Heartland Bank's produced a 12% rise in net profit after tax for the year to June 30, with earnings topping the $60 million mark, (at $60.8 million) which is slightly more than the bank's most recent forecast.

Looking at the year ahead, the bank says it expects after tax earnings for the year ending June 30, 2018 to be in the range of $65 million to $68 million.

"Looking forward, underlying asset growth is expected to continue, with strong Household, Business and Rural volumes projected through execution of Heartland’s strategy, in particular the expansion of customer reach through digital and intermediary channels," Heartland said.

A final dividend for the year of 5.5c a share is being paid.

The bank said the increase in profitability in the 2017 financial year was driven primarily by growth in receivables across all divisions – Household, Business and Rural .

Heartland said achievements for the year, as well as the 12% increase in profit, included:

► Strong growth in receivables of 14%

► Return on equity (ROE) of 11.6%

► Launch of multiple digital platforms

► Implementation of a new core banking system

Formed through the merger of Marac Finance, CBS Canterbury and the Southern Cross Building Society in January 2011, Heartland gained banking registration from the Reserve Bank in December 2012. Under CEO Jeff Greenslade Heartland has targeted niche markets such as reverse mortgages, vehicle lending and livestock finance where bigger banks are not aggressively competing.

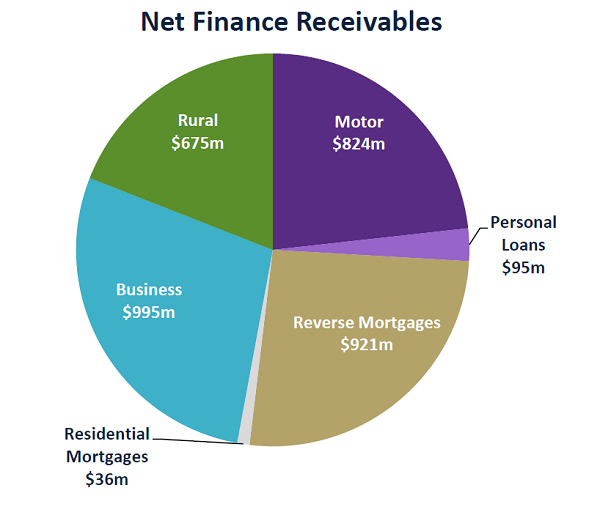

Net finance receivables increased by $447 million (14%) to $3.6 billion during FY2017. Total assets increased by $501.7 million due to the increase in net finance receivables together with an increase in liquid investments.

Heartland said net operating income from the Consumer division (which includes motor vehicle loans, personal loans and lending through the Harmoney platform, in which Heartland has a shareholding) increased $1.9 million (3%) from FY2016 to $57.2 million. Consumer net receivables grew $112 million (14%) to $919.1 million during FY2017.

The bank said the strong growth in net receivables was not reflected in growth in net operating income due to lower earning rates on motor vehicle and personal loans as well as less operating lease income on a smaller lease book.

Strong growth in personal lending was also achieved in FY2017 with net receivables for personal loans and Harmoney increasing by $40.0 million (73%) to $94.8 million.

Net Operating Income was $171.3 million, up $13.7 million (9%) from $157.6 million for FY2016. The increase was primarily attributable to the increased level of receivables.

Heartland’s Net Interest Margin (NIM ) for FY2017 was 4.46% compared with 4.50% for FY2016. The bank said the reduction resulted primarily from changes in the asset mix.

Operating costs were $71.7 million for FY2017, an increase of $1.8 million (2.6%) from FY2016. This increase was due to business growth driving increased staff costs, partially offset by a reduction in one off project and compliance costs.

The overall cost to income ratio was 42% for FY2017 compared with 44% in FY2016.

Impaired asset expense increased by $1.5 million to $15 million for FY2017, up from $13.5 million for FY2016.

Heartland said its new core banking system (Oracle - Flexcube) was implemented in May 2017 at a total project cost of $22 million.

The bank said Flexcube was a modern, modular core banking system which is highly configurable and introduces automation and workflow capabilities.

"Flexcube is a refreshed and contemporary IT architecture that will sustain Heartland’s long-term business objectives. The new core banking system includes an internet portal enabling dealers and intermediaries to originate new business and create customer and account records within Flexcube."

Note offer considered

Separately, Heartland announced that it was considering making an offer of five year, unsecured, unsubordinated, fixed rate notes ("Notes") to institutional and New Zealand retail investors.

If the offer proceeds, it is expected to open in late August 2017.

No money was currently being sought and no Notes can be applied for or acquired until the intended offer opens and the investor receives a copy of the limited disclosure document relating to the offer prepared under New Zealand’s Financial Markets Conduct Act 2013 (“FMCA”). If the offer is made, the offer will be made in accordance with the FMCA. The Notes are expected to be quoted on the NZX Debt Market.

Bank of New Zealand has been appointed the Arranger and Organising Participant, and Bank of New Zealand, Commonwealth Bank of Australia (acting through its New Zealand Branch), Deutsche Craigs Limited and Westpac Banking Corporation (acting through its New Zealand branch) have been appointed as Joint Lead Managers.

2 Comments

" Profitability in the 2017 financial year was driven primarily by growth in receivables" + "Impaired asset expense increased by $1.5 million (+11%) to $15 million" = A drop in lending standards?

It's easy to grow a balance sheet by lending more ( as long as you can borrow to fund that lending) but if Bad and Doubtful Debt increase at a higher rate, then...beware.....

bw that's peanuts?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.