Credit ratings agency Moody's Investors Service says large scale adoption of cryptocurrencies for money transfers could chop about US$15 billion annually from global remittance fees.

That's one of the findings in a new Moody's report titled: "Fintech - Global: Bank of the Future: Innovative incumbents will thrive; laggards will be disrupted".

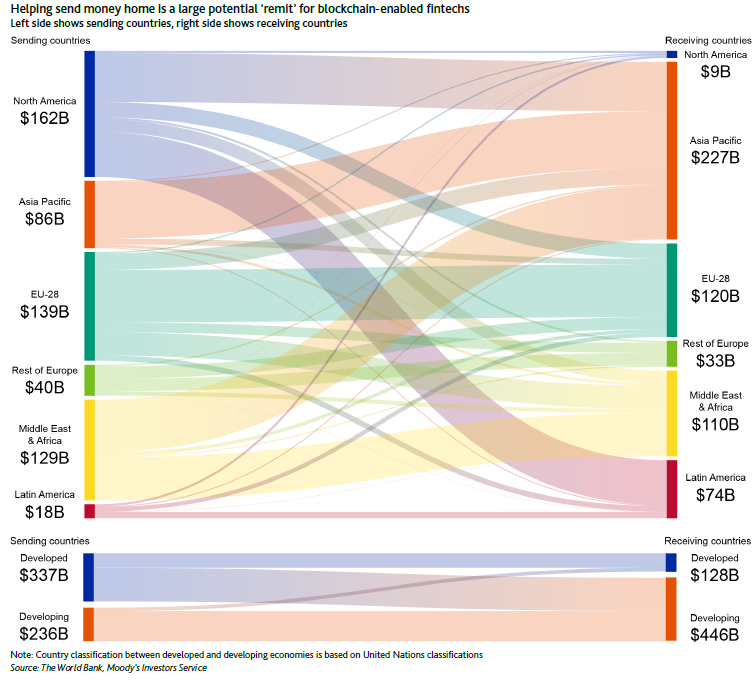

The report says that in 2016, the total value of global remittances, although a small portion of global payments, reached US$575 billion, 70% of which consisted of transfers by international migrants in developed countries home to developing countries.

"The global remittances business is mainly led by money transfer operators, to which correspondent banks have been limiting their exposure because of the risk of money laundering and financial crime.

"In 2017, the average cost worldwide for sending a US$200 international transfer was 7.2%, with costs generally higher in developing countries."

The report says that given banks’ general aversion to the remittances business, fintech companies may be able to gain market share, particularly in regions where fees are highest.

"There are sizable savings to be gained through peer-to-peer alternatives that leverage cryptocurrency technology.

"Assuming half of all remittances transition to a cheaper channel offered by a start-up, at an average of 2% in transaction fees (a conservative estimate of average cost of a cryptocurrency transaction, absent extreme volatility periods), the annual savings would be around $15 billion."

The report says that the blockchain technology used for cryptocurrencies is still untested at large transaction volumes, where authorisations need to be processed in fractions of a second.

"But if the technology proves to be a practical solution for payments, incumbents are likely to adopt it. Indeed, a global consortium of banks has partnered with blockchain start-up Ripple to develop enterprise blockchain solutions for international payments. Ripple has created a payment protocol and exchange network with a much faster consensus method than the Bitcoin blockchain, and introduced its own cryptocurrency, the XRP."

Talking of blockchain, or distributed ledger technology (DLT), more generally and the broader application of it, the report says that tangible gains from it are likely a long way off for the capital markets.

"Given that the greatest benefits of DLT are realised in contexts that include a number of parties, moving the technology from proof of concept to an ingrained part of long-standing processes and markets will require a significant commitment from a number of participants.

'Potential to improve efficiency'

"But even though DLT is still in the early stages of development, it has the potential to improve efficiency throughout the life-cycle of various securities, including 1) issuance, ownership and trading; 2) post-trade clearing and settlement; and 3) custody and securities servicing.

"A shared synchronized DLT could eliminate the need to reconcile various independent platforms and improve process workflows, with a clear view of asset and process ownership throughout the chain, as well as leverage smart contract technology to eliminate some manual processes."

Speaking more generally on the financial services industry as a whole, the report says the widening application of digital innovations in financial services is placing a premium on efficiency and opening up competition that will continue to drive disruption across banking business segments, including payments, lending, capital markets and wealth management.

"How incumbent institutions and new entrants harness these innovations will define the bank of the future.

"In the coming years, we expect the disruption and evolution of business models, financial infrastructure, product pricing models and profit margins to open a split in global banking leadership.

"Incumbent banks that aggressively pursue agile digital strategies will defend their core franchises, broaden their customer bases and improve efficiency, supporting their creditworthiness. Laggards will face increased customer attrition, reduced pricing power and uncompetitive cost structures."

In going into more detail on that point, the report says that "agile" incumbent banks that consistently assert digital leadership will thrive and prosper.

