Table 1: Stable FX ensured similar gold price strength across currencies in December

Analysis by the World Gold Council.

Performance

Gold tagged its 53rd all-time PM price high for the year, reaching US$4,449/oz on 23 December, before closing the year at US$4,368/oz (Chart 1). It was a stellar finish to a stellar year – posting a December return of 4.2% to take the full year return to 67%.

All-time-highs were set in all the major currencies, but with some annual variation in the final return tally due to FX volatility (Table 1).

Attribution

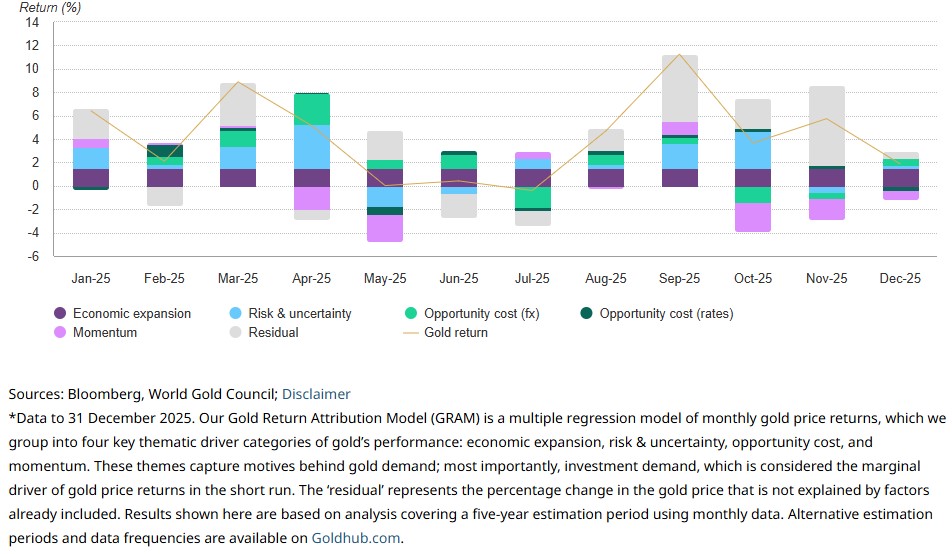

In December, our Gold Return Attribution Model (GRAM) suggested that options activity - a component of risk & uncertainty - was a major contributor to the monthly return, followed by EM FX where US dollar weakening vs the Chinese renminbi (+1.2%) was a key factor. (Chart 2).

For 2025 as a whole, the explicit variables in our model explained c.60% of the FY return, led by geopolitical risk and options market activity, particularly from August to October. A weaker US dollar was also instrumental, led by EM FX. Falling yields provided a slightly smaller but still important boost. See Table 1 on our Gold Outlook 2026 for further details.

Chart 1: Gold has reached 95 new ATHs since 2024

All-time highs in the LBMA PM benchmark price (US$/oz)*

Table 1: Stable FX ensured similar gold price strength across currencies in December

Prices and returns in various currencies

| USD (oz) |

EUR (oz) |

JPY (g) |

GBP (oz) |

INR (10g) |

RMB (g) |

AUD (oz) |

|

| December price* | 4,368 | 3,722 | 22,023 | 3,247 | 132,640 | 973 | 6,546 |

| December return* | 4.2% | 3.0% | 4.7% | 2.5% | 5.2% | 2.6% | 2.3% |

| Y-t-d return* | 67.4% | 47.6% | 66.8% | 55.8% | 74.7% | 57.9% | 55.2% |

| Record high price* | 4,449 | 3,780 | 22,398 | 3,302 | 137,591 | 1,010 | 6,652 |

| Record high date* | 23 Dec 2025 |

23 Dec 2025 |

26 Dec 2025 |

23 Dec 2025 |

26 Dec 2025 |

26 Dec 2025 |

23 Dec 2025 |

*As of 31 December 2025. Based on the LBMA Gold Price PM in USD, expressed in local currencies, except for India and China where the MCX Gold Price PM and Shanghai Gold Benchmark PM are used, respectively.

Source: Bloomberg, World Gold Council

On the flipside, the cumulative lagged gold monthly return was a drag on the full year. This reflects how effectively the gold market self-corrects and balances – even in a bull market – via gold’s dual nature channels of consumer and investor demand. It also contributes to gold’s low average volatility among the commodity complex.

The full-year residual contribution likely reflected some central bank, tariff-related or Commodity Trading Advisor (CTA)/retail activity that the explicit variables did not. In addition, a higher constant - which captures the unconditional mean return after accounting for all explicit factors – likely reflected the persistent demand impact from central banks during the year. We see this as a feature, not a flaw.

