. Their friendly local alternative energy supplier is looking dodgy......

The operative word being 'today'. Economic growth trajectories can change drastically within a matter of months. And I'm sure they will.

RBNZ:

"House prices are not our remit"

"House prices are largely outside our control"

"House prices are above sustainable levels"

So if prices drop 20% to presumably more sustainable level we expect the RBNZ to emergency slash rates?

What happens if

1) House prices crash 30%

2) CPI stays stubbornly high in the 5-10% range

3) Unemployment starts to rise

The RBNZ's CPI mandate suggests they should not slash rates due to the CPI. However the RBNZ's employment mandate suggests rates should be cut to increase employment. They RBNZ will effectively face a monetary paradox of sorts. As they can't solve the CPI issue without raising rates, yet to lower employment they need to decrease rates? This is why you don't let art's majors dictate your monetary policy. Art's majors are all idealists.

Arts majors are all idealists.

So are all cynics, for what is a cynic but an idealist beaten down by reality?

Which discipline should dictate monetary policy in your opinion?

Economics is a social science anyway, so what's the big difference?

... lemmee get this straight : the Covid19 spurt saw house prices across the nation rocket 40 % ... on the back of the Reverse Bank crushing the OCR to the lowest level ever ....

But , they'll only allow house prices to snap back one half or so of this artificial gain ? ... WTF .... are the directors of the RBNZ that badly incompetent ?

Incomes are also up - perhaps by 20% over the 4 year period.

Nah a 40% gain followed by 20% loss is a 12% gain overall. If you consider wage inflation over the period from 2019 until EOY 2023 would need to be 3% each year to hit 2019 level house prices adjusted in that scenario. Some areas of the country are getting close to this already.

Unfortunately the increased prices we saw during covid is considered the new normal. Im not sure if they’ll slash the OCR in 2023 but I think they will be cautious with the current approach

“Unfortunately the increased prices we saw during covid is considered the new normal.”

Just like petrol and takeaway meals, people just get used to it.

20% nominal falls....add in a few years of 8% inflation....suddenly the real price drop is becoming quite significant (assuming the forecast is accurate and inflation is persistent..)

My debt is eroding very nicely

So will the real value of your assets :-)

The value of the asset drops wether there is debt on it or not, thus far better to have some debt on it.

That is a very simplistic view to take. The point of entry and the quantity of debt relative to the price would be very important in this view.

You can try telling somebody in negative equity that the amount of debt they have relative to the asset price doesn’t matter later this year if you like? While the costs to service the debt keep increasing… then somebody else buys the equivalent house for 20% less isn’t in negative equity and has lower mortgage servicing costs.

Why would you even say far better to have debt now, when interest rates are going higher and higher? That's the real killer in this rising cost-of-living environment, is debt.

This whole "inflation eats away at debt so that's a good thing" is nonsense. Banks who lend money get to set the interest rates, and no doubt they would raise to a level to prevent you robbing them of their wealth....

I love having my debt eroded at 6.9% CPI while paying 2.89% interest until August 2024

Your debt is eroded by your personal increased income not by general CPI.

But you know that already.

Yes, that's true

So your cost of living is going up at 6.9%....is your business net income or wages you take from the motels also going up at 6.9%....or wherever else it is that you earn a living?

(and if so, well done to you.....but that isn't representative of the economy as a whole....which is what I'm talking about....and not your personal circumstances)

They don't call it the "Anchor Motel" for nothing.

Anchor Motel, complete with turtle neck on the contact us page.

You got it Dan.

He's done very well out of the government and beneficiaries he openly despises and bashes, emergency housing residents have been keeping his motel business going, propping up his lifestyle in St Marys.....

I am having that debate about whether to pay down any debt when a fixed component comes off later in the year, or just wear the small increase in payments and hold the larger debt. I need to figure out my maths for how to establish which might be better in the long term.

Put the spare cash in an offset facility. Best of both worlds.

ASB only does Revolting Credit, not savings offset. Which seems slightly less securely mine, though I do have a large RC at the moment, not drawn down at all. Bit of an irritation.

You gotta watch out for that revolting credit hoho

If you buy a house outright and it drops 20%, you lose 20%.

If you buy a house with 50% LVR and it drops 20%, you lose 40%.

