Suppose that you had invested your wealth in a broadly diversified set of stocks, starting in January 1871, with the dividends being rolled back into your portfolio, and with your portfolio being rebalanced every January to maintain diversification. If you had also paid no taxes and incurred no fees, you would have had 65,004 times your initial investment, as of this past January. By contrast, if you had performed the same experiment with long-term US Treasury bonds, you would have only 41 times your initial wealth. That is the difference between an average annual inflation-adjusted return of 7.3% for stocks and 2.5% for bonds – 4.8 points per year, or what Rajnish Mehra and Edward C. Prescott called the “equity premium puzzle.”

Of course, neither of these strategies is possible in real life, since one also must pay commissions and deal with the price pressures of rebalancing one’s portfolio by selling winners and buying losers. Taxes, too, would take a big cut. They would be levied on your interest income from bonds, on your realised capital gains from stocks, and – back when stock buybacks were highly disfavoured – on the dividends that you received. Together, these costs would reduce your real return by perhaps one-third, leaving an equity premium for stocks of around 3.2 percentage points per year. That means a stock-market investor could make twice as much as the bond-market investor in 22 years, on average.

Before Edgar L. Smith published Common Stocks as Long-Term Investments in the 1920s, this basic fact about stock and bond investors was not widely known. Most people considered stocks highly “speculative,” because they focused more on the returns from individual stocks and on the high likelihood that any given corporation would fail to maintain its position in the marketplace over time. Betting on individual stocks was best left to gamblers, insiders with special information, or those who truly believed they had special insights into the business cycle. But most retail stock-pickers suffer from the Dunning-Kruger effect (thinking that you are smarter than you really are), which is why their losses have long powered the gains of successful professional equity traders.

This perspective is not incorrect. But while picking individual stocks may be a fool’s game, assembling a large, properly diversified portfolio of stocks is something else entirely. By spreading the risk across companies, one can essentially eliminate it most of the time. Moreover, long-term diversified stock-market investments tend to have other risk-reducing advantages that are missed by investors focused on short-term stock performance of individual companies.

The workings of the semi-regular business cycle mean that low cashflows from a company this year will probably be offset by higher cash flows three, five, or ten years from now. Equally, changes in valuation ratios – the multiple of average expected future earnings and dividends that the market is willing to pay – will also probably be reversed in the future. Hence, it follows that a truly long-term diversified investor should ignore market fluctuations and transitory earnings blips, and simply place his trust in businesses’ long-term profitability.

The success of the diversified, long-term approach to stocks also leads us to ask whether bonds are as safe as they are assumed to be. After all, bonds are extraordinarily vulnerable to inflation, and if there are ever conditions that do substantial permanent damage to business profitability, they will probably derange government finances even more.

Another notable feature of asset markets is that this stock-bond gap has been persistent across the generations. A stock investor ending their 40-year career in 1910 would have accumulated three times more wealth (excluding taxes and transaction costs) than a bond investor, and so, too, would a stock investor ending their 40-year career in 1950, and again in 1990. Past performance is never any guarantee of future results, but it remains the case that in a typical year, business earnings are at least 4% of stock-market equity value, whereas bond investors are lucky if returns are two points above the inflation rate.

If stocks are such a good deal over the long run, why are US stock-market investors not richer? One answer is that some of them are: just look at Warren Buffett’s career. But more importantly, it takes time for the law of averages to work itself out – for “average” to become truly “typical.” If you experience an episode where you lose your entire stake, you will not have time to get it back. Mathematically, your strategy may have had a high expected return. But if you are holding and rebalancing your portfolio from January to January, there could come a year when things go spectacularly wrong. That happened in 1931 and 2009, and it may be only a matter of time before it happens again.

J. Bradford DeLong, a former deputy assistant US Treasury secretary, is Professor of Economics at the University of California, Berkeley, a research associate at the National Bureau of Economic Research, and the author of Slouching Towards Utopia: An Economic History of the Twentieth Century (Basic Books, 2022). Copyright: Project Syndicate, 2023, and published here with permission.

