The following is a Special Topic in the latest (March 2020) Monthly Economic Indicator report from Treasury. The original is here.

With the onset of the global COVID-19 pandemic, the economic outlook has become increasingly uncertain. Despite the uncertainty, it is becoming more likely that New Zealand will see a deeper economic contraction in the June quarter than we have seen in our recorded history. Global spread of COVID-19 has already severely curtailed activity in New Zealand's services export sectors. The move to Alert Level 4 in New Zealand put most of the country in lockdown for a number of weeks. This will have an unprecedented impact on economic activity. Government support, including wage subsidies, increases in welfare benefits, business tax relief measures, the business finance guarantee scheme and industry support packages will cushion the impacts on households and businesses.

As restrictions are lifted, we expect economic activity in many sectors to bounce back quickly. Some though, including those exposed to international markets will take longer, possibly years, to recover. The recovery will also depend on the ability of the governments of our trading partners to limit the spread of the virus and restore the confidence in their economic outlook.

In this special topic we look at the possible impacts of COVID-19 on the New Zealand economy, describing the likely transmission channels and possible size of impacts we may see.

The situation is rapidly changing ...

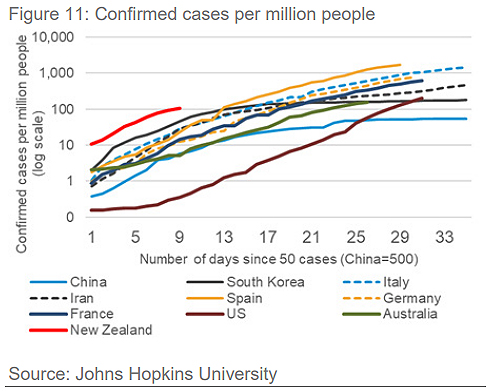

The number of COVID-19 cases globally is rising exponentially. It took around three months to reach the first 100,000 confirmed cases; the next 100,000 took twelve days, and the next just three days. On 19 March, the cumulative number of deaths registered in Italy exceeded deaths in China as the epicentre of the virus shifted from Asia to Europe and the United States. As of writing, there were 1,346,566 cases worldwide, and 74,697 deaths. The number of confirmed and probable cases in New Zealand stands at 1160 as of 7 April (Figure 11).

Activity will be weaker …

The move to Alert Level 4 in New Zealand put most of the country in lockdown for a number of weeks. Given the spread of the virus and the accompanying social distancing measures taken to save lives, the resulting shutdown of New Zealand businesses will constrain economic activity in a way never seen before. This analysis provides a rough guide based on our current understanding of essential services and the nature of COVID-19 transmission.

Under the current classification of “essential services”, “accommodation and food services”, “trade” and “construction” components of GDP are likely to be particularly affected, while the public (education, health, and central government agencies) and primary sectors will be less impacted.

Forecasting sharp downturns

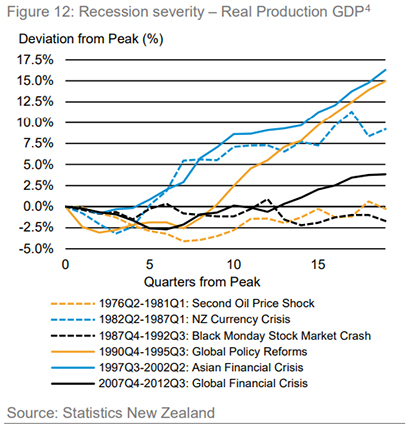

Another way to assess the possible impact of COVID-19 is to look back at past recessions as a guide. What we learn from reviewing past recessions is that economic downturns are inherently difficult to forecast as the typical economic relationships may not hold. This makes forecasting models less useful, and increases the reliance on professional judgement. We also see that in past recessions annual growth typically declines by less than 5% and activity recovers to post-recession levels within eight to twelve quarters (Figure 12). The measures to combat the spread of COVID-19 will curtail activity more acutely than we have seen in the past.

