The following MFAT report provides an update of how trade is being affected in the Middle East for New Zealand exporters. The original is here.

The conflict in the Middle East is the most consequential disruption to energy and petrochemical supply chains in decades. Iranian attacks and threats against commercial shipping, and the US counter blockade of Iranian shipping, have brought tanker movements through the Strait of Hormuz close to a standstill. For New Zealand’s trade with the region, the conflict is causing major disruption for those exporting to or importing from the Gulf.

Early in the conflict there were reports from exporters of cargo being offloaded at unscheduled destinations, leaving exporters to bear the cost of alternative freight forwarding. As the conflict has gone on, these reports have been replaced with concerns of rising input costs, and transport related charges such as freight, fuel, and insurance. In addition, global trade logistics remain challenging, with instances of longer transit times, and congestion at some major shipping hubs like Singapore, as supply chains adjust to changing conditions.

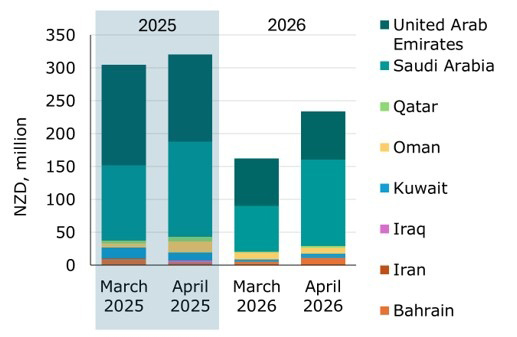

According to StatsNZ’s goods trade data for March and April, exports to the Gulf region have clearly experienced disruption. Exports fell around 37 percent to $397 million compared to the same two months last year with the fall in exports occurring across Gulf markets (Figure 1). Despite the hit to New Zealand’s exports to the Middle East, the region represents a fraction of exports that head to our three largest export markets of China, the US, and Australia.

Figure 1: Export revenue to main Middle Eastern trade partners (March & April 2025 & 2026)

Source: StatsNZ

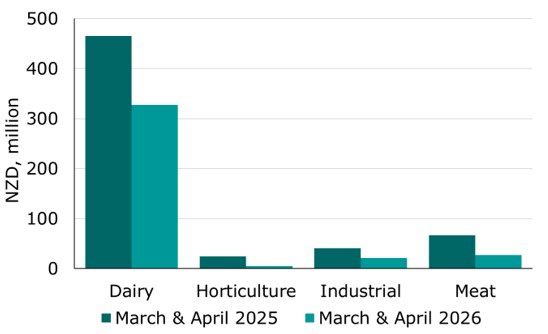

All major exports to the Middle East have decreased since the start of the conflict compared to the same period last year. The largest falls were felt by primary sector exporters, including dairy and meat exports, which fell by $138 million (30 percent) and $40 million (59 percent) respectively in March and April 2026 compared to the same months a year earlier (Figure 2). Other sectors also saw sizeable falls, with horticulture exports down $19 million (79 percent), industrial exports down $20 million (48 percent), and forestry exports down $7 million (84 percent) over the same period.

Figure 2: Export revenue to Middle East by industry (March & April 2025 & 2026)

Source: StatsNZ

Exporters have had to pivot quickly in the face of disruption

In response to the disruption caused by the conflict, exporters trading into the Gulf have been forced to adapt. In some cases, consignments were redirected elsewhere or exporters used land-bridges established in Oman and Saudi Arabia to reach customers in Gulf countries. Oman appears to have been used as a safe point of entry into the region in March, particularly for dairy products. While exports of dairy products into Oman ($10 million) were more than double the value recorded in March 2025, it did not offset declines elsewhere in the Middle East. However, given the increased cost and complexity of exporting to the Middle East at present, there is also likely to have been diversion of trade outside the Gulf region.