Gold ETFs and futures

In December, global gold ETFs managed a seventh consecutive month of inflows, dominated by North American funds, as they had been for the full year. Futures positioning data had caught up by year end showing an increase in managed money net longs of US$11bn (59t) for December, an increase in value of US$8bn but a fall in tonnage by 173t for the full year.

Chart 2: Strong options activity and a weaker US dollar helped drive gold higher in December

Precious metal thunder

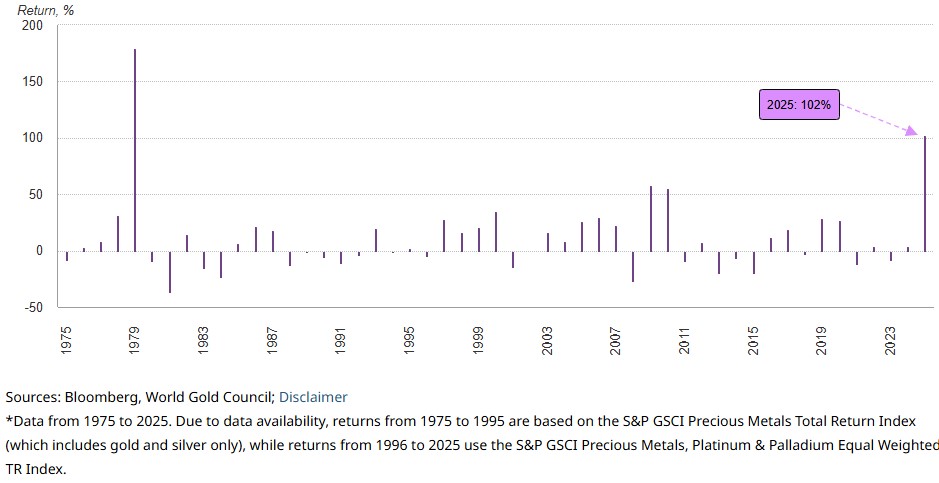

December’s thundering surge across precious metals helped deliver a y/y return for the sector not seen in 45 years (Chart 3) and (Chart 4).

The final leg higher appeared less about an acceleration of structural tailwinds - such as real-asset demand, fiscal concerns or dollar weakness - and more about a policy, and near-market supply squeeze.

