By Alison Brook*

New research from McKinsey Global Institute suggests that companies and countries that invest more heavily in intangible assets can unlock significantly higher levels of growth and productivity. Often misunderstood and underestimated, intangible assets are not fully accounted for in national accounts or company balance sheets.

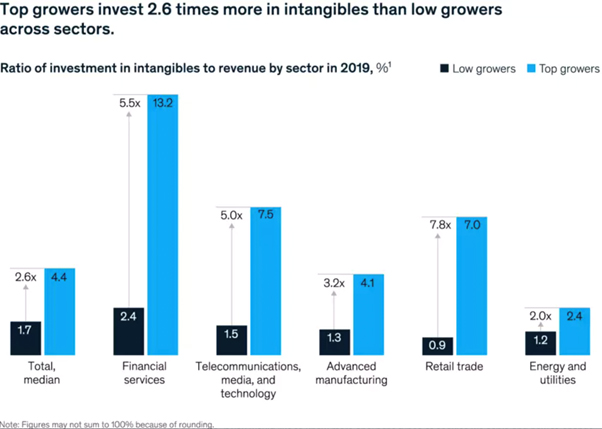

Companies that invest the most in intangible assets are growing faster than their peers. They also tend to be more profitable and have higher valuations. That gap is even greater in sectors like financial services where their competitive advantage is based on knowledge.

Intangible assets include things like human capital, goodwill, brand, software, intellectual property, trademarks, patents and R & D. The switch from investing primarily in tangible assets to intangibles began early in the twenty-first century according to Haskel and Westlake in Capitalism without Capital: The Rise of the Intangible Economy. At that time businesses in major developed economies quietly began to invest more in intangibles than tangibles assets like land, equipment and inventory.

Source: McKinsey & Company

COVID intangibles surge

The Global Intangible Finance Tracker indicates investment in intangibles has grown faster than usual in 2021, increasing by 23 percent since 2019. McKinsey found that by 2019, intangibles accounted for 40 percent of all investments by the US and the largest European countries. But when the pandemic hit in 2020 companies accelerated their investment in digital technologies.

According to McKinsey, not only do the top-performing firms invest more in intangibles and see the competitive advantage of doing so, they also focus on deploying them in their day to day operations. What this means in practice is using data and analytics to make decisions in real time, investing in analytical talent and flexible architecture. These companies were also twice as likely to regard personalisation as core to the customer experience.

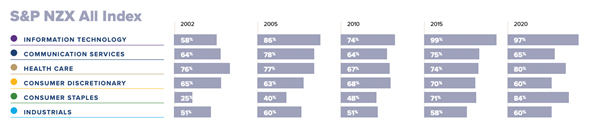

According to the latest EverEdge Intangible Benchmark Index New Zealand, listed companies have also seen a growth in intangibles over the last decade, albeit off a low base. This has been primarily driven by just a few companies like A2 Milk, Meridian Energy, Mercury New Zealand and Xero (before it left the NZX in 2015).

Intangible Assets Index Analysis by Sector 2000 – 2020

Source: EverEdge Intangible Benchmark Index Vol. One 2021

The missing link: labour productivity growth

There also seems to be a strong link between investment in intangibles and productivity growth.

A recent paper by Roth and Sen showed that intangibles investments accounted for 40 percent of labour productivity growth amongst the sample EU countries. There were also big sectoral differences: while R & D investment had been the focus of intangibles investments in the manufacturing sector, for services industries the biggest driver of productivity growth was software, vocational training and organisational capital.

Outdated accounting standards

While intangibles are the primary driver of business value they are rarely recorded accurately according to intangible asset specialist EverEdge Global. Accounting rules were developed at a time when businesses and industries were dominated by physical assets whereas today up to 85 percent of a company’s value may be due to intangible assets.

Unlike an investment in a machine, investing in vocational training for workers is treated as an expense. Similarly, cloud-based software is currently treated as an expense rather than a capital investment. The result is earnings are being artificially deflated and the balance sheet does not really reflect the real value of the company.

Research from Caixabank estimates that half the investment in tangible assets is being ignored by national accounting frameworks. This is leading to serious errors in economic policy at a company and country level. The failure to capture the levels of capital investment being made in intangibles means labour productivity growth rates may be being seriously underestimated in more advanced knowledge economies.

It may also be disincentivizing management and boards from investing in innovative, cloud-based new technology because of the impact it would have on short-term earnings.

In addition, it raises the question about whether the barriers to financing intangibles as capital assets is increasing the productivity gap between firms, particularly for smaller, less well-resourced firms. Recent research from Demmou and Franco seems to suggest this is the case.

Intangible assets now represent a huge slice of the global economy and the pandemic has only accelerated this trend. Ignoring their contribution to the capital base of the firms creates the very real possibility that suboptimal decisions are being made by investors, companies and countries.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission. The New Zealand GDPLive resource can also be accessed here.

5 Comments

Two thoughts here.

- The conventional definition of 'assets' includes the multi-year persistence of their value to the enterprise. This is much harder to establish for an employee who may be poached next week, goodwill that may be trashed when a signature product recipe is changed (poster child, Cadbury), or the cloud goes offline (AWS outage takes Xero out with it).

- Accounting is inherently very conservative. To be otherwise destroys the core concept of comparability across years, jurisdictions, industry sectors. Changing fundamental definitions of accounting will take time, have to be coordinated via international standards, and then have to be implemented in millions of enterprises. And then there's the valuation of said new Assets......

Short version, don't bet the farm on this happening quickly. But it could be useful to run an alternate ledger (or make an alternate categorization of accounts and report using it) based on these changes, if it were deemed important enough to the business to devote the resources to do so.....

Well said waymad.

The Savy investor reworks the Financial Statements anyway

Ironic how, innovation, dynamism, agility, empathy, constant learning and improvement are all key ingredients for a modern successful business, and yet the industry that values these very same businesses displays very few of these qualities.

As generic (or tangible if you will) as the accounting industry is or seems to be, it may we'll be its undoing. AI will see to that.

"Intangible assets now represent a huge slice of the global economy"

Translated:

A huge slice of our 'economy' doesn't actually exist; cannot be cashed-in for anything real.

I read it more as "companies are counting things that don't actually represent their ability to earn cash."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.