Inflating asset prices against the dollar will inflate away your debt. Deflating asset prices will have the opposite effect. What would inflate your debt away would be increase wages that pay for that debt, yours or your tenants. However interest rates and CPI inflation are currently deflating wages.

HPI and CPI are different metrics and inflation is in CPI currently. So if your debt is against increasing value of consumer goods and services, it is being inflated away. If your debt is against a house it is currently increasing in cost.

Agreed with your post but that's not what is being discussed in this thread. We're discussing debt.

I think you mean Yvil is discussing debt....but nobody else is because they can see the interdependent relationship between asset prices, debt, income, CPI and interest rates.

Incorrect, nktokyo started discussing debt, here is his post:

by nktokyo | 31st May 22, 11:44am

My debt is eroding very nicely

Lol - you replied to me and not ntokyo...

"The value of the asset drops wether there is debt on it or not, thus far better to have some debt on it"

In which you start talking about asset drops as well as debt.

But have subsequently decided that you are only talking about debt and not the relationship that occurs between asset prices and debt (which is incomes, CPI and interest rates).

Just trying to connect the dots for you but it might be a stretch too far.

Yes I replied to you, on purpose, because you said "you mean Yvil is discussing debt", so I quoted nktokyo to show that he started talking about debt.

Here is the thread (time stamped) to clearly show:

1) nktokyo started talking about debt

2) you replied by talking about assets

by nktokyo | 31st May 22, 11:44am

My debt is eroding very nicely

by Independent_Observer | 31st May 22, 11:47am

So will the real value of your assets :-)

IO, you are extremely disingenuous, why just not admit, you are wrong?

Yvil - I think as is often the case, we see issues from completely different points of the spectrum.

Will leave it at that as there is no point resorting to personal insults.

Have a good night.

The one comment missing from the reference is the very top one, all good FTFY;

0) IO opened a thread talking about asset value and inflation.

It’s ok we all get confused.

Anyway the relationship with debt in NZ is swinging massively currently and during a time immediately after record high debt volumes, times they are a changing.

I do wonder if in 20-30 years time the generations hit hardest now will be advising against debt in NZ to the same tune as generations hit hardest by the 80s crash advise against investing in the stock market.

OP (IO) comment was price drops and inflation, then came the comment on inflating away household debt based on CPI inflation, which is a backwards observation.

The 2.x% you mentioned you locked in until 2024 has been inflated away based previous years inflation in asset prices, not current inflation. Come 2024 you may have paid down debt but the % equity in the asset could have decreased still - depending on how leveraged you are. If you've got high equity it shouldn't matter too much. But again, none of that really matters until you liquidate the asset. All that matters in the meantime is servicing the debt, and to do that you'd need wage inflation to be truly inflating away the debt as was the original post.

I too could decide now to change the subject and reject your comment, but that would be silly and a waste of your time.

* correction

If you buy a house outright and it drops 20%, ON PAPER you lose 20%.

If you buy a house with 50% LVR and it drops 20%, ON PAPER you lose 40%.

You only "lose" the money when/if you sell. Something that people on here always forget.

House prices went up like crazy, now they are going down, in a few years time they will be going back up again. Only matters if you have to sell.

Funny how when prices were going up and I tried saying they were just 'paper gains' but was told no no no its wealth....so if they fall, and you purchased at or near the top, is it wealth destruction?

Sure for people who purchased 5-10 years ago or more....no drama....but for the thousands of FHB's who loaded up with debt the last few years...its quite a serious problem.

And its also a big assumption that in a few years time, house prices will be going back up again.

