This article first appeared in Russell Investments' Communiqué. It is reposted here with permission.

The thought is that if interest rates are rising, portfolios should have a materially lower allocation to bonds, or that cash is a better alternative.

Yet investors should look beyond short-term movements and consider the longer-term rationale for having fixed income within a portfolio.

Further, the entire question regarding the impact of interest rates should be answered in the broader context of ensuring that fixed income portfolios achieve an appropriate balance between the range of premiums available to investors.

Why do investors hold fixed income securities in the first place?

The starting point for any discussion should be to ask: “Why are bonds in the portfolio in the first place?” While current bond yields may not be particularly impressive when compared to those in the past, the underlying rationale is that bonds help diversify a portfolio. Within a multi-asset portfolio, bonds are generally viewed as defensive assets due to their lower volatility. Rephrasing the rationale slightly, bonds aren’t generally viewed as return boosters but rather seen as volatility dampeners. Bonds can and will fluctuate in value, but they are nowhere near as volatile as some other asset classes, such as equities. This means that adding bonds to a portfolio is analogous to adding cool water to a hot bath to make it more comfortable.

Even very aggressive investors can benefit from keeping part of their investments in bonds, given the diversification they bring to a portfolio. As many investors face the perennial question of ’bonds versus stocks‘ within a multi-asset portfolio, the reality is that nothing has changed when it comes to reducing volatility. A portfolio containing global bonds remains an investor’s best defence against an uncertain future investment environment.

If the aim is lower volatility, why not add cash?

If an investor wants to reduce volatility, why not simply allocate more to cash and avoid the impact of higher interest rates? It’s true that adding cash to an equity portfolio will also lower volatility, but perversely, it may not reduce risk as much as adding bonds.

Even though cash has lower absolute volatility, it may not be as good a diversifier as bonds in a portfolio that contains equities. This is because bonds tend to have a negative correlation with equities during times of market turmoil.1 When stocks plummet and the economy is in recession, interest rates typically fall, which drives up bond prices. That boost can offset at least some of the losses investors experience on the equity side of their portfolios.

By contrast, holding cash in a portfolio during a stock market correction offers a much smaller benefit due to the lack of interest rate duration. An investor’s cash holdings will never spike in value and offset losses on the equity side. Further, cash holdings are likely to

disappoint if central banks react to a stock market correction by cutting rates. This would reduce cash yields and illustrates how cash and bond returns can be negatively correlated in some circumstances, such as a stock market correction. This possible negative correlation between bonds and cash means investors shouldn’t think in terms of one or the other. Instead, they should consider holding both.2

If the strategic rationale for holding bonds is unchanged, should an investor always hold the same allocation within a multi-asset portfolio? Or in the context of today’s environment, should investors tilt away from bonds if they expect interest rates to rise? Such a tilt may make sense, but investors should keep the following points in mind.

It isn't whether interest rates rise that matters, but whether they rise by more than the market expects

To decide whether it makes sense to tactically tilt away from global bonds, investors who believe that yields ’can only go one way from here’ may need to ask whether their view reflects any special knowledge? In other words, do they know something the market

doesn’t?

The reason is that longer-dated bonds are simply the average of the market’s expectation of future shorter-dated bond rates plus a term premium. This arises because, in an efficient market, changes in bond prices are typically driven by changes in the market’s consensus view of future interest rates (which in turn takes account of expectations concerning how short-term rates will evolve). These expectations are priced in to bond prices in much the same way that a company’s future earnings are built into stock prices. The result is that a 10-year bond yield is an estimate of what the market expects the 1-year bond rate to be over the next 10 years.3

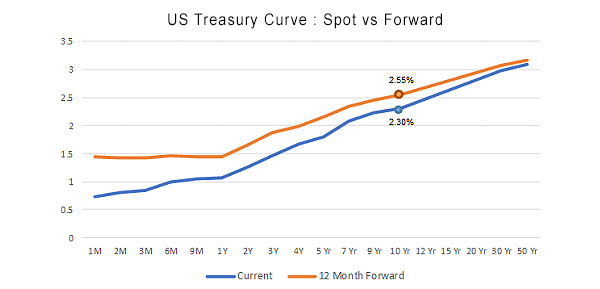

The implication is that if the market and the individual investor expect interest rates to follow the same path, then the individual investor’s opinion is already built into bond prices. To illustrate, the chart on page 13 shows the spot US yield curve and the 12-month forward curve4. While the spot 10-year bond rate is 2.30%, the 12-month forward 10-year bond rate is 2.55%. Here, the view isn’t that rates will rise. Rather, it is that the 10-year bond rate will rise materially higher than 2.55% (or rise by more than 25 basis points) over the next year. When considering and incorporating a directional view on rates, the direction of the view is less important than the spot expectation versus what the market has already priced in.