The conflict is also disrupting imports from the Middle East that New Zealand firms need

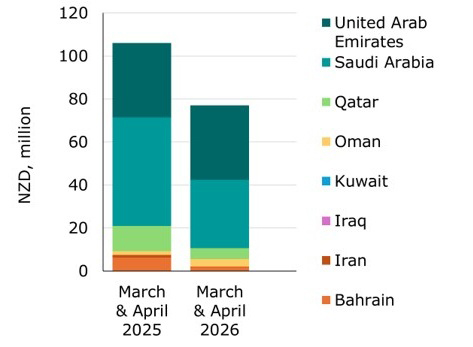

Since the conflict began in late February, imports from the Gulf region have also fallen sharply compared to a year ago. At $77 million (Figure 3), imports were 27 percent lower over March and April, and contrasts to a period of very strong growth in imports experienced in 2025. As a key input into primary production, New Zealand sources over a fifth of its imported fertiliser from the Middle East. Imports of fertiliser from the region fell 27 percent to $33 million compared to the same period last year. For now, domestic suppliers report they are well stocked and have access to imports through all of 2026. However, the disruption to supply chains have come at a cost. Global prices of fertilizer have increased significantly since the onset of the conflict, with urea prices increasing 40-60 percent above pre-crisis levels.

Figure 3: Value of imports from main Middle Eastern trade partners (March & April 2025 & 2026)

Source: StatsNZ

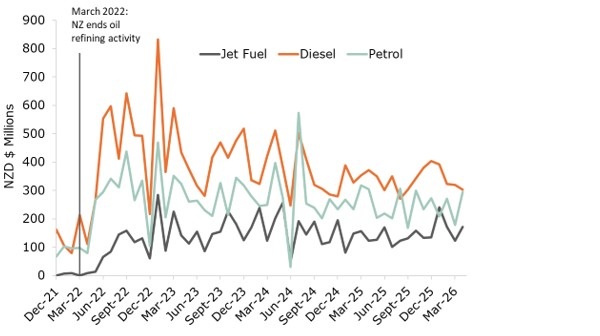

The impact on New Zealand’s trade and the economy goes beyond our direct trade with the Middle East. A major import that is highly exposed, and used extensively in the economy, is fuel. While we no longer directly import oil from the Middle East for refining, Asian refineries who supply the vast majority of New Zealand’s petrol, diesel, and aviation fuel sourced most of their crude oil from the Gulf prior to the Iran conflict.

The value of fuel imported into the country from global refiners was 21 percent ($345 million) lower than March and April last year, driven by lower imported volumes over the period. Fuel imports are highly volatile month to month (see Figure 4) due to several factors, including changeable shipping schedules. The volumes imported of jet fuel, diesel and petrol since the conflict began have remained well within the usual ranges experienced over the course of a typical year. We would expect to see the cost of refined fuel imports increase in future months as higher contracted prices filter through in upcoming trade data.

Similarly, the tightness in global supply chains for many petrochemical derivative products, such as plastics and synthetic resins, has yet to flow through to the trade data. Most plastics product imports reported since the start of the conflict were at levels consistent with the previous year.

Figure 4: Fuel imports from major Asian suppliers by main fuel type (December 2021 to April 2026)

Source: StatsNZ

Since the start of the conflict, overall trade activity has continued to grow strongly

Despite the impact of the conflict New Zealand’s total trade activity continues apace. New Zealand’s $16.3 billion in total goods exports over March and April was 8.0 percent higher than the same period last year. The value of goods imports at $14 billion was 6.4 percent up over March and April on last year. As a result, New Zealand recorded a hefty $2.4 billion trade surplus over the two-month period. New Zealand tends to record a goods trade surplus in late summer and autumn, coinciding with the main harvest period for many primary sector exports and the Christmas related import surge being in the rearview mirror.

The trends that were supporting export growth during 2025 looked to have continued into 2026. Generally favourable on-farm conditions and high global commodity prices that have supported New Zealand’s export success over the past year, look to have underpinned New Zealand’s overall merchandise export performance in both March and April. For instance, beef exports surged in March and April to $1.2bn which was 33 percent up on the same period in 2025, supported by elevated global beef prices because of supply constraints being experienced in the US. Exports of another major primary sector commodity, dairy, have held their ground since the start of the conflict up 2.1 percent up on a year earlier.