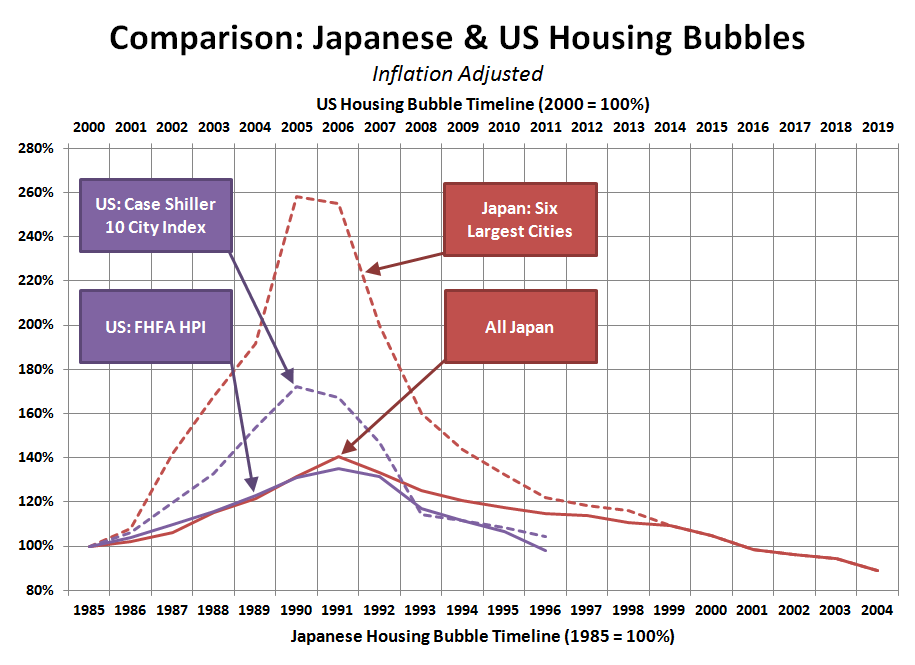

The anglosphere may have just done what Japan did in the 1980's....and its very possible that we have stagnant house prices for years or decades. Those people who purchased could be in negative equity for a very long....not saying that is a probability....but I am saying its a possibility that should be considered/factored in to the discussion.

I don't know who the paper gains comment is directed towards?

Only if they can't make their repayment obligations and have to sell.

A few years time, sure, might not be heading back up by then but over the lifetime of the mortgage they will eventually be positive.

Yes over the lifetime there is a reasonable probability, but not necessarily a certainty given the amount of price appreciation that we have witnessed the last 20 years. We've essentially taken 50 years or so of historical price appreciation and packed it into the last decade or two. Without mortgage rates being able to continously fall further...the only way for prices to appreciate further is for wages to start to outstrip inflation so that the growth of the cash flows is higher than the rate at which they are discounted. Or to import overseas capital...but that has more or less been stopped for now.

https://seattlebubble.com/blog/wp-content/uploads/2011/09/Japanese-US-H…

{kind=link}

Yes agree, paper only. I did think the same, only matters if you have to sell… however changing my tune a little after getting a better understanding of some of the predicaments some investors and FHB may be in.

It only matters if you:

- Have to sell.

- Are trying to buy.

- Need a line of credit for renovations etc

- Need credit for unforeseen circumstances.

Bit of a stretch the last one but declining equity could effect your line of credit against mortgage. If for example small time investor needs a root canal and has little to no cash (I know this happens, unreal) then accessing money will be more difficult and more expensive.

It actually has a fairly significant impact on access to debt, and it’s clear we live in an economy with household debt as it’s foundations. With paper loss comes increased debt to equity ratios. It really matters a whole lot more than just when you sell.

Now it's worst time to hold debt, why?

1. Your wage growth is not keeping up with inflation.

2. Interest rate is higher than your wage growth.

3. Assets values are decreasing and likely will be flat in future. So your debt is not generating returns.

1) I don't earn a wage, I own a business

2) my interest is 2.89% until August 2024

3) Again, we're discussing debt, not asset value

Then you should add "base on your own personal circumstances".

I've come to realise that when you have discussions with Yvil its about what is happening to Yvil and not necessarily and always to the economy as a whole.

Bang on IO.

Yep, it's all about Yvil........

That's very much what I did coh, when I wrote

by Yvil | 31st May 22, 2:07pm

I love having my debt eroded at 6.9% CPI while paying 2.89% interest until August 2024

Read the thread before assuming

My comments were responding to your

by Yvil | 31st May 22, 12:29pm

The value of the asset drops wether there is debt on it or not, thus far better to have some debt on it.

Maybe you should read before assuming?

"we're discussing debt, not asset value"

It would appear that you are, but nobody else is because asset prices and debt are interdependent factors on a persons individual balance sheet when it comes to residential property.

Incorrect again, nktokyo started discussing debt before you changed the subject to assets.

by nktokyo | 31st May 22, 11:44am

My debt is eroding very nicely

Lol - and you replied to me about asset prices (and debt). But appear to miss the relationship that happens between asset prices, debt, income, CPI and interest rates.