"These banks will pursue transformative digital strategies that drive: relentless investment in data analytics; the upgrade of core systems and cyber defenses; ongoing innovation in product design, distribution and strategic marketing; and deliberate choices to cede ground to competitors in select markets where necessary. We expect successful incumbents to achieve these ends both on their own and via acquisitions and partnerships with fintechs, ranging from niche new entrants to big tech firms."

Laggard banks 'will be disrupted'

On the other hand "laggard banks" that lack the vision or resources to develop competitive digital strategies will be disrupted.

"These firms will find themselves unable to deliver the quality of service or price competitiveness necessary to maintain their market share and revenue streams. They will lose ground as more nimble peers poach clients, as new fintech entrants gain a foothold in low-efficiency banking service niches, and as big tech firms and digital challenger banks expand their suite of banking alternatives across markets. As the business activity and profit margins of laggard banks shrink, they may increase risk taking, consolidate business lines or, ultimately, be subsumed in larger or stronger firms."

The report says that successful incumbent banks will have to continue investing heavily in IT systems to support efficient digital solutions.

"Current banking platforms are often based on a patchwork of outdated IT systems stemming from past acquisitions and expansions, preventing many incumbents from taking full advantage of their data. Challenger banks and fintech firms are not encumbered by legacy systems, and can more quickly implement technological changes.

"Modernising or replacing legacy infrastructure is not a small task but it will be required to support digital offerings, improve processes, gain cost efficiencies and better leverage banks’ existing big data. Banks that do not allocate sufficient resources to IT upgrades are more likely to be displaced as timely, agile startups fill under-served market niches."

'Joining forces'

The report says that in some situations, banks will join forces to innovate and maintain their central roles. In markets most threatened by non-bank competitors, there could be greater collaboration between banks to keep new entrants at bay.

"One recent example is the Nordic mobile payment platforms, Vipps and Swish, which are shared digital ecosystems underpinned by bank-driven innovation and collaboration among multiple Nordic banks to stave off fintech entrants and overseas competitors. Banks will also work with fintech firms to create new infrastructure solutions. For example, in 2016 the UK challenger bank, Virgin Money, formed a partnership with 10x Future Technologies to develop the bank’s digital banking platform.

"Beyond partnerships, some larger banks with more resources are likely to invest in fintech firms to help develop promising solutions. For example, Barclays Bank has an incubator platform, Rise, to provide resources to a number of fintech firms. Incubators offer banks a way to establish relationships with fintech firms at an early stage, identify those firms with most potential, test their solutions, and invest when they deem appropriate."

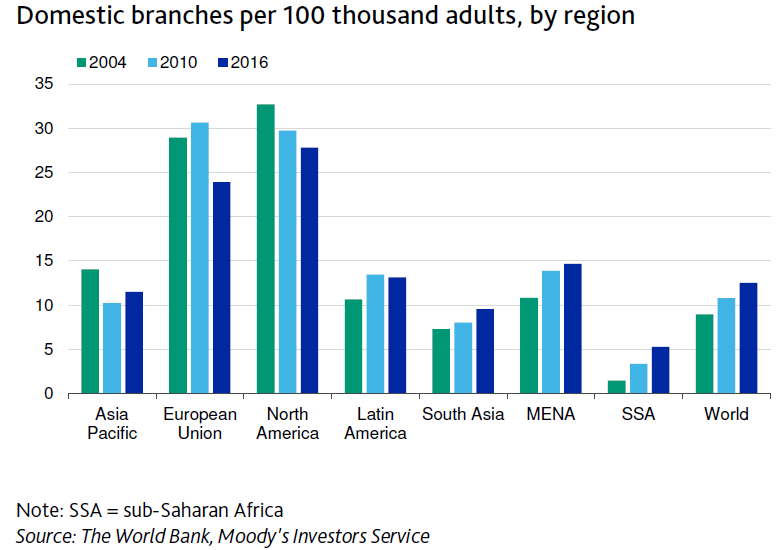

In terms of branch networks, the report says the bank of the future will have a smaller physical footprint as digital solutions help prune branches.

"Reduced demand for traditional branch services is a logical extension of the increasingly mobile financial ecosystem, but the pace of branch closures will vary by region and reflect the income level and digital literacy of local consumers.

In North America and Europe, customer demand for branches will continue to decline over the next decade, giving banks an opportunity to drive down costs by reducing physical footprints and offering more efficient alternative platforms, the report says.

"In some countries where consumers have historically had limited access to financial services, on the other hand, there will be a balance between a measured ‘catch-up’ in bricks-and-mortar branch numbers and the ‘leapfrogging’ of traditional branches to attract new customers via digital offerings. Branches will increase, but likely stay materially lower than peak levels in systems that developed earlier."

Tipping the balance in Brazil

The report says Brazil is an example of where the balance has tipped toward digital platforms following a period of bricks-and-mortar expansion.

The largest banks in Brazil – Banco do Brasil, Itau Unibanco, Banco Bradesco and Banco Santander (Brasil) – have accelerated digitization, including through platforms that offer a variety of open banking services.

"All four banks have mobile-based payment platforms that allow users to open a digital deposit account. Under this strategy, the number of traditional bank branches in Brazil has sharply declined by around one third between 2013 and 2016, and now more than 75% of banking transactions are handled on the internet and through mobile apps."