Transmission channels of COVID-19

The pandemic is creating a combination of supply and demand shocks to the economy, with complex interactions between the two.

Demand shock

Demand shocks arise from global and domestic travel restrictions and social distancing measures, resulting in lower tourism and non-essential consumption of both goods and services. Higher consumer and investor uncertainty and weaker export demand abroad lower aggregate demand further through lower investment and consumption.

Social distancing measures will have direct impacts on activity in the short run, but if successful in limiting the spread of the virus, will have benefits in the long run. The more stringent the “social distancing” measures, the greater the impacts will be in the short-run, but also the lower the infection and death rates, lowering the adverse long-run effects of the pandemic on New Zealand’s economic activity.

Weaker demand for New Zealand’s exports of goods and services

Recent data shows a sharp fall in tourist arrivals to New Zealand, while goods exports are expected to weaken in the face of falling international demand. Prices for many of the commodities New Zealand exports will also decline as demand weakens. It will take some time for this to turn around.

Lifting the border controls for tourists is unlikely to result in a quick resumption in arrivals as we may anticipate that travellers would be cautious about travelling abroad until the global pandemic has been controlled. The depreciation in the New Zealand dollar, as investors shift into safe haven commodities and currencies, will provide a partial offset.

Consumer confidence lowers private consumption

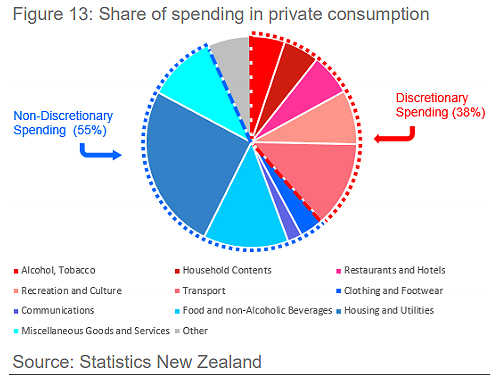

Discretionary spending, which includes non-essential purchases like restaurant meals, recreation and motor vehicles, is expected to fall sharply due to the ongoing measures to limit the spread of COVID-19. Discretionary spending makes up around 38% of private consumption (Figure 13). Nondiscretionary spending, which includes essential purchases like food and housing, makes up around 55% of private consumption and is forecast to remain fairly stable.

Supply shock

Much of the decline in activity due to COVID-19 is likely to come from weaker demand. And the supplyside of the economy, including the effective labour force, will also be adversely affected.

The reduction in demand will directly flow into the labour market, particularly due to the near-total shutdown of the tourism sector in the near term. A high share of employees in the tourism sector tend to work on casual and temporary contracts.

The closure of non-essential businesses will also have direct impacts, although the wage support measures that have been announced will lessen the effect of weaker demand on unemployment. Forced work closures, sicknesses, and caring for others will result in fewer hours worked. If the labour market outlook remains weak for a long period, job hunters will leave the job market as they believe their chances of being hired are low as more job seekers chase fewer jobs. This will lower the labour force participation rate.

Production in some sectors like agriculture and horticulture will continue, and won’t be as adversely affected by the downturn in demand. Agricultural sector jobs, including primary manufacturing are considered essential, and will endure.

As more long-term and permanent migrants arrive into New Zealand than leave, restricting people’s movement will result in lower net migration. Migrants are more attached to the labour market as they tend to be younger than the average Kiwi. A reduction in migration will therefore impact adversely on labour supply and lower demand, particularly in sectors like housing.

The policy response will mitigate the shock

The impact of the initial shock will be cushioned through monetary and fiscal policy, although this may have a limited impact on activity while social distancing measures remain in place. Supportive macroeconomic policy will play a significant role in influencing how the recovery period will play out.

Although interest rates are near zero, the Reserve Bank’s quantitative easing programme will provide support to the economy through lowering long-term interest rates.