Incorrect again, I’ve just started talking about the price of fish. And I don’t think household debt has anything to do with fuel prices increasing the price of fish and chips.

Depends on asset and incomes amount of debt ... I was banking with ASB years ago just after the GFC ..LVR less than 50% ... also had a small investment loan ...and they basically told me to go elsewhere for lending after... I never missed a payment ..banked with ASB for several years 20yr+ same job....incomes easy covered all outgoings ... but they just wanted me gone as they didn't like my business investing in companies on the ASX .... the same is going to happen for thousands of Kiwis with businesses and investment properties ...etc ..when refinance comes around they will be shown the door ...spending will fall it will be like dominos hitting all NZ business and asset values

Yea I’ll admit I had the same thought process as everybody else “only matters if you have to sell” etc etc

But in reality, holding significant debt in a market trending down as some pretty unavoidable consequences depending on your situation. Banks looking to de-risk in the face of recession won’t be afraid to shut the door.

A comment yesterday, somebody’s neighbour went to the bank for support as they weren’t sure they’d be able to make high interest payments and no support there. Rough ride ahead unfortunately

Between 1971 and 1982 my house value went from 4,950 pounds to 47,500 pounds. My mortgage in 1971 was horrendous but inflation made it almost go away so that I could upgrade to a vastly superior house. In the short term there may be a bit of pain that has to be managed but in the end inflation is a mortgage dream come true. My wages during this time went up in line with inflation.

So are you predicting 20% mortgage rates in 10 years time as was the case in the following period (1980's) to recover the economy from that level of inflation?

Pounds finished in 10th July 1967.

Mate back then the mortgage rate was 4% and fixed for 25 years with a govt loan.That advantage does not exist today.

Depends which index you use.. the block of cheese index, the big mac index, or the litre of petrol index. That last one is great, we've almost halved our mortgage in 2.5 years.

Right....so you spend all your money on petrol then do you? Must be a good way to lose weight...by not eating anything....and it also must be very cold a boring by having no power, no internet, no television.

I'm thinking I might be on the wrong website given the level of thinking that is going into this from some people.

Society is currently experiencing financial repression as the cost of living inflation far exceeds wage inflation.

If you think conditions of financial repression are a good way to pay down debt....lets see how the next few years plays out.

As always I think it is peoples ability to understand other peoples point of view...

Person A - Mortgage free and with significant cash in the bank, for them interest rate increase is a positive

Person B - Mortgage on house, increase in mortgage payments means less money for other expenses. Also reduces ability to pay down debt as that money now goes toward debt servicing. For them increase in rate is negative

Person C - Doesn't own a home yet but with prices sideways or declining they can spend more money in the economy on other things rather than saving every dollar toward a deposit. They will also get a savings rate bump. For them an interest rate increase is positive.

Fair call

(As long as they are in a position to resist rent increases arising from landlord mortgages)

*Assuming that the average landlord has a mortgage?

"Real" house prices don't matter.

Existing owners care about nominal prices (mortgages are nominal).

Potential FHB care about prices relative to income, not relative to CPI.

Ok then prices might fall by 20% in nominal terms and then can be adjusted relative to income growth not CPI - would that settle the nerves a bit better for you?

We experience the economy in real terms not nominal terms. And if you don’t believe this to be, then there is no such thing as a cost of living crisis. It’s a make believe myth 😜

The RBNZ is not required to "sustain" house prices under its mandate target, only to advise the Govt of the expected impact of RBNZ actions such as OCR on house prices.

In theory, house prices will be "sustained" at whatever price level the various market input factors (eg mge rates, market sales volume, rental investment criteria) are assessed at by willing buyers & sellers in an open market. Which is as it should be.

B...b...b...but house prices aren't a factor in RBNZ's MP decision-making process, yet here we have learned persons implying the exact opposite - that they're actually a primary driver. WTF?!?!?!

House prices are of absolutely no importance to the RBNZ. The RBNZ couldn't care less which way they go.

Unless house prices fall of course. Then the RBNZ have to step in to prop the prices up.

But again, to be clear, the RBNZ does not care one jot about house prices.