23 Comments

Great article. It’s not so much the time you need back, it’s the capital and balls to have another go. Once it’s gone or significantly less then you may not be able to go again.

It’s also sometimes trust, take Serko for example. Recently they announce their results that were well outside of guidance which means both Management and the Board failed to keep the market informed. What happens to them? Nothing. Probably high fives for the results but anyone that sold prior got screwed. A 40% change in share price and the FMA does nothing.

And while I am at it, I think the biggest fallacy of equities is that the money is productive. The original IPO is, sure, but after that it’s just another for of gambling (like Serko) until the next equity raise comes along.

And while I am at it, I think the biggest fallacy of equities is that the money is productive. The original IPO is, sure, but after that it’s just another for of gambling (like Serko) until the next equity raise comes along.

I wish this was repeated over and over until it's household knowledge

Do you mean that you wish that "do not invest (speculate perhaps) in a single stock/company" was household knowledge?

If so then yes agreed otherwise what do you mean?

I invest in ETFs that include real businesses doing stuff this includes Simplicity who are investing in start ups and building houses, how is this gambling?

You owning the share does nothing for the business, rather you own a portion of it, and are thus entitled to a share of any profits, or the capital gains from share price increases.

E.g.

- Noncents bought a single share for $10k off XYZ ltd in the IPO. (XYZ Ltd received $10k to use in the business)

- Noncents sold their single share 7 years later to Hitch22 for $15k, (Noncents got $15k. XYZ Ltd got nothing to use in the business)

The fact the share price is more, means potentially the company can borrow more against the value of the business. But don't confuse that with investing.

It's still investing, that's part of the consequence of having public ownership of companies.

If there's no potential for future upside, then there's less of a reason to invest. The alternative is companies bootstrap themselves or finance via debt.

I don't have an issue with that practice so much as I have an issue with how companies are now valued, i.e. out of line with their earnings.

The individual buying the shares is investing their money (Although I would still argue gambling, as most are looking for capital gain rather than long term dividend yields). The company is not being invested into though, they never see a cent. So, many companies do use varying sources of debt.

The valuations have always been hit and miss, to value a company based on the worth of it's shares is lunacy. The share price has zero to do with the actual company worth. Companies survive on cashflow, and "report" profit based on a quarterly or annual time period. Take a longer term view and their actual net worth at any given point in time is generally <0 (with a few exceptions).

The company is not being invested into though, they never see a cent.

Investing generally is some sort of acknowledgement of value (or potential for value). A company aims for some level of continuity, otherwise it's less of a company, and more of a limited time transaction, investment need not apply. So the company's value is an integral part of its existence, both today and in the future, and ongoing market recognition of the value can and does allow for a business to continue to invest in its operations/working capital.

Share values have some relation to worth. It's just that the economy and markets are in an ever increasing state of flux, and people are trying more than ever to make forward bets on who the ultimate dominant market players are. That's going to create a large amount of losers.

While not introducing new funds to the business, doesn't purchasing shares 'maintain' the existing level of funding/equity?

The alternative being the business would have to return your investment at face (or market) value a bit like a co-operative such as Alliance Freezing Company returned my investment.

Therefore, Hitch22 in your example has helped XYZ just as you did initially (because XYZ doesn't have to find some cash to pay you out).

If it wasn't possible to sell shares to someone else easily (share market) then that adds to risk and may put some off investment to begin with so XYZ may never have gotten off the ground.

Yes agree. It is true that buying and selling shares on an exchange does not normally inject more cash into a company it certainly allows that to happen relatively quickly and cheaply (e.g. rights issue). More importantly, it lowers the cost of that capital since you have a reasonable likelihood of being able to fully or partially exit should you need to, without stress or haircut. Private equity is more expensive, illiquid and constrained.

Shareholders are also owners of the company and can make decisions on the how the company is run by appointing directors and bringing shareholder resolutions - for example, several have recently pushed for better environmental performance.