Chart 3: Thundering into year end

Chart 4: Party like it’s 1979…almost

Annual return of precious metals*

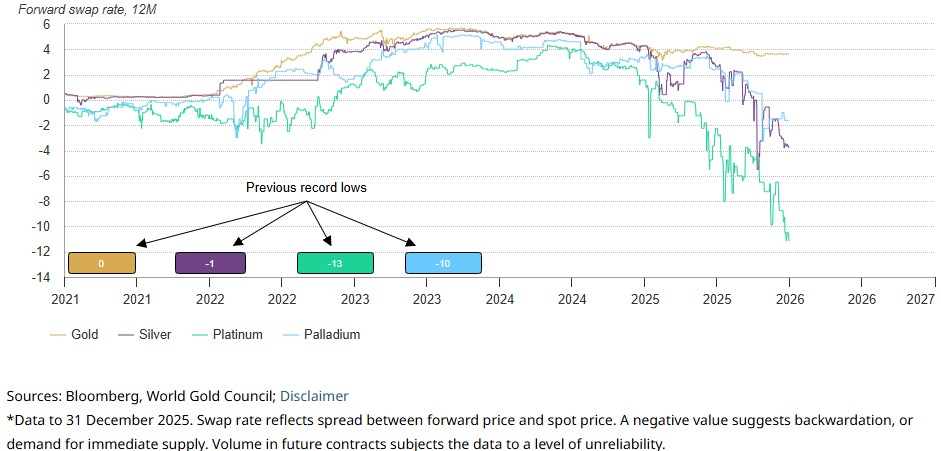

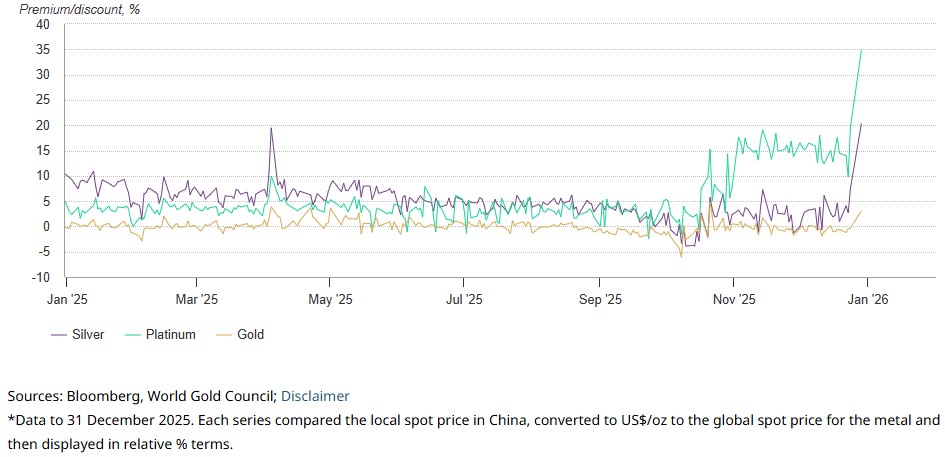

Tariff uncertainty and trade frictions pulled forward investor purchases of physical supply, steepened backwardation (Chart 5), and inflated regional premia (Chart 6), most visible in silver and platinum. China’s announcement on 27 December of export licenses for silver, added fuel to the fire.1

Chart 5: Tenuous signs of tightness, except for gold

Precious metals 12-month swap rates*

Chart 6: China policy on silver a major driver

Chinese local price premium/discount to global price*

Gold continued to move higher in December, but unlike the other precious metals, lacked the hallmarks of a squeeze. This divergence became clear when the seemingly inevitable reversal began late in the month, triggered by raised margin requirements at the CME. The resulting de-risking of leveraged positions, in the context of thin liquidity and year-end tax effects, drove intraday ranges in silver, platinum and palladium to over five times their 2025 average. Gold’s range, by contrast, was just three times its average – a sign of both deeper liquidity and a fundamentally different set of drivers.

While the structural support for gold remains intact, there are near-term channels through which weakness in silver and platinum could briefly propagate: cooling of the ‘scarcity trade’, some rotation into base metals, early-January index rebalancing (post 8 January), and a potential uptick in recycling – particularly in silver, where above-ground stocks are more readily mobilised. There is a small risk this feeds back to gold, which so far has staved off a material rise in price-driven recycling.

That said, the medium-term backdrop for silver – and to a lesser extent platinum – remains constructive, limiting the risk that recent volatility becomes more than a short-term drag on gold’s own story.

Beyond the noise, the signal should emerge

Gold’s support is less dependent on tight physical markets and more on its macro role: sustained central bank demand, hedging demand in a world of policy uncertainty, and diversification demand when stock-bond correlations remain elevated.

Policy could again be the near-term catalyst. The Supreme Court heard challenges to IEEPA-based tariffs in November, with a decision expected in early 2026. A ruling that validates tariffs, barring some short-term relief, would reinforce policy risk and the case for hedging; one that constrains them could compress the policy premium. But tariffs have also provided a partial buffer to the fiscal outlook – and if that buffer is removed, attention is likely to shift back toward deficits and term premia. The effect may be more nuanced for gold, but we believe either outcome could be supportive.

There is also a risk of repricing the Fed’s policy rate path, following the unexpectedly strong US Q3 GDP print.

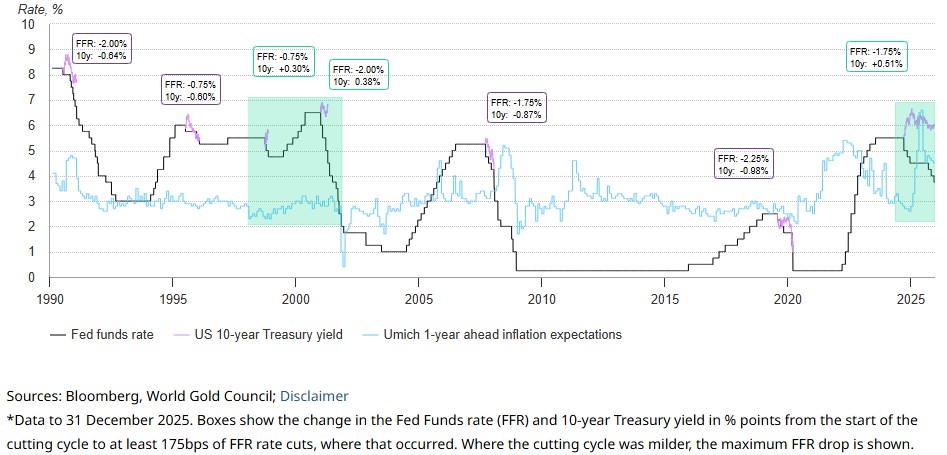

Historically, cumulative Fed cuts of 175bp or more have coincided with falling bond yields; the late-1990s were the notable exception. Today’s parallel lies in optimistic AI-driven growth expectations but with inflation expectations considerably higher. While firmer rate expectations could temper near-term enthusiasm for gold from certain investors, the inflationary implications should remain supportive over the medium term (Chart 7).