Sincerely,

A. Orr

Exactly:

Reserve Bank governor Adrian Orr is not doing himself any favours with his revisionist approach to the house price issue. Not so long ago, he was saying increasing asset prices, including house prices, were a feature and not a bug in the bank's policy response to the pandemic because they make consumers feel wealthier and spend more. This week he suggested his bank's policy settings have only a minor impact on house prices.

He actually has quite a bit to answer for. The bank has been consistently under-forecasting increases in inflation and house prices, and overforecasting unemployment. While no one is expecting perfection in these times, the ongoing nature of the forecasting issues is concerning. Link

Hah! thanks for this. This particular gem struck me:

"The Biden White House has decided the answer [to CPI increases] is easing supply chain bottlenecks. That sounds as likely to be as successful as New Zealand trying to build its way out of high housing prices. Both approaches ignore the core of the current problem: massive boosts in money supply and ridiculously cheap credit.

This shows the leopard can change its shorts. It's not a supply problem resolvable by increasing the supply of land now he's not an MP. Stephen , have a chat with Nicola and Christopher will you?

Falling house prices will decimate the economy as its based on building new houses.... been to Queenstown recently? if housing stopped down their many many locals would be underwater as their income will drop to zero.

Same in Jaffa land.... cheap foreclosed utes are coming peps

Yes and it could play out similar to Ireland where if the slow down occurs in construction, those people in the industry who lose jobs/work decide to pack up and leave the country, reducing GDP further and freeing up more homes for sale on the market (and less renters for landlords).

Isn't that what's already happening? There have been constant headlines recently about construction not being able to get supplies, builders shutting up shop, people leaving the country that had come in during covid etc...

Back in the old days we had the Ministry of Works to smooth over the rough times. But then the ideologues in Treasury won the battle and got rid of them.

that was a long long time ago

The Government could step in and really ramp up its state house building programme, working with the private sector. It would also be in a position to increase the number of Kiwibuild homes. This would have the benefit of mitigating the very damaging boom-bust nature of our residential construction sector.

Look at the Stats NZ experimental data series just published today https://www.stats.govt.nz/news/stats-nz-releases-experimental-indicator… and at table 4 - shows the median days from building consents issue to key milestones - yes data delayed and covers only 22/81 BCAs but covers 60% of new homes consents (stand alones) and also has the proportion of consents that have reached milestones. Yes data not fully up to date but could be telling us the housing market has already gone off the cliff, just not hit the bottom yet

Exactly.

And that's long been the basis for my view that:

1. The OCR won't rise as high as projected

2. It will be slashed far quicker than projected

Our property-dominated domestic economy is going to be a shambles by late 2022.

BuT thE p0NzI!

Let me get this right, so they are predicting inflation will be completely gone by the second half of next year and New Zealand is in recession where CPI will be dropping just based on 20% housing price deduction? I feel there are lots of holes in this prediction.

First, as many people pointing out, 20% housing price deduction will just get us back to where it was one year ago. Majority of house owners' equity is still positive, while their wages are catching up, the demand is still there. Second, if recession happens, we will not be looking at 20% housing price deduction, it will be more than 20% as companies go bankrupts, people will lose jobs, which cause much higher rates of mortgage sales.

Yet just today we learn that the ANZ expect values to fall by 11% ( see other post on this website) ; and Zollner et al use the word "soggy" to predict future growth. Theres too much bullshit spreading currently. The banks don't want to spook the market or admit that they've screwed up by lending too much cheap money .

Historically; Peak to Trough [housing bubbles globally] takes 3-5 years.

These predictions from Capital Economics may be predicated on a correction rather than a popping of a 'housing bubble'. Certainly they believe the RBNZ is a White Knight to the Speculator.

The UK in the early 90's def 3-5+ years top to bottom... the Neg equity at the bottom slowed recovery IMHO.....

Def feeling like Wile E. Coyote and the Road Runner ... BeepBeep

Interesting tweet comparing the speed of our correction with the USA correction (we are correcting much faster, so far).

https://mobile.twitter.com/AvidCommentator/status/1531480014960869377

Only what I have been saying… they will need to slash by more than that though. And I think it will be by April/May 2023.

So if we are refixing in Jan 2023 it might pay to just ride the floating rate for 6 months then look at a fixing once the RBNZ starts throwing out cheap debt again?