The New Zealand government’s low net debt provides capacity to increase spending to mitigate the impacts of the pandemic on both the supply and demand sides of the New Zealand economy.

Highlighted in the recent fiscal stimulus packages are allocations of funding towards wage subsidies and provision of guarantees for working capital support. The measures are intended to decrease the likelihood of business failures, maintain household incomes and support attachment to the labour market. These are expected to lower the impact of the pandemic on business and consumer confidence and underpin a quicker recovery.

Note:

4. Hall, V. B. & McDermott J C. (2016), Recessions and recoveries in New Zealand’s post-Second World War business cycles. New Zealand Economic Papers, 50(3), 261-280.

48 Comments

"This makes forecasting models less useful, and increases the reliance on professional judgement.". That's code for "We are guessing"

"Lifting the border controls for tourists is unlikely..." That's all that needs to be said on that topic. The rest of the sentence "..to result in a quick resumption in arrivals as we may anticipate that travellers would be cautious about travelling abroad until the global pandemic has been controlled." is irrelevant.

"The depreciation in the New Zealand dollar, as investors shift into safe haven commodities and currencies..." Maybe. But won't the NZ$ be one of those safe-haven currencies? I reckon there's every chance.

"As more long-term and permanent migrants arrive into New Zealand than leave,... will result in lower net migration." Someone explain that to me! Unless by "lower net migration" they mean "lower net emigration".

"A reduction in migration will therefore impact adversely on labour supply and lower demand, particularly in sectors like housing.". But the start of this paragraph suggests "As more long-term and permanent migrants arrive..." All too confusing!

Yes you are so right ….just a lot of theoretical B.S ...

I did some contract work for a government agency a few years back. I had some interactions with Treasury.

Technically clever people, but oh so wedded to their models and neo-liberal paradigms. And almost no real-word understanding.

Very limited.

Confusing for a reason.

Have a look at this.

https://youtu.be/zeF2rkyxDIo

Good video. The bit at 10:15 sums it up - the three tenants of being an American worker; of being a human being.

Countries that rely heavily on foreign money are in the most trouble. This trouble will be doubled if the country has high levels of personal debt.

Gold is the money of kings, silver is the money of gentlemen, barter is the money of peasants – but debt is the money of slaves...

This downturn is resulting in less strain on the environment.

And remember my fellow rapacious primates, our economy is a subset of the environment.

For a moment, the bulldozer of exponential GDP growth has “thrown a rod”.

I suggest the bright sparks at Treasury think of how we transition to a sustainable economy rather than trying to restore the BAU growth trajectory.

Think for a moment how a "sustainable economy" will impact those who have leveraged themselves to the hilt expecting the growth trajectory to make them wealthy in the long term.

Aren't we all just being taught a valuable lesson in how little mother nature cares about "leverage"? If we don't move to sustainability, she's just going to hand us our arses again.

" Sharp Global Downturns will Shock our Economy'...

Happy realization.....still cannot imagine the damage after .......

Not completely related to this article, but here's Robert Shiller's take on things using data over the last 40 or so years:

https://www.nytimes.com/interactive/2020/04/10/opinion/coronavirus-us-e…

Gives an insight as to how/why things aren't heading in the right direction in the US - probably equally related to a lot of the western world.

One more from Shiller - more around the behavioural finance/psychology for the US stock market.

Interesting to note that prior to the recent fall, the US market was almost at 1929 valuations based on his CAPE ratio (cyclically adjusted price/earnings ratio). Dotcom bubble is the only time with greater valuations. Long term average CAPE is 17. We're still above that even after the recent fall.

https://www.nytimes.com/2020/04/02/business/stock-market-predictions-co…

Anyone looking at CAPE is being optimistic because the denominator looks backwards. Its forward earnings you need to worry about right now. The price people are willing to pony up for earnings is psychological and changes over time, but the actual earnings change too. The price people are willing to pay has taken a hit because animal spirits are dead, and people pretty much know the bull run is over. Earnings haven't collapsed yet but they will. Lets see how shares do when earnings are next announced.