Even with bad timing you can do alright with the share market, but dollar cost averaging in a low cost fund is hard to beat.

Check the story of "Bob", the world's worst market timer:

https://awealthofcommonsense.com/2014/02/worlds-worst-market-timer/

Yes time in the market not timing the market. My 60/40 returns suggest things went wrong in 2022...time heals all wounds...

2020 $62100

2021 $78100

2022 -$102100

2023 to date $113700

What about in 1929 in the US or 1989 in Japan? How long did it take to get your money back in real terms? I think unfortunately timing can sometimes be very important - be aware of sequencing risk particularly if in or near retirement.

Sequence of return risk needs to be managed as you approach retirement. If you need the money in the short-to-medium term, then you should move it into bonds or cash. There are different strategies for this e.g. have the same bond % as your age, have 10y of expenses on hand, But even at retirement, you could live for another 30 years (more if you retire early) so a proportion of your investments should be in shares so you don't run out of money.

That is the difference between an average annual inflation-adjusted return of 7.3% for stocks and 2.5% for bonds – 4.8 points per year, or what Rajnish Mehra and Edward C. Prescott called the “equity premium puzzle.”

{kind=link}

Can't blame people for buying houses. They've been a pretty good bet over the years, and the cost of building new ones is always going up. And you get a return, you can live in them or rent them out.

I've been dabbling in shares for decades, still do, it's more gambling than investing, I trade a lot. So many companies go bust, lose fortunes, drill worthless holes in the ground, yet we are implored to "invest" our money in the stock market.

Lots out there are still choking on their losses from 1987 when loose cannons like Alan Hawkins and Ray Smith lost fortunes. Remember those days...classic? Aucklanders were partying downtown, buying new cars, mortgaging their houses and 'investing' in the stock market. All everyone could talk about was how much they were making and what companies they'd bought, until....Black Friday. And then there was Brierley's and Air NZ.....OMG!!! Aunty Helen fronted up with a billion dollars and saved the day.

And you get a return, you can live in them or rent them out.

So living in your own home provides a return.

My understanding of current taxation law is that only the later of the two (rent) is taxed - hardly seems fair.

If you were properly diversified, then the Ray Smiths in your portfolio would be tiny to inconsequential.

How did scoundrels like Smith convince the regulators he had a stack of gold in his safe when he obviously didn't? How did the Air NZ financial crash happen, how did companies that actually did nothing get to list on the stock exchange? When it all finally came unstuck, Smith decamped to Utah with his mistress.

The NZ stock market was the most exuberant on the planet, and when it crashed, it plunged the most. I'll always have visions of Alan Hawkins on TV followed around by his apostles, a collection of sycophants. Then financial 'expert' Hawkins decided to launch a takeover of BHP, like a mouse trying to swallow an elephant.

If you'd bought a house in Auckland 40 years ago, paid off the mortgage and looked after it, you'd be sitting on a fortune, if you'd 'invested' in a selection of NZSX companies 40 years ago, you'd own a selection of colourful, but worthless, share certificates. Robt. Jones Investments, Pacer Kerridge Corp, Brierleys, Equiticorp, Goldcorp...hahaha...fangs for the memories.