Who knows really, but I come off a one year in late November, at this stage I'm thinking I will float maybe for 6 months, by mid 2023 I expect fixed rates will be coming down significantly, and I will then fix.

But things could look a lot different by late 2022, so let's see.

There seems to be an assumption that house prices tanking and inflation rate heading back towards 3% are a given, basically I'm guessing due to the infamous wealth effect. But what if houses tank and inflation is still above 5% by mid next year, everyone stops spending but inflation remains high. What then?

Is it a given that the ocr will be coming down next year?

If NZ doesn't get on top of inflation, … we will face very, … very difficult times

Inflation is almost entirely due to high energy prices (greenflation/Ukraine), supply chain disruption (Covid) and border closure (labour shortage). The housing market has alreaady stopped in it's tracks - which means ORRdinary is now trying to send businesses bust and the average punter to th dole queue.

So how about we either put up with it until it burns itself out (it will) or alternatively drop the ETS, start fracking and open the f**-6-n border like 99% of the world....

It’s also because we failed to invest in manufacturing capacity…

in fact we closed a lot down but it made the numbers look better…for a while

I think they will target inflation foremost. But if house prices get to the point where it could threaten bank stability then they will have to u turn. That should be a pretty big drop considering any loan taken out more than say 2 years ago is currently about 30% up plus whatever the deposit was.

Much better analysis than any of the local economists.

"On that basis, we think the Bank will cut rates by 75 basis points, starting in the second half of next year..."

Who said they will? Is this a best guess or is it the painting of a rosey picture for those who are reading this to not panic yet?

Real GDP for 2022 is at 0.8%. Real unemployment is at 11.2%

Real inflation is at 6.9%

So really we're already in a recession heading toward Stagflation🤔

I do not believe that unemployment number there are lots of jobs in tourism in NZ as it opens up, if there is a global recession and tourism dries up then a lot of the south island is going to fold.... and rotorua

Tourism isn't a high paying industry and they don't want to be. They've made that clear. In the context of spending, the question is more about 'how many well-paying jobs are there that leave people with meaningful discretionary spend?'.

The answer is: 'less and less'.

Also a lot of Tourism operators are owned by overseas organisations so the profits head off shore, much like our banking, our supermarkets etc.

It's not only tourism, it's everything comes along with it, local businesses, retail, local councils, IT...

The StatsNZ number is the dodgy one. 1hr of work equates to being fully employed.

Case managers not keeping up their KPI's with people for appointments and phone calls and Cv writing means that those people are unavailable for, or aren't looking for work.

The 11.2% fig. is the number of people in receipt of a benefit. About 349,000 people. MSD's most recent quarterly report.

At some stage the RBNZ may well decide to focus on non-tradable inflation and focus on bringing that down to less than 3%. Once that drops below 3%, and if NZ is in recession, then they may lower interest rates.

I regard it as highly unlikely that house prices per se will be particularly important in their considerations, except to the extent this drives a general recession.

I see no alternatives that will sustain the exchange rates at current levels, but the timing will be determined by the financial reef fish, and that timing is not predictable. When it happens, then tradable inflation will rise further.

KeithW

Good point to include the FX in the OCR equation as well, Keith

"Nzd not sustainable at current rates". Do you mean it will drop further? Had a moment where I wondered it you were thinking of a rise in the nzd.

Keith, with house prices already down 10% to 20% I would say non-tradable inflation is probably already negative.

Higher house prices through Covid supported the economy due to the wealth effect. Falling prices means the economy is toast now. I wouldn't be in consumer discretionary for love nor money. Call Stabicraft and see how the order book is looking...

That would be literally the same mistake the FED made in 1929 prior to the Crash, where they had raised rates and suddenly dropped them again, leading to insane speculation and public sentiment was genuinely rabid for getting rich quick without much work.

Looking forward to the next great depression.

The mistake was to hike rates into an already falling market. I cannot believe we did not learn from history and made the same mistake again.

I have long said that a reduction in the OCR is likely in the second half of 2023, but it's not just because house prices will be down, it will be mostly because of the recession in the first half of 2023, and the many job losses that come with it.

Agree Yvil.

We need approx 100k people to lose their jobs to get to a healthy unemployment level in NZ. the Reserve Bank is gonna welcome those job loses because that means we have a “healthier” economy than currently. Harsh but true. A 3.2 unemployment rate is crippling.