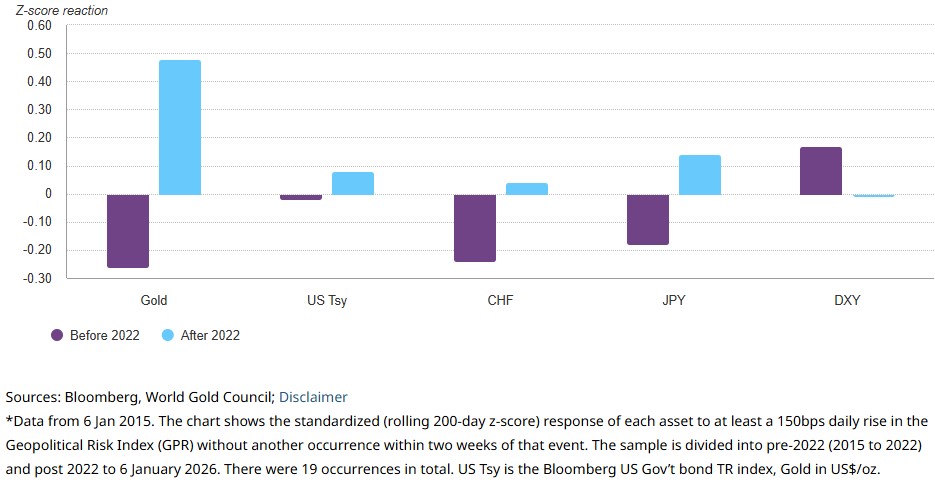

Finally, it is too soon to say what direct and indirect implications of the ongoing tensions in Venezuela and the region will be. Suffice to say that the immediate reaction by assets normally sought during geopolitical spikes is telling. Prior to 2022 – a date selected because it represents both the Russian invasion of Ukraine and the year when the return of inflation was at its worst – the US dollar was on average the main beneficiary of geopolitical spikes. Judging by gold’s reaction this week, it now appears to be the haven of choice.

Chart 7: It is unusual for the 10-year Treasury yield to rise after so many policy rate cuts

In addition, our analysis shows that there is a direct connection between gold and geopolitics. In the short term, a 100pt increase Geopolitical Risk Index translates into 2.5% increase in the gold price. The long-term effect depends on the persistency of the event and the knock-on effects it can have on other key macro variables such as the inflation, rates, and the USD.

Chart 8: Gold now the geopolitical safe-haven of choice

Standardised (z-score) reaction to geopolitical events*

In summary

The December rally underscored the divergent dynamics within the precious metals complex. While silver and platinum were propelled by acute physical tightness and policy distortions, gold’s rise was more a function of market spillover than a shift in its own fundamentals. As those distortions unwind, gold’s resilience – rooted in macroeconomic concerns and structural demand – is likely to reassert itself.

Looking forward, the interplay between policy risk, inflation expectations, and investor positioning will shape the path ahead. With the white metals resetting and gold’s core drivers intact, the stage is set for a recalibration of narratives – and potentially, a reversion to gold’s leadership.

Geopolitical events that reverberate globally have been a frequent feature over the last few years. While those events tend to be short-lived, partly due to the wavering focus of media, they seem frequent enough to raise the general level of investor anxiety – read risk premia. Gold has undoubtedly benefited both during the short-lived spikes and from the climate of elevated nervousness. There are few indications that the status quo will change in the foreseeable future.

Our Gold Outlook 2026 reviews how gold may perform over various macroeconomic scenarios, depending on the ultimate development of global macroeconomic and geopolitical conditions.

Footnotes

1. Based on the BCOM Precious Metals Subindex Total Return as of 31 December 2025.

This article is a re-post from here.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here.

Comparative pricing

You can find our independent comparative pricing for bullion and coins in both US dollars and New Zealand dollars which are updated on a daily basis here »

World Gold council thinks Gold is a good investment.

Why is interest.co.nz giving them a promotion platform, or is this unlabeled advertising?

Gold/Silver has been the outstanding asset class of 2025 and will likely be so in 2026 as well, imho.

So more independent and industry news and articles on precious metals, the better.

We wont hear nothing from the NZ funds or general finance industry, as they simply cannot milk it.

Being an indendant thinker, with the best info inputs, is important!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.