It's unclear to me what areas they think will 'bounce back quickly'

Law and accounting?

Insolvency and restructuring?

Drug supply

Construction, cafes, fast food and films. Other areas will get an unexpected boost eg gardening, fruit and veg and demand for health products as people improve their state of health. Construction is a govt led initiative and the area most labour intensive is residential work over high-rise or roading. They know something you dont?

Kurt Schlicter in his usual coruscating form - ripping the economic illiterates a new one.....

A small sample:

“Cancel rent.” Okay, rent is canceled. Gone! No paying rent! Yah!

Wait, where did the lights go? Power’s out. Wait, you mean that miserable miser is not fronting cash for utilities anymore since you’re, you know, not paying rent? Hey, there’s a plumbing leak! You can just call…oh…awkward! Well, then you can just refuse to pay…oh, right. Well, then maybe you’ll sue your landlord for not doing the things landlords should do, though you are not doing things tenants should do. Oops. He’s bankrupt. Hear that? It’s a sad trombone.

But that’s only at the personal level. Our economy is interconnected. You don’t pay rent, so your landlord doesn’t pay his loan and all those people who used to manage the property. All those guys he used to pay, his bank, the gardener, the power company. Now, they can’t pay anyone anymore. And pretty soon no one can pay anyone anymore.

Congratulations! It’s a depression!

We've been deliberately let down by a raft of leaders & for a long time now. This perfect storm didn't just happen over night. It's been brewing since 2007 that i can work out, & probably goes back to the Asian Crisis/Y2K/SARS period before that & there is an argument that Clinton's arrival as POTUS distracted us from our daily doings enough for China to get up to global speed while we were watching Monica Lewinsky & co. Another key leadership failure is that of he United Nations. It has been hijacked by our very own anti-capitalist left wing(h)ers in association with the biggest thugs that rule the most terrible countries that you can imagine. If we're to save anything out of this the UN has to be disbanded. Immediately. Look at Mr Ethiopia at the head of the WHO. A no-hoper if ever there was one. He's just another thug. If the Republicans cannot hold it together, and they are just about on their own when you look around (Europe derrrr) then we are headed towards chaos of unimaginable proportions. Dear I mention Armageddon? No okay I won't. The thugs have got nothing to lose. Get rid of the Old Yank Tanks & the rest is easy. Chaos rules ok? Shit, I hope I'm wrong.

Long John Martin gets the award for Edgelord of the Day.

What an absolute failure John Key was. We deserved better.

Agree on the failure but "we" voted him in three times. Perhaps it's our failure.

That "failure" and Bill English put NZ in a fiscal position to weather the Covid crisis better than practically every country in the world. I'm sure you'll credit the current gormless wonder, who is likely to use Covid as an excuse to to trash that same economy.

BS. I think you should google up the graph of government debt over the last 40 years. I love showing it to die hard Nat voters that spout the same nonsense. And keep in mind when you are looking at the explosion of government debt when the marvelous JK was in charge, that he achieved that while at the same time flogging off the assets. And also have a look at how much sales commission his mates charged to sell those assets. You won't believe it. He should be in jail.

https://tradingeconomics.com/new-zealand/government-debt-to-gdp

Shows that debt both grew and fell under governments of both colours. The 4th National government took over in 1990, just before the highest peak, handing over a great downward trajectory to Clark and Cullen. The previous Labour government took debt from 30 to above 50% of GDP. Put aside the JK hate.

The period of time leading into Clarks government losing power was the "golden weather" (but in truth a flawed and dishonest global financial period) where all the world grew madly and Cullen salted money aside for a rainy day, but also grew the percentage of government spend to GDP to very high levels.