I agree in principle. That said, a reduction of OCR is required much sooner than 2023, to prevent an economic crash. I cannot understand why they have been hiking rates so aggressively, the economic crash that is beginning now was entirely predictable.

Independent commenter says things are tumbling. As they should, lets face it, you would have to be blind to not see that. I think this is a bit behind the drops but he is probably looking at older stats vs. the coal face of transactions. Speculand in Wellington and Auckland is already down 20% and still falling. We so need and Irish or Iclandic like reality check on foreign debt speculation.

Will the RBNZ actually continue to do its job of inflation control, or flip to a non mandated protection of foreign bank debt speculation....?

An overlooked issue is it all depends on what is happening offshore, we will not be dropping our rates if offshore rates are climbing. To do so would invite a decline in our currency increasing inflation. In this way it is irrelevant what housing values are they do not will not drive interest rates .

Agree with this, if the Fed start pencilling in rate rises, NZ will have to follow suit, also europes inflation is peaking, Germany hitting over 8%, and we all know what happens when there is inflation in Germany :P

Recessions and Depressions break onto land offshore... then wash over NZ... Chinese are so screwed here.....

I tend to agree, although I suspect the RBNZ will pause their hikes for a while before cutting. There's so much private debt out there that the doubling of interest rates (even from a very low floor) recently combined with a huge volume of refixing over the year will act like a giant vacuum for discretionary spending.

So far nobody believes that the OCR will actually reach 3.9%....

They should be up around there already but they aren't and if they start cutting rates within the year they tell everyone inflation is priority number 1 then they'll never be taken seriously again and the average person will be back to ticking up as much as the retail banks will lend.

What we need is an Act of Parliament legislating a minimum DTI level that the RBNZ could make more stringent if needed, so we don't have to rely on the RB to require them. They should always have been in place. LVRs could have been adjusted, but not DTIs.

Here is part of the response I got from a current Labour MP yesterday:

"On your point about the RBNZ introducing debt serviceability restrictions (debt-to-income ratios, or DTIs), I would note that last month, the Reserve Bank announced that they intend to proceed with designing a framework to operationalise DTI restrictions, in consultation with the industry and other stakeholders. ... In August 2021, Minister Robertson agreed to update the Memorandum of Understanding (MoU) on macro-prudential policy to enable the addition of debt serviceability tools"

I have emboldened the bit that annoys me - industry and other stakeholders. Well, I don't see the banking industry being particularly keen to move back towards realistic DTIs (The interest gained on a 7 DTI far outstrips that on a 3.5 DTI), so fully expect to see them pushing back against that. I'm also curious why the government does not consider citizens as part of "other stakeholders" - I guess because there is a small minority who want crazy DTIs so the rest of us who just want something reasonable don't matter?

But basically I was peeved because Labour literally intend to sit on their hands and pretend the housing crisis is somehow not part of their "mandate".

There would be general consultation on that issue, so any pleb could submit. True though that they'll actually meet with the big stakeholders, whereas they won't meet with you outside of a public meeting.

Whilst I agree generally with the article, it is missing two vital words, being "inflation" and "recession".

Will inflation be lower in 2023? If it isn't and house values are indeed down by 20%, would the RB drop the OCR at the risk of stoking inflation?

A recession is very likely by end of 2022 early 2023, to be clear, this means loss of jobs and a lot of pain. This will be a strong factor in reducing inflation and probably a stronger reason than house price drops, to lower the OCR in the second half of 2023

Somebody should let the government know before they approve another 200k round of mass immigration.

Don't worry, droves of young kiwi, skilled professionals, and migrants are abandoning NZ. International moving companies are booked out months in advance for people leaving; similarly story for flights out.

Let me explain what RB means by sustainability, 'the maximum a parasite (extra non-value added costs due to Govt. policy), can extract from the host without killing it,' ie about 10x median income multiple.

Definition of sustainability in other jurisdictions where Govt has their housing shit together, 'no parasites so host happy and healthy, 3 to 5 x median income multiple.

Read a article on bbc website today say NZ one of most expensive places to live for property in the world a people leaving for Australia as can’t afford to live here. Just let house price’s drop

I want a future for my children and there is none in New Zealand. ✈️✅

7% guaranteed

Omg you spammed. Waah wahh.