The supply disruptions caused by the Iran conflict gave some of New Zealand’s export categories a boost in March and April. Higher global prices for crude oil look to have contributed to an almost fivefold increase in New Zealand’s oil exports to $150 million in April. Oil from the Taranaki basin is entirely exported given its grade and the fact that New Zealand no longer refines crude oil. Another commodity facing global supply constraints and high prices is aluminium, which recorded a 38 percent jump in exports over March and April on last year to almost $400 million.

However, the fallout of the conflict is weighing on the minds of New Zealand firms and households...

The impact of the Iran conflict, including petrochemical supply chain disruption and the jump in fuel prices in New Zealand, is now starting to show up in domestic economic data. Readings from recent business and consumer confidence surveys have revealed a fall in general economic sentiment, and in spending, hiring, and investing intentions.

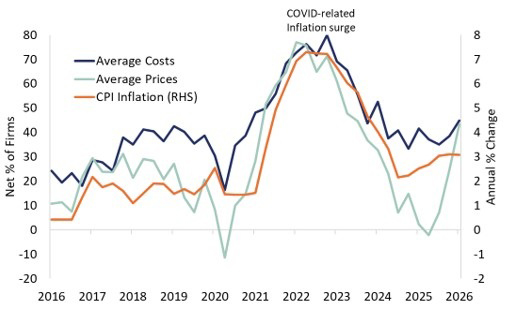

NZIER’s business confidence survey for the March quarter reflected changes in sentiment in the early stages of the conflict. Headline business confidence fell sharply with a net 1 percent of firms surveyed expecting improving economic conditions, down from a net 39 percent at the end of 2025. As would be expected from a major supply-side shock, firms’ responses to questions related to input costs indicated that future costs are expected to rise. But it was firms’ pricing intentions that posted a sizable increase. A net 43 percent of firms intended to raise prices in the coming quarter, well above the survey’s long-run average of 31 percent, and providing more evidence that inflation is set to rise in the coming quarter (Figure 5).

Figure 5: Firms’ cost expectations, pricing intentions, and CPI inflation

Sources: NZIER, StatsNZ

Similarly, the ANZ bank’s latest monthly business sentiment survey for April showed both general business conditions and firms’ outlook for their own activity deteriorated. A net 19.6 percent of firms expect to see an increase in their own activity over the coming year, a fall from 39.3 percent in March (and back to levels seen in early 2024). The retail sector signalled the fastest slowdown in activity compared to other sectors in April. The fragile ceasefire in the Middle East has held so far, easing some pressure at the fuel pump.

Regardless, consumers are feeling gloomier about the impact of the crisis on the cost of living. In response to fuel prices, consumers redirected spending away from discretionary and durables goods to meet rising essential transport costs. According to ANZ’s consumer confidence survey, when asked in April if now was a good time to purchase a major household item, a net 25 percent disagreed – the lowest reading since September 2024.

…translating into a slowdown in spending

Weaker consumer confidence is revealing itself as cautious spending behaviour by households, according to high frequency data. The value of electronic card transactions across New Zealand fell $160 million or 1.6 percent (seasonally adjusted) in April. The fall in spending in April more than offset the jump in transactions in March when households were fuelling up during the initial month of the conflict. The pullback in spending was broad based, with the value of transactions at retail outlets falling $89 million, or 1.3 percent in April. Spending on fuel was 2 percent down in April, at a time when fuel prices rose around 13 percent and diesel prices jumped 37 percent, suggesting that volume of fuel purchased fell significantly.

There is ongoing uncertainty, but growth forecasts are down

There remains significant uncertainty surrounding how the Iran conflict may evolve from here; and subsequently, how the disruption caused to global supply chains will transmit through to the New Zealand economy. Although, even if normal levels of shipping begin transiting the Strait of Hormuz in the near term, disruptions are expected to continue for months to come.

The shock of surging fuel prices and rising input costs has seen business and consumer sentiment fall, and dampened confidence is starting to be reflected in spending data. The IMF has recently revised down its global economic growth forecasts for 2026 from 3.4 percent to 3.1 percent, noting that an extended disruption to trade through the Strait of Hormuz would present further downside risks to this forecast. In their recent Budget forecasts, the Treasury revised down their forecast of New Zealand’s economic growth for the year to June 2026 by half a percent to 1.2 percent, as the crisis pushes out the economic recovery that had been gathering momentum at the start of 2026.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.