They handed over to National in a GFC, together with Chch Earthquakes. "10 years of deficits" were forecast by treasury. So yes, the Nats borrowed and spent on infrastructure, and gradually returned the economy to growth and decent surplus to howls of indignation of the opposition.

So what will happen with debt under this government? Labour spent an $8bn 2018 surplus, running back to deficit and increasing the debt to GDP headroom. Now they will be borrowing more than ever before (circa $50bn of $310bn current economy) so add 16-20% of GDP of debt, and look at the graph now.

When the human body goes into shock, it often has quite subtle signs before things start really collapsing and having multi organ failure. I hope we are not taking the economy too much for granted, because we cannot afford to experiment on civilisation as we know it.With loss of goodwill between nations, what next?

What comes next is a world war.

Ray Dalio has been talking about that for the last few years. Comparing recent past to the 1930's - if one country feels like it gets a bad deal out of all this as it unfolds...watch out. Especially if there are a lot of unemployed yet motivated citizens.

Trade imbalance

Financial crisis

Currency war

Trade war

Hot war.

Each step leads to the next. Where are we currently?

Talk about state the obvious, but missing the answers to the real questions. To qualify for the wage subsidy, a business needs to show a drop of 30% compared to the same month last year, but for virtually all tourism, we are talking a 100% drop, and the wage subsidy doesn't even come close to helping avoid business failure. It just kicks the can down the road. Isn't that what we have been doing for the last ten years.

We introduced a tourist tax, great idea, but too little and too late, and now all those tourists have gone, and we missed a great opportunity. If anyone has travelled in Europe, any time in the last 20 years,you would has seen the tourist tax on every receipt, like the cost for looking at the view, and we gave it away year after year, for nothing. Please don't make that mistake again.

all Covid is telling me is how poorly the Key Govts repsonded post GFC, Euro Zone meltdown and Chch quakes...we stayed depressed for 10 years because that government did...nothing. This is true leadership that we are seeing from the current crop. V impressive.

Was there an act of War from China with this Covid virus? This economist says so. 5 minute clip and explaining why.

https://www.youtube.com/watch?v=c47KVyz0Gsg&feature=youtu.be

It's time to wheel out the greatest economist of all time: Mr Micawber from Charles Dickens' "David Copperfield". Micawber said:

"Annual income 20 pounds. Annual expenditure 19 pounds, 19 shillings and sixpence; result happiness."

"Annual income 20 pounds. Annual expenditure 20 pounds and sixpence; result misery."

Nothing more to say. It's really that simple.

Sounds like ponzi yields. No margin for error.

"Annual income 20 pounds. Annual expenditure 19 pounds, 19 shillings and sixpence; result happiness."

"Annual income 20 pounds. Annual expenditure 20 pounds and sixpence; result misery."

Let's take it a step further. These are some of the questions business owners and employees should ask themselves:

1) what happens if there is a recession or unexpected shock like a natural disaster?

2) how much could income / revenue drop in a such an event?

3) how much is needed in a cash emergency fund to cover expenditure in the event of an unexpected loss in revenue? how many months of expenses should be allowed for?

a) 1 month?

b) 3 months?

c) 6 months?

d) 12 months?

e) Other?

Each person and business will have their own answer to suit their level of risk tolerance.

I read one comment by a property investor that if they had a sufficiently sized emergency fund, then that was also sufficient to use as a deposit to buy another investment property.

There is wisdom in the adage "hope for the best, prepare for the worst". Many people and businesses read only the first half of the adage and "hoped for the best". They forgot or failed to read the second half of the adage - "prepare for the worst."

For many businesses and employees, many have insufficient emergency funds for a rainy day and now that rainy day has arrived.

Your question about the required size of a rainy day fund is more relevant than ever. I would argue that based on even at 30% equity for another property, that an emergency fund is not enough to last more than a couple of years. Remember also we are working off some overinflated prices for property Some are saying five years, some in tourism are saying it will never get back to where it was.