Copying you champ.

So how does that work? There is 7% more future, guaranteed?

I was going to say that the IQ of both countries and increased, but after reading they were leaving Wellington (after all, they constantly vote the likes of Grant Robertson in!) I thought, bloody hell, I'm wrong! The only surprise is that half the population there haven't left for Australia.

No sympathy for people that have four kids then tell us they are struggling.

Harsh but true. They often expect others to be responsible for their children's future. If they can’t feed, educate and provide a quality life for each of their children then they become burden to society.

Landlords are the real burden on society.

Too much entitlement mentality, and too much influence of those possessing it on the legislature and executive at the top.

USD $5,000,000,000,000 was the US Government stimulus response for 2020-2021. It is all gone now. It caused the inflation. The wave of layoffs coming to the US in Q3 and Q4 will cure inflation. Most prices will stay at their elevated current levels. But they will not rise further. Therefore inflation back below 3%. People will simply not have the ability to pay any more than they are paying now. Interest rate rises so far can only take the froth off the top. The rate cuts will be required to put it back on once the glass is half empty.

When a small 3 bedroom house in Auckland cost over a million and 12 x average wage couples income lowing rates would just cause more pain for most kiwis. I don’t think opening the door to more inflation is a wise move.

That's right, there is no mention in the article about inflation. Which is weird, because it's the number 1 reason why the OCR was raised late last year.

Wow looks like this government are being really successful in not helping first home buyers into the market

Forcing up int rates increases mortgage repayments so the drop in prices is of no use because affordability is being shifted away from the purchase price to the cashflow, go figure?

First home buyers are SO much worse off now than when this government first took office when they promised to "solve the housing crisis" as if we had a crisis back then!

Capital research has no clue, would get more accurate forecast from a tea leaves reader.

So house prices are a mandate now. When will the govt and RBNZ make the announcement?

In other words, it will be business a usual...

It's likely National will be at the helm next year & help bolster the property market back up.

If governments want to wage war on fossil fuels inflations going to be persistent

"Independent global economic researcher Capital Economics is forecasting a 75-point reduction in the OCR in the second half of 2023 as house prices hit the bottom of the RBNZ's 'sustainable' range"

One should be aware and should take it with a pinch of salt whenever one addresses themselvves as Indiependent .....Independent global economic .......

Just like...Tony Alexander - Independent Economist

Definitely at sometime in future, OCR will be dropped as is economy cycle but will it be in 2023 or 2024 or may be 2026, will all depends on future economy condition and inflation.

For now, is going up and not comming down in a hurry..no harm in wishing and trying to motivate for vested agenda.

I didn't think that house prices figured significantly in the CPI/OCR RB control regime. They certainly never gave a toss about it while prices were rising so it seems that they are inconsistently and dishonestly cherry picking what they do if house prices form part of their consideration now.

"Even such a large drop in prices would only restore affordability to its late-2021 level or its pre-GFC peak, which would still be very stretched. (See Chart 2.)"

In my experience with markets, when they turn down from from extremely overvalued levels, that correction doesn't stop at a point that would still be considered "very stretched".

This correction is way overdue, it's not stopping at still stretched levels. It could go on for years.

I agree, markets tend to over correct. Could be back to 2015/16 by the time this settles.

Fear not home sellers. Real Estate Agents, will still do whatever they can, in order to get you more for your home that what it's ever worth.

Correction will be what it will be. Unfortunately probably slow and long and deep.

The RBNZ really has limited control over the OCR has be - whilst I am certain the RBNZ will be under pressure to reduce it in the coming years... they have to reduce inflation for our economy (exporters, food and oil prices..) to work, and if everyone else is raising, so do we.

The probability of more global significant issues stemming from recent events is also greater than most people think - which will put more pressure on inflation. Soros did a great talk on this recently and touched on a couple (but the list is growing as serious geopolitics comes back)

Sold our investment property in Queenstown in Feb'22 ... paid off $1/2m in debt ... balance into a 15% stake in a big 380ha Southland dairy farm equity syndicate. Rather rent to a sharemilker with 1050 cows than 1 financially tapped-out human being for the next few years !!

Why should house prices be part of the reserve banks remit?

They are not. Thank goodness

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.