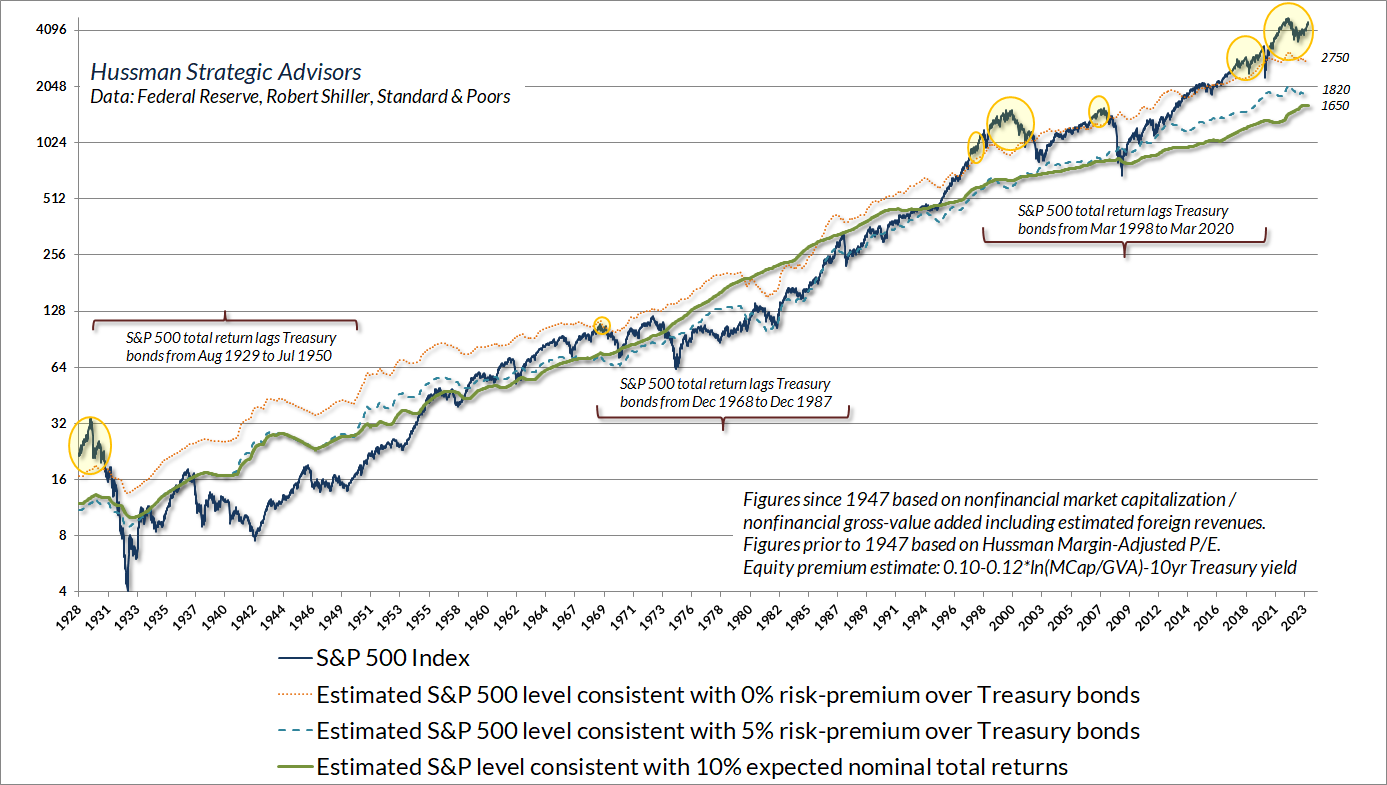

Here's a chart for people interested in investment portfolio theory/risk v return.

It is possible that we are now in a similar era to the late 1920's in terms of the expected 12 year return for a 60/30/10 portfolio of stocks/bonds/cash. i.e. horrendous.

https://pbs.twimg.com/media/F2yrnU0WYAAvFJH?format=jpg&name=900x900

This happens when you steal cash flows from the future (by artificially dropping interest/discount rates) to pump asset prices in the short term.

There's a recession and market pullback coming but that is only a short-term problem. But after every fall comes a rise. If you are investing for 20+ years then you can look through the noise and earn the trend.

Investing shares in NZ is very different (and better) than any other developed country. No capital gains, no wealth tax and many companies with tax free dividends. I have gotten rich by picking 65% winners and 35% losers and will continue to do so. You need to learn to let you winners run and know when you were wrong and sell the losers. Also NEVER take a tip without doing your own DD and never give a tip, so you don't feel guilty when your friend loses money.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.