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

12 Comments

Remittance costs are high because they are government regulated monopolies. PayPal was kicked out of India in 2010 until they started applying the remittance rules.

PayPal has always been a bit of a fair-weather friend with it's policies & application of them.

There are a lot of people who confuse blockchain & distributed development with cryptocurrencies. The difference in the technology principles and one form of implementation. The lesson is to learn to separate the two. Blockchain *might* benefit companies in certain use cases & with certain tech but not cryptocurrencies unless they were in the business of selling financial speculation with poor regulation, i.e. good for exchanges as another source of income through customer fees. "Laggard banks 'will be disrupted'" is a comment bereft of any understanding of the tech used in banks today and existing technical projects they have been working on the past decade (and yes blockchain tech has already been kicking around more than a couple of decades). However the deployments with banks take years and namely because losing hundreds of millions to billions permanently due to a single dev basic update failure is not good for business. Moody's report is very clear on one thing; they have been sufficiently blind to technological shifts for years and missed so much. But then again this report is trying to ride a wave that has already passed years before.

David I am so disappointed, this article (a summary of the Moody report), is cut and pasted directly from another source word for word. Have you really nothing to add? No review of the report to offer? You might as well post which source you got the summary or a link to the report source, (yes both might be paywalled but there is a free recording available which can be linked to and "Moody's: Innovative and agile leaders will harness technology to shape the bank of the future" https://www.moodys.com/research/Moodys-Innovative-and-agile-leaders-wil… which is a better to the point summary of the report). [FYI there is another site which has copied a portion, added comments and then linked back to your version which is good for your traffic].

Even a comparison ref back to the other report from PWC "FinTech 2.0

Beyond blurred lines: Have Financial Services

Institutions misread the innovation landscape?" would be interesting as the local shifts apply to a NZ audience. https://www.interest.co.nz/sites/default/files/embedded_images/New%20Ze…

Or even comparisons to Moody's: "Fintech to drive transformation rather than disruption for banks" with report link referenced "Financial Institutions - Global: Fintech Transforms Competitive Landscape, but Unlikely to Displace Banks' Central Role" https://www.moodys.com/research/Moodys-Fintech-to-drive-transformation-… But then that was back in a time when blockchain tech was old news, 2016. Heck many institutions already had tech R&D teams in the area back then. Looking at it the new Moody report really does look like it is trying to recapture the moment from a year ago or more.

Thank you for your comment, but I must take issue. This was not sourced from elsewhere. It was sourced directly from the report, which I have a copy of, and therefore quotes directly from the report. I did not believe I had the right to embed the report with the article, so, I did not. I picked the items from the report I believed would be of greatest interest to our readership. I do NOT EVER take material from other sources - at least not without due attribution. You are perfectly at liberty to be critical of the angle I have taken to the story, but you are quite incorrect in the assumption that the article as such has been 'lifted' from elsewhere. If I wished to comment on the report, I would do that in a separate article.

David this is a classic troll attack. Ignore .

Really, I have a valid concern, and at least David answered it instead of being arrogant and dismissive about something you obviously have no idea about. I found copies of the article word for word from other sites, (with a couple not linking back to sources etc), yet outside the quotes there was little added in review. Perhaps Andrew you are instead the troll, trying to insult others without any relation to the article in question. Lord knows there may be many political trolls on sites, and while I would never stoop so low they seem to be right at your level.

But he put his reputation on the line, he posted under his own name, he tried to inform, you tried to shoot him down.

Someones saving is eroding anothers profit margin.

Thank you David, I doubt there would be much in it in going after the other sites on the basis of copyright, especially in relation to an article reporting a report. But I wonder if you keep the sort of link SEO & sharing stats to ascertain the distribution of interest's articles. Particularly the more investigative ones, certainly the views would be interesting (I know you put out most commented topics information around New Year).

So why should these fintech companies using cryptocurrencies be immune from the sort of regulation (and thus cost) that governments think are needed for banks ? Whether that be for AML or simply to stop gouging or to facilitate tax gathering, changing the way that finance is transacted will not change the underlying behaviours of operators whatever they are called. There is no magic to disrupters - they aren't "good" just because they are. Already there is a failure to recognise the fees they extract from users - using cryptocurrencies is not a free ride. It also is ironic that the banks are getting out services (ATMs, the NZ credit card payment system (can't recall name) that is currently for sale etc. Once out of bank hands it will no longer be possible for consumer lobby groups to allege bank gouging cos the public and the banks will merely be paying (more in my view) for the same service from a "third party" which miraculously makes it ok. Simply adding a "disruptor" to the mix is no guarantee of improvement. Disrupt away but let's not get 20 years down the road and find we simply have a new unregulated monopoly.

Sod this cryto currency hype. It is a flash in the pan.

All B/S.

Stop the limits on people using Govt issued legal tender cash.

And then all these man in the middle types, clipping the ticket, at every stage they can, can go jump in the ocean.

I believe you are absolutely right moa man.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.