Insurer Tower says it is expanding its risk-based pricing model for customers' insurance premiums to include landslide and coastal hazards, with advanced selection for landslide risks "already in place" across New Zealand.

Tower made the announcement alongside its interim financial results. Tower reported an underlying loss, including large events, of $3.3 million versus profit of $5.4 million in March 2022 half year, and a reported loss after tax of $5.1 million versus a $2.9 million profit.

The storm in Auckland on May 9, the latest extreme weather event to hit the upper North Island over recent months, is expected to be a large insurance event costing between $4 million and $6 million, Tower says. It has between $10 million and $12 million in large events allowance remaining in the second-half, and won't be paying an interim dividend.

“Now more than ever it is critical that New Zealand maintains a strong insurance industry for the future. Tower remains focused on careful risk selection and risk-based pricing, which is a fairer way to price insurance as customers only pay for the risks that apply to their property," CEO Blair Turnbull says.

"In 2023 Tower will expand its risk-based pricing model to include landslide and coastal hazards. Advanced selection for landslide risks is already in place across New Zealand."

Tower already has flood and earthquake risk-based pricing in place.

Tower says it has successfully completed "the reinstatement of its reinsurance arrangements" providing important protection from the volatility of large events.

"Tower has cover for any potential third and fourth catastrophe event up to $889 million in the financial year," Turnbull says.

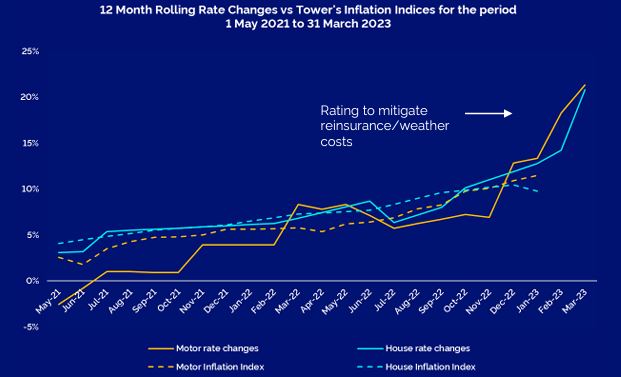

"Tower’s full year underlying net profit after tax guidance remains between $8 million and $13 million, assuming full utilisation of the $50 million large events allowance. Gross Written Premium guidance is between 15% and 20% reflecting organic growth and a strong rating response to address inflation, rising reinsurance premiums and higher motor claims costs. Tower will not pay an interim dividend. A decision on a full year dividend will be made when Tower’s full year results are finalised."

He says about 30% of claims for the Auckland and Upper North Island weather event and Cyclone Gabrielle, and 5% of claims for Cyclones Judy and Kevin in Vanuatu have been completed. Tower is "working efficiently" to settle the rest, with these events "predominantly" covered by reinsurance.

"The cost to Tower for each of the New Zealand catastrophe events is limited to an $11.9 million excess, while the estimated cost of the Vanuatu cyclones is $10 million net of reinsurance recoveries," Turnbull says.

“Tower continues to grow both premium and customer numbers while reducing our expense ratio. We expect to deliver a full year profit along with sustainable long-term growth in revenue and earnings.”

“Investments in technology, operational efficiencies and robust reinsurance continue to underpin Tower’s resilience and ability to address external challenges. We are proactively managing climate related weather impacts through risk-based pricing and product innovations, keeping pace with inflation via targeted rating and underwriting actions and addressing increasing vehicle theft with rating and excess changes," says Turnbull.

Summary of key HY23 results:

• Gross written premium (GWP) $245m, up 15% on HY22

• Customer growth up 5% to 320,000

• Business as usual (BAU) claims ratio 51.6% vs 48.6% in HY22

• Management expense ratio (MER) improved to 35.1% vs 35.8% in HY22

• Underlying net profit after tax (NPAT) excluding large event costs $23.6m vs $18.2m in HY22

• Large event costs $33.9m vs $17.9m in HY22

• Combined operating ratio including large events (COR) 105.3% vs 94.8% in HY22

• Underlying loss including large events $3.3m vs $5.4m profit in HY22

• Reported loss $5.1m vs $3m profit in HY22, including strengthening of the residual Canterbury earthquake and multi-policy discount remediation provisions, partially offset by the sale of Tower’s Papua New Guinea subsidiary and its building in Suva.

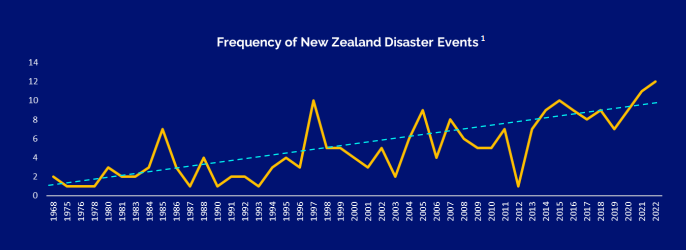

1) Chart above sourced from the Insurance Council of New Zealand.

9 Comments

I do recall it being said - if you can't get/afford insurance, you can't get a mortgage.

As a lot of NZ householders will be finding out.....

OOooooooo climate change - this is sure going to hurt.

Especially if you just paid anywhere close the recent crazy asks on fast disappearing beachfront. Even rocks wont hold the tide for ever.

The only solution is massive expensive sea walls and we simply cannot afford it. Parts of critical roading infrastructure still have not been fixed let alone finding money to build seawalls. People are just going to have to move or risk it with no insurance.

That photo reminds me of the road out by Ngawi.

So when you say 'move' you mean walk away.

Because no one is going to buy the place as the land will be uninhabitable/uninsurable = resale value? $Nil.

Correct, walk or drown its your choice. Huge number of places are also slip prone, built on the sides of hills that should never have been allowed in the first place. Loads of cliff top properties that are accidents waiting to happen. Its pretty obvious to me that climate change is finally here and its pretty dramatic and it should now be the number 1 thing you should consider when buying a property.

Earthquakes, wildfires, tornadoes,cyclones,flooding, as with other parts of other nations there will be areas and/or property that are uninsurable. Add to that households that can’t afford the premiums in the first instance, a percentage of which has been recently revealed, this century anyway, that many might see as surprising. Resultantly New Zealand is facing a decreasing ability for sufficient insurance cover across the board and would wager most New Zealanders have not the slightest idea of the implications involved.

Correct - the consequences for the FIRE economy when the I is the first domino to fall should be obvious but is attracting little attention. Which leaves the state to step in as the insurer of last resort (as has already happened in some parts of the UK and the US). Oh the irony - can you imagine the typical right wing, 'free' market loving, low tax worshiping, big state hating, climate change denier having to put his/her hand out to get rescued by a government funded insurance program for their beach/river side palace? They'll be strangely silent on the hypocrisy of it all when that particular chicken comes home to roost.

Given local government has zoned land that has known hazards as suitable for residential use, it's difficult to see how they can avoid liability - but I'm sure they'll try.

Some years ago I was privileged to see some of the original survey maps for Canterbury, from the mid-19th Century. Large areas along the coast were noted as being unsuitable for housing - but that didn't stop it happening.

What's really bizarre is that local government is held accountable as the last resort with faulty building, because the building enterprises simply go out of business when things go wrong.

Sometimes I wonder about us as a species.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.