Achieving diversity of premiums within fixed income portfolios

Just as bonds are one exposure within an investor’s portfolio, it is important to remember that interest rate risk may be only one exposure within an investor’s bond portfolio. This is best illustrated by considering that for most bond portfolios the main drivers of returns are not only interest rates but also credit spreads. These tend to be negatively correlated over the cycle. Accordingly, simply focusing on the outlook for interest rates may risk overlooking other interactions within a bond portfolio. To highlight an extreme example, assume that an investor has a bond portfolio that is 100% longer-duration global credit. Within this portfolio, the interest rate duration and credit spread duration can together act as a natural hedge (i.e., they tend to be negatively correlated over the cycle). Now the investor is concerned about the risk of rates rising so decides to hedge out all interest rate risk. Perversely, by eliminating the offsetting impact of interest rates and credit spreads, the investor may actually be increasing the risk of the bond portfolio.5

The interaction between interest rates and credit spreads is an example of the diversifying impact of combining different premiums. More generally, investors should ensure that a fixed income portfolio, subject to investor constraints, strikes a balance between exposures to the different premiums available. The key premiums available to investors are listed below.

Term premium

This is simply the premium associated with the expectation that ’normal’ yield curves are positively sloped (i.e., investors receive a higher return for assuming longer-duration securities). However, term premiums are not linear, so the optimal point for accessing such premiums can be at the shorter end of the curve where roll down assists investor returns.

Credit premium

This is simply where securities that exhibit higher levels of credit risk will generate higher returns than those of comparably lower credit risk. Normally, such a premium is quantified as the return earned over government bonds (i.e., government bonds are viewed as being risk-free).

Illiquidity premium

A bond illiquidity premium is the compensation an investor seeks for investing in less liquid debt securities. Credit and illiquidity premiums are often closely connected, and in practice can be difficult to separate.

Real yield premium

This relates to the tendency for bonds issued by sovereign countries with higher real yields to have a higher likelihood of outperforming those with low real yields. There are three drivers for this outperformance: (a) higher carry associated with the real yield premium;

(b) potential for longer-term real rate convergence; and (c) a steeper yield curve associated with higher inflation volatility.

Currency premium

Russell Investments believes that carry, valuation and momentum strategies are the three dominant ways investors can capture returns in currency markets.

Proactive management to help navigate this environment

Ensuring that a bond portfolio incorporates a diversified range of premiums helps avoid excessive reliance on any single source of return enhancement. Just as importantly, it may assist in proactively managing exposures over the cycle in the event that the investor wants to tilt exposures. For example, an investor may be concerned about the outlook for interest rates and want to reduce the exposure to those rates. As has been highlighted, such an action may have flow-on impacts to other risks within the portfolio. By having a more diversified range of premiums within a portfolio, the investor may be in a better position to minimise any negative impact from reducing their exposure to interest rate risk. In fact, the increased diversification of premiums may be a more efficient means of managing interest rate risk than simply trying to tactically tilt at different points in the cycle. Russell Investments also believes skilful active management can add value over passive management, and that it has a demonstrated ability to identify such capable managers.

Summing up

It’s always important to consider asset classes in context, rather than in isolation. On their own, bonds may appear unattractive today if an investor’s goal is simply to maximise returns from that part of a multi-asset portfolio in the short-term.

However, if an investor is in it for the long-haul, they should never forget that bonds are still the asset class that puts the 'balance' in a balanced portfolio.

This does not mean that all bond portfolios are created equal. Investors should ensure they maximise the range of premiums within their portfolios to reduce their reliance on any particular premium when building value in their bond portfolios. In our view, this is key because the diversification of bond premiums is likely to become more important as volatility rises across the global investment market.

Notes:

1. This relationship explicitly assumes that the bond portfolio has a low level of credit risk incorporated within it. To the extent that there is credit risk within the bond portfolio, the greater the credit exposure, the more the bond portfolio will tend to behave like the equity markets it is trying to diversify. Investors need to keep this in mind when determining the appropriate mix of bonds and equities within a portfolio.

