This article is a re-post from yieldreport.com.au and is here with permission.

Any bond issued by any company has some chance of default. After all, who knows what may happen to a company’s fortunes in the next year or five years or decade.

However, some bonds are thought to be riskier than others, possibly as a result of the issuer of the bonds or the structure (rules) of the bonds.

“High yield” bonds, once referred to as “junk” bonds, are simply bonds which are not rated as investment-grade by ratings agencies. That is, they have a credit rating of BB+ or lower or no credit rating at all. As such, they are perceived to have a higher probability of default than bonds with investment-grade ratings.

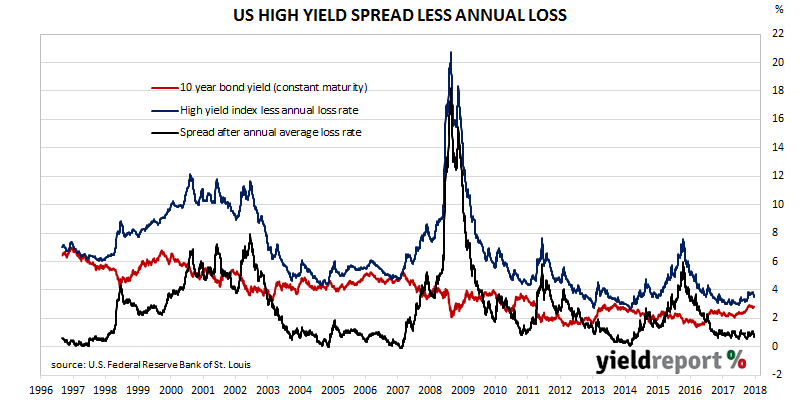

Currently, the spread between the Bank of America Merrill Lynch US High Yield Master II Index (used by the Federal Reserve as a measure of sub-investment grade yield) and U.S. 10 year bonds is around 3.3%. 3.3% is a useful amount per year but as John Coumarianos from Institutional Imperative pointed out, this is not the full story. “The truth is that it’s much riskier than it seems from doing this simple yield, or yield-spread, analysis. That’s because the annual loss rate for junk bonds over the past 35 years has been around 2.5%.”

What he is referring to is the annual loss high yield investors have experienced in the past, assuming they held diversified portfolios of high yield bonds for lengthy periods. Taking into account annual default rates on high yield bonds average about 4.2% according to Standard & Poor’s research, in conjunction with the fact not all bond defaults result in 100% losses, he calculated the average annual loss works out to be 2.5%.

After adjusting the Bank of America Merrill Lynch US High Yield Master II Index for this amount the spread between it and the 10 year bond yield is around 0.8% per annum. That’s not quite so attractive.

While the Australian market for high yield bonds is nowhere as deep and as developed as the US market, there is a lesson for Australian investors and, indeed, investors anywhere in the world. Some bonds may look better and offer superficially more-attractive yields if investors do not take all factors into account.

This article is a re-post from yieldreport.com.au and is here with permission.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.