I speak to a lot of people about various kinds of investments, and they all talk about the principal of leverage, and yield, but have no idea about the effect of leverage on risk. Who encourages them into more risk than they can handle? more often than not, its the bank manager or their accountant.

NOT, when as forecast by all Blue teams (Banks, Nat co.) - our heavy China backup, will save us. Trust us! - Just unsure, at what 'price' for NZ being saved again by them. Last time we knew the worldwide GFC, deferred by QE upon QE (until now), then the easy Far East money to lift up the OECD GDP numbers, by RE procurement, then it's people movement.. in preparation of mass scale 'magic weapon'..Alas Covids

The China idea is nice, yet nz does have a slight problem. We are married to 4 other nations in a way which the country may not believe. The 5 eyes make up a very important part of the western fabric. Escaping that hold, to turn to China, maybe not as easy as we think. The biggest trading partner for EVERY country on the planet is China. Think about the impact of that. Even they will have to prioritise who they trade with, as things begin to recover.

I don't think China is going to be in anybody's good books going forward after the CCP virus.

We should have nothing to do with them.

Good luck with that.

"likely that New Zealand will see a deeper economic contraction in the June quarter than we have seen in our recorded history."

No sheet sherlock. Its fascinating that they did not use the R word and later in the article they talk of the mitigation effect. With 40000 kiwis flying in since 20 march that adds up to a lot of extra demand. That sounds like a big demand for accommodation and the numbers of available rental properties available is also continuing to drop. Let's wait and see the effect I hate to say it but pass the popcorn.

Evolution. Its not the virus that's the big issue, it the massive over reliance on debt that has everything strung out down to the bone like junkies. Hope the govt implements some new financial policy's to avoid NZ being taken to the cleaners again by the financial over leveraging class.

How much is the government going to pay immigration agents in India to keep them on the books until the "all-clear" is given.

The 'Berlin Airlift' style to revive NZ supply by it's allied Master, has just begun:

https://www.stuff.co.nz/business/industries/120973641/coronavirus-predi…

As the Bluey team (political+banks), indicated NZ should open soon for 'direct investment/people movement' again from the mainland China to allow 'revolving door of Funds' to sustain the current F.I.RE economy - Investment/people move in again,retain F.I.RE GDP, then re-sell to the next incoming people movement into the country/continual Investment..this is the only way to ensure the 'magic weapon' able to work.. $ to buy the ruling elite, allow 'investment' further, therefore allowing further people movement (student, tourist, restaurant workers, other hospitality), to do the United Front works of motherland, injection of growth funds=injection of more people in=more money for the F.I.RE gdp numbers, No One shall able to resist the power of money.

Just a note: China moves the funds via local/OZ banks, other worldwide channel, also competing for those funds; Canada, UK, USA & other OECDs - which beg a dumb question, why won't they do that in other world countries of non-anglo Saxons club? go figure ;-) ...all rosy until..this Corona You!

Orr has said he's not going to do a knee jerk, couple days later the rest is history. Now this is my frequent reminder, for readers:

- DGM = Doom, Gloom Merchant - always stating the obvious precautionary, sensible measures.

- BGM = Bright, Glitter Merchant - always negating any sensible measures, leave it to greedy market.

Even the 'selfish brigade' old argument of Supply vs Demand also pondering the equation, how the hell we're going to inject upward trajectory growth graph, without demand? ans: NZ duffrunt, Any respective govt at the helm? is the one that 'will create the ANI(Artificial Non-Intelligent) demand'side of equation.

Happy Easter everyone, .. around 1.5 week more to go.. should be enough time to read this;

https://www.scoop.co.nz/stories/HL1507/S00101/the-fire-economy-new-zeal…

Here's the video link, from her.. 5years ago! - Red team initiated, then followed by Blue team bought by direct support link to CCP; enjoy...

https://www.youtube.com/watch?v=MGrBCtOt4Qs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.