2. This argument still holds even if cash rates are zero, provided there is a positive yield curve, as yield curves can still become inverted. However, the argument becomes less persuasive where cash rates are zero and the yield curve is already highly inverted (i.e., nominal longer-date bond rates are negative). The rationale for holding longer-date bonds becomes much weaker in this scenario as there is a floor under the zero cash rate and the holding of longer-date bonds involves a negative carry versus cash.

3. Note that the estimate will be biased in that the market’s expectations should normally incorporate a positive term premium.

4. The forward curve is the current estimate of the market's expectation of 10-year bond rates 12 months from now.

5. This historical interaction between interest rates and credit spreads also highlights the importance of ensuring portfolios are appropriately constructed to be consistent with the investor’s desired objectives. For example, duration and credit within a fixed income portfolio will assist in diversifying each other as interest rate duration and credit spread duration tend to offset each other during periods of market stress (i.e., major risk-off events). However, this diversification benefit can only be used once. Put another way, the more the interest rate duration within a fixed income portfolio is needed to offset credit risk within the fixed income portfolio, the less is left to offset the investor’s equity exposure. Accordingly, if an investor is using interest rate duration within a fixed income allocation to protect against adverse equity moves, then it makes sense to also use more conservative credit exposures, if any credit exposure at all, to provide the maximum level of diversification with respect to the investor’s equity holdings. Conversely, if an investor is using higher-risk credit strategies within their fixed income portfolio, they may want to reconsider their allocation to equities given the potential overlap in exposures.

Clive Smith is a senior portfolio manager for Russell Investments based in the Sydney. This article first appeared in Russell Investments' Communiqué. It is reposted here with permission.

7 Comments

You want to hold cash as an asset class .............. stick with plain old savings in the Bank .

Anything else is about as safe as swimming off Coffin Bay in Australia .........where you will likely get eaten

Given the low yields on new Bond issuances and the high prices on older higher yield bonds , and the risks of capital losses , un-needed haircuts , defaults , and all manner risks lurking , you should just stay out of this investment class for now .

If you think my assertion is wrong , just ask Warren Buffet why he is sitting on a cash pile , and NOT putting it into stocks and Bonds

Be interesting to see if anyone on this site is a Modern Portfolio Theory guru - and what their thoughts are on its robutsness in current market conditions with possible end of stock market and bond market bulls simultaneously - and how this might effect asset allocation..(and mix in the influence of QE).

Going back through history - have we ever had a 30+ year bond bull co-exist with a significant stock market bull? Would appear there is little room for interest rate cuts in the future so do bonds and stocks really have a 'negative correlation' as Clive puts it in this situation?

I partly use MPT. If I stuck by the rules I'd own some bonds, however they make no rational sense whatsoever. The yields are too low and at best only maintain the value of the money. Dividends, while unreliable long term, still outperform bonds.

Bond prices will keep falling. It's good for yield but if I was balancing a portfolio with bonds I'd have to keep buying more and buying into what I think will be a long term falling value doesn't make any sense. The large central banks have distorted and broken the markets.

I think picking the balance of shares to bonds needs to be done carefully but MPT doesn't need to be abandoned.

Thanks Dictator - funny that you hear Dalio saying that you're going to feel foolish for holding cash in the near future, but then at the same time you hear the amount of cash that the like's of Buffet are holding on the sidelines. One would think that if there is some form of correction/crash in stock markets, there's enough cash on the sidelines to jump in when P/E's and yields look attractive enough? What's surprised me is how quickly the US market has recovered from the correction - it's almost back to it's January high once more...

I always look back to 1987. In the US it took one month to shrug that off. In NZ it took years of pain and a lot of cheap property was bought by those that actually had cash.

The correction is just a minor blip and there's more to come. Big players have exited the risky bets including a lot of junk bonds being dumped (might as well get you money rather than lose it completely). When there's the next big move down there will be more damage. Stop losses will get triggered and margin calls will kick in.

Independent_Observer,

I am no guru of anything.A key insight of MPT related to diversification and while seemingly novel in the early 50s,it is standard advice now.I have been a stockmarket investor for many years,initially in the UK and since 2004,in NZ. Throughout,my focus has been entirely on dividends-sustainable and growing dividends. I hold a portfolio of some 36 equities,a small and decreasing number of bonds and an increasing pile of cash.

At the age of 72,my aim is conservation of capital,with a gradually increasing income,largely from dividends and some from rent.

I am uncomfortable with the valuation of many equities now and would welcome a significant correction.

Interested in peoples thoughts on inflation indexed bonds. I'm assuming they may be the best bet when it comes to buying bonds in a rising rate environment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.